On December 19, 2021, I published a long article ” Make a 2021 Lost Fund Portfolio “, planning to make a solid fund portfolio from the 10 worst performing mixed funds in 2021, and look forward to some performance in 2022. And on December 28, 2021, they respectively issued the article ” “2021 Lost Fund Portfolio” has started to build positions! “, January 2, 2022 ” “2021 Lost Fund Portfolio” firm offer opening! “. (For the above three articles, you can directly click on the title to read the original text)

Now that 2022 is a thing of the past, will the 10 bottom-performing funds in 2021 perform as expected in 2022 and achieve a performance reversal as scheduled?

The performance of the “2021 Lost Fund Portfolio” in 2022 is listed below:

“2021 Lost Fund Portfolio” annual performance return -23.87%, underperforming the Shanghai and Shenzhen 300 Index (-21.63%), still “lost”! No performance reversal was achieved . Seven of the 10 funds underperformed the Shanghai and Shenzhen 300 Index.

The best performer was Guo Jie’s “E Fund Reform Dividend Mix”, with a yield of -6.67%; Luo Chunlei’s Nuoan Theme Selection Mix and Liu Yanchun’s Invesco Great Wall Dingyi Mix, with -13.38% and -14.81% respectively. name.

The three worst-performing funds all fell by more than 30%: Eastern Emerging Growth Hybrid, Southern Innovative Economy Flexible, and Qianhai Open Source China’s scarce assets, with yields of -37.93%, -31.08%, and -30.35% respectively.

The initial principal of 30,000 yuan will only be 22,838.18 yuan by the end of 2022, with a loss of 7,161.82 yuan.

According to the plan, the funds of this combination will be replaced with the funds with the lowest performance in 2022, and the name of the combination will be changed to ” 2021-2022 Lost Fund Portfolio “.

1. 2022 Lost Fund Screening

The 2022 Lost Fund screening criteria are essentially the same as in 2021:

1. According to the classification of Wind funds, a total of 2,010 funds were selected from 7,264 mixed funds that underperformed the Shanghai and Shenzhen 300 Index (that is, the annual performance in 2022 was lower than -21.63% );

2. From the 2010 stocks that underperformed the Shanghai and Shenzhen 300 Index, screened out the funds established for more than 5 years (that is, established earlier than January 1, 2017), a total of 718;

3. From the 718 stocks that have been established for more than 5 years, select the current fund manager to manage the fund for more than 1800 days (about 5 years) , and ensure that the medium and long-term performance of the fund is obtained by the current fund manager, a total of 252 stocks;

4. Select funds with excellent long-term performance from 252 funds, set the condition that the five-year cumulative performance return is greater than 100% , to ensure that the fund manager has the ability to achieve performance reversal, and the remaining 20 funds.

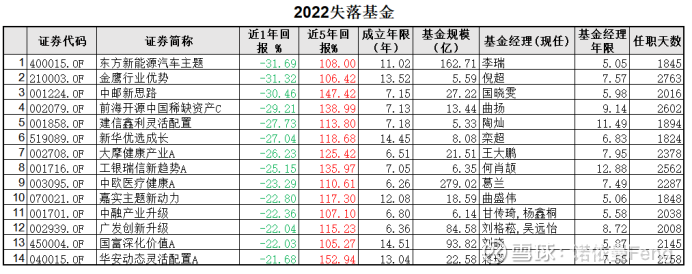

5. Only one of the funds managed by the same fund manager is selected, and the funds whose fund size is less than 100 million yuan may be liquidated are excluded, and the funds are arranged in ascending order according to the performance return in 2022. The list of 14 funds is as follows:

From the list above,

The ” Qianhai Open Source China Scarce Asset C ” managed by Qu Yang is impressively listed, not because of anything else, but because it is included in the “2021 Lost Fund Portfolio”. Qu Yang is the deputy general manager of Qianhai Kaiyuan Fund Company. He is known as the ” all-around master ” of public funds. After three years of high light in 2018-2020, he has fallen from the altar and fell to the bottom of the performance in the past two years.

Liu Gesong is the 2020 annual performance champion. The 2022 performance of the ” Guangfa Innovation and Upgrade ” under his management underperformed the market, falling -22.04%, and entered the “2022 Lost Fund” list.

Ge Lan, known as “Sister Ge “, was once one of the four “top 100 billion” in the public fund industry, and her management scale in 2021 exceeded 100 billion. In 2022, Ge Lan and the other three “Top One Hundred Billion Players” Zhang Kun, Xie Zhiyu, and Liu Yanchun will all be defeated at the same time. Liu Yanchun has been included in the “2021 Lost Fund Portfolio” in 2021, and Gu Lan will continue in 2022. The performance return of ” China Europe Medical and Health A ” managed by him is -23.29%.

Guo Xiaowen of China Post Fund is a master at timing, earning trading income with high turnover, and continues to achieve outstanding performance. She has long been heavily involved in the military industry, and is known as the ” Military Goddess “. In 2022, the performance of the ” China Post New Ideas ” managed by it was appalling, falling -30.46%, disappointing investors.

Tao Can , who calls himself “Brother Volcano”, is a veteran of public offering funds. He has worked in the industry for more than 15 years and has served as a fund manager for more than 11 years. The performance of the masterpiece ” CCB Xinli Flexible Allocation ” in 2022 -27.73%, unfortunately fell into the ranks of “lost funds”.

