Welcome to the WeChat subscription number of “Sina Technology”: techsina

Text / Yan Xue Gong

Source/Snow Leopard Finance and Economics (ID: xuebaocaijingshe)

From 2019 to 2021, Tesla’s stock price has soared 16 times in three years. But entering 2022, Tesla, which has repeatedly created growth myths, began to show weakness, and its stock price fell by 38% in the second quarter alone. In the first half of the year, it not only failed to achieve the target of a 50% year-on-year increase in deliveries, but also lost the global electric vehicle sales crown, which had been sitting on a solid four-year basis.

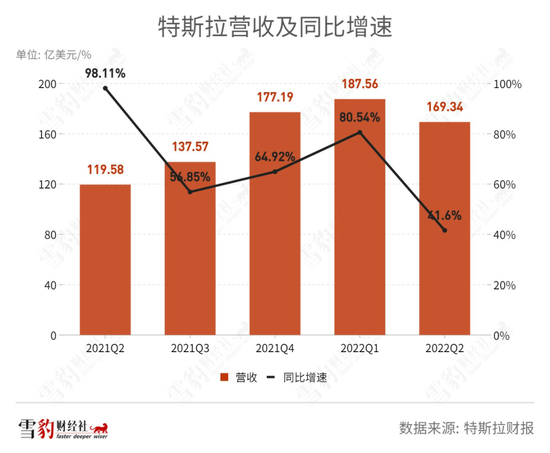

On July 21, Beijing time, after the US stock market closed on Wednesday, Tesla released its second quarter 2022 financial report: revenue rose 41.6% year-on-year to $16.93 billion, lower than market expectations; net profit rose 98% year-on-year to $2.259 billion, higher than market expectations.

Compared with the previous quarter, the key word for Tesla in the second quarter is the decline:

Revenue fell 10% sequentially;

Net profit decreased by 32% month-on-month;

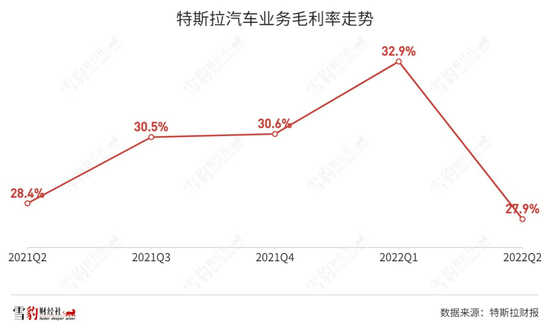

Automotive gross profit margin decreased by 5% quarter-on-quarter;

Deliveries fell 18% sequentially.

Before Tesla released its earnings report, many investment banks got together to lower Tesla’s target stock price. Mizuho lowered it from $1,300 to $1,150, and Morgan Stanley lowered it from $1,300 to $1,200. The reasons for the downgrade are basically the same: concerns about rising component costs and falling car prices will limit Tesla’s future sales and profitability.

Tesla delivered a new record in June as capacity recovers, but the market still has concerns about Tesla’s future: two new gigafactories that were supposed to be capacity boosters have turned into a money melting pot. Internal production capacity is difficult to climb, and cash flow is under pressure, and external competitors are catching up. Tesla, which has just emerged from the darkest moment, is still a dark light ahead.

black “first time”

Tesla, which is recognized as the leader of new energy vehicles, ushered in many black “firsts” in the second quarter of this year: the first time in two years, the number of deliveries dropped month-on-month, the first time in four years that it lost the global electric vehicle sales crown, and its stock price has been listed for 12 years. The biggest drop in a single quarter.

According to the financial report, the auto business is still Tesla’s largest cash cow, with revenue of $14.6 billion, accounting for 86%. As the delivery volume in the second quarter suffered from Waterloo, Tesla’s overall revenue was severely affected, down 10% from the previous quarter to $16.93 billion, up 41.6% year-on-year.

Compared to the high-speed rush of previous quarters, today’s Tesla feels like it’s being slammed on the brakes.

In the first half of this year, Tesla lost to BYD’s 641,400 units with a delivery of 564,000 units, giving up the global electric vehicle sales crown.

Elon Musk’s goal set on the Q1 earnings call was to deliver 1.5 million new cars in 2022. Now halfway through, Tesla has only completed 37.6%. This means that to complete the target, Tesla will deliver nearly 940,000 new vehicles in the second half of the year.

Faced with this situation, analysts have begun to question whether Tesla’s goal of a 50% increase in full-year deliveries is reasonable.

Colin Langan, an auto analyst at Wells Fargo, said, “I’m a little bit unbelievable about their 50% growth forecast. I think the second half of the year will be difficult.” However, Tesla reiterated its annual delivery growth rate of 50% in this earnings report. % of expectations.

As the most profitable new energy car company, Tesla’s net profit growth in the second quarter also slowed down significantly. According to the financial report, Tesla’s adjusted net profit was $2.259 billion, the first time in the past five quarters that it lost triple-digit growth, up 98% year-on-year and down 32% month-on-month.

Tesla’s 11 consecutive quarters of profitability are all supported by high gross margins. In the first quarter of 2022, Tesla’s gross profit margin was as high as 32.9%. But in the second quarter, that number dropped to 27.9%, after several price hikes for Tesla products.

In order to save the decline, Musk also raised the knife to reduce costs and increase efficiency. In June, Tesla announced 10% layoffs, involving 10,000 employees, while adding hourly part-time workers. Analysts at Goldman Sachs believe the layoffs will save Tesla $225 million to $1 billion in annual operating costs.

Falling into production hell, net revenue plummeting, and layoffs affecting 10,000 people, Tesla’s crown of new energy vehicle companies in the second quarter has lost a lot of light. What is behind the darkness?

behind the dark

Factors such as the black swan of the epidemic, supply chain pressure, and high costs have become stumbling blocks for Tesla to run wild.

