The first trading day of 2023 passed quietly, and the Hang Seng Index ushered in a “good start” for the Hong Kong stock market with a 1.96% increase. Looking back on the past time, from March 2021 to October 2022, Hong Kong stocks have experienced an 18-month bear market decline, which happens to be the length of a wave cycle. attractive.

In 2023, how should the opportunities and risks of the Hong Kong stock market be dealt with? How should we look at the outlook for the first half of 2023, and even the whole year? This article will conduct some analysis on these issues and give some opinions. The opinions do not constitute investment advice and are for reference only. I hope that in the new 2023, we can learn from each other and achieve the goal of asset appreciation from each other.

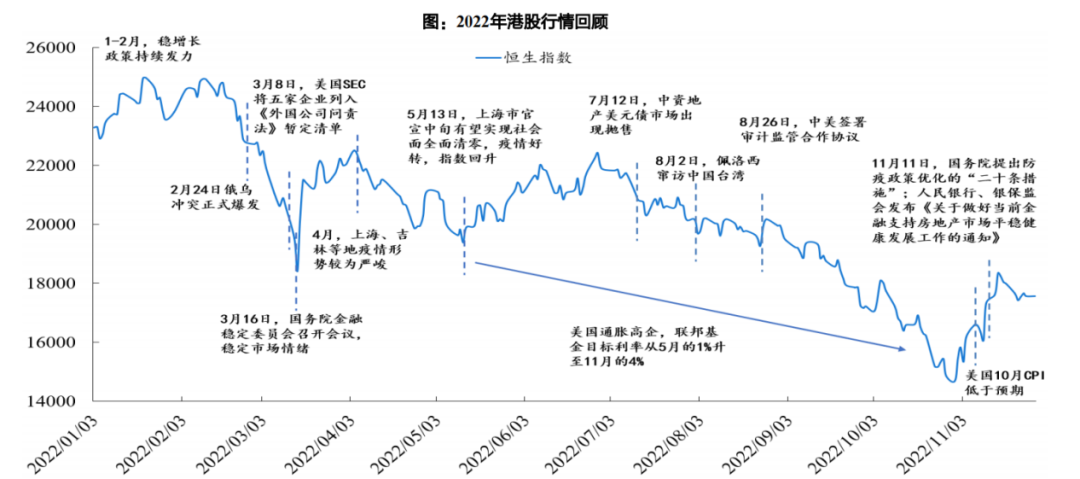

01 Review: The global economic downturn suppresses the liquidity of Hong Kong stocks

From the perspective of valuation, the Hang Seng Index’s valuation will drop by more than 50% from 2021 to 2022. The magnitude and duration of the decline are rare in history, which also makes Hong Kong stocks currently in an oversold position. The valuation is low. Compared with the European and American markets with high inflation and high valuations, the Hong Kong stock market, which has experienced continuous corrections, currently has a higher margin of safety.

(Photo source: Sealand Securities)

2022 will be a year of severe pressure for the world. Leaving aside the repeated domestic epidemics, the most serious incident is the military conflict between Ukraine and Russia. This conflict that exceeded expectations and has continued to this day has led to high global inflationary pressures, including damage to various fields such as commodities, finance, and shipping, making countries have to make adjustments. As a result, major central banks have raised interest rates since March to tighten liquidity and launch fiscal stimulus policies, which have increased downward pressure on the global economy.

The most representative of these is the Fed’s aggressive interest rate hike policy six times this year, which will cause the U.S. to raise interest rates by 375 basis points in total in 2022, thereby affecting the violent fluctuations of the U.S. dollar in disguise. Since most commodity assets in the world are currently settled in U.S. dollars when they are in circulation, changes in the U.S. dollar have impacted the entire capital market, and rapid interest rate hikes have triggered large fluctuations in the global economy and financial markets, which will also continue to put pressure on the Hong Kong stock market in 2022 , the valuation contracted and declined.

The reason why Hong Kong stocks will continue to weaken in 2022 can be attributed to two aspects. One is that the strong contagiousness of the Omicron mutant strain has led to the closure of many important economic cities in China. And market confidence has taken a toll. The second is because there is a certain correlation between the Hong Kong dollar and the U.S. dollar itself. Against the background of violent fluctuations in the U.S. dollar, Hong Kong stocks are facing severe liquidity pressure. It can be clearly felt that the new Hong Kong stocks in 2022 lack liquidity, and it is difficult for the stock price to have upward momentum.

