Welcome to the WeChat subscription number of “Sina Technology”: techsina

Text / Zhou Weiwei

Source: Good-looking Business (ID: IGreatBI)

From 2012 to 2022, Baidu will continue to develop AI, with a cumulative R&D investment of more than 100 billion yuan. After the Q1 financial report last year, Robin Li mentioned that with the growth of artificial intelligence business, Baidu’s non-advertising revenue will exceed advertising revenue in the next three years.

“Artificial intelligence has been on fire for so many years, and commercialization has always been one of its soft underbelly, and the lack of good business prospects will lead to stagnant growth of startups, huge losses, difficulties in financing and listing, and large companies will become less and less grounded.” .

This passage comes from a speech delivered by Baidu founder Robin Li recently at the 2022 World Artificial Intelligence Conference. It is almost a true portrayal of Baidu’s AI business over the years.

As early as 2012, Robin Li was thinking about whether AI technology had ushered in a historical turning point, so Baidu promoted the establishment of a deep learning research institute.

2013 was the year that Baidu AI went from planning to implementation. They set up AI research centers in China and the United States, and have since embarked on the road of “deadly fighting” AI.

By 2022, Baidu has been deeply engaged in the field of artificial intelligence for ten years, with a cumulative R&D investment of over 100 billion yuan. Baidu’s revenue has also grown from 22.3 billion yuan in 2012 to 124.5 billion yuan in 2021.

However, in the past ten years, Baidu’s market value has been maintained at around $50 billion for a long time, and even hovered at $30 billion.

Baidu’s revenue mainly includes Baidu Core and iQiyi. Baidu’s core revenue mainly comes from two parts: online marketing (search/information flow advertising business) and non-online marketing (intelligent cloud, Apollo, Xiaodu speakers and other innovative businesses).

Online marketing has always been the largest source of Baidu’s revenue. Its revenue in Baidu’s core revenue has long maintained at more than 80%, and its current proportion is still over 70%. Baidu AI’s contribution to revenue is still very limited, so it is even a drag on Baidu’s market value in the capital market.

In March 2021, Baidu will be listed on the Hong Kong Stock Exchange with the “first AI share”. After the release of the Q1 financial report in 2021, Robin Li mentioned on the conference call: With the growth of artificial intelligence business, Baidu’s non-advertising revenue will exceed advertising revenue in the next three years.

This means that Robin Li already has a relatively clear timetable for the commercialization of artificial intelligence. Even if Baidu’s revenue grows by 10% every year, the revenue scale in 2024 can reach 160 billion yuan.

By then, if the non-advertising revenue exceeds half, it is to achieve a scale of 80 billion yuan. In 2021, Baidu’s non-advertising revenue will be 21.2 billion yuan, a year-on-year growth rate of 71%.

What is the commercialization path of Baidu’s non-advertising business? At present, Baidu has drawn a gradually clear map: Baidu Intelligent Cloud + Autonomous Driving (cooperating with OEMs, building cars, and sharing unmanned vehicles).

Behind Li Yanhong’s timetable, how will Baidu Intelligent Cloud and autonomous driving drive commercialization? What are their odds?

The task of “Second Curve” is handed over to the intelligent cloud

The “Second Curve” theory proposed by the famous British management guru Charles Handy is regarded as the “Bible of Growth” by many companies.

Looking at the world, among the top 10 Internet companies by market value, Alphabet, Microsoft, Amazon, Ali, and Tencent are all developing cloud computing as the second growth curve.

Who is Baidu’s second growth curve?

In the past, the answer to this question was AI, but the commercialization of AI has been slow to land, and it can only be regarded as Baidu’s third growth curve in the end.

For a long time in the past, Baidu has been looking for the second growth curve. Cloud computing, short video, live broadcast, etc. were all options.

Judging from Baidu’s latest external caliber, they finally locked Baidu Smart Cloud as the second growth curve.

