Welcome to the WeChat subscription number of “Sina Technology”: techsina

Text/Director of Dong

Source / Yuanchuan Technology Review (ID: kechuangych)

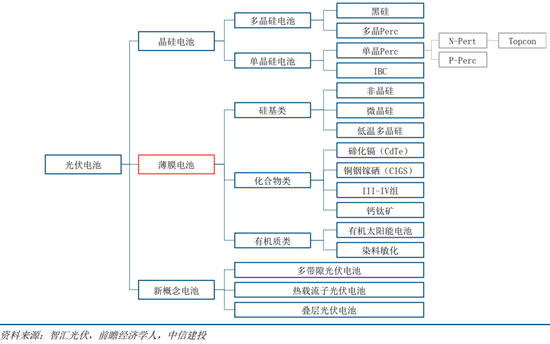

When it comes to solar cells, you can basically think of “monocrystalline silicon, polycrystalline silicon”, but there is actually another form, “thin film battery”: the use of compounds to convert light energy.

Thin-film batteries are not “unknown” either. In the 1980s, they also accounted for about 30% of the market size. Although the overall market was not large at that time, it felt a little rich on paper. But in 2015, thin-film batteries were highlighted again.

In 2015, when the Internet was in full swing, the richest man in my country was not the Internet industry, but the solar energy field, and it was also a “thin film battery”. Li Hejun’s Hanergy Thin-Film Battery Company was listed in Hong Kong, with a market value of more than 300 billion Hong Kong dollars at one time, and Li Hejun was also named the richest man in mainland China by Forbes in March with his worth of 160 billion yuan.

Regrettably, on May 20 of that year, a day full of love, foreign capital brazenly launched a short sale on Hanergy Films. More than an hour after the opening bell, it fell nearly 50%. Hanergy Film, which suffered a slash in half, also plunged in performance that year, with a net loss of 12.2 billion Hong Kong dollars, and then ushered in a suspension of more than three years, and finally had to be privatized.

The ups and downs of Hanergy Film Company seem to be another “richness on paper”. This has to make people question “whether thin-film power generation is feasible in the end.” In the technology-driven field, the interesting thing is that technology often dies and comes back to life, ushering in the second spring. So, what about thin-film batteries?

Why fail?

Let’s first review the reasons for the failure of thin-film batteries.

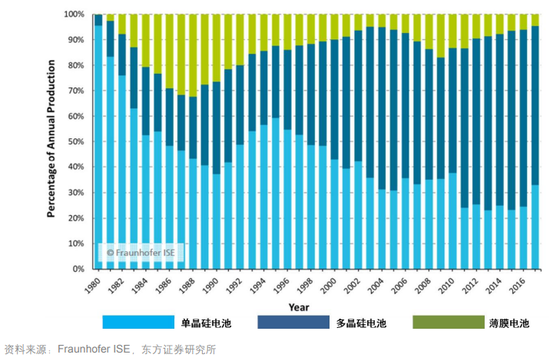

Compared with crystalline silicon cells, thin-film cells have the disadvantage of “low photoelectric conversion efficiency in mass production”, and the advantage is “simple process, low price, and good response to weak light”, that is, “cost-effective”. The market share of thin-film batteries has two peaks, one in 1988 and the other in 2009.

In the 1980s, thin-film batteries were based on silicon, with a market share of about 30% at the peak. But the overall scale of the industry was not large at that time, so there is no need to be too entangled. Eyes can focus on after 2004.

In 2004, First Solar, which focuses on thin-film batteries, achieved a breakthrough in the mass production of low-cost CdTe (cadmium telluride) batteries; at the same time as technological breakthroughs, the industry is also booming: Since 2000, Germany has taken the lead in developing solar energy in Europe, and the industry has become a success. For the better. In the process of the brutal growth of the industry, although the conversion efficiency of thin-film cells is about 7% lower than that of crystalline silicon, various technologies have also ushered in “rain and dew”.

