The last snowball column: From the perspective of asset quality, the review of each bank has received good feedback, with more than 4 million readings. This article continues to ask questions from 2017 to the end of 2021. We select 5 years of data and the top 22 by market value Which banks in bank stocks have improved their asset quality? Which banks generate real profits? Which banks’ asset quality remains stagnant? Which banks have even regressed. Finally, the question is raised, what causes the phenomenon of the study, and I hope all golfers will discuss it.

1. Data source: the top 22 banks by market capitalization in the wind database;

2. Two data dimensions: (1) Non-performing/overdue data, that is, how many non-performing loans were identified as overdue for 1 yuan?

(2) Provision coverage ratio: the thickness of the reserve pool;

The data collation link is omitted, and two important pictures are directly displayed:

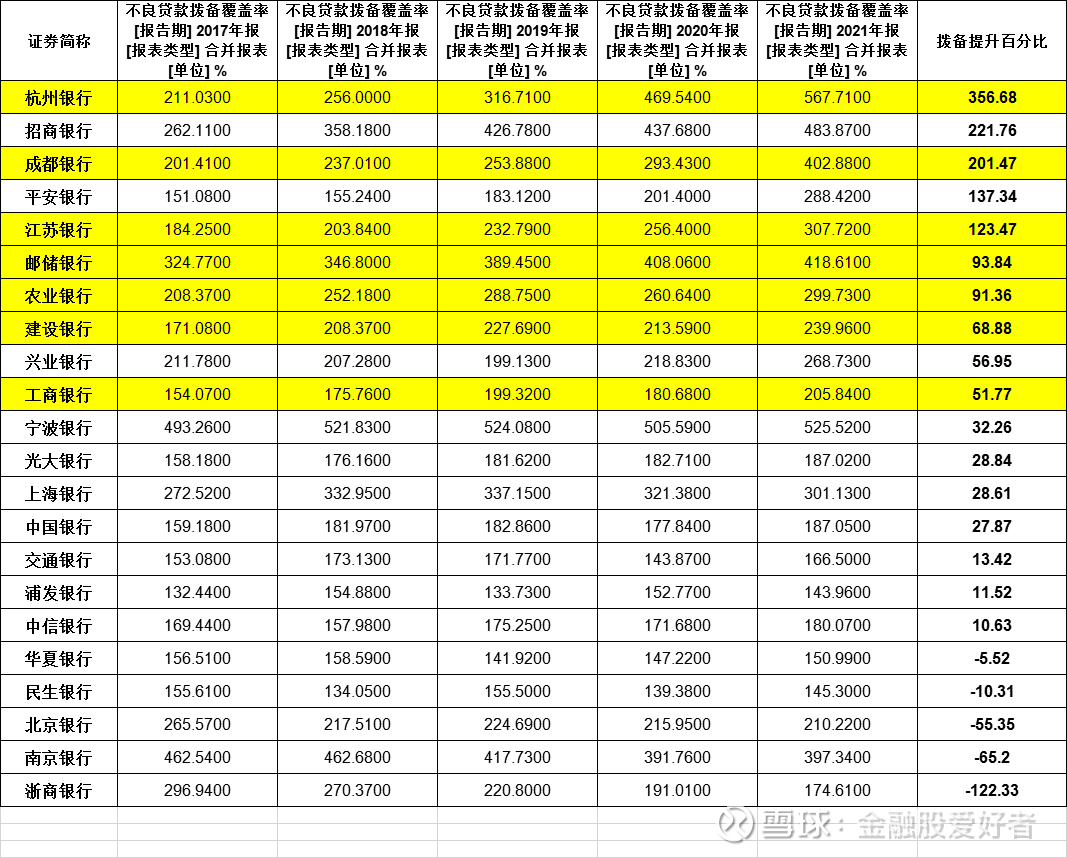

First of all, let’s look at the ranking of provision improvement. The provision of Hangzhou Bank at the end of 2021 has increased by 356.68% compared with 2017, ranking first, followed by China Merchants Bank; the third is Bank of Chengdu, which has increased its provision by more than 100%. There are also Ping An Bank and Bank of Jiangsu; more than 50% of the banks are Postal Savings Bank, Agricultural Bank, China Construction Bank, Industrial Bank and Industrial and Commercial Bank.

The bank whose provision coverage ratio has regressed is Zheshang Bank. The provision coverage ratio of Zheshang Bank has dropped from 296.94% in 2017 to 174.61% by the end of 2021, a decrease of 122%; Bank of Nanjing and Bank of Beijing have also dropped by 55%. Bank and Hua Xia Bank also declined a little bit;