02 Current: Policy improvement plus economic recovery boosts valuation

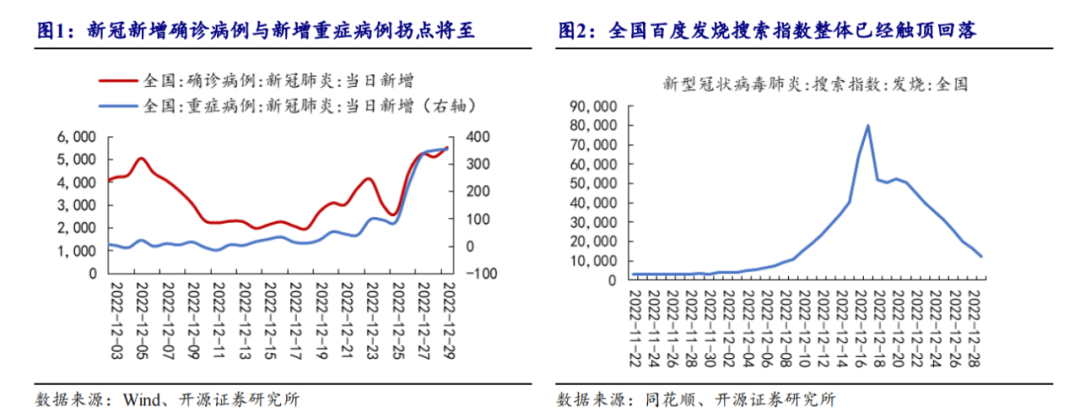

Among the recent changes, the optimization of policies related to the epidemic has been repeatedly mentioned. In the short term, the liberalization of the epidemic has increased the number of infected people and affected residents’ willingness to travel and consume, but in the long run it will undoubtedly be good for consumption. From the perspective of high-frequency data, as of December 29, the number of new daily confirmed cases and the number of new severe cases of the new crown in the country are still on the rise but have tended to slow down. Monday’s 66.27% dropped to 8.09%, indicating that the number of incremental individuals infected by the epidemic is gradually decreasing, and the epidemic is gradually peaking.

According to reports, the new crown virus infection will be classified as “Class B and B management” from January 8, 2023. Hong Kong and overseas returnees will no longer need full nucleic acid testing and centralized isolation after entry. After three years of traffic control, it is the first time that the real sense of “letting go” has been ushered in. The resumption of normal customs clearance between Hong Kong, Macau and the mainland will not only benefit the consumer market in the mainland, but also drive local consumption in Hong Kong and Macau, especially the improvement of the business of Macau’s gaming sector companies and Hong Kong’s local retail listed companies.

In terms of specific valuation growth, the author cannot give an accurate calculation answer, but it is foreseeable that under the premise that the overall economic recovery in 2023 is relatively optimistic, the current Hang Seng Index is obviously underestimated, and the corresponding expectations The price-earnings ratio is expected to recover upwards. As the two major factors that have dragged down economic growth this year, the repeated epidemic and the downward trend in real estate, the slowdown in the pace of interest rate hikes by the Federal Reserve has also cleared the obstacles for the restrictions on the liquidity of Hong Kong stocks. The overall valuation of the Hong Kong stock market in 2023 Value restoration is expected.

03 Outlook: 2023 focus on several mainline opportunities for Hong Kong stocks

When it comes to the topic of the recovery of the Hong Kong stock market, there must be a “leader”, that is, the industry/stock with the most advantages and the most violent recovery in the valuation restoration process of the Hong Kong stock market. In previous articles, the author has repeatedly mentioned opportunities related to consumption recovery after the epidemic, and this view has not changed. At present, both consumer confidence and actual consumption data in China are at the bottom. Under the continuous optimization of epidemic prevention policies, consumer confidence is expected to improve, and leaders in pharmaceuticals and biology, food and beverage, social services, gold and jewelry can all benefit from it.

In addition to consumption, the author believes that the current “advantage” of Hong Kong stocks that is different from the A-share market is the Internet technology companies in the Hong Kong stock market. The existence of domestic Internet giants including Tencent, Meituan, JD.com, and Alibaba is the most noteworthy part of the valuation restoration of the Hong Kong stock market. Internet technology companies play an irreplaceable role in promoting the real economy, and the digital economy will also promote the deep integration of the real economy. After several years of anti-monopoly, the current valuation of Internet technology companies has also been adjusted back. With the recovery of the Hong Kong stock market in 2023, the valuation restoration of Internet technology companies is worthy of attention.

On the other hand, since November, “exploring and establishing a valuation system with Chinese characteristics” has become an opportunity point of common concern for the Hong Kong stock market and the A-share market. Since the reform of state-owned enterprises in 2016, the profitability and profit growth rate of state-owned listed companies have improved significantly, but the positioning of state-owned enterprises has kept their valuations in a low state. In the context of economic downturn and policy guidance, follow-up listings The state-owned enterprise sector will develop in the direction of improving value perception, and it is also expected to become one of the main lines of the Hong Kong stock market in 2023.

However, it should be noted that Hong Kong stocks with a short-selling mechanism pay more attention to the performance of listed companies than A-shares. Therefore, in the first quarter and the annual report window period, there is a high probability that the logic of expected improvement will be converted to the logic of performance realization, and in 2022 Due to the downturn of the overall economy, many companies whose performance cannot be realized are at risk of stock price fluctuations. During the period, there may be no shortage of companies that have achieved high valuations in the recovery market.

At the same time, due to a certain lag in economic recovery, if the Hong Kong stock market realizes a valuation recovery in the spring, then after entering the performance window period, the Hong Kong stock market may face the possibility of a correction due to the lack of an upward catalyst. Therefore, the Hong Kong stock market in 2023 It will not be smooth sailing, and the probability of showing an “N” or “W” trend is higher. During the period, there will be an objective rise, and there may also be a large retracement. This will be the normal state of the Hong Kong stock market in 2023.

This article comes from the WeChat public account “Mangu Jinglun” (ID: MGJL2022) , author: Mangu Jinglun, 36 Krypton is authorized to publish.

media reports

Sina interface 36Kr

related events

- 2023 Hong Kong stock market outlook, some analysis of Hong Kong stock trends and opportunities2023-01-03

- CICC: It is expected that more qualified Chinese stock companies will return to Hong Kong stocks2022-08-15

- Tianqi Lithium’s Hong Kong stock market broke on the first day of listing2022-07-13

- Aneng Logistics is about to enter the capital market2021-10-30

- China Unicom’s Hong Kong stock rose to 15%, with a market value of HK$ 160 billion2020-08-13

This article is transferred from: https://readhub.cn/topic/8mgd2l3bCNn

This site is only for collection, and the copyright belongs to the original author.