At the same time, the cost-effective advantage of thin-film cells is outstanding: since 2003, the price of polysilicon has been rising, from US$25/kg to more than US$400/kg in 2008, which has led to a rapid increase in the cost of crystalline silicon cells. During this period, First Solar even raised the cost of thin-film cells to $0.98/W at the end of 2008.

Under the advantage of cost performance, the market once believed that in 2012, the market share of thin-film batteries is expected to reach 30%. But unfortunately, the cost advantage that thin-film batteries rely on most has disappeared.

In 2009, under the influence of the financial crisis, European and American countries reduced their solar subsidies, and the demand for polysilicon decreased. However, due to the large number of enterprises joining polysilicon production (the number of enterprises doubled to 400 in 2008 alone), the supply has expanded significantly. As a result, polysilicon prices plummeted.

The price of polysilicon has plummeted in a “self-destructive” manner, resulting in higher conversion efficiency and lower cost of crystalline silicon cells than thin films, and the fate of thin film cells is obvious. The subsequent breakthrough of LONGi in the field of monocrystalline silicon completely turned thin-film batteries into “industry leftovers”, with an industry market share of less than 5%. For example, they are used in non-mainstream scenarios such as shared bicycles.

But thin-film batteries have not died down. Since it uses active materials, its light absorption ability is very strong, which is two orders of magnitude higher than that of crystalline silicon. This principle is commonly understood, that is, the sunlight we see every day is the polymerization of light of various wavelengths such as red and purple. Thin-film batteries cover a wider spectrum than crystalline silicon batteries.

A wider spectrum also means a higher potential photoelectric conversion efficiency. When Hanergy chose thin-film batteries, it also had this consideration. Therefore, although thin-film batteries have a low market share, they have always been placed on high hopes and “just around the corner”.

The second spring in history

Before analyzing whether there will be a second spring for thin-film batteries, we can review several cases of the second spring. The first is “lithium iron phosphate” in the field of power batteries.

Lithium iron phosphate used to be the king in the field of electric vehicle power batteries, and its competitor was “ternary lithium technology”. Similar to thin-film batteries, lithium iron phosphate has the advantage of being “cheap”, while the disadvantage is its weak capability, low energy density, and short cruising range.

In 2016, the market share of lithium iron phosphate was as high as 60%. However, at the end of 2016, due to the national policy to incorporate battery energy density into the assessment system, ternary lithium batteries were more dominant and began to grow. In 2019, the market share of lithium iron phosphate fell to about 30%, but after 2020, the market share increased again, reaching about 55% in 2022.

Looking back, there are several reasons why lithium iron phosphate can usher in its second spring:

(1) Costs continue to fall: This is to continue to play strengths. From 2014 to 2019, the cost of domestic lithium iron phosphate batteries dropped by about 60-70%. In 2020, the price of lithium iron phosphate battery packs is even about 15% lower than that of ternary.

(2) Energy density improvement: This is a quick fix for shortcomings. From 2010 to 2020, the energy density of lithium iron phosphate batteries has doubled, from 90Wh/kg to 190Wh/kg. At the same time, the CTP technology of CATL, BYD’s blade batteries, etc., continue to improve lithium iron phosphate batteries in established The energy density of space is close to the current level of ternary battery packs in 2020, but the price is about 15% lower and safer.

(3) Market preference drive: This is to pull the opponent to the same starting line. After 2019, subsidies for ternary lithium batteries have been reduced, and the industry has begun to transform from policy-driven to market-driven. The C-end market is sensitive to “price”. As a result, Tesla, New Force, BYD, Wuling Hongguang and other manufacturers have increased the application of lithium iron phosphate batteries to reduce the total price and open up the market.

(4) Development of more scenarios: In addition to the use of new energy vehicles, 5G base stations, photovoltaic energy storage and other fields are also booming. Lithium iron phosphate is used as energy storage, although it is larger than the ternary (downstream does not care), but it is more The ternary battery is half cheaper, and the downstream prefers it.

