#雪球星图# The first part of Conch is more about thinking on a high-level strategic view. The second part is actually a simple financial analysis, and the most important valuation and transaction landing, which is the conclusion everyone has been asking about in the last part. This conclusion It was made 3 months ago, but the price decline mentioned in it (although I don’t know how it fell) did happen later, so everyone should think about whether this price decline is a periodic weather factor or cement. A violent price war begins, which dictates the timing of the trade. Out of the conch business world, and then into the mist of Mr. Market. Many people will make an absolute judgment on a company, whether it is good or bad, but all companies are intertwined with positive and negative, and in the end they show weights rather than a single judging factor.

financial analysis

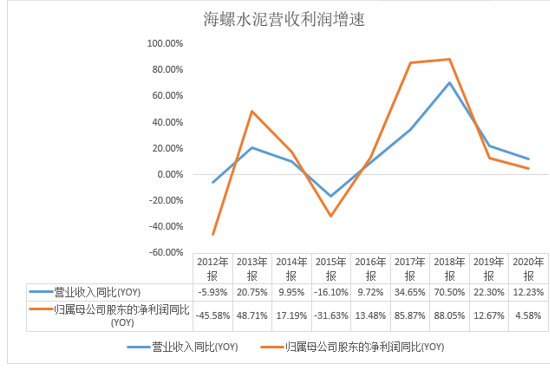

The first is the growth rate of Conch Cement’s revenue and profit, which can be said to be very good. Except for the negative growth caused by the decline in cement prices in 2012 and 2015, the others are all positive growth. In 2017, due to the industry supply side reform, the company has obtained The fastest growing period, so the growth of cement companies is closely related to cement prices.

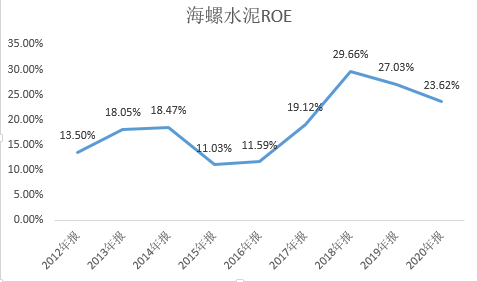

The return on equity of Conch Cement also started from 2017 to the highest point of 29.66%, and then we split it to see where the contribution of ROE came from