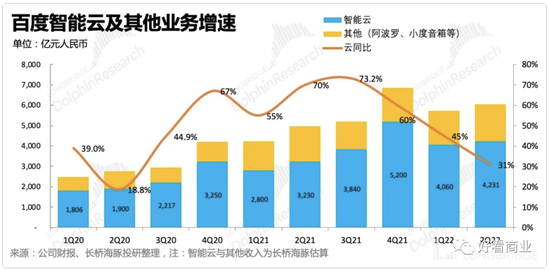

According to this year’s Q2 financial report, Baidu Group achieved a total revenue of 29.6 billion yuan. After excluding iQiyi, Baidu’s core revenue was 23.2 billion yuan; Baidu’s intelligent cloud revenue was 4.2 billion yuan, accounting for 18.1% of Baidu’s core and 18.1% of Baidu’s total revenue. It accounts for 14% of revenue, which is Baidu’s largest single source of income outside advertising.

In May of this year, Li Yanhong announced a new round of cadre rotation. The former MEG (Mobile Ecology Business Group) head Shen Dou was transferred to be in charge of Baidu Smart Cloud Business Group (ACG), and CTO Wang Haifeng no longer served as the head of ACG.

Adjusting ACG to be independently responsible by Shen Dou means that Baidu’s emphasis on and investment in the intelligent cloud business has reached a new level.

For the past ten years, Baidu Intelligent Cloud has been a long process of constantly getting to know oneself and finding oneself.

In the past ten years, the cloud business of peers has been running fast, and there is a clear gap with Baidu Smart Cloud in terms of revenue scale and market share.

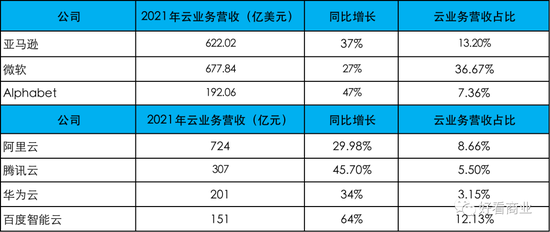

Data source: Financial reports of various companies, Tencent Cloud revenue data from Dolphin Investment Research estimates

Data source: Financial reports of various companies, Tencent Cloud revenue data from Dolphin Investment Research estimatesIn 2021, Baidu Smart Cloud’s revenue is 15.1 billion yuan, about 1/5 of Alibaba Cloud’s and 1/2 of Tencent Cloud’s in the same period.

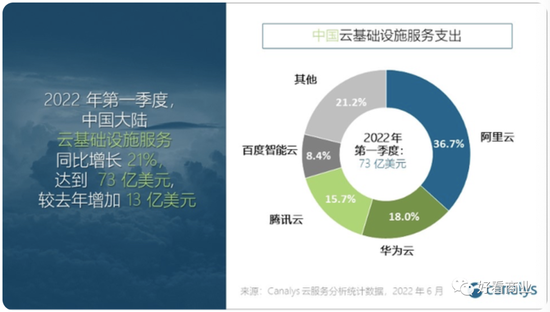

According to the China cloud computing market report released by Canalys, in Q1 2022, Baidu Smart Cloud’s market share will be 8.4%, the smallest share among the “Four Chinese Clouds” formed by Alibaba Cloud, Huawei Cloud, and Tencent Cloud.

However, Baidu Smart Cloud’s growth rate is ahead of its peers. In the past 8 quarters, Baidu Intelligent Cloud’s revenue growth rate has remained above 30%.

In Q1 and Q2 this year, Baidu Smart Cloud revenue increased by 45% and 31% year-on-year, respectively. During the same period, Alibaba Cloud grew by 12% and 10%, respectively. Enterprise services including Huawei Cloud grew by 27.5% year-on-year in the first half of this year.

Next, the resources in the hands of Baidu Smart Cloud will support it to continue running, and it is expected to outperform the top three of the “Four Clouds in China” in terms of growth rate.

“AI + cloud” is the differentiated label and advantage that Baidu Intelligent Cloud has found for itself. According to IDC’s report, as of the first half of this year, Baidu Smart Cloud ranked first in the domestic AI public cloud market for six consecutive quarters.

Intelligent transportation, smart city, industrial Internet and traditional financial industry are the advantageous areas of Baidu Intelligent Cloud. For example, in the financial field, the six state-owned banks of China, agriculture, industry, transportation, construction, and postal savings, more than a dozen joint-stock commercial banks, hundreds of city commercial banks, and traditional financial institutions such as insurance, securities, and asset management are Baidu Smart Cloud customers.

