After the concept of the “Line Drawing School” fund manager was born last year, the concept has gone through a process of “hot speculation – swarming – ebb”, and the market has gradually become rational about the “Line Drawing School”.

I warned about the future sources of risk for such products in July last year:

1. How long can the shock style last, and how long can the transaction create excess returns?

2. The scale of the product is large, what should I do if the style rotation and position addition and subtraction cannot be done?

Some “Line Drawing Schools” could not control their withdrawal soon after being discovered by the market, while some “Line Drawing Schools” grew in size after being hyped up and were unable to create such an astonishing excess – even with basic foundations. People’s reflection: The so-called “line drawing school” is easy to mislead people, and historical performance does not represent future performance.

There is nothing wrong with the statement that historical performance does not represent future performance; but without historical performance, we cannot draw a picture of fund managers through changes in net worth, let alone predict their future style.

The market is full of volatility, but why does Christian Democrats always yearn for such an abnormal trend of the fund’s net value? Looking at the essence through the phenomenon, the core of this desire of Christian Democrats is actually the need for low drawdown and absolute returns .

Why is everyone so obsessed with controlled retracements?

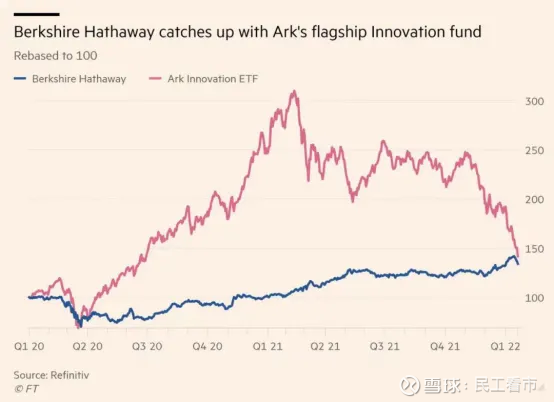

In the first quarter, there was such a picture circulating on the Internet:

The red line in the picture is the net value of the fund managed by Catherine Wood, an American Internet celebrity fund manager since 2020, and the blue line is the stock price trend of Berkshire, which is owned by Mr. Buffett.

There is no doubt that Sister Mutou’s income curve looked very sexy at one time, and the excess was huge, but in the end, it returned to the mean, and it came to the same destination as Buffett, who had been steady and steady all the way.

Looking at the two yield curves, although the final yield is similar, the process of Ms. Mutou is very tortuous. If these are the curves of two public funds investing in A shares, which one would you prefer?

There is no doubt that Christians who invest in the red line have a high probability of being hanged on the top of the mountain, while those who invest in the blue line are more likely to make money.

Even if you are a base person who has held two products from the beginning, the holding experience will be completely different. Sister Mutou’s products have huge fluctuations and drawdowns. Without a big heart, it is easy to fall asleep at night.

There is a saying in the NBA: Offense wins the regular season, defense wins the championship.

The same applies in fund investment: if the fund manager is good at offense, it is easy to run out of extremely high returns in stages, which are seen by many people, but once the retracement is not well controlled, the fund manager will rush in at the highest moment of the fund manager. The people may be hopeless.

And many investors also misunderstand the investment concept of “absolute return”. Absolute return is a concept, not “absolute profit”. The so-called absolute return refers to taking the risk-return ratio as the top priority in investment. Focusing on odds over odds provides a long-term upward low volatility, low drawdown yield curve.

The reason why many former “line-drawing” fund managers seem to have turned over is that they are not essentially making absolute returns (especially those with low bottom-up turnover and infrequent equity positions swinging), but It just happens that the investment style is more in line with the market, which creates an illusion that the net worth is very silky. Once the market style begins to change, the volatility of the portfolio will increase.

Essentially I don’t think they are wrong, it’s just the market’s wishful thinking that they are “line-drawers”.

If you want to get a better holding experience, you can’t just look at the equity curve to filter, but you must combine the maximum drawdown, volatility, equity position changes and investment ideas to explore.

What I want to say today is a “grey horse” fund manager who is rarely mentioned and has little publicity and is hidden in big factories:

Yu Bo.

First look at the net worth trend:

(Data source: Tiantian Fund, as of August 23, 2022)

Does it feel normal? It has only made 70% in the past three years. You must know that the funds that have doubled in the past three years are like crucian carp crossing the river in the whole industry. This performance can only be regarded as above average.

But if I tell you that in the past three years of Fuguo Xinyi’s management, the biggest drawdown is 10.7% , do you still think this performance is ordinary? It looks ordinary, but it’s actually amazing.

The following conditions were screened with the Jiuquaner APP and found:

The only one in the whole market.

Of course, if you relax the maximum drawdown or yield, there are still many products that have done a good job in the return, but what is even more terrifying for Yu Bo is the ability to swing equity positions.

The 70% yield in the past three years is based on the premise that the stock position is 40% to 60% all year round.

Yu Bo’s position management ability is very strong (to put it bluntly, it is a large-scale timing, which can also be called asset allocation). The market fluctuates greatly in the first quarter of each year for three years.

