Before the reorganization of the container shipping industry in 2016, the companies in the industry that could provide investors with long-term earning returns were: OOIL, CMA CGM, Hapag-Lloyd, and Maersk. In addition to these four companies, other companies have their own problems. Therefore, when the industry is reshuffled, inefficient companies will either go bankrupt, such as Hanjin, or be acquired, such as CMA CGM’s acquisition of President Steamship, or merge, such as Japan’s Kawasaki, Merchant Marine, and Mitsui Mitsui merged into ONE. The only one that has undergone two changes is COSCO SHIPPING Holdings. In 2016, COSCO Container Lines and China Shipping Lines merged, and in 2018, they completed the acquisition of OOCL. If the merger is to clarify the main business and establish the direction, then the acquisition of OOCL is a qualitative leap. . As shown below:

It can be seen from the comparison of changes in average container revenue that the efficiency of COSCON has gradually improved since 2018, and has remained at the same level as OOCL.

For the earlier history, I looked through the annual reports of OOCL in recent years. This is more objective information than the annual report of Haikong before 2016, because the reorganized Haikong is more like OOCL than China COSCO. In terms of affiliation, OOCL is a subsidiary of Ocean Holdings, accounting for nearly half of Ocean Holdings’ profits; in terms of operational efficiency, OOCL is basically the world’s best container shipping company, and after Ocean Holdings acquired OOCL, COSCON’s The operational capability and efficiency are also close to those of OOCL; in terms of business types, OOCL has historically focused on container transportation, and also operates part of the terminal business, which is in line with the current Haikong. It can be said that COSCO SHIPPING Holdings is a larger-scale OOCL backed by mainland China and the State-owned Assets Supervision and Administration Commission.

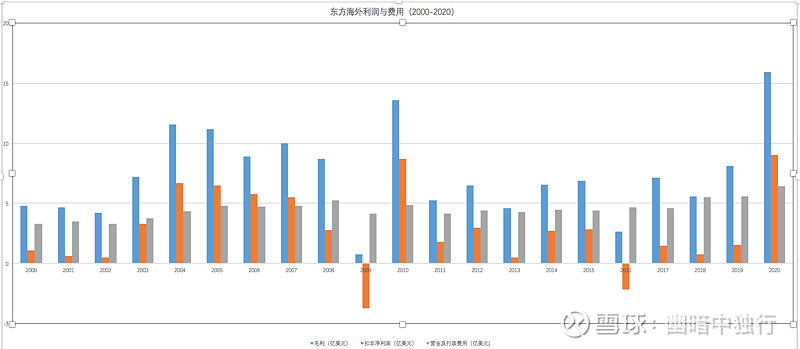

The historical profit data of OOCL is as follows:

First, gross profit. From 2000 to 2020, OOCL ’s gross profit was positive in all years, and there was never a negative gross profit . The lowest gross profit was US$76 million in 2009, followed by US$262 million in 2016. And there are only two years when gross profit was below average.

Second, deducting non-net profit, there were only two losses in the past 20 years. It was the two years when the gross profit was lower than the average. In 2009, it lost 376 million US dollars and in 2016, it lost 219 million US dollars. The loss was mainly due to the inability of gross profit to cover operating and administrative expenses.

To sum up, it can be deduced that even in the most extreme cases, the upper limit of the loss limit will be less than the operating expenses of the company , specifically: management expenses, sales expenses, research and development expenses, etc.

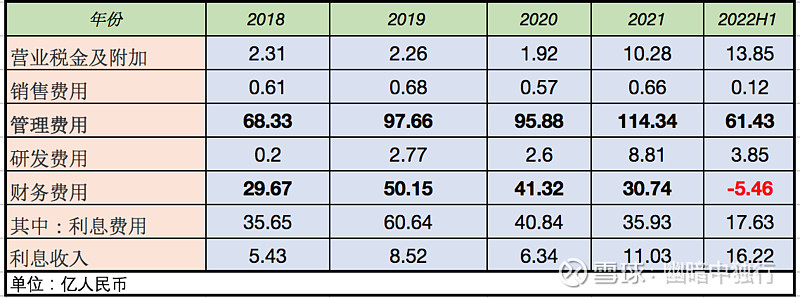

Look at the figure below, the current operating expenses of Haikong:

Since OOCL was consolidated after July 1, 2018, 2019 and 2020 can be seen as similar to the future. That is to say, the operating expenses of Haikong are mainly management expenses and financial expenses. In terms of management expenses, since 2019, Haikong’s management expenses have been roughly around 10 billion.

