This article is about 1500 words and takes 3-5 minutes to read.

Looking at A-shares, only the animal husbandry industry and the supermarket convenience store industry have recorded a record high average debt ratio in the past 2-3 years. Although the interim report has not yet been released, it can be inferred that the overall debt ratio of the animal husbandry industry will further rise (arrow). direction), and further up, it will approach finance and real estate.

In the past, the pig cycle was always accompanied by various epidemics. At present, ASF has entered a state of normalized prevention and control. In view of the relatively rare phenomenon that the overall debt ratio of the industry has rapidly exceeded the historical high, what problems may arise?

The financial industry has strong supervision, and there is a safety bottom cover for non-performing provision; the main products of the real estate industry are differentiated and are an important supporting force for the national economy, which is greatly affected by policy factors; for the pig breeding industry, the products are basically the same. Quality and liquidity are extremely strong. Because of the high homogeneity of the products, pig companies lack pricing power in most cases. Once the supply slightly exceeds the demand, the company may face losses. The judgment of supply and demand is extremely important in business operations. Unfortunately, this kind of Judgment is extremely difficult, which brings a lot of challenges to the expansion of enterprises. Once the supply and demand situation is judged wrongly, the consequences of expansion will be disastrous. Take Zhengbang Technology, which has rashly expanded due to mistakes in market research and judgment, as an example. In 2020, Zhengbang’s live pig slaughtering scale surpassed Wen’s shares and became the second largest in the industry. The asset-liability ratio was less than 59% that year. In the past year, the asset-liability ratio in 2021 The rate has soared to 93%, and today it is struggling on the line of life and death. There is a factor that the cost of breeding is too high, but the bigger reason is the rash expansion . Hasty expansion will either make a fortune or seek death. The case of Zhengbang Technology is of great significance for studying the expansion of pig enterprises, and it is also of great value to those who over-trust the so-called Propagation Data (Imagine whether Zhengbang believed too much in the Data of Propagation at the beginning). Compared with finance and real estate, pig enterprises’ business model, product characteristics, and breeding attributes determine that their risk tolerance is not as good as the former. , when the debt ratio is too high, the risk factor is extremely large, and if you are not careful, you may follow the footsteps of Zhengbang.

Greed has always been an indelible aspect of human nature. As mentioned earlier in the article analyzing the financial situation of 17 pig companies in 2022Q1, the huge profit effect under the ASF cycle will prevent pig companies from leaving the battlefield easily. In fact, it is true in this way. The debt ratio of Aonong Biotechnology is as high as nearly 90%, the debt ratio of Wen’s shares is in the middle and upper reaches, and the pig enterprises such as Tangrenshen, Superstar Agriculture and Animal Husbandry, and Xinwufeng with medium debt ratio have all been investigated in recent months. Talking about grand plans, let’s not care whether these companies have the solid conditions to achieve their goals, or whether they are out of pleasing the capital market. By their nature, the non-plague profit-making effect has long been deeply engraved in their brains, and they are sent to them. Hope to be able to show great plans in the future. On the contrary, Mu Yuan and New Hope, who are in the top and two strong, seem extremely cautious. Although expansion will face huge risks, greed will inspire everyone to move forward actively. Expanding the scale of pig farming requires funds, and the level of debt will restrict the expansion of the company. The constraints include three aspects: first, debt repayment, which needs to be solved at the moment. The first problem is that most companies are already facing unprecedented debt pressure and are in urgent need of capital replenishment or a positive cash flow due to a warmer market. The second is willingness. Once bitten by a snake, they are afraid of a rope for ten years. For expansion, pig companies say they will go home. It is said that when it comes to investing real money, it will be repeatedly weighed, and the willingness of enterprises to expand under higher leverage will decrease; the third is ability, expansion requires funds, in addition to working capital, financing channels, financing amount, financing costs, and financing efficiency. consider. Under the high debt ratio, the pressure of debt repayment increases greatly, the willingness to expand decreases, and the expansion capacity shrinks. Against such a background, what can we do to expand significantly in the short term?

It is also for the above reasons that the rapid rise in the debt ratio caused by the skyrocketing price of raw materials and the leverage of pig companies will substantially restrict the expansion capacity of enterprises/individuals. The current level of debt has never been encountered at the bottom of any previous cycle. Earlier, when analyzing the “Family Portrait of Pig Enterprises’ Financial Status in the First Quarter of 2022”, he proposed an idea to observe this cycle: instead of observing the number of sows that can reproduce, it is better to observe the financial endurance of pig enterprises. For the original text, see the webpage link . It’s not that the pig companies don’t want to expand, but most of the pockets are running out, the disabled, the injured, the expansion strength and confidence are not as good as the hard core in the past, how easy is it to restore it for a while? As the saying goes, the worse the loss, the more fierce the rise, and the extreme will be reversed.