With different customer structures, cloud service providers may face very different growth scenarios. In recent years, the regulation of the Internet industry has become stricter, which has affected the performance of Tencent Cloud and Alibaba Cloud, which account for a large proportion of Internet customers, to varying degrees.

Most of the customers are from traditional industries, which has become an advantage of Baidu Intelligent Cloud.

Entering 2022, Tencent, Alibaba, and Huawei are all reducing costs and increasing efficiency, and more emphasis on profitability rather than scale and speed. Under this tone, Alibaba Cloud and Tencent Cloud will not emphasize growth as in the past. In particular, Tencent Cloud has voluntarily abandoned some loss-making projects, and its revenue has experienced negative growth for two consecutive quarters.

The strategy of Baidu Intelligent Cloud is different. In the Q2 conference call, Baidu management made it clear that Baidu has ample cash and will continue to invest in intelligent cloud in the next step. As of the end of Q2, Baidu’s cash and cash equivalents were 42.533 billion yuan.

Now that Li Yanhong has handed over the task of Baidu’s “second growth curve” to Shen Dou, the running of Baidu Smart Cloud can’t stop, and it has to continue to “jitter”.

Apollo Realization Timeline

In May last year, when Baidu released its 2021Q1 financial report, Robin Li announced for the first time in a full-staff letter that Apollo’s three commercial monetization paths were clarified: providing Apollo autonomous driving technology solutions for OEMs; building cars; and sharing unmanned vehicles.

At present, the three commercializations of Baidu Apollo are accelerating, and a preliminary timetable has been given.

Image source: Good-looking business is organized according to public information

Image source: Good-looking business is organized according to public informationLi Yanhong once mentioned that in the second half of 2021, Apollo intelligent driving will usher in the peak of mass production, and a new car will be launched every month. In the next 3-5 years, it is expected that the pre-installed mass production will reach 1 million units.

Apollo’s Lego-style automotive intelligent solution includes four series of products: “Intelligent Driving, Intelligent Cabin, Intelligent Map, and Intelligent Cloud”. It can provide customized solutions according to the intelligent mass production needs of different levels of car companies.

Taking Apollo Smart Driving as an example, it includes the world’s first L4-level autonomous driving capability-based driving domain solution ANP and the world’s first mass-produced L4-level autonomous driving parking domain solution AVP.

Huaxing Capital once predicted in 2021 that by 2025, ANP alone is expected to contribute 28 billion yuan in revenue to Baidu.

Jidu is Baidu’s car-making project. It was established in March 2021, and Baidu and Geely jointly hold shares. Jidu’s target market is family cars, and its products are priced at more than 200,000 yuan. The core competitiveness of “high-end intelligent” Jidu is.

On June 8, Jidu officially released its first automotive robot concept car ROBO-01. The production version of this car will be officially delivered in the second half of 2023.

According to Xia Yiping, CEO of Jidu Automobile, the exterior design of Jidu’s second model will be unveiled at the Guangzhou Auto Show at the end of 2022, and delivery is expected to begin in 2024.

In August this year, Jidu Automobile also announced the “2880 Plan” – in 2028, Jidu will achieve a product lineup of 6 models, with the ability to deliver 800,000 vehicles throughout the year, and the production capacity and sales plan will be consistent.

The 6 models have achieved the sales target of 800,000 units, which means that each model will become an explosive model with annual sales exceeding 100,000 units. For a company that has only been established for 7 years, the dream is full and the challenge is very big. After all, judging from the practice of “Wei Xiaoli”, they are still working hard for the annual sales target of 100,000 vehicles.

Compared with selling self-driving solutions and building cars, sharing unmanned vehicles is a faster mode of realization. In August 2021, Baidu released a newly upgraded self-driving travel service platform – “Carrot Run”.

As of July 20, 2022, Carrot Run has covered more than ten cities including Beijing, Shanghai, Guangzhou, Shenzhen, and Chongqing, with a cumulative order volume of 1 million, making it the world’s largest self-driving travel service provider.

Baidu launched the sixth-generation mass-produced self-driving car Apollo RT6 in July, with a target mass production cost of 250,000 yuan. According to the calculation of Baidu executives, according to the average price of 20 yuan per order, Carrot Run will only need 12 orders per day to break even. Baidu claims that with the mass production and operation of the Apollo RT6, taxi fares can be reduced by half.

