Welcome to the WeChat subscription number of “Sina Technology”: techsina

Text / Zhou Zhehao

Source / Yuanchuan Research Institute (ID: caijingyanjiu)

On May 17, four months before Apple’s iPhone 14 was released, Cook did two things: first, received the visiting Vietnamese Prime Minister at the company’s headquarters; second, reconfirmed that Apple would expand in Vietnam supply chain.

Less than 20 days after the launch of the new product, Apple once again flirted with India, saying that it is “delighted to produce the iPhone 14 in India”.

However, during the same period, the penetration of Chinese mainland enterprises in the Apple industry chain has also been “good news”: the value ratio of mainland China + Hong Kong in an iPhone has risen from 3.6% 10 years ago to 25% today. 7].

In the list of the top 200 supply chains released by Apple in 2021, companies from the mainland have 7 in and 6 out, with a total of more than 50 companies, becoming Apple’s largest supply area.

The New York Times wrote that the iPhone has changed from a product designed in California and made in China to a joint creation of the two countries.

But the plate of Apple’s supply chain is so big, and behind the success of one supplier, it is very likely that another company will exit.

So who is brilliant and who quits?

Before answering this question, we need to understand one thing, what does Apple need?

Luxshare Precision: Relying on Foxconn’s favor than Foxconn

The first iron law of Apple’s support for suppliers is that as long as it doesn’t die, it will die.

In June of this year, Liu Yangwei, the always low-key chairman of Foxconn, publicly complained that competitors were “digging footsteps” in Vietnam: “When these factories saw where Foxconn was building a factory, they went to buy a piece of land next to the factory, and wanted to use this way to carry tailwinds. car, and relying on high salaries to poach Foxconn talents to quickly enter the market.”

Foxconn did not name names, but reported an ID card – Luxshare Precision, a company from mainland China.

Luxshare’s Vietnam factory and Foxconn are just across the road. This company started with spare parts such as connectors and acoustic devices. From Airpods to iPhones, it eroded Foxconn’s Apple OEM orders. The boss, Wang Laichun, worked at Foxconn for ten years before starting his business.

Before 2013, Foxconn contracted almost all of the iPhone’s foundry. Today, its foundry share has dropped to less than 70% [1]. In addition to the old rivals Pegatron and Wistron, Foxconn’s biggest rival is Luxshare, which is supported by Apple.

In 2020, Taiwan media once published an article titled “Luxshare’s market value surpasses Hon Hai! Wang Laichun’s in-depth investigation into “female version of Guo Dong”, behind Apple’s scheming”, although the title is very Hong Kong reporter, but the content is very solid, clearly pointing out that Luxshare is in the top position, and Apple is behind it many times.

As early as 2015, Wang Laichun followed Apple’s advice and acquired the mainland factory of Meilu, an acoustic company in Taiwan. At the end of 2016, the first generation of AirPods was launched, and Luxshare won the AirPods OEM orders in one fell swoop through this factory, and the stock price has quadrupled in three years [4]. In 2020, Apple also suggested that Luxshare should invest in Kecheng Technology, which is a supplier of Apple’s smartphone and notebook metal casings[5].

Why support Luxshare to contain Foxconn? It may be that Foxconn in Apple’s eyes still earns too much.

After Pegatron took over, Foxconn’s gross profit margin was only about 10% in 2015-17, but Apple believes that there is still room for decline. Therefore, after Luxshare Precision took over, Foxconn’s gross profit margin will drop to 8.31% in 2021.

Of course, in addition to enough volume, Apple also requires the foundry to be obedient.

Before the 12-inch MacBook was released, Apple accused Foxconn of giving Google a tour of a factory that makes metal frames for computers. When Apple asked Foxconn to provide visitor logs and security information, Foxconn refused[2]. In Apple’s view, this kind of behavior must be beat and beat.

