How big is the risk of rolling over trillions of urban investment bonds across the country?

Text丨Wuji

BT Finance original article

During the Spring Festival, an article about “local infrastructure debts of more than 60 trillion yuan” caused quite a stir in the financial circle. The article shows that the total balance of urban investment bonds across the country has reached a terrifying 65 trillion yuan, which is equivalent to 30 Evergrande. Based on a population of 1.4 billion, each person needs to share an average of 46,400 yuan.

There is a view that urban investment bonds are only one step away from the explosion of thunder, while others believe that urban investment bonds are thunderous and rainy, not only will there be no thunder, but housing prices will still rise moderately.

As we all know, urban investment bonds have always been inseparable from the infrastructure and real estate industries. On January 16, three listed companies of the Evergrande Group replaced their auditors and provided two sets of debt extension plans to foreign creditors, with a maximum of 12 years to pay off all debts. Such a long debt extension is already rare in the industry. Compared with previous The 20-year extension period of the Zunyi Road Bridge in Guizhou that has been exposed is still insignificant.

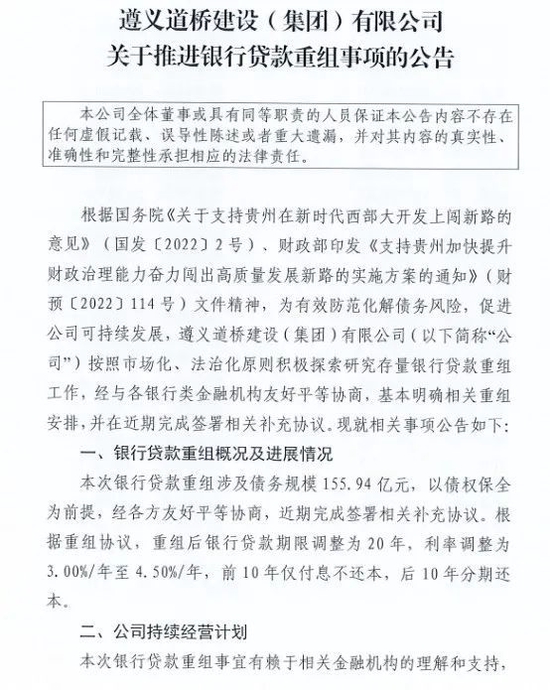

On December 30, 2022, Zunyi Daoqiao, the largest urban investment company in Zunyi City, Guizhou, announced that 15.594 billion yuan of bank loans will be extended for 20 years, and the interest rate will be adjusted from 3.00%/year to 4.50%/year. What surprised the market is the first ten years Only the interest is paid but the principal is not repaid, and the principal is repaid in installments in the next ten years, setting a new record for debt extension.

What happened to the city investment debt?

How much is the city investment debt?

What is the current balance of urban investment bonds across the country? I’m afraid no one knows for sure.

According to an article during the Spring Festival on “local infrastructure debts of more than 60 trillion yuan”: “In 2021, the balance of interest-bearing debts of my country’s urban investment platforms will reach 56 trillion yuan. In the past 2022, the total scale of urban investment debt may It has reached 65 trillion yuan.”

The basis is that, according to the report of the Financial Associated Press, as of the end of November 2022, the balance of local government debt across the country will reach 35.0 trillion yuan, and the balance of urban investment debt is usually about twice the explicit debt of local governments. The balance of interest liabilities has reached 65 trillion. Of course, these calculations are based on the statistics of formal urban investment bonds that have been publicly issued, and the total amount of urban investment bonds should be far greater than the official debt.

In fact, Chengtou’s interest-bearing debt is not equal to standardized Chengtou bonds. The total amount of debt including bonds, bank loans, and non-standard financing (such as trusts, asset management plans, factoring, and some financial leases) is included in the interest-bearing debt of urban investment, not just government urban investment debt. Among them, non-standard financing includes trust, factoring, asset management plans, and some financial leases.

