Investors who buy industry-themed funds are generally optimistic about the beta market of a certain industry. The performance of themed funds is often highly correlated with the prosperity of the industry. To a certain extent, for industry-themed funds, the industry’s beta is more important than the fund manager’s individual alpha creation ability.

However, for some industries with particularly complex industrial chains, there are obvious differences in the prosperity between sub-industry industries and individual stocks, so there is still room for fund managers to actively create alpha.

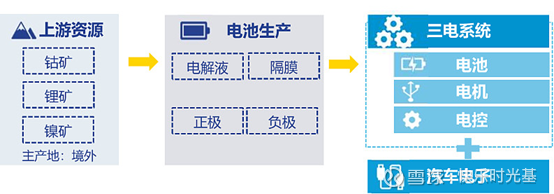

The new energy industry chain involves upstream mineral resources, midstream lithium battery materials, and downstream key components and vehicle manufacturing. Different links have obvious differences in bargaining power in the entire industry chain. Prosperity is not in sync. Therefore, when fund managers enjoy the beta market of the industry, they also have room to tap individual stock opportunities and look for differences with market expectations.

New energy industry chain (source: Guo Weisong_Xinxin Investment)

So, today, let’s make an in-depth comparative analysis of the actively managed new energy-themed funds on the market. Which funds have created significant alpha returns? What are they doing right?

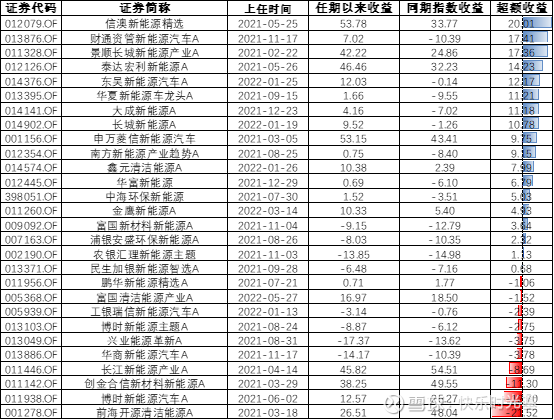

At present, there are 40 actively managed new energy themed funds in the market. Here are the results screened according to the product name and contract agreement, excluding those funds that have heavy positions in new energy stocks but have no clear contractual constraints. Because once the industry boom has switched, it is easy for these funds to adjust positions.

How to measure the alpha creation ability of individual fund managers? We use the return of the fund manager during his tenure and compare it with the return of the industry index in the same time interval to calculate the excess return of the product.

However, considering that many new energy-themed funds were established late, the observable performance period is short. Therefore, for those established in 2021 and later (or for current fund managers to take office after 2021), we use the interval returns of the product and the corresponding index to compare; for those established in 2020 and before, we use the interval between the product and the corresponding index. Annualized returns for comparison.

From the results, most thematic funds established after 2021 have obvious excess returns. The possible reason is that the new fund avoided the sharp drop in market conditions due to the existence of the position-building period. Among them, “Xinao New Energy Selection”, “Caitong Asset Management New Energy Vehicles” and “Invesco Great Wall New Energy Industry” are the top performers of excess returns:

“Xin’ao New Energy Select” was established in May 2021, and its income since its establishment is close to 54%, with an excess return of 20%; $Cinda New Energy Select Mix (F012079)$

“Caitong Asset Management New Energy Vehicle” was established in November 2021, with a profit of 7.02% during the period and an excess return of 17.41%;

“Invesco Great Wall New Energy Industry” was established in February 2021, with a profit of 42.22% and an excess profit of 17.36%.

The excess return performance of some new energy-themed funds (after 2021)

There are not many thematic funds that have been established for a long time and have accumulated obvious excess returns. The more prominent ones are “Xinao New Energy Industry”, “Huaxia Energy Innovation”, “Harvest New Energy New Materials” and “Chuangjin Hexin New Energy”. “Energy Vehicles”:

“Xin’ao New Energy Industry” was established in October 2016. During the period, the annualized income was close to 30%, and the annualized excess income was 12.57%; $Xinda Aoyin New Energy Industry (F001410)$

“Huaxia New Energy Innovation” was established in June 2017, during which the annualized income was 29.33%, and the annualized excess income was 7.1%;

“Harvest New Energy and New Materials” was established in March 2017, with an annualized income of 25.15% and an annualized excess return of 7%;

The excess return performance of some new energy-themed funds (before 2020)

However, there are not a few new energy funds that actively manage negative excess returns. The excess returns of “BOC Securities Clean Energy”, “Qianhai Kaiyuan Clean Energy” and “Rongtong New Energy” are all below -15%.

It can be seen that the two new energy themed funds of Cinda Australia and Asia are the products with the most outstanding short-term and long-term performance respectively. We will make further comparative analysis of these two products.