Luan Chao is an excellent Mesozoic fund manager who has grown up in recent years. He has been a fund manager for less than 7 years. He is a typical growth fund manager. He has achieved good performance in the bull market. He once won a “Golden Bull” and three “Stars”. The grand prize can be said to be low-key luxury. ” Xinhua Selected Growth “, which has been managed by it for more than 5 years, even if it fell sharply by -27.04% in 2022, it unfortunately fell into the “2022 Lost Fund List”. The cumulative performance in 5 years can still reach 118.68%, which shows its past glory.

Different from Luan Chao’s “growth style”, Liu Xiao , who is also an excellent fund manager in the Mesozoic era, has a typical “value style”. Low, the stocks are scattered, the industry is scattered, stable and restrained. Its “National Wealth Deepening Value A” performed “lost” in 2022, down 22.03%;

Qu Shengwei , the manager of Harvest Fund, is a typical reverse investment style. It is a bit unexpected that he will fall into the “lost list” in 2022. Because when I participated in the “Fund Manager Research Group” organized by Xueqiu to interview him in early September, the return of ” Harvest Theme New Power ” was around -5.20%. At that time, the Shanghai and Shenzhen 300 fell by about -18.90%, which was still a good excess return. Looking at the trend of its net worth, it is true that it has fallen all the way in the fourth quarter.

2. Add the “2022 Lost Fund List” to the “2021-2022 Lost Fund Portfolio”

According to the portfolio strategy, regardless of the performance of the portfolio, all funds in the 2021 Lost Fund Portfolio will be redeemed and replaced with the selected “2022 Lost Funds”.

Since there are only 14 funds screened out, it is planned to include all the funds in the list into the portfolio to form a new “2021-2022 Lost Fund Portfolio”. The new portfolio consists of 14 funds and distributes funds equally. in,

》”Qianhai Kaiyuan China’s scarce assets” will be directly transferred from the 2021 portfolio to the new portfolio according to the weight, and the remaining part will be redeemed;

“The “Oriental Emerging Growth Hybrid” with the worst performance in 2021 will be converted into the “Oriental New Energy Vehicle Theme” of the same company with the worst performance in 2022 according to the weight, and the rest will be redeemed;

“The remaining 8 funds will all be redeemed on the first trading day in 2023 (it has been redeemed today), and new funds will be purchased.

》The “2021-2022 Lost Fund Portfolio” list and investment amount are as follows:

(Costs involved in redemption, the actual investment amount will be slightly different)

3. Is the performance of the “2021-2022 Lost Fund Portfolio” worth looking forward to in 2023?

At present, the market is at the bottom, and the impact of the epidemic will be greatly reduced in 2023, and the speed of economic recovery will be accelerated; most institutions predict that A shares will have a good upward market.

So how will this “2021-2022 Lost Fund Portfolio” perform in 2023?

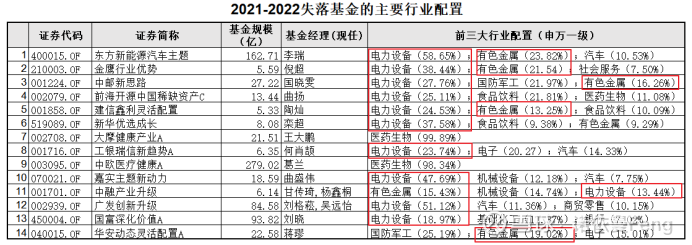

Let’s take a look at the industry configuration of this combination:

Of the 14 funds, except for the two pharmaceutical-themed funds, the remaining 12 funds are all heavily loaded in the “new energy” (electrical equipment + non-ferrous metals) track without exception.

(This is the main reason for the “lost” in 2022, right?)

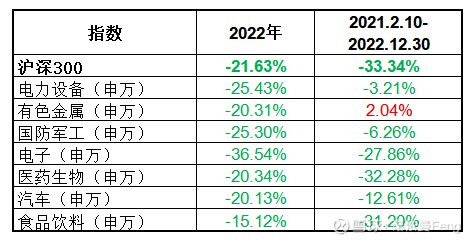

In 2022, power equipment (Shenwan) fell -25.43%, underperforming the Shanghai and Shenzhen 300 by about 4 points; non-ferrous metals (Shenwan) fell -20.31%, slightly better than the Shanghai and Shenzhen 300 index;

From the perspective of February 10, 2021, when the A-share market began to decline, the CSI 300 Index fell by -33.34% by December 30, 2022, while power equipment (Shenwan) only fell -3.21%, and non-ferrous metals (Shenwan) fell by -3.21%. million) rose 2.04%, the risk has not been fully released, and the industry is still overvalued.

There is a high probability that medical biology, food and beverage, and electronics will rise in tandem with the broader market in 2023; however, there are uncertainties in electric equipment, non-ferrous metals, and national defense and military industries in high-prosperity tracks.

Therefore, the performance of the “2021-2022 Lost Fund Portfolio” in 2023 mainly depends on the trend of the “new energy” sector .

(full text)

( Note: 1. The content of this article only represents my point of view. It can only be used for reference. It does not constitute investment advice. It cannot be used as a recommendation or guarantee for buying, selling, or subscribing securities or other financial instruments. 2. Comments are welcome for criticism and discussion. 3. Information and data source: Wind financial terminal; my actual operation data)

@雪球创作者中心@今日话话@雪球基金@球友福利@ETF 星向官

This topic has 1 discussion in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/3179670287/239149085

This site is only for collection, and the copyright belongs to the original author.