According to the data analysis of Everbright Securities, as of the end of December 2022, the balance of my country’s existing urban investment bonds is 13.91 trillion yuan. According to Pengbai News, the latest urban investment bond market analysis report of Lianhe Credit pointed out that as of the end of the second quarter of 2022, the remaining balance of urban investment bonds is 14.15 trillion. Assuming that all rights-containing bonds choose to exercise their rights, the total scale of urban investment bonds due in the third quarter is 1,091.378 billion yuan.

Liu Kun, Minister of Finance, mentioned in an interview with Xinhua News Agency: “As of now, the ratio of the national government debt balance to GDP, which is commonly referred to as the debt ratio, is lower than the internationally accepted 60% warning line, and it is also lower than the At the level of major market economies and emerging market countries, risks are generally controllable.”

It should be noted that data from the Ministry of Finance Data Center of China Statistics Network shows that in 2021, my country’s government debt accounts for 47% of the annual gross domestic product, while that of the United States is as high as 133%.

What exactly are urban investment bonds?

It can cause shocks in the financial circle. In fact, many people don’t even know what urban investment bonds are.

According to public information, Chengtou Company is the abbreviation of Urban Construction Investment Company, which is an investment and financing platform for the governments of major cities across the country. Chengtou was established not long ago. In 1991, the first urban investment company in Shanghai was established only for more than 30 years. At that time, the urban investment company was mainly jointly established by the financial department and the construction committee. The company capital and project capital were allocated by the finance department, and the rest were borrowed from banks with financial guarantees. At that time, the city investment company was only the carrier of the government’s investment and financing platform and had no assets of its own. The disadvantage of this model is that once there is no financial guarantee, because it has no assets, it will be unsustainable.

After the “Guarantee Law” was fully implemented in 1995, local finances could no longer provide guarantees for Chengtou, and Chengtou’s debts soared, reaching the verge of bankruptcy.

The financial crisis in 2008 brought a turning point for Chengtou. In the second half of 2008, after the government’s stimulus policy of 4 trillion yuan to rescue the market was introduced, various commercial banks announced their active support for key national projects and infrastructure construction. At this time The city investment company has ushered in a golden period of development. Through the allocation of assets such as land, equity, fees, and government bonds, companies that can quickly package assets and cash flow that can meet financing standards. When necessary, supplemented by financial subsidies as a repayment commitment, in order to achieve the purpose of assuming various funds, and then use the funds for municipal construction and other projects.

Chengtou’s business covers a wide range, including water supply, power supply, gas supply, heat supply and other urban infrastructure related to the national economy and people’s livelihood. In terms of public transportation, Chengtou has great power, including expressway project investment and operation, railways, ports, docks, Airport and other capital construction operations, rail transit capital construction operations, urban transportation capital construction operations, etc. And many of these are money-losing businesses, such as subways and high-speed rails.

Many of Chengtou’s projects are public welfare projects, such as urban greening and landscape lighting. These investments that burn money without return will inevitably lead to continuous accumulation of debts. However, Chengtou is backed by local governments and has government credit guarantees. Urban investment companies can use various channels for financing or borrowing, almost all of which are non-public debts. At the same time, Chengtou issued related private placement bonds through financial institutions such as trust companies and securities companies. It was difficult to make profits only by borrowing, causing Chengtou’s debts to snowball.

Therefore, urban investment companies have a wide range of borrowing channels and sources of funds. In addition to conventional bank credit loans, an important way is to issue bonds, which are generally non-public debts of exchanges. In the past few years, urban investment companies also raised funds through trust companies and securities companies and other financial institutions to issue trust plans and asset management plans, and some urban investment companies also conducted private placement debt business through local equity exchanges. Due to the relatively strong financing ability of urban investment companies, the debts of urban investment companies are also increasing. Only then did Zunyi Daoqiao fail to repay the bank’s 15.6 billion yuan loan.