According to the plan, by the end of 2023, Carrot Run will deploy at least 3,000 autonomous vehicles in 30 cities, covering 3 million users; in 2024, Apollo RT6 will be put into operation on a certain scale, covering 65 cities in 2025 and 2030. 100 cities.

According to JPMorgan’s forecast, Baidu Luokuaipao will achieve bicycle profitability by 2025.

In general, Baidu Apollo has a gradually clear realization path and preliminary timetable, but it will still take several years for it to achieve large-scale commercial revenue.

Robin Li himself also believes that the commercialization of artificial intelligence still needs to grope in the dark for some time.

The price of gambling

Looking at Baidu’s financial report, you will find that the company is almost “paranoid” in R&D investment.

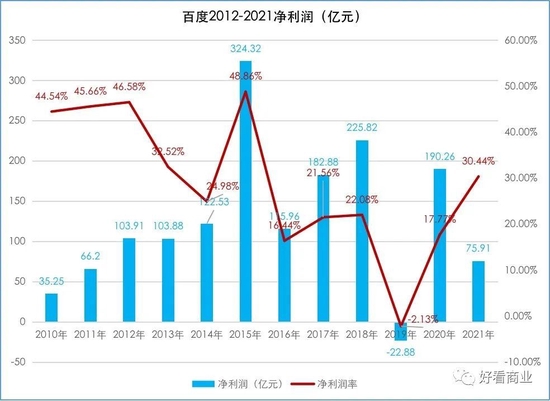

In the ten years from 2012 to 2021, Baidu has invested 125.217 billion yuan in R&D, accounting for 16.34% of its cumulative revenue and 105.09% of its cumulative operating profit.

In the past ten years, Baidu’s R&D expense rate has been above 15% almost every year; in 2021, Baidu’s core R&D expense rate will reach 23.21%, which is leading among large Internet technology companies in the world. Huawei has always been known for its heavy R&D investment, but in 2021, Baidu’s core R&D expense ratio will lead Huawei by 0.8 percentage points.

Since 2012, Baidu has continuously invested heavily in research and development in the field of AI, which has allowed it to accumulate significant advantages in AI patents, and the number of patent applications and authorizations continues to lead.

According to the “Analysis Report on China’s Artificial Intelligence High-value Patents and Innovation Driving Forces” jointly released by the National Industrial Information Security Development Research Center and the Electronic Intellectual Property Center of the Ministry of Industry and Information Technology in October 2021, the number of Baidu AI patent applications has exceeded 13,000, and the number of AI patents authorized More than 3,600 cases, ranking first in China in terms of AI patent applications and authorizations for four consecutive years.

However, the cumulative investment of hundreds of billions in research and development has also “eaten” Baidu’s profits and market value.

Since 2012, after two consecutive years of technology investment, Baidu’s net profit margin has dropped sharply. By 2014, Q2 had dropped to 22.9%, while the net profit margin in 2012 and before remained at around 45%. The decline in net profit margin has caused Baidu’s market value to shrink sharply.

But Robin Li doesn’t seem to care about the reaction of the capital market.

In early 2015, he responded in an interview with the media, “In just two years, the profit margin has dropped so much, which actually shows a determination, that is, I am willing to spend money, I am willing to invest, I don’t care what Wall Street thinks, I I don’t care if my stock price falls in half or more, I’m going to make it happen.”

In March 2021, Baidu was listed in Hong Kong for the second time, and Robin Li was still emphasizing technical investment in his speech at that time.

He said, as a company that has always believed and loved technology from day one to today, we are willing to invest for the long-term and for the future. Even in the most difficult times, we persist: when we have 1 yuan, we will invest in technology; if we have 100 million, we will invest in technology; if we have 10 billion, we will still invest in technology.

In Li Yanhong’s external speech, he has been emphasizing Baidu’s “technology belief” and trying to “change the world with technology”. He believes that this is an era that re-crowns technological innovation; only by continuously investing in technological innovation can we seize the opportunities that belong to Baidu.

So, when did this era start rewarding Baidu?

If Baidu achieves what Li Yanhong said “non-advertising revenue exceeds advertising revenue” as scheduled in 2024, it means that Baidu’s “dark night walk” will not be too long.

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-09-12/doc-imqmmtha6963702.shtml

This site is for inclusion only, and the copyright belongs to the original author.