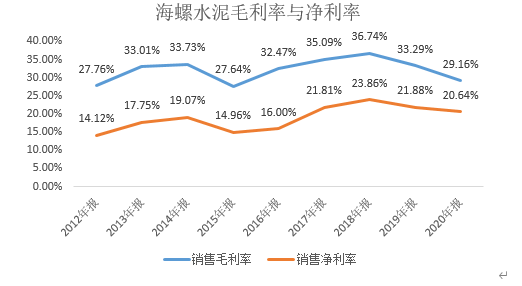

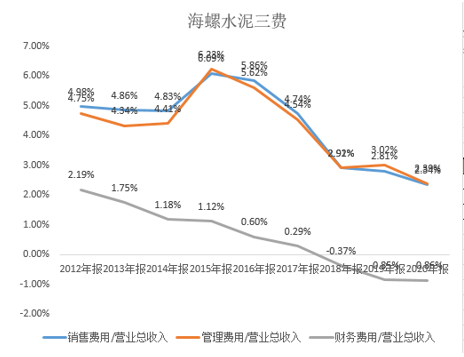

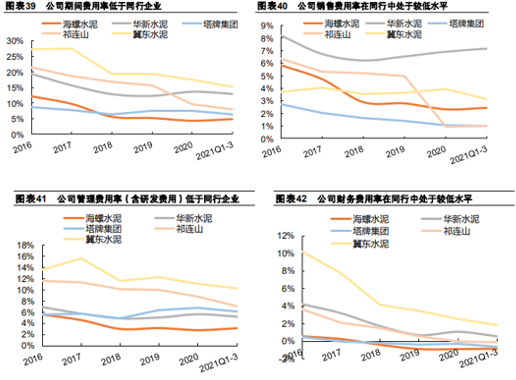

First of all, from the perspective of the first net profit margin, the increase in ROE is partly due to the increase in gross profit margin, that is, the increase in cement prices, and the high gross profit margin of Conch Cement compared to the same industry is also in the forefront, not only The high gross profit margin brought by cement prices is also brought about by the strong cost advantage of Conch Cement. The net profit margin is also superimposed on Conch Cement’s declining three fees, and its cost management and control capabilities in the entire industry are in the forefront. It can be said that Conch Cement’s profitability is the result of the resonance of cement prices, cost advantages, and strong internal operation capabilities. It is the strongest in this undifferentiated industry. Behind the excellent figures are excellent people.

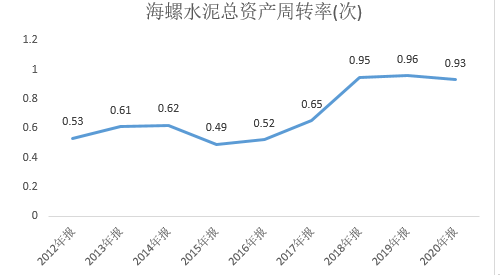

At the same time, the total asset turnover rate of Conch Cement has also increased rapidly, which is mainly due to the supply-side reform. The increase in cement prices has led to a surge in revenue, which has led to an increase in the total asset turnover rate.

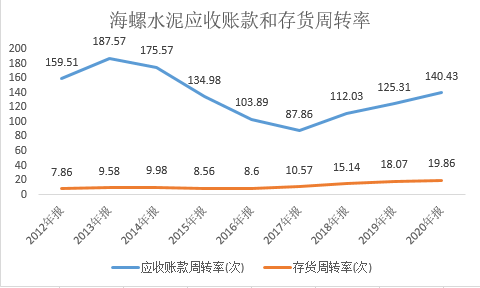

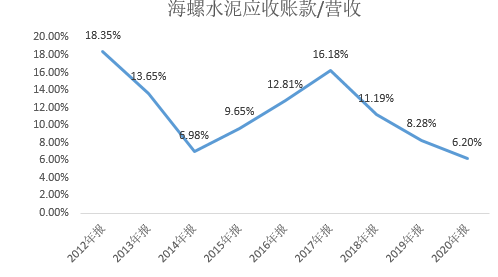

Conch Cement’s accounts receivable turnover rate and inventory turnover rate have increased significantly after 17 years, which is relatively good, and in such a “sunset” industry, Conch Cement’s accounts receivable only accounted for 6% of revenue , which reflects the strong voice of the enterprise

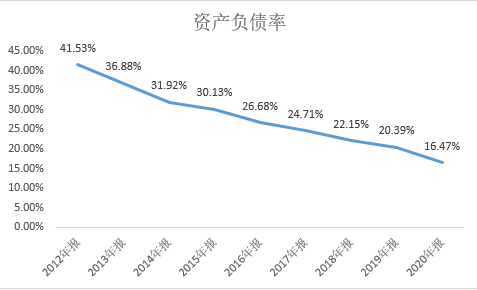

Judging from the asset-liability ratio of Conch Cement, the debt ratio has been declining since 2012, which reflects the company’s good solvency, but on the other hand, it also indicates that the company has reduced its plans for large-scale expansion and turned to mature conservative operations. .

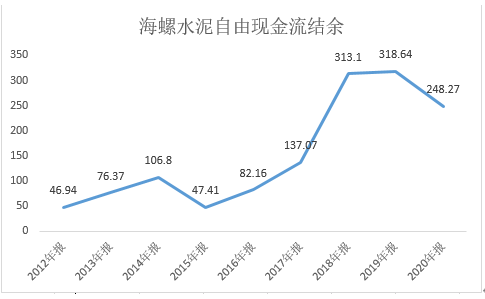

From the point of view of cash flow, the ratio of corporate sales to revenue has always been higher than 100%, and Conch Cement’s annual free cash flow balance is getting higher and higher. Many companies are giants in profit, but dwarfs in terms of cash flow , Conch Cement let us see that there are also a small group of A-share companies that are carefully maintaining cash flow and focusing on their main business. They are not necessarily the best in the short term, but they do live the longest.