Because of the background of Zunyi Daoqiao, the borrowing bank finally extended the loan for 20 years and halved the loan interest. The 20-year repayment period is also divided into two parts. The first part is the first ten years, only interest is paid, and the principal is repaid year by year in the next ten years.

As the largest urban investment company in Zunyi City, Zunyi Road and Bridge’s financial situation continues to deteriorate. The bond interim report shows that in the first half of 2022, Zunyi Road and Bridge’s total revenue was 673 million yuan, a year-on-year decrease of 36%, and its net loss was 286 million yuan. In the first half of 2022, the interest-bearing debt of Zunyi Road and Bridge is as high as 45.858 billion yuan, which is much higher than the 15.6 billion yuan of the 20-year extension period. The remaining 30 billion yuan is how to repay the extension period. It is not shown in the announcement, but if Based on their annual income of less than 700 million yuan, even if they no longer borrow in the future, it will take more than 90 years to pay off all debts. Judging from the current annual income, it cannot even cover the interest generated by interest-bearing loans.

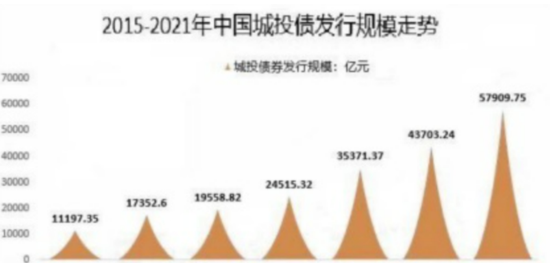

Zunyi Daoqiao’s debt of 45.858 billion yuan is only one of 20 urban investment debts in a prefecture-level city in Guizhou, and there are hundreds of urban investment companies like them in China. What worries the outside world is that, judging from the growth rate of urban investment bonds in the past seven years, the total liabilities of urban investment bonds are still increasing.

The Butterfly Effect Caused by Zunyi Road Bridge

Taking the interest-bearing debt of Zunyi Road and Bridge as of the first half of 2022 as an example, the balance of bank loans is 16.448 billion yuan, accounting for 35.87% of the balance of interest-bearing debt. The 20-year extension of 15.6 billion yuan accounted for 95% of the bank’s total interest-bearing debt.

The specific creditor Zunyi Daoqiao has not disclosed, but it can be seen from the cooperative relationship with the bank mentioned in its report that China Merchants Bank, Agricultural Bank, Bank of Communications, Bank of Guiyang, and Bank of Guizhou may all be creditors.

During the reporting period, the balance of credit bonds of Zunyi Daoqiao Company was 19.671 billion yuan, accounting for 42.90% of the balance of interest-bearing debts, of which 3.52 billion yuan of corporate credit bonds were due or resold by the end of 2022; loans from non-bank financial institutions were 7.283 billion yuan. RMB 100 million, accounting for 15.88% of the balance of interest-bearing debts; the balance of other interest-bearing debts was 2.456 billion yuan, accounting for 5.36% of the balance of interest-bearing debts.

During the same period, the company’s book monetary funds continued to decrease, only 601 million yuan, a decrease of about 45% from the previous period, and 95% of them were restricted assets. The cash and cash equivalents at the end of the period were only more than 30 million yuan.

According to the report of Zhongzheng Pengyuan, since the second half of 2022, Zunyi Daoqiao has added more information on persons subject to enforcement. As of December 15, 2022, the company has 158 information on persons subject to enforcement, mostly due to overdue debts and guarantees dispute. Just on December 7, 2022, Zunyi Daoqiao was listed as the executor because a 400 million yuan trust loan was overdue, and the applicant was Bairui Trust.

Although the 20-year debt extension of Zunyi City Investment is only 15.6 billion yuan, this amount is insignificant for Guizhou, which has a total GDP of 2.02 trillion yuan in 2021, but they have had a very far-reaching impact, like triggering a butterfly effect. Now Zunyi City Investment’s 20-year extension loan has almost triggered a “tsunami” of urban investment bonds.