After that, Apple strongly promoted the Type-C interface on the Macbook, and Luxshare was the only manufacturer in mainland China that participated in the formulation of the Type-C standard. When AirPods was first launched, due to the difficulty of module integration, Inventec, a major assembly manufacturer, gave up directly, but the Luxshare team took only five months to achieve a 100% yield rate.

In order to affirm the spirit of Luxshare’s king, Cook personally visited Luxshare’s Kunshan foundry in December 2017, and left a rainbow fart saying “super-first-class foundry” and a cordial photo with the little girl in the workshop. Cook just left, and 50% of AirPods orders were delivered.

By 2020, Luxshare has become the first iPhone foundry in mainland China. But so far, is the story happy?

In the first half of this year, the Prime Minister of Vietnam visited the Apple headquarters in California, and Cook took a photo with him. The production order for the latest Airpods became a gift for the photo.

There is no most volume, only more volume of reincarnation, which seems to never stop.

BOE: Apple dances the sword, aiming at Samsung

Never allow yourself to be stuck in the neck, this is Apple’s second iron law to support suppliers.

The struggle over Apple’s screen is a typical case. The two protagonists of the war are Samsung and BOE.

Samsung is the world’s largest mobile phone brand and the iPhone’s number one competitor. But Samsung’s other identity is a major supplier of iPhone screens, NAND flash memory, and DRAM memory chips.

Especially on the screen side, after the iPhone X became Apple’s first mobile phone with an OLED screen, Samsung was once the only company that could meet Apple’s quality control and production capacity requirements. You must know that the screen is the third largest component in the mobile phone after the chip and the lens.

As a result, Apple is paying Samsung $120-$130 to produce an iPhone X, almost three times the price of the iPhone 7’s LCD panel.

It is precisely because of the popularity of OLED screens that Apple’s dependence on Samsung has reached the point where the court is fighting a plagiarism lawsuit for the appearance of mobile phones, and at the same time, it has not placed orders with Samsung to make iPhones.

Therefore, Apple chose to pursue a two-pronged approach in “de-Samsungization”.

In a popular sense, panel is a capital-intensive industry, and latecomers have the opportunity to build higher-generation production lines through larger capital expenditures to catch up with the first movers. Japan’s panel industry is just like this:

In 1994, Japan’s LCD panel production accounted for 95% of the world’s total, but most of these production capacities were 1st and 2nd generation lines. However, due to the lack of investment willingness of enterprises and the impact of the Asian financial crisis, Japan did not upgrade the production line. As a result, it was surpassed by South Korea, which smashed the third-generation line two years later.

Therefore, the first step for Apple to support suppliers is to give money.

In 2017, Apple invested $2.7 billion in LG to build a new Gen 6 OLED production line. It’s a pity that LG has always been good at large-size OLEDs for TVs and computers, and in small-size panels such as mobile phones, it is still a step behind Samsung.

This is another feature of the panel industry: after the production line is built, how to debug the equipment and how to ensure a higher yield are all know how in exchange for countless hours.

Therefore, when supporting a new supplier, BOE, Apple changed its strategy.

In an interview with Commonwealth magazine, an executive of a panel factory said that Apple directly asked Samsung to teach BOE some old technologies from a few years ago to help BOE overcome technical difficulties.

With the help of Samsung, in 2017 when the iPhone X was released, BOE’s sixth-generation flexible screen production line was mass-produced ahead of schedule, becoming the only sixth-generation flexible screen production line in the world except Samsung at that time. It was also in this year that BOE appeared on the list of Apple suppliers for the first time, but it was only responsible for products such as iPad, MacBook, and Apple Watch.

After that, the company continued to build factories to expand production capacity.

Although there is still a distance from Samsung in terms of production capacity and yield, it has made great progress compared with itself: in 2021, the yield rate of BOE’s mature OLED products will exceed 80%, an increase of 20% over the previous year (Samsung is around 95%). ) [13].