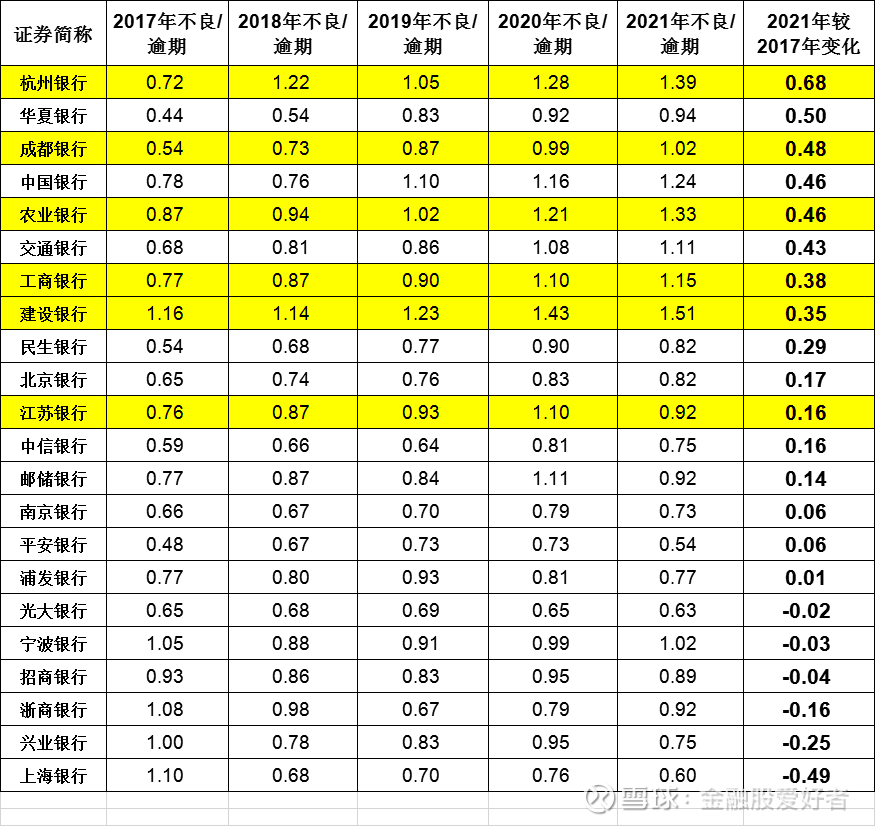

Secondly , let’s take a look at the strictness of non-performing/overdue identification. The Bank of Hangzhou has increased the most in the past five years. In 2017, only 0.72 yuan of non-performing loans was identified as overdue for 1 yuan, and by the end of 2021, 1.39 yuan of non-performing loans had been identified. Non-performing; secondly, Huaxia Bank also rose more, and Chengdu Bank still ranked third; Bank of China, Agricultural Bank, Bank of Communications, Industrial and Commercial Bank of China, and China Construction Bank, the five state-owned banks, also rose significantly;

Banks whose non-performing identifications have decreased in strictness are Bank of Shanghai, Industrial Bank, Zheshang Bank, China Merchants Bank, Bank of Ningbo, and China Everbright Bank; in particular, Shanghai Bank has serious problems. The year is only 0.6; China Merchants Bank and Ningbo Bank are relatively strict because they have been identified as non-performing, so the improvement is not large;

All in all, we want to invest in those banks with strict non-performing identifications and a substantial increase in the provision coverage ratio. If the asset quality of these banks is truly improved, then they will earn real money;

Looking back, Hangzhou Bank has the most obvious improvement in the strictness of non-performing identification and provision, and the substantial improvement in asset quality is a very suitable investment target;

Although China Merchants Bank has not improved its NPL identification level (it has always been strict), its provision coverage ratio has increased significantly, and it can be regarded as a bank with rapid improvement in asset quality;

Similar to Hangzhou Bank, Chengdu Bank has made remarkable progress in asset quality; both the degree of non-performing identification and provision have been improved;

Although the provision of Ping An Bank has increased significantly, the degree of non-performing identification has not been strict, so the gold content is greatly reduced;

The overall provisions of the six major state-owned banks are slowly increasing, and the degree of non-performing identification is also on the rise. Therefore, the asset quality of Industrial and Commercial Bank of China, Agricultural Bank of China, China Construction Bank, Bank of China, Postal Savings Bank and Bank of Communications must have improved in the past five years.

The strictness of the non-performing identification of Jiangsu Bank has always been good, and the provision is also increasing rapidly, showing a good level of asset quality;

Although the provision coverage ratio of Industrial Bank is increasing, the strictness of non-performing identification has regressed greatly. In 2017, Industrial Bank’s non-performing identification was very strict, reaching 1, which is a market-leading position, but at the end of 2021, it is only 0.75, which shows that the quality of assets has deteriorated;

Bank of Ningbo has always been stable, and the provision has not increased significantly, but it has always maintained a high level of 500%. The non-performing identification is also very strict, and the asset quality is very good;

Everbright Bank has always been relatively poor. The non-performing identification has been relatively loose, and the provision has not been raised; the quality of assets is poor at first glance;

Bank of Shanghai’s NPL identification was very strict five years ago. Although the provision is still at a high level, the NPL identification at the end of 2021 has been very loose, and the asset quality should be said to show a downward trend;

Needless to say, Shanghai Pudong Development Bank and China CITIC Bank have always been very general, very general;

Hua Xia Bank is a bit special. The provision has been fluctuating at 150%, but the strictness of non-performing identification has increased more, so whether there is a possibility of reversal of the predicament in the future, continue to pay attention;

Minsheng Bank’s provision has also been low, but the degree of non-performing identification is on the rise. Continuing to observe, it has never reached the buying stage;

As the bank with the largest assets among the local banks, Bank of Beijing, Beijing’s own son, the asset quality used to be good, but now it is getting worse every year. What happened? Bank of Shanghai used to be the second largest local bank in China, but now it is surpassed by Bank of Jiangsu, the son of Shanghai, and its asset quality is also deteriorating. These two first-tier cities are rich in resources, but their operation is so poor, which is worth reflection and thinking.

Zheshang Bank’s provision has dropped the most, and the non-performing identification has also declined, and its asset quality is definitely on the decline;

To sum up, although all banks are doing business, the results of their operations are very different. Asset quality is the core factor of bank valuation. We know that bank asset quality depends on people, products, systems and corporate culture; It is up to everyone to discuss what a bank with great asset quality has done right, whether it has reference value for other banks, and whether it can be learned, imitated or unique.

This topic has 4 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/5725525083/232143312

This site is for inclusion only, and the copyright belongs to the original author.