For financial expenses, Haikong has made nearly 200 billion net profit in the past two years, the operating cash flow has been greatly improved, and the balance sheet has been greatly improved. The debt ratio will be lower than 50%, and financial expenses will change from a cost in the past to a source of income today. In the first half of 2022, revenue of 500 million has been brought in, and the actual revenue of 900 million in a single quarter in the second quarter. According to the data brother’s calculation, the revenue from Haikong’s financial expenses will reach more than 5 billion yuan per year in the future. For details, see @laviedeParis’s article : After the capital and qualifications are complete, the rise of another Chinese advantageous industry

Over the years, the operating expenses of OOCL have not changed much. In 2006, the capacity was less than 300,000 TEUs, and in 2017, the capacity was nearly 700,000 TEUs, and the operating expenses were around US$470 million. The following chart shows the historical capacity of OOCL:

It can be deduced that even if the scale of Haikong continues to grow, the operating expenses and management expenses will not increase significantly, and will basically remain at the current level.

In addition, in addition to containers, Haikong also has an extremely stable port business, contributing a relatively stable net profit attributable to the parent of around RMB 1 billion every year:

Take a closer look at what happened in 2009 and 2016?

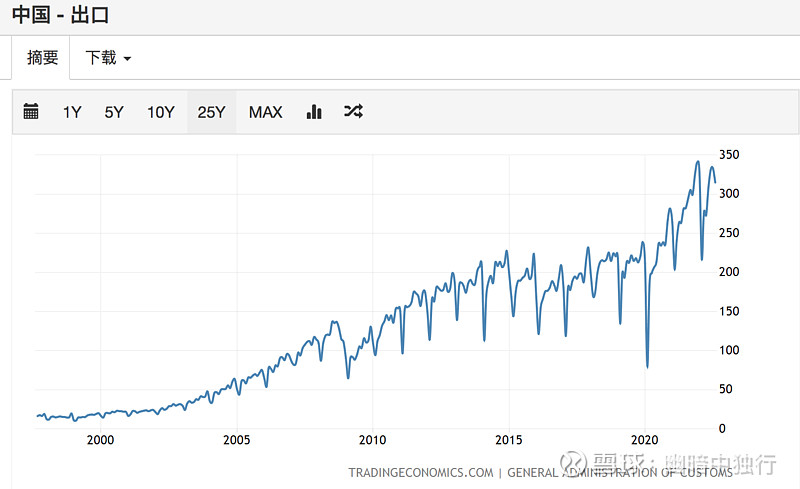

In 2009, the subprime mortgage crisis in the United States spread, the global economy was damaged, demand fell sharply, and freight rates fell. It can also be seen from China’s export data that the decline in exports in 2009 and the duration.

In 2016, the price war initiated by the industry giant Maersk reached the most tragic moment, the superimposed demand slowed down, and finally Hanjin went bankrupt, triggering a wave of industry mergers and reorganizations.

So, looking from the past to the future:

First, if there is a financial crisis similar to that in 2009, and demand drops sharply, how will Haikong deal with the situation? Haikong’s current shipping capacity is 2.8 million TEUs, which is a little more than nine times that of OOCL in 2009. By analogy, under the same conditions, the gross profit of Haikong’s container business in 2009 was roughly US$680 million, equivalent to 4.75 billion yuan. Then, adding more than 5 billion financial expenses, excluding operating costs such as management fees, it can roughly break even, and the port can also contribute 1 billion net profit attributable to the parent. Therefore, the probability is above the break-even point. (If you take into account the increase in gross profit brought about by the new capacity of Shanghai Holding, and the operating expenses that will not increase too much, the profit is even more certain.)

In reality, the situation similar to 2009 has been rehearsed in reality. In the first half of 2020, the global demand dropped sharply due to the epidemic. However, due to the suspension measures of the three major alliances, the gross profit of Haikong in the first half of 2020 was 6.9 billion. If it is extended to The annual profit is 13.8 billion yuan. If financial expenses are added, the annual profit is also about 8 billion yuan.

That is to say, if a situation similar to the financial crisis in 2009 occurs, after the current industry and the company’s own conditions change, Haikong will still be difficult to lose money in the most extreme situation, and it will be difficult to have an impact on its balance sheet.

Second, if there is a similar industry crisis in 2016, competition will intensify and demand will be sluggish. In 2016, the gross profit of OOCL was US$265 million, and the shipping capacity was 570,000 TEUs. The current shipping capacity of OOCL is about 5 times that of OOCL, and the gross profit of OOCL is about 9.3 billion yuan. In addition to financial non- and port income, Haikong can still make a profit of more than 6 billion.

To sum up, Haikong’s bottom line has been raised, and it can generally remain profitable in the most extreme financial crisis.