In 2021, BOE will provide AMOLED screens for the standard version of the iPhone 13, marking the first time that Apple has used domestic OLED screens for its flagship phone that year. By this year, the shipment volume of screens provided by BOE for the iPhone 14 is expected to be around 30 million, which is almost in the same order of magnitude as the 70 million expected to be provided by Samsung [10].

According to the forecast of UBI Research, an OLED research institute, by 2023, BOE will replace LG as the second supplier of iPhone panels.

Of course, Cook is not a good person: in China alone, both TCL CSOT and Visionox have provided products to Apple for inspection. Tianma Microelectronics has become an AMOLED screen supplier for Apple Watch [15].

Whether it is showing favor to China at the level of public opinion or supporting suppliers, it is essentially Apple’s business considerations. Apple’s purpose has always been clear: not only can it not be stuck in the neck, but the more intense the upstream fight, the better.

Yangtze River Storage: Apple shows its attitude towards water

Killing two birds with one stone, achieving political correctness by supporting suppliers is the third iron law.

For example, domestic memory chips like YMTC are almost perfectly in line with Apple’s logic.

To make a simple science first, flash memory chip is a common memory chip, which can ensure that data will not be lost even if the mobile phone is powered off. In terms of cost, the price of flash memory is less than one-third of that of OLED; but in terms of status, since 2018, the status of the chip industry chain has been rapidly linked to technological independence, and its importance has increased unprecedentedly.

In August this year, the United States passed the “Chip Act”, which will give the chip industry a subsidy of 52.7 billion US dollars, but there is one condition: companies receiving financial support are prohibited from building factories below 14nm in China.

Obviously, whether Apple is interested in subsidies or not, its actions are contrary to the political correctness of the United States. If you want to simply sort out Apple’s actions, it is that – at the same time as technology is recognized, Apple hopes to stabilize the Chinese market by supporting suppliers.

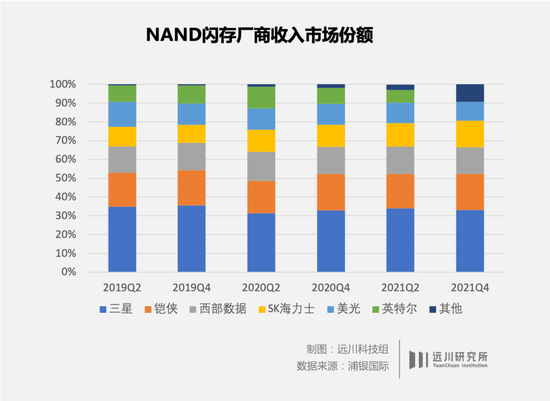

Let’s first look at the market structure: with the first-mover advantage, Samsung, Kioxia, SK Hynix, Western Digital, Micron, and Intel have dominated the flash memory market for a long time, with a combined market share of over 95%[8].

The flash memory of the iPhone 12 comes from Samsung, and the flash memory of the iPhone 13 Pro Max comes from the Japanese Kioxia sold by Toshiba.

For domestic enterprises, 2020 is a milestone year for YMTC, because its market share has achieved a breakthrough from “0 to 1” – indeed a literal breakthrough, from 0% to 1%.

Although it is not enough to shake the position of the Big Six, it is also the leading role in “others”.

Behind this breakthrough, of course, there are solid efforts, but in terms of effect, it is still far from the leading manufacturers.

From the perspective of two important indicators of flash memory, the number of layers and storage density, YMTC is currently able to mass-produce 128 layers. It only took three years to complete the leap from 32 to 64 to 128, which is six years for international manufacturers. Just finished [14]. Moreover, with the support of its own unique architecture, the storage density of YMTC’s 128-layer flash memory chips is higher than that of rivals such as Samsung and Micron.

But at present, Kioxia and Western Digital have produced 162 layers of energy, while Samsung and SK Hynix have produced 176 layers. When foreign media described it, they called their leading position in Changjiang Storage as “generational leadership”.

