Welcome to the WeChat subscription number of “Sina Technology”: techsina

Why do Internet platforms like to force open business?

Author丨Sakuragi Editor丨Tsukimi

Source: New Entropy

The Internet financial circle, which has become calm, is once again rippling.

On September 15, Zhang Qingsong, deputy governor of the central bank, said at the 11th China Payment and Clearing Forum that it is necessary to continue to implement and strengthen the supervision of large-scale payment platform enterprises. According to incomplete statistics, since the beginning of this year, JD.com, Duxiaoman, Ctrip, Ping An Puhui and other companies with multiple Internet small loan licenses have carried out the integration and removal of relevant licenses.

However, unlike the gradually tightening supervision and the continuous rectification of the financial business of major manufacturers, ByteDance still shows a sign of overweight this year. On April 28, 2022, Shenzhen Zhongrong Microfinance Co., Ltd., a subsidiary of Byte, underwent an industrial and commercial change, and the company’s registered capital increased from 5 billion yuan to 9 billion yuan. On July 22, the original Douyin small loan product dou was officially renamed Douyin Monthly Payment in installments. Judging from the company’s extensive promotion, the Douyin payment system has completed a phased layout.

The changes in Douyin’s financial payment business are not unrelated to its rapidly developing e-commerce landscape. Douyin E-commerce was established in June 2020. Last year, some industry analysts predicted that Douyin E-commerce GMV has reached nearly 800 billion. Entering 2022, at the second Douyin E-commerce Ecological Conference, Douyin E-commerce President Wei Wenwen announced the Douyin e-commerce business data from May 1, 2021 to April 30, 2022: GMV reached 3.2 times that of the same period, and over 10 billion items were sold.

However, with the rapid development of Douyin’s payment finance, Douyin’s financial disputes also began to appear.

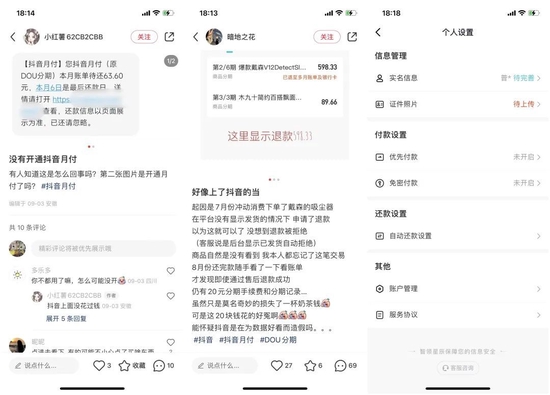

Since the 921 Douyin Good Things Festival, social platforms such as Xiaohongshu and Weibo have received a lot of complaints from users, and Douyin will open its related online loan business without users’ knowledge. “During the live broadcast, due to the speed of rushing for goods, I opened online loan services such as Douyin monthly payment without my knowledge, and then, it didn’t take long for people to call me to claim whether there was a need for borrowing.” A Xiaohongshu user complained.

01

“Inexplicably opened” Douyin small loan

“Douyin shopping forces users to open online loans by default, and it has been activated twice by default.” Recently, according to media reports, Douyin user Mr. Zhang reported that he was in a hurry to pay for purchases through Douyin’s live broadcast room, and found himself without any prompts. Douyin monthly payment was opened.

If you turn off the business, there will be a second forced opening. On the Xiaohongshu platform, a user said, “After the Douyin monthly payment is closed for the first time, there will be a second time. As long as you buy something on Douyin, you will jump out first. Yin doesn’t understand this, and he doesn’t even know if he has a loan on his back.” There are hundreds of related complaints.

Douyin’s consumption scene is more “short and smooth” than the purchase scene of search e-commerce such as Taobao and JD. Few users are unable to take into account the risk warning of the small loan attribute of Douyin monthly payment in a short period of time. In the words of industry insiders, such a design is more like an inducement operation to “take advantage of the chaos” for users.

In order to promote the monthly payment function of Douyin, the activation process is extremely simple, and the activation of Douyin monthly payment does not even require complete real-name information, and ID card photos are not required.

Zhang Qiang, a senior practitioner in the financial industry, when evaluating Douyin Monthly Payment, believes that when customers open Douyin Monthly Payment, they only select the installment payment method and password-free payment by default on the customer payment interface to induce customers to open installments. Clearly displaying the installment agreement and the authorization for credit inquiry, and failing to let the customer confirm the authorization to inquire about the credit inquiry through a clear interface is actually out of compliance.

According to Article 10 of Chapter 2 of the “Measures for the Administration of Credit Investigation” of the People’s Bank of China, credit investigation agencies shall clarify the principles of information collection and their respective rights and responsibilities in obtaining customer consent and information collection through clear forms such as agreements. Article 12 of the Measures stipulates that the collection of personal credit information by credit reporting agencies shall obtain the consent of the information subject, and clearly inform the information subject of the purpose of collecting the information.