In addition to lithium iron phosphate batteries, another “second spring” case that is currently taking place is “granular silicon”.

Granular silicon is a technology in the field of polysilicon production, and its opponent is the current “bulk silicon” technology of Tongwei and other companies. Granular silicon technology has lower theoretical cost and lower energy consumption, and is more suitable for downstream silicon wafer production. However, due to the difficulty of production technology and the general progress of commercialization, in the past few decades, the market accounted for only about 3%.

During this period, many companies worked hard in the field of granular silicon, such as Norwegian REC, American MEMC (later merged by SunEdison) and German Wacker. But the results were not good. REC lost money for a long time, SunEdison went bankrupt, and Wacker gave up. However, in 2021, granular silicon seems to be ushering in the second spring: financial and industrial capital investments such as Hillhouse and CMOC have increased; silicon wafer companies such as LONGi and Zhonghuan have also locked in production capacity.

The reasons why granular silicon can usher in the second spring include: (1) the price of polysilicon has risen sharply, the trial and error cost of new technologies has been reduced, and the benefits have increased, that is, the “rain and dew” under the rapid development of the industry; (2) technological breakthroughs, After years of accumulation, GCL-Poly and other companies have solved some of the previous technical difficulties.

To sum up these two cases, both of them are “opportunities in the change”: to play the long board, supplement the short board, have technological breakthroughs, have new players to promote, open new scenes, etc., and if it continues to condense, who is more Click on “Cost Reduction and Efficiency Improvement in Usage Scenarios”.

Where does the second spring of film come from?

With changes, there are new opportunities. The current thin-film battery has also ushered in several changes:

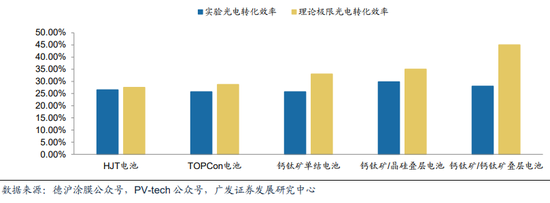

New breakthrough in technology: The biggest breakthrough in technology is perovskite. The conversion efficiency of perovskite has improved very quickly, and the conversion efficiency in the laboratory has reached about 25%. In the same way, crystalline silicon cells have been used for 40 years, and perovskite has only been used for 13 years. And it is highly scalable and can be used in combination with crystalline silicon cells to continue to improve conversion efficiency.

Moreover, perovskite maintains the advantages of thin-film batteries, and the production process is short, only 45 minutes in a single factory, while the comparison of crystalline silicon batteries requires three or four factories to cooperate and takes more than three days; in addition, the investment cost of 1GW capacity is 500 million yuan, about half of that of crystalline silicon cells. From the data point of view, perovskite batteries have significant advantages.

At the same time, thin-film battery technologies such as cadmium telluride and copper indium gallium selenide have achieved a mass production conversion efficiency of 19% after accumulation in the past. Although they are still behind perc batteries by 23%, they can also be mass-produced. , commercial application.

Driven by new players: In the first ten years of thin-film batteries, mainstream players were still overseas. According to the report of CITIC Construction Investment, in the field of cadmium telluride thin film batteries, the American company First Solar has an absolute leading advantage, with a market share of more than 90%. Chinese companies include Longyan Energy, founded in 2008 by Wu Xuanzhi, an expert in the field. It is one of the few companies in China that has achieved large-scale module production.

In the field of copper indium gallium selenide thin-film batteries, Japan’s Solar Frontier and China’s Hanergy are relatively leading, with their market share exceeding 30%.

Overall, the market share of Chinese companies in the thin-film photovoltaic cell industry is about 15%. Chinese players are still weak. Without the vigorous intervention of Chinese players, the progress of cost reduction and technology diffusion and maturity will be slow. But it is different in the field of perovskite, and Chinese players are enthusiastic.

In the field of battery cells, LONGi, Ningde, GCL and other battery leaders are all working hard; in terms of production equipment, Chinese companies are also leading the global industry. The participation of a large number of Chinese players will accelerate the progress of perovskite.

