Author | Wan Chen

Editor | Zheng Xuan

The metaverse boom that has lasted for more than half a year seems to have reached an inflection point of development.

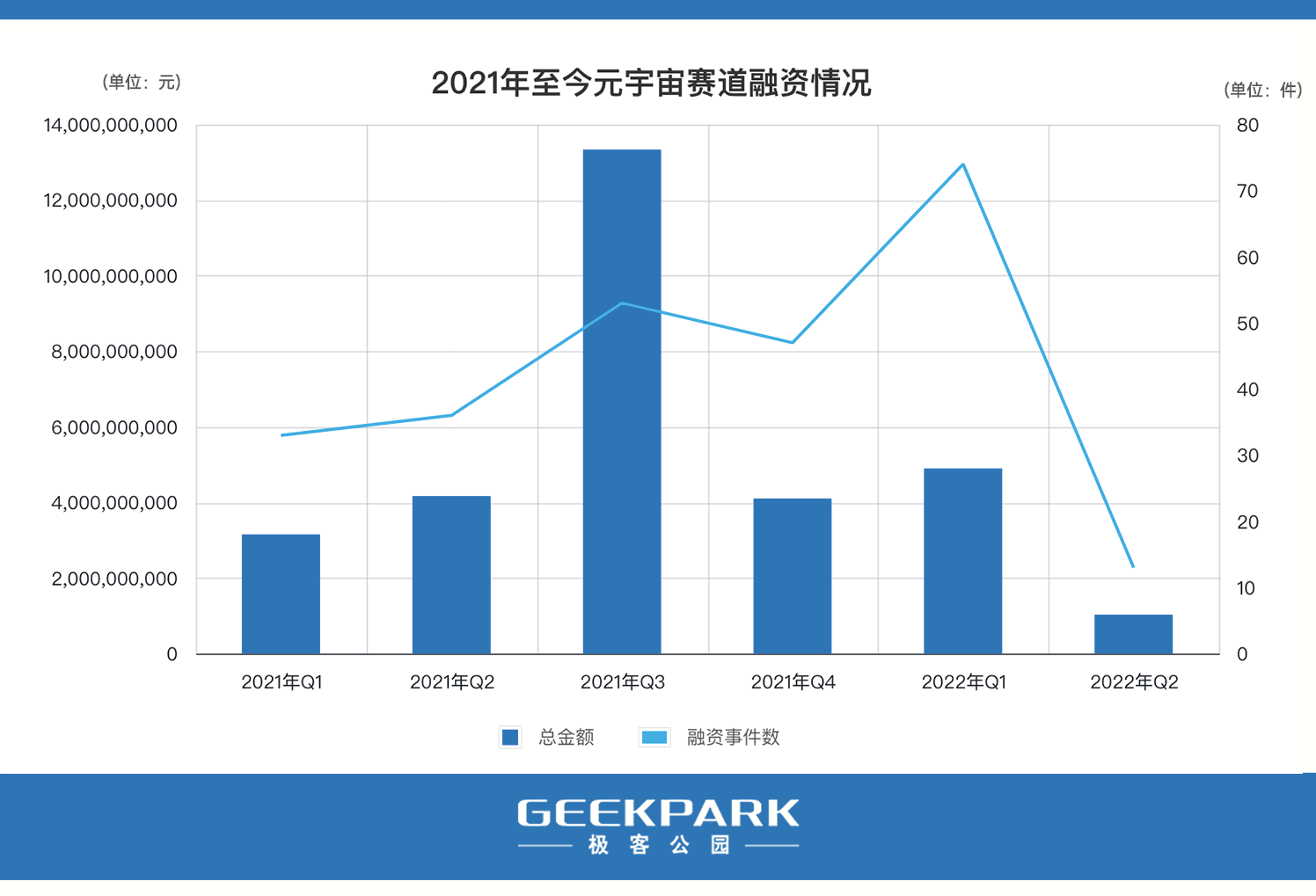

Since the second half of 2021, the domestic Metaverse track financing has accelerated. Based on public information, Geek Park has completed a total of 187 financings since Q3 in 2021, with a total financing of more than 30.6 billion yuan. Even after deducting 9 billion yuan from ByteDance’s acquisition of Pico, the industry still attracted nearly 21.6 billion yuan in financing in 10 months.