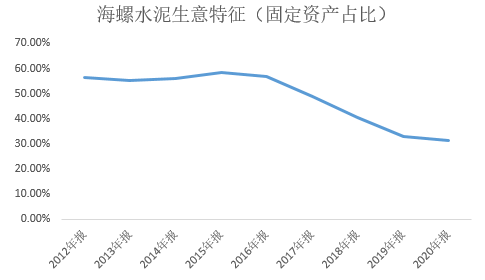

Finally, let’s look at the characteristics of Conch Cement’s business. In essence, this is an asset-heavy business, but Conch Cement’s operational capabilities and management capabilities have made it an asset-light business, which means that the cash flow is very rich, but We should also be vigilant, that is, it is difficult for enterprises to find opportunities worth expanding fixed assets, which is a mature period.

Risk :

1) The demand for real estate declined, and the newly started area and sales area continued to decline in the second half of the year; cement prices fell and price wars

2) The issuance of special bonds has not yet been implemented on new projects, and the project progress has slowed down; in 2021, my country’s generalized infrastructure investment will grow by 0.21%, and real estate investment will grow by 4.4%, and the monthly growth rate will continue to decline.

3) Double control of energy consumption, enterprises are forced to reduce production.

Valuation

Qualitative :

In Q3 2019, Hillhouse Capital entered the top ten shareholders of Conch Cement. Some people speculate that it is to accelerate the merger and acquisition of Conch Cement, but it seems that there has been no action in recent years, and it is more inclined to pure financial investment.

From the perspective of a large industry, the growth of enterprises can no longer be pinned on the expansion of production and volume growth. In the face of the decline in industry demand, the policy level has made it clear that some traditional industries need to reduce production capacity. 2016 and 2017 are the industry’s 10-year production capacity. The low point of the industry, and clearly put forward the reform of the supply side, this process is sustainable, and it is in line with the reality of the industry development, the supply reform means fewer players, the supply reform is still at the starting point, the long-term perspective is clear, the first half of the industry , the company earns the capacity expansion of the industry, and in the second half, the company earns the increase in the concentration of the industry, and the strong cyclical characteristics of the industry gradually begin to weaken.

From the perspective of mergers and acquisitions, looking at the balance sheet, the book currency is 44.5 billion book cash, accounting for 26%, the interest-bearing debt ratio is 6%, the goodwill is 500 million, and other wealth management funds have not been counted, and the ROE is close to 20%. Ability to carry out mergers and acquisitions, but it seems that the company does not have much action and plans at present. (The merger and acquisition expectations cannot be put too high, because the top companies are living well at least without losses, and everyone has a certain ability to acquire small factories.)

However, compared with CNBM, CNBM’s business is more complex and diversified, with 32.7 billion cash, accounting for 7%, 42.6 billion goodwill, at least 23% interest-bearing debt ratio, large goodwill, and debt, and its operating level is worse than Conch a lot of. Conch still has priority, at least in companies with PB close to 1, Conch’s debt is very, very low, and the sustainability of dividends is also Zhang Lei’s consideration.

It is difficult for both volume and price to go through. For the supply-side reforms analyzed above, it is difficult to increase market share, because the top 10 are living very well, and the price of the cement industry is still not low. Therefore, if Conch Cement wants to grow, it can only be seen in overseas markets. Aggregate, the overseas market is relatively slow, and cement companies in other countries have already formed, and they have little advantage in the cost side. Only in Southeast Asia may have opportunities to develop, so in the end, we can only look at aggregates.

From the qualitative point of view of the operation of the company itself, the industry structure has been determined. Conch is basically the strongest, and it has achieved sufficient cash flow in an undifferentiated industry. In addition, this industry is also close to sustainable, but its growth is insufficient, and dividends can be distributed. long-term maintenance. From the perspective of the company’s three expenses and gross profit margin, the cost has been compressed to the extreme, and the cost side has also been optimized to perfection, and the cement price has also provided flexibility, so there is not much room for further improvement of the net profit margin.