1. Xinao New Energy Industry

“Xinao New Energy Industry” is a well-known Internet celebrity fund in the past two years. It is the representative work of Feng Mingyuan, a well-known fund manager. As of the first quarter of this year, the scale of this product was 14.041 billion yuan, and it is currently the top 4 new energy-themed funds.

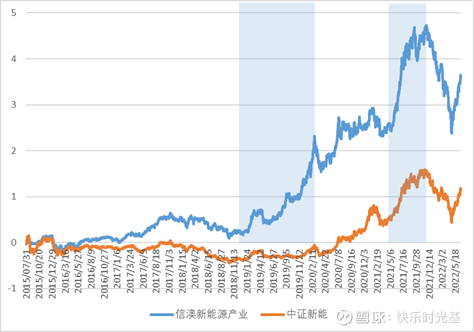

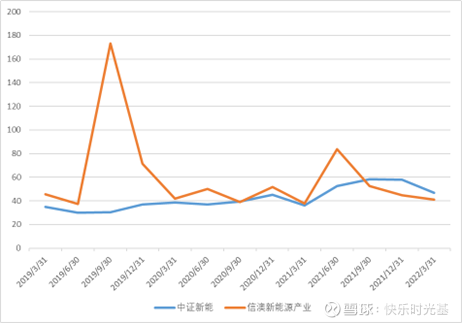

Judging from the performance trend, “Xinao New Energy Industry” mainly accumulated significant excess returns relative to the industry index in the first half of 2019 and the second half of 2021. In addition, after mid-2021, the trend of Xinao New Energy Industry and the industry index is basically the same.

Comparison of the trend of “Xinao New Energy Industry” and the new energy index

Feng Mingyuan’s investment style can be summed up as the following characteristics: give up timing and maintain positions above 90%; spread distribution at the industry and individual stock levels; high proportion of small and medium-sized stocks; do not chase high, focus on valuation protection; change hands The rate is not low, and the transaction has contributed a certain amount of income to the portfolio.

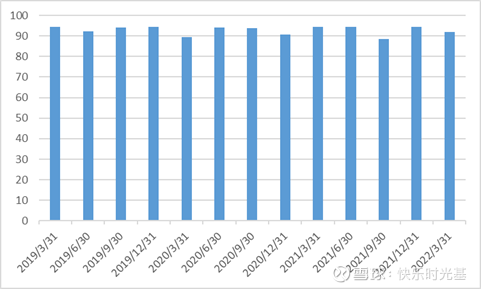

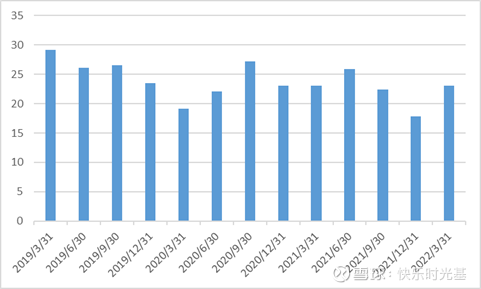

The timing of “Xinao New Energy Industry” in recent years is not obvious. The stock position bound by the product contract is 80%-95%, and the stock position of this product has been above 90% in recent years.

The stock position of “Xinao New Energy Industry”

The dispersion of holdings is mainly reflected in two aspects: the proportion of heavily held stocks is low, and the number of holdings is large. In recent years, the proportion of the top 10 heavyweight stocks of “Xinao New Energy Industry” has basically been below 30%, and it has further dropped to 17.86% by the end of 2021. In the past three years, the number of shares held by Xinao New Energy Industry has been more than 400 in the past three years. At the end of 2021, Feng Mingyuan even took 652 shares.

The proportion of heavy holding stocks in “Xinao New Energy Industry”

Industry distribution is also very fragmented. At the end of 2021, the top three industries of Xin’ao New Energy Industry are power equipment, electronics and automobile industries, accounting for nearly 50% of the total, and the industry concentration is much lower than other actively managed themed funds.

Except that the average valuation of the heavyweight stocks in Xinao New Energy Industry was significantly higher than that of the industry index in mid-2019, there was no significant deviation from the valuation level of the industry index during the rest of the period. And since the middle of 2021, when the overall valuation of the new energy sector is rising, the average valuation of the heavyweight stocks in the Xinao New Energy Industry has begun to decline. As of the first quarter of 2022, the dynamic PE of CSI New Energy was 46.62 times, and that of Xin’ao New Energy Industry continued to drop to 40.93 times.

Comparison of Valuation Changes between “Xinao New Energy Industry” and New Energy Index

Feng Mingyuan also has relatively obvious trading behavior. The turnover rate in recent years is not low. The turnover rate from 2019 to 2021 is 2.72, 3.92 and 2.92 times respectively. The higher turnover has created certain actual benefits for the product. , it can be seen that the transaction is also a relatively important revenue contribution of “Xinao New Energy Industry”.