In fact, as early as July 2018, the first non-standard default of urban investment in Guizhou broke out. This opened the prelude to the debt default of Guizhou Urban Investment and also caused market concerns. In 2021, there were 23 non-standard breaches of contract in Guizhou City Investment, involving 18 cities.

The continuous exposure of defaults has greatly affected the issuance of Guizhou Urban Investment Bonds. In 2018, only 50.5 billion yuan was issued, and the final net financing was -17.7 billion yuan. It is typical to borrow new debts to repay old debts. In 2020, mainly due to loose bond issuance during the epidemic, net financing rose to 47.6 billion yuan. However, in 2021, due to the tightening of policies, the issuance of Guizhou urban investment bonds will drop to 69.4 billion yuan, and the net financing will be negative again, at -2.3 billion yuan. The 20-year extended debt of Zunyi Road and Bridge was generated under such a general environment.

Affected by the extension of Zunyi Daoqiao’s debt default, it is unknown whether urban investment companies in other cities will follow suit. Once many urban investment companies like Zunyi Daoqiao come to a 20-year extension, the impact on banks will be Bigger than ever.

There are not a few urban investment companies with high debts and insolvency like Zunyi Daoqiao. According to incomplete statistics from Huaan Securities, as of December 31, 2022, 31 urban investment companies have overdue loans, interest arrears or extensions. There are 31 urban investment companies located in 12 provinces, of which 2 have venture loans exceeding 6 billion yuan, and 6 have venture loans exceeding 2 billion yuan.

According to data from the China Banking Regulatory Commission, as of June 30, 2022, the total assets of all banks in China are 3.448 million yuan, and the 65 trillion liabilities of urban investment companies account for 19% of the total assets of banks. Even if all banks are not in trouble, It will also cause many banks to fail.

Is the decline in land transfers the source of the crisis?

The state’s macro-control of the real estate industry has led to a continuous decline in land transfer fees.

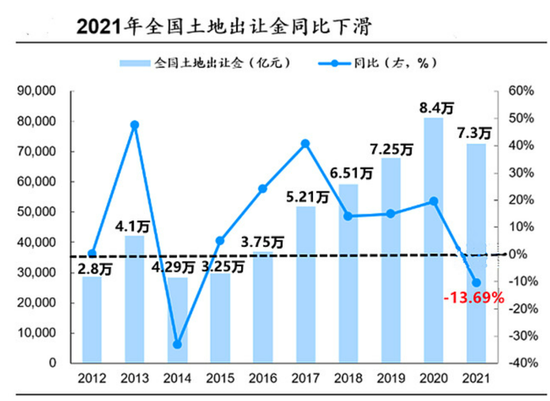

According to WIND data, the national land transfer fee in 2021 will be 7.3 trillion yuan, while the land transfer fee in 2020 will be 8.4 trillion yuan, a year-on-year decrease of 13.69%. This is the first negative growth since 2014. Only Beijing, Jiangsu and Tianjin have positive growth in the country, and the rest of the provinces have negative growth. Among them, the negative growth in Guangdong is higher than the national average, reaching 15%, while the negative growth in Yunnan and Hainan is more than 60%. .

From 2015 to 2021, the average annual increase in interest-bearing liabilities of the 11 sample urban investment platforms in Zunyi reached 23.483 billion yuan, while the average annual increase in local GDP in the same period was only 32.783 billion yuan. 72% of the increase has brought heavy financial pressure to the local government.

According to public reports, in 2021 there will be an overall decline in land transfer fees across the country, and Zunyi City is no exception. It will further decline in 2022. In the first half of 2022, the total land transfer fees in Zunyi City will be 8.337 billion yuan, a year-on-year decrease of about 19%. There is still a downward trend in half a year. It is estimated that the land transfer fee for the whole year is only about 16 billion yuan, while the interest of Zunyi City Investment Bonds will be as high as 16.7 billion yuan in 2022. The total land transfer fee cannot cover the interest of interest-bearing liabilities. Further trigger the debt risk of urban investment bonds.