The growth of the company is insufficient, but the quality is good enough, and it has a mine value of about 50 billion yuan, the cash flow can be close to sustainable, and the dividend rate can be maintained without a substantial decline in the cement price. It is the first in the industry that cannot be subverted. , the quality of the enterprise may be underestimated, but the future growth is not underestimated.

Quantitative :

1. Conch cement scale in limit state:

On the business side of the enterprise, the conch state under the extreme optimistic state has been simulated, and with a market share of 26%, the traditional business has a total scale of 260 billion + aggregate 30 billion, 290 billion, and the current scale is 176.2 billion, and there is still 64% room for development , but this is still less as a guarantee space for valuation multiples.

3. Profit forecast : under normal circumstances

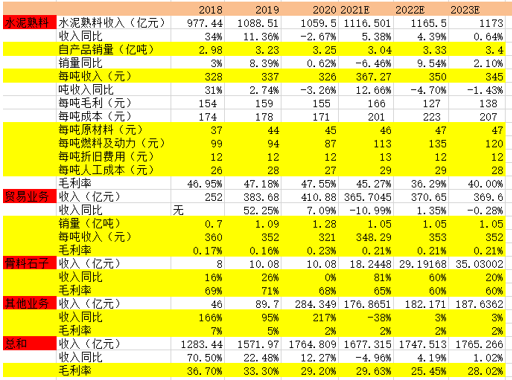

The first is cement. In 2022 and 2023, due to the steady growth of demand, the relaxation of infrastructure and real estate will have a boosting effect on cement, so it is expected that the sales of self-made products will increase at a slow growth rate. Assume 333 million tons in 2022 and 340 million tons in 2023.

Cement revenue per ton is related to the price trend. Under normal circumstances, cement prices are resilient. At the same time, it is assumed that the US interest rate hike is expected. In 2022, it is assumed that the cement price will fall slightly. In 2023, it is assumed that the overall commodity will fall. At the same time, with the decline of coal and electricity costs, the price will continue to fall.

Trading business: We wrote earlier that the company will not vigorously promote this aspect, in order to control the amount on an equal footing with CNBM

We have seen that the aggregate business is a new business. At the same time, Conch Cement plans 700 million tons in the 14th five-year plan, giving a higher growth rate expectation.

Other businesses: such as commercial concrete, do not make expectations and remain unchanged.

Among them, there are three main points that exceed expectations in 2021. One is fuel and power per ton. Maybe Conch Cement has a long-term agreement with coal companies, so it has a strong ability to withstand pressure. In addition, aggregates have high gross profit margins, and the growth exceeds expectations. Finally, cement Prices are regional and resilient in 2021, but judging from the forecast for 2022, the gross profit margin may decline. On the one hand, the price of cement will decline, and the cost of coal will continue to rise.

The meaning of a table like the one below is basically very small, because predicting performance is like going to a scratch, and more performance forecast is a grasp of the business situation, rather than the calculation of specific numbers.

Market Evaluation Section:

From the perspective of cement prices, cement prices are already at a high level, and it is difficult to maintain the original price level under the background of declining demand. However, after the reduction of players, the volatility of cement will decrease. The level of the problem, overseas progress, and the trade-off between the development of the aggregate market, these belong to the vague direction and unclear direction, so we should grasp the extreme position when the direction is clear. After fully expressing the negative factors and lowering the valuation, an opportunity will be formed, and there is a better valuation base.

From the perspective of investment, it mainly takes dividends, and the long-term growth is not so certain. Therefore, it is best to expect the occurrence of aggregates or some mergers and acquisitions when the price of cement is low. There is a margin of safety for intervention in extreme positions. Low, mainly due to the market’s anticipation of the downturn in real estate, and some of them have the same goal. However, if the concrete price of cement falls, how the market will reflect it still needs to be considered. What everyone needs to think about later is that the price decline is a periodic weather factor. It was the beginning of a fierce price war for cement, which determined the timing of the deal. At present, the company’s static valuation of 1.10PB is not high, and the industry is in a state of near-sustainability, and the competitiveness of the company is unshakable.

