Welcome to the WeChat subscription number of “Sina Technology”: techsina

Text/Li Shuiqing

Source/Smart Things (ID:zhidxcom)

In just half a year, the top two national-level short video manufacturers in China have entered the video cloud.

In February 2022, ByteDance’s cloud computing brand Volcano Engine launched a video cloud product matrix. In August of the same year, Kuaishou also launched the “StreamLake” video cloud brand, covering video on demand, live broadcast, real-time audio and video interaction, video AI, etc. Multiple To B (enterprise level) service areas.

Video cloud, as the name suggests, refers to the subdivision of cloud computing with audio and video production, processing, transmission, and consumption as the main application scenarios. According to a report from the well-known research agency IDC, China’s video cloud market will approach 70 billion yuan in 2021.

The big short video manufacturers are “rolling” into the video cloud enterprise-level service track with lightning speed: the delay of live video broadcast is reduced from 3s~20s to less than 1s, and the real-time audio and video of 200ms~400ms also makes the interaction even with microphone, Scenarios such as video conferencing and online karaoke have become possible… New records on delay, picture quality, and standards have brought new experiences to users.

Many people will ask, isn’t the video cloud a red ocean market?

A number of cloud computing practitioners told Wisdom that the overall video cloud market has not found significant growth yet, and the entry of Byte and Kuaishou has intensified competition in the stock market. A video cloud industry insider said that Volcano has more than 600 people invested in audio and video cloud services, more than many well-known industry peers, and has a large cross market with them; Kuaishou’s investment is smaller, but there are also hundreds of people. It can be said, “very rolled”.

Throughout this industry, there are already two leading players: one is Alibaba Cloud, Tencent Cloud, Huawei Cloud, Baidu Smart Cloud and other large cloud computing platforms, and the other is Agora, NetEase Yunxin, and Qiniu Cloud. and other vertical PaaS (Platform as a Service) players, as well as a large number of other CDN (Content Delivery Network) and application vendors.

You can sing and we can sing, whether it is the cloud conference and cloud topics that broke out during the epidemic, and the e-commerce live broadcast that created a phenomenon-level anchor like Li Jiaqi, or from the traditional live broadcast of game sports events to the emerging metaverse, Smart cockpit, these players have already experienced a wave of battles around technology and market in the sea of blood.

The entry of Byte and Kuaishou has undoubtedly injected a powerful third force into this market. This force is threatening, with the temperament of a new generation of Internet “curling king”, and is expected to change the order of the video cloud industry dominated by traditional leaders such as BAT with a lower video industry base and a business scale of over 1 billion users.

This leads us to think about more in-depth questions: Is the video cloud really still a red ocean? Why are Byte and Kuaishou involved in the video cloud market? Where is the fate of the three types of industry players heading?

Very curly: Bytes are held high, and Kuaishou is small and beautiful

First of all, let’s take a look at the action of the volcano engine, which can be said to be held high.

Following the establishment of the internal goal of becoming the “fourth cloud”, in February this year, Volcano Engine launched a video cloud PaaS product matrix, covering the needs of multiple scenarios such as live video, on-demand, real-time audio and video, cloud games and cloud rendering. The core middle platform, products and solutions.

On the one hand, these PaaS products and their previous IaaS (Infrastructure as a Service) constitute a complete cloud computing service, which is rare in the industry and comparable to the service level of Alibaba Cloud, Huawei Cloud, Tencent Cloud and other major players. player. Since Byte’s own business is related to social entertainment and games, the product roadmap of Volcano Engine Video Cloud is similar to Tencent Cloud.

On the other hand, Volcano Engine, together with Alibaba Cloud and Tencent Cloud, released an “ultra-low-latency live broadcast protocol signaling standard”, which brought shocks to the audio and video industry. This standard can shorten the delay of live broadcast technology from 3 to 6 seconds in the past to 1 second, indicating that it has joined the two major cloud computing companies to master the right to speak in the new generation of video cloud technology.

In addition, it is worth mentioning that PICO, a VR headset manufacturer that was acquired by Byte, is also its user, showing its substantial layout in the metaverse market.

PICO has designed a set of solutions based on the volcano engine RTC (Instant Communication) technology, which realizes high-definition bit rate VR video transmission based on VR equipment, and low latency of voice and video transmission, thereby creating an immersive video cloud service experience. Among the current Internet giants, only Byte VR equipment has made a big move, which is expected to become another big help for it to break through the video cloud market.

Compared with Byte, Kuaishou’s video cloud can be said to be small and beautiful.

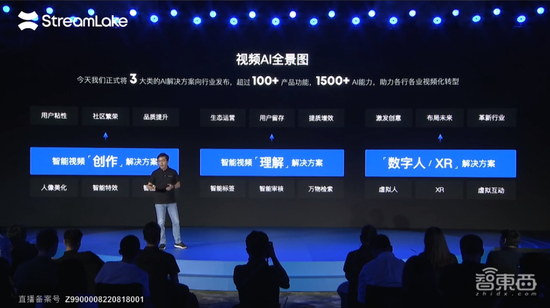

In August, the “StreamLake” video cloud brand was launched. Kuaishou’s public business is mainly output through editing, on-demand, short video and other capabilities, and has not disclosed more capabilities in live broadcast, real-time audio and video.

“We hope to be Snowflake in the video field, talk to customers about audio and video + AI, solve these two problems, and do nothing else, as long as it is a video upgrade, and do aggregation and distribution, just look for StreamLake. Yu Bing, senior vice president of Kuaishou and head of StreamLake, said in an interview at the time.