In conclusion, imperfect information flow, unclear rights and responsibilities, and overly succinct reminders have all become key factors for consumer complaints. From the results, such a design also brings inconvenience to many users. Xiaohongshu blogger Li Meng (pseudonym) claimed that because he was in the exam and needed to issue a credit report, he did not expect that he was accidentally loaned when placing an order on Douyin, which affected the credit results and thus the test scores. .

According to the black cat complaint, there are as many as 14,000 complaints related to Douyin monthly payment. Among them, the impact of credit reporting is countless, from being harassed by phone calls, to leaking personal information, from forced opening, to difficulty in closing functions. As the basis of social credit, credit issues often affect people’s lives in all aspects.

Secondly, another contradiction in the chaos of Douyin monthly payment comes from the mismatch between payment methods and consumption forms. From the principle of Douyin monthly payment, the original intention of its design is still the credit card logic of installment payment, which is based on offline consumption. scene, but its applicability is also being challenged when it moves online.

Taking the common pre-sale products of Douyin e-commerce as an example, there will be a misalignment between the delivery time of completing the order and the fixed repayment date of Douyin monthly payment. The item has not been received or will be returned. If it involves refunds, returns, and the remaining repayments after refunds, the complexity of the process will increase exponentially.

A closer look at the function and design of Douyin Monthly Payment will give people a sense of urgency. This kind of panic is constantly being pulled to the front of the magnifying glass when Douyin’s daily active users have exceeded 700 million in 2022. .

02

chasing, reaping

Douyin monthly payment is not special among many Internet small loan products.

Products such as Alipay Huabei and Meituan Monthly Payment have many overlaps with Douyin Monthly Payment in terms of positioning and functions. Even the experience that users complained about in Meituan Monthly Payment was repeated in Douyin Monthly Payment. Someone once used “Meituan’s red envelope “temptation”, how many people can seriously read the credit payment contract?” to describe the contradiction between Meituan Monthly Payment and users when it was expanding. It forms a perfect confrontation with the dilemma of Douyin Monthly Payment.

The official name change of DOU installment to Douyin Monthly Payment will be on July 22, 2022, which is 2 years later than Meituan. The time lag means that the cost of the education market is higher than that of other giants.

From the perspective of actual operation, Douyin’s small loan business is almost everywhere subject to mainstream payment platforms, from the user’s mind, payment scale to related functions. According to analysts’ forecasts, the market shares of WeChat Pay and Alipay Pay in 2022 will be between 35%-38% and 44%-48%, respectively. The highly overlapping product channels, from the perspective of user habits and business habits, consumers who have transferred from e-commerce platforms such as Taobao to Douyin are also more inclined to the original payment methods such as Alipay. How to break the game has become a major problem for Douyin after completing its financial layout.

From the actual operation point of view, in addition to the chaos such as forced opening, Douyin monthly payment and rest assured borrowing and pulling new activities continue on the platform. Among them, rest assured borrowing has launched “invite friends to earn red envelopes”, as long as the user successfully invites one person to activate You can get a red envelope of 30 yuan if you borrow the amount with confidence; for every new user you invite to successfully open Douyin monthly payment, the user can get a monthly payment of 500 yuan, and the invited friends can also get up to 15 yuan for instant discount coupons.

In terms of effect, the growing scale of Zhongrong Small Loans and the rapidly growing GMV of Douyin e-commerce both confirm the feasibility of this approach.

On the other hand, from the inside, Douyin’s huge content traffic obviously has more room for imagination. In addition to e-commerce, advertising business, financial business and other directions, before the small loan and other payment businesses are not expanded and perfected, almost It is impossible to fully digest the flow of traffic in its own ecosystem. In other words, Douyin still plays the role of the “God of Fortune”. How to maximize the effectiveness of its own ecology, as a relatively late-developed Douyin Finance, obviously needs to bear heavier responsibilities.

At the same time, the pressure of byte growth did not give Douyin much time.

At the end of 2021, the commercial product department of ByteDance held a general meeting. At the meeting, it was mentioned that the advertising revenue of ByteDance’s domestic business had stopped growing in the past six months. As the fastest-growing company in the mobile Internet in recent years, the stagnation of the advertising business, which accounts for about 70% of its revenue, almost means that the ceiling era experienced by the giants has also fallen mercilessly on their own heads.

The Douyin e-commerce, which the company regards as the second growth curve, also needs to press the fast-forward button under pressure.

In the era of ceilings, algorithm recommendations directly attack human weaknesses, and financial services provide ultra-convenient means of payment. Under the synergy of the two, ordinary people have little resistance. From the perspective of the company, such a joint effort has made the addictive short video of Douyin, and it has also achieved the rapid development of Douyin e-commerce finance.

In the face of the upcoming shopping festival, when people see the credit limit being raised again, what exactly do they use to control their desire to consume, which has become a difficult problem for Douyin and many e-commerce platforms.

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-09-28/doc-imqmmtha9128732.shtml

This site is for inclusion only, and the copyright belongs to the original author.