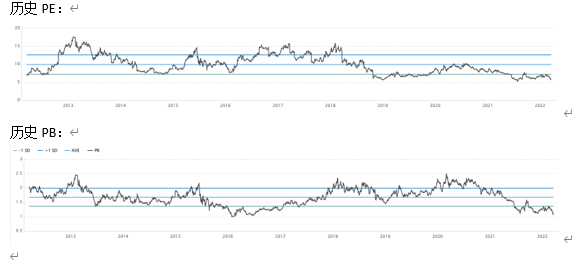

From the perspective of market cognition: from the perspective of historical PE and PB, they are all historically low levels. On the one hand, the low PE is due to the boom in cement price increases in the past few years. The short-term pessimistic expectations and concerns about the long-term growth of Conch Cement must be reversed unless the short-term policies on real estate and infrastructure are relaxed, or the long-term aggregate market is opened. Can’t find enough reason and logic for confrontation. Still take dividends steadily, looking forward to the short-term pulse of real estate relaxation or infrastructure development. Not suitable for heavy storage.

Transaction landing

Target classification: long-term holdings have no obvious growth unless the aggregate market is opened, or the market share increases, and the cash flow is excellent in time to get dividends. If short-term holdings, expect real estate relaxation and changes in infrastructure expectations

Timing: When real estate and infrastructure are expected to be pessimistic, or when cement prices unexpectedly drop sharply, it is best to be in an extreme area where two negative factors occur at the same time, otherwise the direction is unclear.

Position: The long-term growth is not clear, there is no obvious blind spot, it is not suitable for heavy positions, medium and low positions hold stable dividends, and at the same time look forward to the opportunity of low valuation repair.

It can be seen from the above framework that my judgment on a company is never good or bad, but a balance of good and bad. I use the target classification, timing, and position to fine-tune the risk part. A good company is not necessarily a good stock. The question is whether the good can be better, the average can become better, and the poor can become average. The core is change. Fundamental analysis is a subject, but fundamental analysis only provides the probability of an event, letting us know the possibility of such a change and growth, and market cognition is an auxiliary tool, unless People with strong business insight can surpass the industry and can ignore the market cognition and surpass the cycle. Knowing Mr. Market and understanding the market reflects a kind of humility. I have seen a passage before. From a certain point of view, the market is always effective, but the dimensions of enterprise evaluation are different in a certain period of time. Sometimes the short-term dimension is emphasized and the long-term is ignored. At this time, there are often long-term Bottoms, and medium-term tops, and if you focus too much on the long-term dimension (such as the market in recent years), there will be long-term tops and medium-term bottoms.

This market is full of too many people in the industry and research gods. For example, we will be crushed when we try to compete for research ability, and we will also be crushed when we try to compete with industry knowledge and information. The only two points are that we can do it, one is to use them After fully interpreting the negative information and reflecting it on the stock price, we will look for framed information and changes that will improve the future, and wait for them to interpret. The second point is to have a better temperament and be calm in the ups and downs . Then one point to avoid is to use your own assumptions to delusionally correct the market.

Of course, the highest pursuit is to be like Li Lu and Buffett, to be honest in the face of knowledge, to be within the circle of competence for a company or some things, and to grow together with excellent companies. This kind of research and perception requires a lot of effort. For a long time, it is suitable to spend on heavy stocks.

The recent market is a bit “weird” again. I still hope to calm down and prepare slowly to deal with various “situations” that will appear in the future.

Forwarding comments and likes is a kind of support, and following is a kind of fate.

@Today’s topic $ Gree Electric Appliances (SZ000651)$ $ Conch Cement (SH600585)$ $ Vanke A (SZ000002)$

There are 22 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/1577913976/223612237

This site is for inclusion only, and the copyright belongs to the original author.