In addition, the holdings of “Xinao New Energy Industry” are mostly small and medium-cap stocks. In response to the rapid expansion of the management scale, Feng Mingyuan’s shareholding has also increased sharply, from 223 at the end of 2019 to 652 at the end of 2021. How to find more targets that meet the investment requirements in the future is still a big challenge.

2. Selected by Xinao New Energy

The fund manager of “Xin’ao New Energy Select” is Zeng Guofu. He has joined Xinda Australia and Asia since September 2006, and has been managing public offerings since 2008. He is a veteran in equity. The current scale of “Xinao New Energy Selection” is 3.511 billion, which is far from the scale of “Xinao New Energy Industry”.

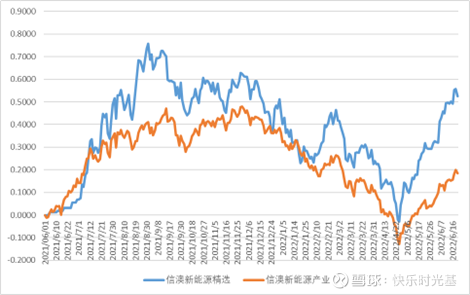

From the performance point of view, the rebound of Xin’ao New Energy Selection since the end of April is significantly higher than that of Xin’ao New Energy Industry. Since April 25th, Xinao New Energy Selection has rebounded by 51.68%, while Xinao New Energy Industry has only rebounded by 28.54%.

Comparison of the trend of “Xinao New Energy Industry” and “Xinao New Energy Selection”

Although it is a new energy-themed fund of the same company, Zeng Guofu’s holding style is completely different from that of Feng Mingyuan. Judging from the regular reports disclosed, it can be roughly seen that Zeng Guofu’s investment style is: individual stocks and industries are highly concentrated, and he is a player who dares to ALL IN; the turnover rate is high, and he will rely on trading to obtain band income; there is no obvious There is no obvious sign of chasing high.

In the past three quarters, the weighted stocks of Xinao New Energy Selection accounted for more than 65%. The number of holdings at the end of 2021 is only 57. In terms of industry distribution, the top three industries are non-ferrous metals, automobiles and basic chemical industries, accounting for a total of 63.3%.

Compared with the industry index, there is no obvious deviation in the average valuation of the heavyweight stocks selected by Xinao New Energy. As of the first quarter of 2022, the average valuation of the heavyweight stocks selected by Xinao New Energy was 30.5 times, a significant decrease from the previous two quarters.

Comparison of Valuation Changes between “Xinao New Energy Select” and New Energy Index

The turnover rate of Xinao New Energy Selection is very high, as high as 4.46 times in 2021. One of the manifestations is that there are frequent changes in the stocks with heavy holdings. For example, in the fourth quarter of 2021, 6 stocks entered the list of the top 10 stocks with heavy holdings for the first time. Individual stock trading is also one of the important sources of Xinao New Energy’s selection.

To sum up, these two themed funds reflect different investment styles: ” Xinao New Energy Industry” is a new energy themed fund with a partial balanced allocation, and “Xinao New Energy Select” is an ALL IN segment. New energy-themed funds for industries and individual stocks.

Finally, let’s briefly discuss whether it is still suitable to start a new energy theme fund at present?

After a strong rebound since the end of April, the configuration cost-effectiveness of the new energy track has declined, and the current entry point is far less comfortable than at the end of April. From the perspective of dynamic PE, on June 21, the dynamic PE of the CSI New Energy Index was 38.93 times, at a historical quantile of 59%; the dynamic PE of the new energy vehicle index was 57.82 times, at a historical 53%. quantile. From this perspective, the current valuation level of the new energy sector is still in a moderate state.

But from the perspective of PB, the new energy sector is still on the expensive side. The latest PB of the CSI New Energy Index is 5.52 times, at the historical quantile of 22%; the latest PB of the New Energy Vehicle Index is 8.39 times, at the historical quantile of 25%.

However, with the continuous release of the recent favorable policies, coupled with the previously accumulated demand for oversold rebounds, this wave of rising prices is indeed beyond the market’s expectations. However, the bull market does not say the top, and the bear market does not say the bottom. If you are worried about stepping out of this wave of rebounding market, it may be a wise choice to participate in the relevant themed funds with obvious excess returns, and gradually increase the positions on every dip.

@snowball fund @snowball creator center @today’s topic

#星Plan creator# #New energy vehicles continue to skyrocket! The daily limit of many stocks such as Xiaokang shares#

# Lao Siji Hard Core Evaluation# + $Cinda Australia Bank New Energy Industry (F001410)$

This topic has 0 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/1810621710/223561411

This site is for inclusion only, and the copyright belongs to the original author.