Discuss whether what will happen in the future, insisting that there will be no losses, and it is not necessary. The key is how much you lose when you lose and how much you earn when you are profitable. In today’s boom, it can make hundreds of billions of profits, and in extreme situations that rarely occur, it can be no loss, or the limit of loss is less than 10 billion. Isn’t this a change?

If you put aside the fluctuations and look at the long-term center, if you compare 22 years to 2003-10, the long-term center of Haikong will be converted to around 50 billion. If you consider the future as 12-19 years, the long-term center of Haikong will be converted into around 20 billion. Isn’t this a change?

One more question, will shipbuilding and capacity growth necessarily lead to losses? If so, why has OOCL’s capacity increased year by year for the past 20 years, but only suffered losses in extreme years? If not, then why the loss of China COSCO and the bankruptcy of Hanjin?

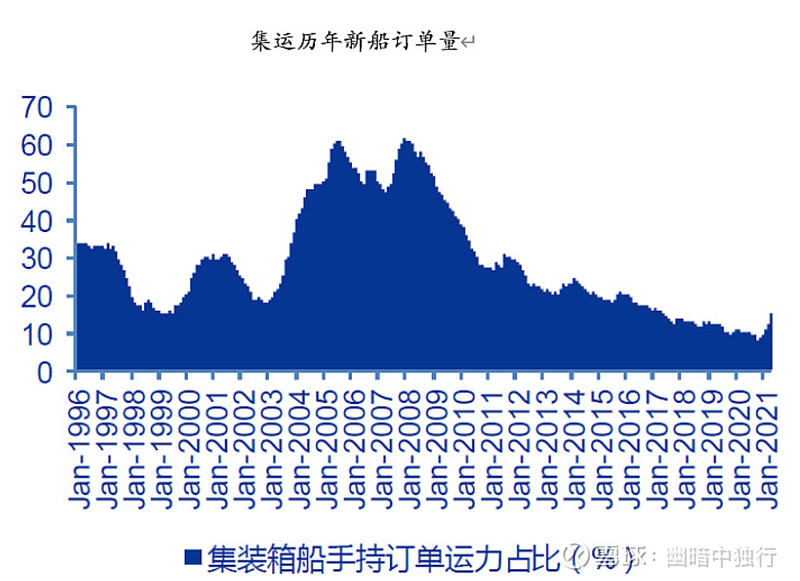

As shown in the figure above, in terms of hand-held orders and capacity delivery cycle, the largest growth in capacity delivery is in the second half of 2007 and the second half of 2010. If the impact of order delivery is so great, then the freight rate should drop sharply and continue to be depressed after this time, and the company should be in a loss, but in fact, OOCL made normal profits in 2007 and 2008, except for 2009, which was affected by the financial crisis. In addition, in 2010, it obtained excess profits due to demand recovery after the impact of the financial crisis, as well as normal profits in 2011, and subsequent normal profits in 2012-2015. That is, capacity growth will flatten freight rates, but it will not lead to losses. What really leads to losses is the mismatch between the aggressive management capabilities and management strategies of shipping companies and the environment. That is to say, like China COSCO and South Korea’s Hanjin, the asset-liability ratio is too high, and the business strategy is too aggressive. And the current Haikong, the leverage has gone, after the bottom of the cycle, the operation is relatively conservative. Now that the freight rate has fallen, there is no more radical reason.

Finally, for the global trade-related business of container shipping, it is difficult to escape the macroeconomic cycle, but the industry and enterprises have indeed changed.

First, the increase in industry concentration, the improvement of the competition pattern, and the countermeasures such as price protection and co-storage, such as the 20-year epidemic and the 22-year Shanghai epidemic, the industry can take effective measures to stabilize the situation when faced with predictable unfavorable conditions. short-term price fluctuations.

Second, companies are improving their balance sheets. For example, when Haikong Holdings has significantly reduced its interest-bearing liabilities, its assets and liabilities are less than 50%, and it has a large amount of cash in hand, its financial expenses have been greatly reduced, and the previous costs have become profitable. Business operations can be more stable.

Third, the supply chain crisis in 2021 will bring companies to attach importance to supply chain stability. For large cargo owners, the importance of supply chain stability is far greater than the cost. The chairman of LONGi Co., Ltd. visited Haikong for two consecutive years, as well as the mutual visits between many companies and Haikong. This is not just a discussion. A price, which brings about the continuation and growth of the future long-term contract ratio, provides the underlying foundation for future profits.

Fourth, the company’s own operating capabilities have been improved. Since the acquisition of OOCL in 2018 by Haikong, not only in terms of transportation capacity, but also in terms of operating capabilities.

Operational efficiency of the world’s best container shipping companies:

There are 17 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/5273564401/231976089

This site is for inclusion only, and the copyright belongs to the original author.