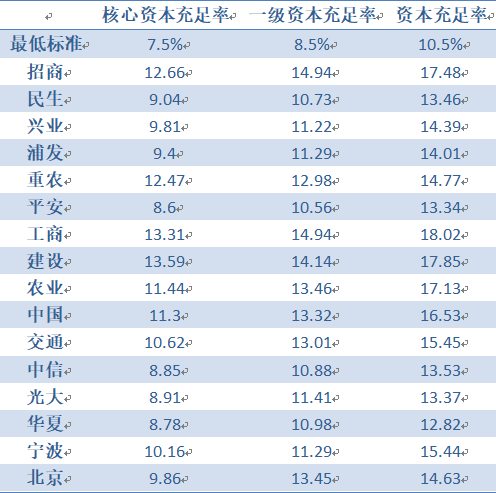

First, let’s look at the capital adequacy ratio:

Capital Adequacy Ratio Statement

In recent years, the capital adequacy ratio of each bank has basically not changed from a vertical perspective. The abundant ones continue to be abundant, and the nervous ones are always nervous. The banks in difficulty have also enjoyed the benefits brought by the release of water. Debt and other means to replenish capital, but this will continue to dilute the rights and interests of old shareholders, especially banks with limited funds need to replenish capital frequently. At present, only China Merchants Bank can achieve real endogenous growth without asking for money from the capital market. In this regard, there is still a big gap between Ning Bank and Ping Yin. Let’s look at the bank’s asset quality, non-performing and provisioning situation:

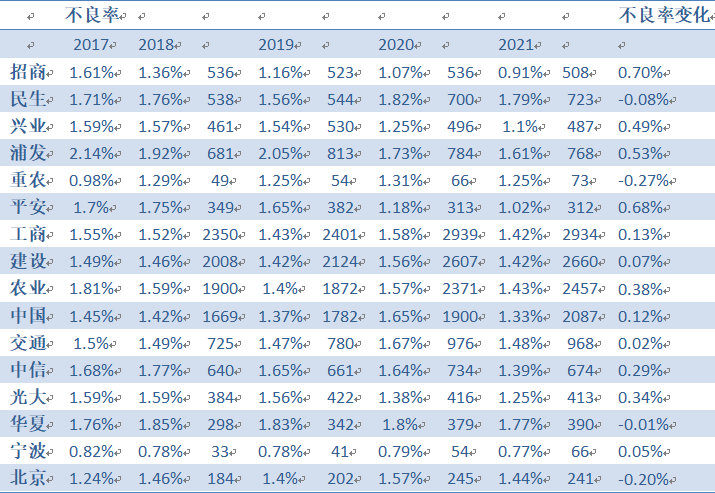

Special mention loans are the reserve pool of non-performing loans. Looking at the ratio of special mention loans can roughly determine the ratio of non-performing loans. Looking at the ratio of special mention loans of China Merchants Bank and Ningxing Bank is higher than the ratio of non-performing loans, it is very easy to reduce the non-performing rate later. Explain that the criteria for identifying non-performing loans are very strict. And like Minsheng, CCB’s loan rate is one point higher than the non-performing rate, and the prospect of a reduction in the non-performing rate in the future is not optimistic. Special mention loans can be regarded as a forward-looking indicator of non-performing loans, and it is more likely to be non-performing before paying attention to certain problems. Although the standard of non-performing ratio is different for each bank, the vertical comparison of each bank can clearly see how their own lives are:

In the past five years, the overall NPL ratio of banks has been in a continuous decline. This trend can also be seen from several large banks that do not act. In 21 years, the NPL ratio of major banks has dropped to about 1.4%, while the NPL ratio of active banks has dropped. The speed is significantly faster than that of its peers. China Merchants Bank has a non-performing rate of up to 0.7% in the past five years, and it is the most stringent standard. The non-performing rate and the non-performing rate and the amount of non-performing loans have both decreased under the condition of continuous growth of loans; followed by Pingyin, although Pingyin’s identification standards are not as strict as those of China Merchants Bank. The NPL ratio and amount of NPLs that have also dropped sharply fully illustrate the progress of the company’s risk control system. What Pingyin should continue to learn from China Merchants Bank is to continue to suppress the non-performing loans of new students. Reducing non-performing loans is the key at present, but the proportion of Pingyin credit cards is too high, and it is unrealistic to hold down new non-performing loans under such a background. , the non-performing amount was basically flattened, the non-performing rate dropped by 0.53%, and the non-performing rate finally came to around 1%. Although the non-performing rate of Shanghai Pudong Development Co., Ltd. has also dropped by nearly 0.5%, the rapid progress is due to the low starting point. The non-performing rate is above 2%. It started to drop, and it is only reasonable to drop to 1.6%.