Affected by the epidemic, Tesla’s Shanghai Gigafactory has repeatedly stopped production since the end of March, and the production has been suspended for more than 20 days. Based on the production capacity of 2,000 units per day, Tesla has reduced production by at least 40,000 to 50,000 units. The situation did not begin to ease until June.

The butterfly effect caused by the Shanghai epidemic has affected Tesla’s global production capacity.

In order to climb out of the capacity hell, in March and April, Tesla’s two Gigafactories in Berlin, Germany and Texas, USA were put into production one after another. However, neither of these two factories can fully produce their own batteries at present. The Texas factory is in the dilemma of increasing production capacity with new battery packs. The traditional batteries used in the Berlin factory rely on the delivery of the Shanghai factory and the Fremont factory. The new factories that should ease the pressure on production capacity are doing nothing.

In June, the weekly production capacity of the Berlin factory was only 1,000 units, only 1/10 of the original production capacity plan, far lower than the 17,000 units of the Shanghai factory. Musk disclosed at the Q2 earnings report that it will take a few months for the Texas factory to reach 1,000 units per week.

According to a report in the Wall Street Journal in early July, Tesla’s poor performance in the second quarter was not only due to the epidemic. Supply chain pressures and high costs are also weighing on Tesla’s performance.

Not only are the Texas and Berlin factories weak, they are also creating high costs for Tesla. Musk once told the media, “The factories in Berlin and Austin (in Texas) are now huge melting pots, like there is a huge roar, which is the sound of money burning.” According to him, the two factories At least cost Tesla billions of dollars.

The overall high cost of the new energy vehicle industry is also eroding Tesla’s gross profit margin.

Average raw material costs for electric vehicles totaled $8,255 per vehicle as of May this year, compared with $3,381 per vehicle in March 2020, U.S. consulting firm AlixPartners said in a new report. up 144%.

Of course, macroeconomic factors are also a headache for the Silicon Valley Iron Man. The appreciation of the U.S. dollar has inevitably affected Tesla, which has a high proportion of its international business.

After driving through the dark and rough second quarter, can Tesla usher in a bright and smooth road?

dark road ahead

As the haze of the epidemic dissipated, Tesla’s production capacity recovered. According to data from the Passenger Federation, Tesla sold 78,000 units in June, a year-on-year increase of 138% and a record high.

But looking to the future, there are still many unfavorable factors on the way for Tesla.

The sci-fi FSD (Fully Autonomous Driving) supports Tesla’s “market dream rate”. But now, FSD has not been able to land, and the installation rate is only 11%, and Tesla has begun to “make a knife” in the autonomous driving department.

On July 14, Tesla’s head of autonomous driving, Andre Karpas, announced his resignation, and the core department lost its pillars. According to Bloomberg, Tesla has cut about 200 people in its self-driving division, causing an uproar in the industry.

In addition, Musk’s promised robots, pickups, Model 2, etc. have not landed, and the tickets have been repeatedly bounced.

This means that Tesla’s advantage as a first mover is diminishing, it is increasingly difficult to pull away from followers, and competitors have never slowed down in catching up with Tesla.

BYD, which surpassed Tesla in sales in the first half of the year, is using a “dumpling”-style intensive new and bottom-up approach to confront Tesla in the mid-to-high-end market. The June sales of BYD Han with an average price of more than 250,000 yuan (25,209 units) were almost the same as those of Model 3 (25,788 units). “Wei Xiaoli”, a new car-making force that is also taking the mid-to-high-end route, has also established a firm foothold in the 10,000-car club and continues to drive to the next milestone.

“We don’t have a demand problem, but we have a production problem.” Musk still emphasized the capacity dilemma on the earnings call. In the short term, the production capacity of the two new factories in Texas and Berlin is still in the ramp-up stage, and it will take time to reach the planned production capacity.

Supply chain issues are also still Musk’s nightmare. Both new factories are facing difficulties in battery pack production and engine component supply challenges. “It will take more effort to get these two plants to mass production than it would have been to initially build it,” Musk said.

Aruba expects supply constraints in the automotive industry chain to continue until 2024, and expects total global vehicle sales to fall to 79 million units this year (compared to 81.05 million in 2021).

In its annual “Car Wars” report, Merrill Lynch believes that Tesla’s electric vehicle market share will plummet from 70% today to 11% by 2025 because Tesla isn’t expanding its offering fast enough combination. Traditional automakers and new carmakers are expanding their product lineups, with Ford and GM both planning to surpass Tesla in electric vehicle sales in the U.S. around 2025.

At the end of May, Musk said in an interview with the Tesla Owners Club of Silicon Valley, “The bad things are happening one after another, and we are not out of the woods… Tesla’s main concern is how to keep the factory running, so that we can Employees can be paid normally without going bankrupt.”

In addition, Musk still feels “super bad” about the global macro economy, which he believes could be a “canary in the mine” moment that heralds a recession for the entire auto industry. This is also the direct reason for his 10% layoff.

In addition to the cloud over Tesla, Musk himself has been in trouble lately. The acquisition of Twitter is pending, and it is about to go to court with the Twitter team, which has attracted the attention of many investment banks. Analysts believe that if a mandatory takeover is ruled, Musk may have to sell more Tesla shares to raise capital, which would then take another hit to Tesla’s stock price.

The growth myth has been shattered, the Iron Throne has been loosened, and the midfield battle of new energy vehicles has just begun. Can Musk, who is in charge of Tesla’s steering wheel, break through the darkness of the road ahead?

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-07-21/doc-imizirav4745623.shtml

This site is for inclusion only, and the copyright belongs to the original author.