According to what she said before, on the eve of the Spring Festival in 2020, after observing that there were cases in Wuhan, and at the same time seeing that the market trend was weak and consumption led the decline, based on the experience of SARS, it was judged that the new crown epidemic was a small probability event at that time. However, once the outbreak occurs, the impact on the market and net value will be very large, and considering the inability to trade during the Spring Festival holiday, the product will be reduced in advance. Then, under the impact of the second wave of the epidemic, considering the increase in macroeconomic risks at home and abroad in 2022, based on the drawdown control system and the avoidance of unknown risks, we also actively reduced positions to reduce the risk of drawdowns, thereby smoothing the huge fluctuations in net worth.

In this era of bottom-up, emphasis on stock selection and downplaying of timing, Yu Bo does not shy away from doing position management by himself. In fact, he must have a top-down perspective for absolute returns.

(Data source: Wind, as of August 22, 2022)

Compared with the CSI 300, it is more intuitive. It can be found that every time the market pulls back sharply, she can quickly stop the pullback, and when the market starts to rise, she can quickly keep up. A quote from the interview:

Low drawdowns are one of the core sources of long-term compounding.

Frankly speaking, the current track-type fund managers are everywhere, and Yu Bo’s offensive ability is not particularly outstanding, but her defensive ability is almost “perverted”.

This is really what a flexible allocation fund manager should look like in my mind.

As an additional mention, since May this year, as major fund investment and advisory portfolios have been launched on third-party channels, I have also bought almost all public equity fund investment advisors in the market, and found a very interesting thing. Various fund investment advisors like to allocate products from Wells Fargo, and they do not focus on one or two products:

CEIBS’ investment advisors are paired with Zhang Xiaowei’s Fuguo Tianhe, ICBC Credit Suisse’s with Wang Yuanyuan’s Fuguo consumption theme, Huaxia with Sun Bin’s Fuguo value advantage, Cao Wenjun’s Fuguo Quality Development in the South, Xu Youhua/Fang Min’s Fuguo CSI Dividends And Wang Yuanyuan’s rich country consumption theme, CCB matched Cao Wenjun’s rich country transformation opportunity, E Fund matched Sun Bin’s rich country value advantage and Wang Yuanyuan’s rich country quality life, Bo Shi matched Yang Dong/Zhang Fusheng’s Fuguo Clean Energy, Wang Menghai/Wang Wanyi The Fuguo Dividend Selection and Tang Yiheng’s Fuguo Tianyi… The long-distance running Lao Siji and the selected Mesozoic under Huabao Securities are respectively equipped with Yuan Yi’s Fuguo State-owned Enterprise Reform and Zhang Xiaowei’s Fuguo Ruize, look, don’t follow the trend, choose The two are rather biased.

I am very pleased that Yu Bo did not appear in the mainstream attention, and most of her representative product Fuguo Xin income is also held by institutions, not many retail investors; the second quarterly report shows that her management scale is only less than 5 billion. , is now a typical “grey horse” fund manager.

In fact, we can no longer be obsessed with looking for “line drawing schools”. High returns and low drawdowns are often not compatible. Find out your expected returns and risk preferences to find the most suitable products for you. I don’t judge who is more powerful than Mrs. Wood and Buffett. Some people like low drawdowns, while others can handle high volatility. But for most ordinary people, smoothing the yield curve is more important than winning high yields. For fund bloggers, the speed of digging out “grey horse” fund managers needs to be accelerated, because blue-chip fund managers cannot hide for long.

(Risk warning: Equity funds are high-risk varieties, and investment should be cautious. This material does not serve as any legal document, and all information or opinions expressed in the material do not constitute investment, legal, accounting or taxation. The content in this document makes any guarantee for the final operation suggestion. In any case, I am not responsible for any loss caused by anyone using any content in this information. The operation time of our fund is short and cannot reflect the development of the stock market. All stages. The past performance of fixed investment does not represent future performance. Investors should fully understand the difference between regular fixed investment and zero deposit and withdrawal of funds. Regular fixed investment is a simple and easy way to guide investors to make long-term investment and average investment costs. However, regular fixed investment cannot avoid the inherent risks of fund investment, cannot guarantee investors to obtain returns, and is not an equivalent financial management method to replace savings.

Before investing in a fund, investors should carefully read the fund’s “Fund Contract”, “Prospectus” and other fund legal documents, fully understand the risk-return characteristics and product characteristics of the fund, and fully consider their own risk tolerance. On the basis of the situation and listening to appropriate opinions, rationally judge the market, prudently make investment decisions based on factors such as your own investment objectives, duration, investment experience, and asset status, and independently assume investment risks. There are risks in the market, and you need to be cautious when entering the market. The fund manager reminds investors of the principle of “buyer is conceited” in fund investment. After investors make investment decisions, investors are responsible for the investment risks caused by the operation of the fund, fluctuations in the listed trading price of fund shares and changes in the net value of the fund. The past performance of the fund and its net worth are not indicative of its future performance. )

This topic has 0 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/9371934674/229137504

This site is for inclusion only, and the copyright belongs to the original author.