Therefore, realistically speaking, Changjiang Storage is still far from the first-tier manufacturers in terms of technical indicators, and it is naturally partly due to Cook’s pattern that it can enter the Apple industry chain.

At present, China remains Apple’s most important market – in the second quarter of 2022, Apple’s shipments increased amid a decline in smartphone shipments in China, and the corresponding 16.3% share was a 10-year history of the second quarter New high [14].

On September 7 this year, Cook even posted two Weibo posts in a row. In addition to pre-heating for the upcoming press conference, there is another one that says that Apple cares about all the people and regions in Sichuan affected by the earthquake.

This statement shows the attitude of Master Duan Shui. It’s just that in the face of political pressure in the United States, Apple has also played a trick: it will not sell mobile phones with Yangtze River memory chips outside mainland China.

Apple has taken into account both sides, but in this way, the iPhone 14 that Chinese consumers receive has also become a “special version” in a sense.

end

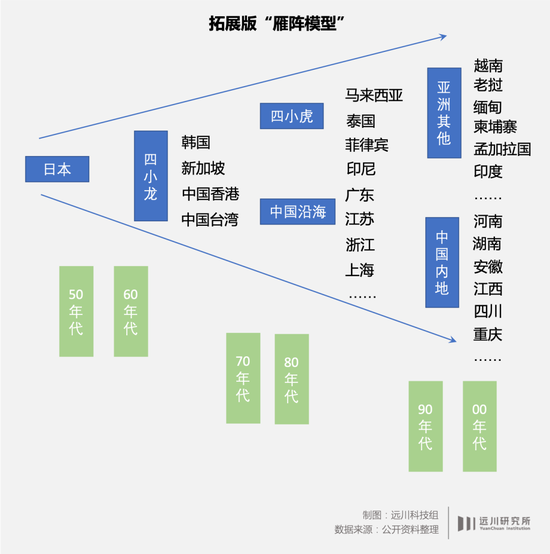

The foundry industry goes from Taiwan to the mainland to India and Vietnam; chips from Europe and the United States to East Asia; panels go back and forth between China, Japan and South Korea. Regarding the changes in the industry, Japanese scholar Akamatsu Kaname once summed it up as “the transfer of wild geese”:

Japan, the Four Asian Tigers, China’s Coast, China’s Inland, and Southeast Asia, each region will carry out industrial upgrading in sequence according to labor-intensive industries represented by assembly, capital-intensive industries represented by panels, and technology-intensive industries represented by chips , vacate the cage for the bird.

In essence, Apple’s checks and balances, transfer, and control of suppliers are all miniature versions of this transfer of geese.

So, among the geese of Apple, are we at the head of the geese?

A somewhat unfortunate fact is that in the field of foundry, the iPhone 14 Pro and iPhone 14 Pro Max are still exclusively produced by Foxconn. In the field of panels, BOE can only supply the iPhone 14 standard model, and miss the Pro series. In flash memory chips, we are still 1% of others.

Apple’s rules have always been clear, such as fully transparent profit margins, competition from multiple suppliers, and a ruthless elimination mechanism. The confidence to do this lies in the annual shipments of more than 200 million high-end mobile phones, MacBook shipments that have grown more than twice in the PC market, and a series of accessories represented by AirPods that are priced higher than the average price of Xiaomi mobile phones.

Higher pricing and higher shipments mean more upstream profit margins. So for the supply chain, although Apple’s rules are cruel, they are already the best rules.

Therefore, for a long time in the future, the progress of the mainland’s electronics industry chain may still be exposed to Apple’s cruel rules. But on the other hand, the transfer of the geese array to this point itself marks the progress from nothing.

No matter what the reason is, getting on the car of Apple’s industrial chain is already a kind of recognition and a ticket to industrial upgrading. What we have to do at this stage can be summed up in 12 words: accept the rules, sit at the poker table, and talk about the future.

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-10-09/doc-imqmmthc0284047.shtml

This site is for inclusion only, and the copyright belongs to the original author.