Since the second quarter, market disagreements and suspicions have emerged one after another:

Three bottoms. Experts predict that the price of pigs will reach a high level around September, which will lead to large-scale replenishment of the industry. After 6 months (near March 2023), the industry will start to detoxify again due to three dips due to heavy supply. The implicit premise of the three-dip theory includes that the industry can be proliferated and not yet fully decomposed. If the industry can be prosperous enough, who will provide the bottom-line supply? Will the high price of pigs trigger the large-scale replenishment of the industry? Has it been considered that the high debt ratio will impose substantial constraints on the company’s ability to expand?

The cycle height and length are too short. In terms of height, it is impossible to meet the super cycle in the period of ASF, but it is not necessary to be too pessimistic; in terms of length, the natural time difference between the reproduction of live pigs and the release of commercial pigs is the original factor driving the cycle, while human emotions magnify the cycle Whether it is the real Nengfan that determines supply and demand, or whether people believe that Nengfan affects supply and demand, is that you have me, and I have you, which is complicated.

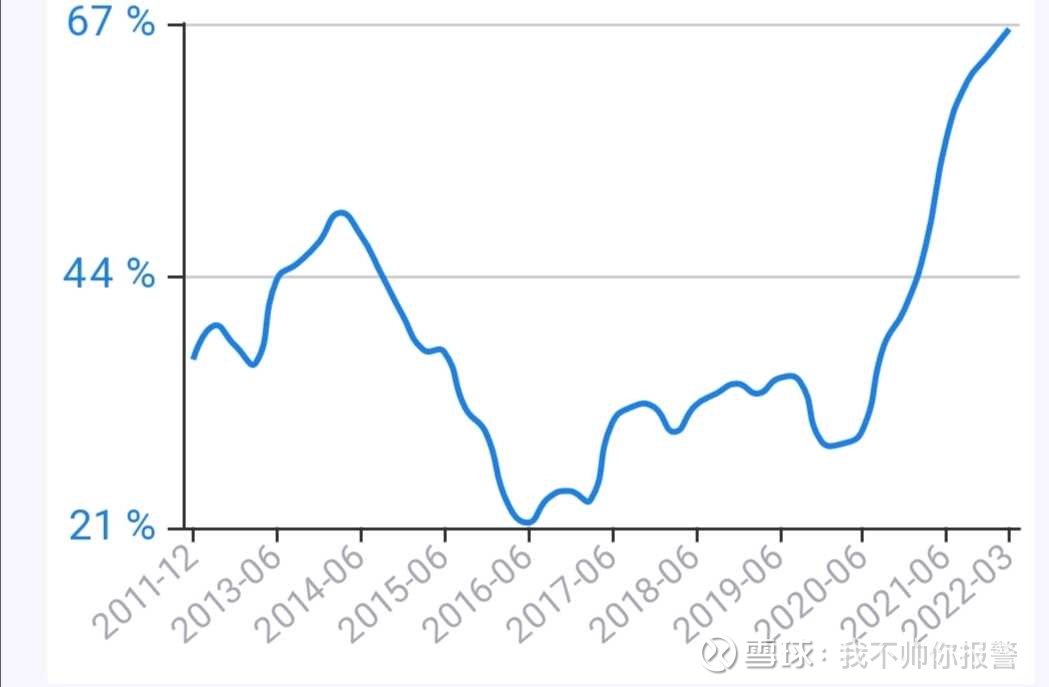

Deep loss period is too short. A large pig company quoted official data during institutional research and gave the statement that the industry’s deep loss period is short and discontinuous. Whether this statement is accurate or not will not be commented. Here is the historical debt ratio of the pig company for your own taste. :

From the perspective of industrial development, the general direction of the increase in the concentration of the pig breeding industry will not change, and the underlying logic of excess profits providing expansion ammunition will not change (supplemented by expansion forms and financing capabilities), and most retail investors will be in the cycle. Only by being gradually compressed and practicing internal skills can we improve the probability of survival and development in dealing with the ups and downs of the market environment.

Underestimating the degree of leverage/detoxification of pig enterprises, overestimating the ability to multiply and expand, the pig cycle driven by high debt ratio may have quietly been staged amid disagreements and suspicions. Unfortunately, if expectations are highly consistent, that could be brewing the next tragedy.

Adhere to independent thinking, welcome rational discussion!

Note: The chart in the text is from Jiuwu

$Muyuan Shares (SZ002714)$ $Wen’s Shares (SZ300498)$ $New Hope (SZ000876)$ Zhengbang Technology Tianbang Food Aonong Biological Superstar Nongmujin Xinnong Dabei Nonghefeng Shares Luoniushan Tiankang Biology Tangren Shenxinwu Fengzhenghong Technology Dongrui Co., Ltd. Shennong Group @Today’s topic @snowball creator center @snowball talent show

This topic has 130 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/4069897501/224036342

This site is for inclusion only, and the copyright belongs to the original author.