However, compared with the previous six months, the financing speed of the Yuan Universe track has slowed down to a certain extent in the past two months, and the news of the big factories taking action and deploying this track has also decreased. This is hard not to recall the last wave of VR/AR boom in 2015 and 2016. After losing the favor of capital, the VR/AR industry fell from spring to winter in a few months.

After 8 months, is this wave of Metaverse fever really going to ebb?

01 Metaverse cooling down?

Many practitioners in the VR/AR field can feel that: entering the second quarter of 2022, starting from March 2022 to be precise, the almost crazy investment boom in the metaverse in the past six months seems to have begun to cool down.

Production: Geek Park (Note: 2022 Q2 financing data is as of April 30, 2022)

As shown in the picture above, according to the public information, after ByteDance acquired Pico at the end of August, in the three quarters of Q3, Q4 in 2021 and Q1 in 2022, the number of domestic Metaverse Circuit financing events was 53 and 47 respectively. and 74, a significant increase from the first two quarters of 2021 (33 and 36).

A large number of VR/AR startups that were established around 2016 and were active in the last wave of VR/AR boom, but whose financing pace has slowed down in the past two years, such as Xiaopai Technology, Dapeng VR, Zhongqu Technology, VEER, Immersive World, Lingxi Weiguang, etc., all completed a new round of financing during this period.

However, since March, the financing rhythm of the Metaverse Circuit has slowed down. Geek Park statistics found that in March and April 2022, there were 22 and 13 financings on the Metaverse Circuit, respectively, a slight decline compared to the previous months.

A senior practitioner who has been in the industry for many years told Geek Park that he also feels that the financing fever in the industry has cooled down recently. The most obvious signal is: the number of screen refreshes in the circle of friends to congratulate peers for financing. At the end of last year and the beginning of this year, it was often once a week or even several times a week. Recently, the frequency has dropped to once or twice a month.

After communicating with several industry insiders and investors, it is generally believed that there are three possible reasons:

At the beginning of the year, it was reported that large Internet companies would be restricted from investing in and M&A abroad. Investors were worried about this and became more cautious.

After several years of great waves in the industry, there are not many high-quality companies that have survived. They have been robbed by investors in the past six months, and now there are few projects worth selling.

The main focus of the Metaverse track is the US dollar fund. Recently, the US dollar fund has been in a difficult situation and its ability to sell has weakened.

Investment enthusiasm in the primary market is waning, raising one concern: Will the metaverse craze ebb like it did in 2016?

02 How did this wave of Metaverse fever come about?

To figure out whether the metaverse craze has cooled, we must first understand how the craze came about.

From the perspective of most ordinary people, metaverse fever is the explosion of metaverse concept stocks in the secondary market. In September last year, stimulated by several major industry events, a group of Metaverse concept stocks ushered in a surge. In the craziest few weeks, a company can pull up several daily limits with just a little bit of metaverse concept.

VR/AR-related public companies are naturally the biggest winners. GoerTek, which is the OEM for two major VR manufacturers, Meta and Sony, saw its share price rise by more than 20% in a few days; NetEase, whose share price fell to the bottom, also rebounded by nearly 20% in two weeks.

However, the VR/AR industry is still in the early stage of development, and there are not many listed companies, which also makes a group of listed companies with the concept of becoming the biggest winners.

The most representative of them are the two mobile game companies Zhongqingbao and Tom Cat. After throwing out two game development plans under the banner of the Metaverse, Zhongqingbao’s stock price once rose from 8 yuan to 42 yuan, an increase of 42 yuan. Up to 400%; Tom cat also rose from 3 yuan to nearly 6 yuan when it was the highest, an increase of nearly 100%.

Tom Cat

Investors are speculating on concepts, and it is the investors in the primary market who really invest in the industry.

As mentioned above, starting from Q3 in 2021, the financing of the Metaverse Track in the primary market has accelerated, including ByteDance, Tencent, NetEase, Perfect World, Sanqi Interactive Entertainment and other Internet manufacturers have successively shot, which is also stimulating investment in the primary market. The immediate reason for the influx of people to this track.

There are two main reasons for investors: First, investment opportunities for consumer Internet have gradually disappeared in recent years, and the market lacks a high-quality track to absorb investors’ funds. This is why large institutions have turned to ToB’s industrial Internet and hard technology. And new consumption and other tracks, Metaverse, as the next-generation Internet ecology, has enough imagination and ceiling, and the huge industrial chain also means rich investment opportunities.

