Real estate has always been a topic that cannot be avoided by investment banking stocks. If real estate is not regulated and allowed to rise and fall, it will have a huge impact on the economy. The impact of real estate is reduced, which is conducive to the future market development of the banking sector.

This is a very useful set of data, let me share with you how to interpret it:

Interpretation:

A macroscopic view

From a macro perspective, China’s real estate regulation has achieved good results, preventing the last crazy surge. The main goal of current regulation is to prevent housing prices from plummeting. Under the condition of stable housing prices, gradually ensure delivery, destock, and gradually reduce the scale, so as to achieve real estate The slow landing of the economy. For bank stocks, the specific manifestation is that with the growth of M2, the scale of real estate loans in the bank loan structure gradually decreases.

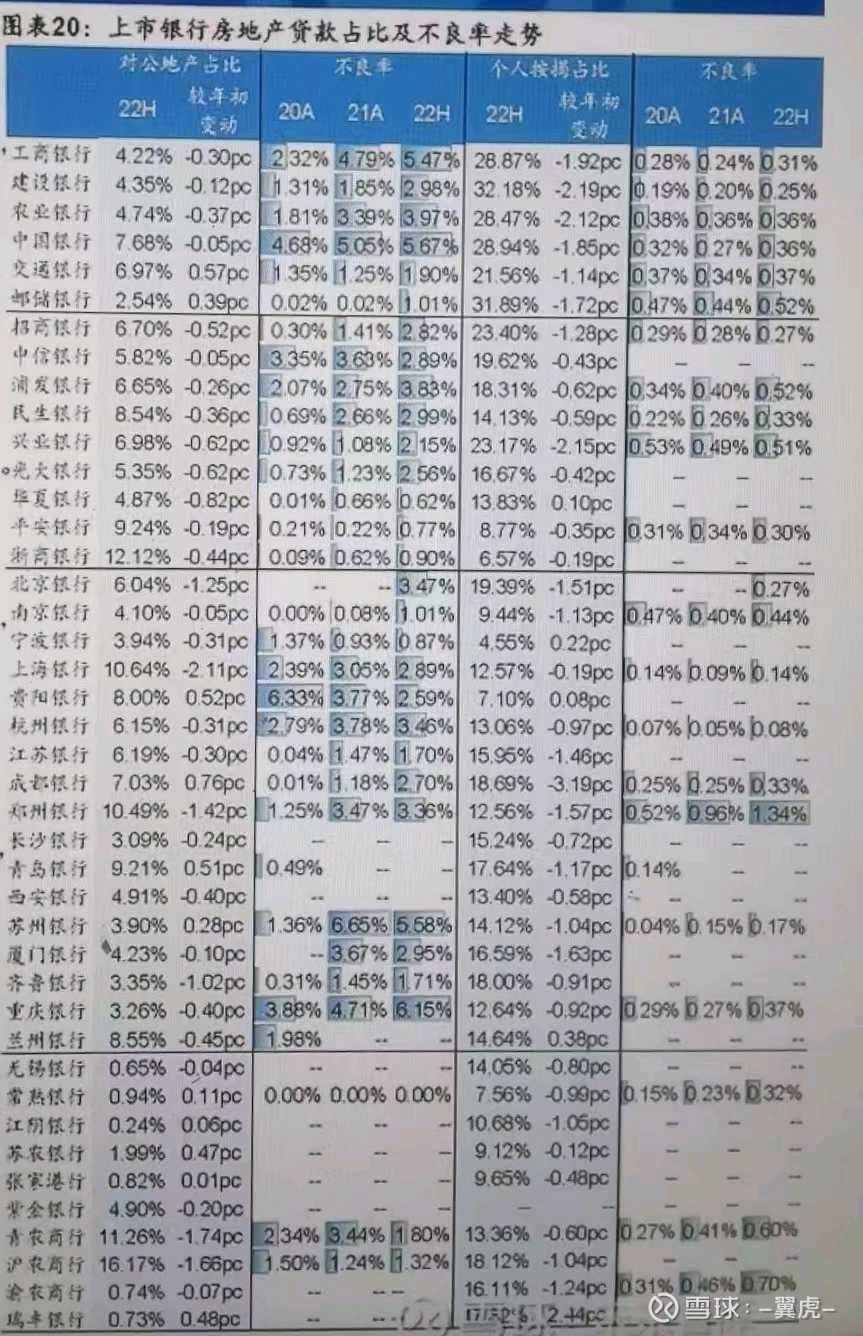

2. Data Analysis of Real Estate Corporate Loans

The bad situation of corporate loans in real estate is closely related to real estate companies. In the past two years, real estate regulation has put enormous pressure on them, which is the main source of bad debts in real estate.

1. Scale

From the perspective of the proportion of loans, some banks are relatively high, and the impact of real estate will be relatively large, such as Zheshang, Zhengzhou, Qingnong, Hunong, etc.;

Some banks have very few, so the impact of real estate is almost negligible for them, such as Wuxi, Changshu, Jiangyin, Zhangjiagang, Yunong, Ruifeng and so on.