At present, from the perspective of non-performing rate, banks can be clearly divided into several grades. 1% and 1.5% can be divided into two groups. Ningxing and China Merchants Bank’s non-performing rate is lower than 1%. Changes, others are low-level consolidation, the non-performing rate has been around 0.8%; Pingyin and Xingye are close to the 1% non-performing rate. These two companies have made rapid progress in the past five years, and the 1% non-performing rate is also a good result. Just from the point of view of special-mentioned loans, the basis for the subsequent decline of the NPL ratio is not strong, and it needs to be stable for two years here; the NPL ratio of most banks is around 1.4%, and the big banks are the ducks in the pond. The water surface is ups and downs, and others can’t see anything. It is thanks to the general environment that we can maintain this. The two difficult households with a non-performing rate of more than 1.5% are Minsheng and Shanghai Pudong Development. Still no sign of a reversal.

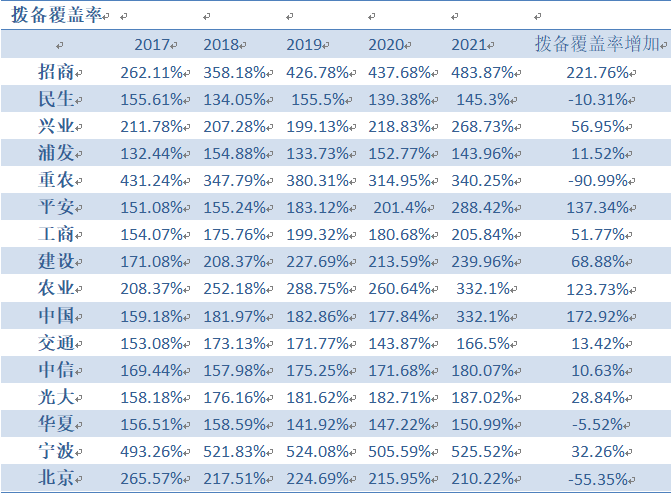

Looking at the NPL ratio of banks vertically, we can see some changes. After all, the standards for classifying NPLs are different, and we cannot simply compare horizontally. Moreover, the NPL ratio is only a part of the gap between banks. Even the worst NPL ratio of Minsheng Bank is 1.79%. The gap with other banks is not too much. Another thing that can significantly indicate the gap is the provision coverage ratio. The gap in performance growth between banks is too large, and it will give face to peers. If the profit is released to a certain level, it will be put into the capital reserve pool, that is, the provision for impairment. The capital reserve pool of an excellent bank is getting bigger and bigger, and the bank’s risk control system is very good. The non-performing loan has remained at a stable level, and the provision coverage ratio has been increasing. Continuous impairment consumes profits and does not want the profits to be too ugly, so we can only store less water in the capital reserve pool. The increase in non-performing loans is faster than the increase in impairment provisions, and the provision coverage ratio has been declining. From the level of provision coverage, it is easy to see who has more than enough and who is stretched. The provision coverage ratio of China Merchants Bank and Ning Bank is 483% and 525%, which means that the surplus is full, which continues to increase by 46% and 20% compared with last year. Although the CBRC has repeatedly emphasized It is necessary to reduce the provision coverage ratio to release profits, but these two companies have strict identification standards, and it is difficult to increase the non-performing balance. Unless the general environment is not good, the provision coverage ratio is really difficult to reduce.

People’s livelihood, Shanghai Pudong Development Bank, transportation, and Huaxia’s provision coverage are at 150%. The change in the provision coverage ratio in recent years has become more obvious. The increase in the provision coverage ratio of China Merchants Bank is unique. The safety pad is getting thicker and thicker. It is also using the waterproof cycle to increase reserves, and in such a year, the problem that the provision coverage is still declining is a bit big. Chong Nong and Bank of Beijing are both representatives of decline, and Bank of Communications is the worst among large banks. , Minsheng and Huaxia are the worst among medium-sized banks. In recent years, the only thing that can reduce the provision coverage rate is to give you the opportunity to use it. What else can you say. In the past five years, China Merchants Bank has irrigated the most water in the reserve pool. It is not surprising that Ning Bank has grown a lot. Originally, the provision coverage ratio of others has reached 500%. How can it increase? Five years ago, the provision coverage ratio of Ping Yin and Bank of China was also Struggling on the 150% line, the provision coverage rate of rapid progress in the past five years has doubled to 300%, which is relatively abundant; the other provisions coverage rates have not changed much and have negative growth. I really don’t know what to say. , once the economic cycle is over, there is no safety pad and profits are lost. I don’t know how miserable it will be.

$ China Merchants Bank (SH600036)$ $ Ping An Bank (SZ000001)$ $ Industrial Bank (SH601166)$

21 Years of Bank Data Analysis (Part 1)

21 years of bank data analysis (middle)

21 Years of Bank Data Analysis (Part 2)

21 Years of Banking Data Analytics (continued)

This topic has 4 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/3501227211/223680925

This site is for inclusion only, and the copyright belongs to the original author.