Second, Metaverse companies generally lack a mature business model, and it is difficult to enter the secondary market within a few years, and it is difficult to exit after investing. This is the reason why investors were reluctant to touch this track in the past. However, Internet giants have entered this track, and their investment and mergers and acquisitions of startups in this field have provided investors with a new exit channel.

In other words, the entry of big factories into this track is the direct cause of the boom in the primary market, and it is undoubtedly ByteDance and Tencent that pulled the trigger. ByteDance doesn’t need to go into too much detail here, and Tencent’s layout is actually earlier.

As early as 2020, Ma Huateng emphasized in an internal letter that the “full true Internet” similar to the concept of the Metaverse is the key to the next generation of Internet. In addition, for the acquisition of Pico, there are rumors in the industry that Tencent participated in the bidding, but the price offered by ByteDance was too high, and Tencent felt that it was not worth it and gave up.

Here is a question worth thinking about: For big Internet companies such as ByteDance and Tencent, what is the real reason for deciding to start deploying VR/AR?

Investing in cutting-edge technologies and preparing for the competition in the next ten years is an important part of Dachang’s strategic investment. In this sense, it is believed that the Metaverse (or VR/AR, or the true Internet) is the next generation of the Internet, and it is the fundamental reason why ByteDance and Tencent began to deploy.

But why choose the time point of 2021? In fact, Tencent has made plans for VR/AR many years ago. After Facebook acquired Oculus for $2 billion in 2014, in the next few years, Tencent organized several teams to develop VR hardware and VR games. And VR social products, and even low-key launched a VR social product Solar VR.

At that time, the attempts were basically just scratches. Today, Tencent and ByteDance are investing a lot of resources into this track. The information that Geek Park has learned from a number of industry professionals who have communicated with Tencent and ByteDance is: Meta China’s VR hardware shipments have crossed the threshold of 10 million units, which is the direct reason for stimulating ByteDance, Tencent and other big companies.

Zuckerberg walks through crowd wearing VR equipment

There is a commonly used term in management science called “flywheel effect” – in order to make a stationary wheel roll very difficult, you need to push in circles at the beginning, each circle is very laborious, but it reaches a certain “critical point” After that, the gravity and momentum of the flywheel will become part of the driving force, and even if you don’t try too hard, the flywheel will roll on its own, and it will roll faster and faster.

The flywheel effect is often used to describe the Internet economy and the platform economy. For the VR ecosystem that Meta and Pico are building, hardware and content are like the two flywheels that drive the industry – more hardware ownership means that developers can earn more money from developing a good content, and they are willing to Invest more human and material resources to develop higher-quality content; and the more good content, in turn, will stimulate more consumers to buy hardware.

However, in the early days, this process was very slow: insufficient hardware shipments made it difficult for developers to make money and were unwilling to invest; and lack of good content caused users to lack purchase intentions, and even old users were constantly losing.

In the early stage, capital was needed to promote, and in the later stage, the self-hematopoietic development of the industry accelerated. The “tipping point” of the VR industry was communicated with a number of leading entrepreneurs in the industry a few years ago. The consensus is that 10 million high-end VR devices will be shipped annually. It will become a turning point in the development of the industry.

From 2015 to 2018, before Oculus launched Quest, the total shipments of Sony PSVR + HTC Vive + Oculus Rift + other brands were around one million units, and the annual increase was not high, which is why other domestic or overseas The reason why big factories were reluctant to invest in the VR/AR track in the past few years.

However, with the emergence of Oculus Quest, coupled with the promotion of the epidemic, shipments of high-end VR hardware products began to rise sharply. According to data from SuperData, the shipment of high-end VR hardware in 2019 was close to 3 million units. In 2020, due to the decline in PSVR sales and insufficient Oculus inventory, the total shipments will not increase much, but in 2021, it will be released with the Oculus Quest 2. , the total sales of this product alone reached nearly 10 million units.

The shipment of VR hardware has reached an important critical point, becoming an inflection point in the development of the metaverse industry. However, due to the inability of Meta to enter China, the development of the domestic VR market has begun to lag behind the global market, but this is also an opportunity for big companies such as ByteDance and Tencent. Meta has flattened the technical pit, educated the market, and raised a group of Developers will greatly reduce the uncertainty of domestic investment and development.