2. Change trend

The macro analysis results above show that it is a trend that the scale of real estate loans is gradually decreasing. I believe that the risk decision-making departments of all banks are also very aware of this. Therefore, according to the data reported in the mid-term report, the scale of real estate corporate loans of most bank stocks is gradually decreasing.

However, it is incredible that the development loan scale of individual bank stocks has increased, which is contrary to the practice of most bank stocks and the ultimate goal of real estate macro-control. Traffic, Guiyang, Chengdu and Qingdao have the largest increase. There may be two reasons behind it, one is that the local real estate market is very hot; the other is to borrow a new life for the original developer. If there are other possibilities, please comment.

3. The trend of non-performing business

It is difficult to determine whether this data is good or bad according to the data, because whether it is good or not needs to be analyzed according to the characteristics of each bank.

For example, over the past three years, the NPL ratio of many banks’ development loans has gradually increased. The typical ones are China Merchants, Industrial Bank (SH601166)$ , Jiangsu, Chengdu, etc. This shows that the NPL ratio of real estate is gradually exposed, which is not a bad thing. , but a good thing.

While the whole industry is increasing the identification of non-performing real estate loans, individual banks are still very low, which is not a good thing, because this is determined by the nature of the industry, so their non-performing rate should increase in the future, such as Huaxia, Ping An , Zhejiang businessmen and so on.

I have to talk about $Hangzhou Bank (SH600926)$ alone. Its development loan non-performing rate was relatively high three years ago. At that time, other so-called good banks were still relatively low. What do you mean? I am afraid that Hangyin’s investors have the most say, because the quality of Hangyin’s assets is very good, and there is almost no new bad, so Hangyin had to increase the standard for the identification of real estate bad two years ago, and really take precautions. 21 years to further become bigger, also for the same reason. On the contrary, the data this year has decreased, indicating that it has reached an inflection point. It basically reflects a microcosm of the non-performing property in the real estate industry. Comparing the data from top to bottom, it can be seen that Hangzhou Bank’s real estate non-performing settlement is a full two years ahead of other banks, and the impact of real estate will become less and less in the future. Other bank stocks will also go up and down in a year or two.

3. Personal Mortgage Loans

Personal mortgage loan is a high-quality asset of the bank anyway! ! ! I would like to ask everyone here, who is willing to take the risk of breaking the loan, the house will be confiscated, and they will owe a lot of debt?

In terms of scale changes, the vast majority of bank stocks are declining, which is consistent with the goal of macroeconomic control and the actual situation of the current real estate market.

The shrinking market and early loan repayment may lead to a decrease in the proportion of personal mortgage loans. From the bank’s point of view, of course, they do not want customers to repay their loans in advance, and hope that the slower the decline, the better. Data comparison can be found, some banks decline faster.

4. Summary

The data and trends of real estate development loans and mortgage loans from banks for three consecutive years show that:

The proportion of real estate loans of listed banks is gradually decreasing, which is consistent with macro-control;

The clearing of non-performing real estate is in progress, and the inflection point of individual outstanding clearing has already been reached;

The NPLs of most banks will start to decline after one or two years.

$Chengdu Bank (SH601838)$ is the first among all banks in terms of the increase in the scale of development loans, and the first among all banks in the rapid decrease in the scale of mortgage loans. The two are contradictory. The decline in mortgages shows that the local real estate market is not hot, and other cities in Wu are no different. The increase in the scale of development loans is very unusual. I will not comment on the specific reasons, so as not to say that I am subjective, you may wish to comment on it if you know it.

V. Data Analysis of Bank Stocks

In recent years, data analysis of bank stocks has gradually increased, but you can see from my previous analysis that many data cannot be determined at a glance. Even the same data is good in one bank, but not necessarily in another bank. If there are several levels of bank data analysis:

The lowest level: You can read static data, you can make tables in EXCEL, and the data will be swallowed up, and the result may be superficial;

Primary: Ability to dynamically compare data, see changing trends, and objectively evaluate individual stocks;

Intermediate: Can analyze the reasons for data changes through the vertical and horizontal comparison of data, combined with the macroeconomic level and the basic situation of individual stocks, and can select excellent individual stocks from multi-dimensional comparisons of numerous data;

My level is probably beginner to intermediate.

Advanced: Know the bank data and business well, and can accurately analyze all the company’s data, down to a specific business of the bank. Ability to make very accurate forecasts of individual stock earnings. For example, snowball millet and the like.

Top level: It can not only conduct accurate research and judgment on the macro, but also analyze the industry, and can also conduct multi-dimensional analysis of individual stocks, and can judge whether it is good or bad based on multi-dimensional comparison. This is the ceiling, out of reach.

Notice:

Finally, let me explain that everyone is willing to accept that a certain bank is good through data analysis; many people will be unhappy if a certain bank is not good after analysis. Everyone has seen the recent events, so there may be no more similar data analysis in the future, so let’s be forewarned!

This topic has 20 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/3260327054/232149268

This site is for inclusion only, and the copyright belongs to the original author.