Open a new scene: The application field of thin-film batteries is expected to be “BIPV photovoltaic building integration”. Strictly speaking, BIPV is not a new scene. It has been developing since 2008. However, the economy is relatively low. For example, compared with the ground photovoltaic power station, the cost is about twice as high, and the power generation efficiency is 30%-50% lower, so the industry develops slowly and the scale is small.

However, the guiding force of the policy on BIPV is being strengthened. On the one hand, there are requirements. Under the carbon neutral policy, energy conservation and emission reduction is the key concern of every unit. By 2025, the photovoltaic coverage rate of new public buildings and factory roofs will reach 50%. %; on the other hand, there is encouragement. For example, Beijing subsidy for BIPV projects is 0.4 yuan/kWh (tax included), and the subsidy is 5 years.

With the strengthening of integration and the improvement of photovoltaic utilization, the cost of photovoltaics will also be integrated with the costs of building materials, building installation and operation, resulting in the effect of 1+1<2.

In the field of BIPV, thin-film cells will be more suitable than crystalline silicon cells.

Thin-film batteries are more flexible than crystalline silicon batteries, and can well meet the needs of architectural modeling; at the same time, they have good light transmittance and meet the needs of architectural lighting; in addition, through design, thin-film batteries can achieve a variety of colors, which is more expensive than the blue color of crystalline silicon batteries. More abundant, more meet the needs of architectural aesthetics. And the power generation efficiency is not bad. The report of China Securities Construction Investment shows that a project in Malaysia, the monthly power generation efficiency of cadmium telluride cells is 5.56% higher than that of crystalline silicon cells.

Of course, in the thin film battery, which is more suitable for BIPV, perovskite or cadmium telluride, we need to wait for the commercialization of perovskite to further observe. In addition, the current commercialization of perovskite has just started, and factors such as cost and large-scale preparation still need to be observed. But on the whole, if you compare the feasible methodology of the “second spring”, the second spring of thin-film batteries can be expected.

end

Change is the greatest opportunity. The demand side of photovoltaics will also usher in a broad space for development. With the insistence of many companies, especially companies such as Longyan, who have 14 years of industrial experience, the market share of thin-film batteries is expected to increase.

In this process, thin-film battery production lines must be newly built, which cannot be compatible with existing battery production lines. Therefore, if thin-film batteries are to develop, there is a high probability that a round of “capital expenditure” will be ushered in, and equipment manufacturers are important manufacturers. Shovel people.

The landing of BIPV requires both the photovoltaic side background and the architectural background to meet the architectural requirements of fire protection, waterproof, dustproof, shock absorption and so on. Manufacturers who can have both have more advantages.

Although photovoltaic is a technical product and needs technical promotion, the more important factor is “business ecology”. And back to the field of thin-film battery products, whether perovskite or cadmium telluride will run faster remains to be seen. But from the perspective of industry players, perovskites are undoubtedly more popular. Will there be a situation where the second spring of thin-film batteries has come, but the old companies that have been sticking to it before have not eaten meat?

Perhaps, there is another situation, that is, the second spring of thin-film batteries, but it is gone when it is sprouted, but this is still worthy of attention, and it is also worthy of enterprises to try.

The United States has also been trying to promote the development of the solar energy industry recently, but if the United States wants to catch up with China’s photovoltaic industry, it is somewhat similar to China’s catching up in semiconductors: chasing business and technology at the same time. Business pursues cost and application; technology pursues efficiency and scale. These two points are not easy for the US photovoltaic industry. After all, China’s photovoltaic industry has experienced all kinds of tragic inversion, leaving not only scars, but also barriers.

More importantly, changes are still taking place, and only with continuous changes can we not fall into the “cost killing” of the manufacturing industry, and allow technology to spring up and breed the seeds of various opportunities.

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-08-10/doc-imizmscv5673591.shtml

This site is for inclusion only, and the copyright belongs to the original author.