“The money owed by the city investment company to the bank is not a big problem, and it is not difficult to extend the period, but the city investment bond not only involves the bank, but also other investors. It is difficult for these investors to accept the 20-year repayment method. If these problems are not resolved, The risk of urban investment bonds will be magnified.” Financial analyst Wang Yiran believes that it is easy to roll over bank loans, but it is not easy to roll over non-bank debts. “In the past, urban investment bonds may have placed hope in real estate, but the real estate industry is also struggling. In the third quarter of 2022, the balance of real estate development loans was 12.67 trillion yuan. Based on this data, the total debt scale of the real estate industry is about 90.5 trillion yuan. It is obviously unrealistic to hope for a real estate recovery.”

Who will bear the debt?

The debt of Zunyi Daoqiao was extended for 20 years, and the bank silently undertook it all.

However, there are Internet big Vs who believe that in the face of bad debts, banks have a set of effective and mature solutions, and banks can pass on risks, and they may even profit from it.

Internet celebrities pointed out that taking Zunyi City Investment Bonds as an example, the final extension period is as long as 20 years. Only interest is repaid in the first ten years, and principal and interest are repaid in installments in the next ten years. It seems that the pressure is on the bank, because the problem that the bank is facing is that, judging from the current development of urban investment bonds, it is unlikely that urban investment companies will be able to repay the money after 20 years. What if the money cannot be recovered after 20 years? manage? Obviously, banks will not sit still. For this kind of long-term debt, banks usually use accounts receivable as the underlying asset, and package this debt into a security to sell to retail investors. MBS is the most typical example. The essence of MBS is a security with mortgages receivable by banks as the underlying assets.

According to public information, banks provide mortgage loans to home buyers, and home buyers need to repay the loans on time. For banks, the mortgages repaid by installments by home buyers are accounts receivable, and these accounts receivable are the assets of the bank. Banks then cooperate with financial institutions to issue securities with these assets as the underlying assets. This type of securities is MBS. If an investor purchases MBS, the underlying asset purchased is the account that the bank will collect in the future. If home buyers repay the mortgage normally, the bank will have the money to redeem the MBS purchased by investors. Once a large-scale home buyer defaults, it will be difficult for the bank to have the money to redeem the MBS of investors. There are also certain risks.

The 20-year extension of urban investment bonds is also considered by investors to be similar to repaying housing loans. They are paid in installments over several decades, and the cash flow structure is basically the same as that of housing loans. However, it is important for banks to transfer risks in the form of MBS. , or a good choice.

It is undeniable that the continuous accumulation of local debt, especially the disorderly expansion of hidden debt, may increase the risk of local government debt under the condition of weaker growth expectations, and needs to be guarded against.

However, some scholars believe that the “large scale” and “high risk” of local government debt are two different things. Under the expectation of sustained economic growth, the accumulation of debt will not cause the risk to intensify. Under the circumstances of the impact of the epidemic and the intensification of foreign political and economic uncertainties, the macro economy is under the triple pressure of demand contraction, supply shock, and weakening expectations. We are facing huge challenges, but this is all staged.

Throughout the history of development, the essence of Chengtou’s debt issuance is for development. The money owed in the past few decades can be maintained as long as it is converted from non-standard bids, replaced by low interest rates with high interest rates, and repaid with new loans. “Debt-Investment” -growth” mode can also be benign and continue to roll down.

(Disclaimer: This article only represents the author’s point of view, not the position of Sina.com.)

This article is reproduced from: https://finance.sina.com.cn/tech/csj/2023-01-29/doc-imycvatx2755873.shtml

This site is only for collection, and the copyright belongs to the original author.