This is why ByteDance is willing to spend real money and buy Pico, which is the only consumer-grade VR hardware company in China, although its shipment volume is only a few tenths of Meta.

03 VR hardware shipments soar, the domestic market catches up

Now that we understand the source of this wave of meta-universe vents, let’s talk about whether it is true heat or false fire.

In today’s metaverse, it’s hard not to be reminiscent of the last wave of VR/AR boom in 2015-2017. After Facebook acquired Oculus heavily in 2014, a wave of VR craze in China quickly set off. A number of local VR startups such as Dapeng, Ant Vision, 3Glasses, and Leke have successively obtained hundreds of millions of financing. Xiaomi, Huawei, Microsoft, NetEase, etc. Big factories also entered the game one after another, and also gave birth to the VR demon stock Baofeng – 36 consecutive boards after listing with the VR concept, with a market value of more than 40 billion yuan at the highest.

This craze quickly ebbs in less than two years, and the speed is comparable to that of shared bicycles. Looking back at today’s review, all the heat is only at the capital level, and the entry of big manufacturers is just a taste. The reason why the capital hot money has not been converted into the driving force for the development of the industry, in the final analysis, is because the shipments and holdings of high-end VR hardware are lower than expected after the money is burned.

There are various product forms of VR hardware, but they can be roughly divided into high-end and low-end. Low-end hardware is represented by Cardboard developed by Google engineers. In the early years, Samsung GearVR, Baofeng Magic Mirror, and Oculus’ first-generation all-in-one GO were all low-end VR products. They were characterized by low price and low threshold, but the picture was blurry and processing. The performance of the device is poor, and you can only play some rough mobile VR games or watch panoramic videos.

Representatives of high-end hardware include the early Oculus Rift, PSVR, HTC Vive, and the later Oculus Quest, with higher screen resolutions and processors using more powerful PCs, game consoles, or custom processors, so they can be used to play games. Create better, more realistic VR content.

In 2016, the VR industry also claimed to have tens of millions of shipments, but most of the products sold were low-end VR products ranging from dozens to hundreds. The shipments of high-end VR products were only about 1 million units. More than half of it flows to B-end customers such as VR experience stores. Except for PSVR, the number of VR hardware that is really in the hands of consumers is very limited.

This is why, as mentioned above, the shipment of Oculus Quest, a high-end VR hardware, has reached a milestone of tens of millions, which will have a huge impact on the industry, and whether the domestic market can break out depends on the shipments and ownership of VR hardware. is the decisive factor.

Oculus Quest 2 | Image credit: Amazon

After ByteDance completed the acquisition of Pico, it invested a lot of resources to promote VR hardware. Whether ByteDance’s own Douyin, major e-commerce platforms, and even the Spring Festival Gala can see Pico’s advertisements.

Such a promotion campaign quickly paid off. It is understood that before being acquired by ByteDance, the total sales of Pico for more than six years was about 500,000 units. Pico’s new target is as high as 1 million units.

Some time ago, an industry exchange summary from a brokerage said: ByteDance raised Pico’s annual sales target in March this year, from 1 million units to 1.8 million units. The increase in the target is mainly due to the better sales data in the first quarter, which not only exceeded the initial expectations, but also grew rapidly month-on-month.

However, this statement was denied by ByteDance. The relevant person in charge replied to Geek Park saying: It has been repeatedly confirmed from the business department that ByteDance has not raised its Pico sales target, and this year (target) is still 1 million units.

But whether it is 1.8 million or 1 million, it is a milestone figure for the country. The agency predicts that global VR hardware shipments will reach about 15.7 million units in 2022, with 1.8 million units representing an 11% global market share and 1 million units having 6%. Although there is still a certain gap compared with the smartphone market (about 22% of the world in 2022), it has narrowed significantly compared with 2019 and 2020.

More importantly, the demonstration effect of Byte and Pico is attracting more important players to enter the game, accelerating the development of the domestic VR/AR industry. Previously, Tencent acquired mobile phone manufacturer Black Shark. It is rumored that the team’s focus has been reset to XR hardware; Huawei, OV, etc. are also accelerating the deployment of VR/AR hardware. Once the time is right, mobile phone manufacturers with mature brands, channels and production capacity , will be an important contender for XR hardware.

Sales are the last word, and this wave of Metaverse has only just begun.

This article is reprinted from: https://www.geekpark.net/news/301949

This site is for inclusion only, and the copyright belongs to the original author.