Kuaishou’s style of play is similar to Baidu Smart Cloud, which launched Smart Video Cloud 3.0 Panorama in May 2021. Although it covers the entire industry chain, the actual service focuses on video creation and video AI, emphasizing “Cloud Intelligence”. One” advantage.

In fact, short video companies have tested the video cloud SaaS before, “rolling” a wave of collaborative office market.

Byte Feishu is a major representative, and the video conference service is a core function of Feishu, representing the earliest external output of its video cloud capabilities. According to the latest data from third-party agency QuestMobile, Feishu’s monthly active users (MAU) reached 7.89 million in August 2022. Feishu focuses on major customers, just like Pinduoduo has entered the hinterland of Taobao and JD.com, directly poking DingTalk and corporate WeChat targeting the collaborative office market for many years. Insiders in the video cloud industry told us that “Feishu is used by major customers, enterprise WeChat is used by C-terminals, and DingTalk is used by small and medium-sized enterprises” has become a common impression in the market. For other players who want to enter the game, even Baidu, it is difficult to squeeze in by throwing money at it.

With Feishu SaaS products testing the water, short video companies are getting involved in the field of video cloud. And this time, it is expected to make a bigger splash in another market.

The video cloud market has a long history. In the early days, the CDN video distribution business was the main business, and now it has evolved into two types of services: the basic layer and the application layer. From the dismantling point of view, the basic layer also includes the underlying CDN (video content distribution network) and RTC (real-time audio and video communication network), which includes the IaaS capabilities of video production, processing, dissemination, consumption and other links, thus supporting video on demand, PaaS services such as live video, real-time audio and video. At the application layer, the video cloud supports SaaS applications such as enterprise live broadcast, education and training, video conferencing, and radio and television media.

According to a report from iResearch, a well-known research organization, in the video cloud revenue, the ratio of the base layer and the application layer is stable at 8:2. From the perspective of application scenarios, consumer Internet is still the main field, including pan-entertainment, e-commerce, live broadcast, etc.

Focusing on IaaS and PaaS, the short video manufacturers have customers who focus on entertainment and games, and compete head-to-head with players such as Tencent Cloud, Shengwang, NetEase Zhiqi, etc.; they are deployed in traditional markets such as finance, medical care, and automobiles. Short video manufacturers At the same time, it attacked the positions of big factories such as Alibaba Cloud, Huawei Cloud, and Baidu Smart Cloud.

An audio and video practitioner told Zhixing that (the audio and video market) is “very rolled” – the number of people who have invested in the video cloud by Volcano Engine has exceeded 600, which has exceeded many traditional head players. On the Kuaishou side, Yu Bing also said in an interview that Kuaishou has accumulated a group of industry leading experts with hundreds of people since 2016.

The future of the video field is self-evident – the well-known research agency IDC predicts that by 2025, more than 80% of global data will be unstructured data such as audio and video, and such hyper-video has become an important feature of the digital age.

However, when Byte and Kuaishou entered the video cloud market, there were more signs of “involution”.

Two waves in three years, with no video cloud?

Xiang Zhidong, a professional from the video cloud field, talked about the anxiety about this kind of involution. He believes that practitioners are like bees in a glass bottle – they have a bright future and lack a future.

Since 2020, the video cloud industry has had two opportunities to open up new blue oceans, but neither has brought a visible incremental market to the video cloud market.

The first time was at the beginning of 2020, when the global COVID-19 epidemic broke out, prompting a surge in demand for online conferences, distance education, telemedicine, and e-commerce live broadcasts, driving the development of video cloud manufacturers. For example, the daily active users of Zoom, a leading player in online conferences in the United States, rose from 10 million to 200 million, and its stock price once soared several times; in my country, the leading player in the real-time audio and video field, Shengwang, landed on Nasdaq in the United States, and its stock price rose 152.5% on the first day , with a market value of $5.06 billion.

From the perspective of technological development path, a new revolution is emerging. In 2021, as Google’s open-source WebRCT is included in the official standards of W3C and IETF, the end-to-end delay will be reduced to less than 1s, and the two major audio and video technologies of RCT and CDN technology will converge. Based on this, many leading players such as Tencent Cloud, Shengwang, and Netease Yunxin have launched integrated CDN live broadcast products, which are manifested at the application level, such as adding some interaction, connecting microphones to the live broadcast, or bringing lower latency. Support live e-commerce, etc., which greatly improves the video cloud experience.

However, when the time came to 2021, this market rebounded rapidly, and players from all walks of life “like entering Baoshan but returning empty-handed”.

Looking at the battlefield of giants, Tencent Conference, which Tencent spends money on, occupies the leading position that other players cannot challenge. C-side online conferences have become a market for increasing profits without increasing income; looking at the vertical track, the education online video market of less than 10 billion yuan is enough to exceed 10 billion yuan. With 100 existing players, the “double reduction” has squeezed the market space again; looking at popular startups, popular stocks such as Zoom and Shengwang are also facing severe challenges such as insufficient growth and plummeting stock prices.

The second opportunity comes in 2021, with the birth of the concept of the metaverse, which is considered to be a new demand driving the development of video cloud.

Applications such as VR content production, AR interaction, and virtual humans are becoming more and more popular. Alibaba Cloud, Tencent Cloud, NetEase Yunxin, and Shengwang have all launched Metaverse-related products and solutions. At the Winter Olympics in early 2022, Alibaba Cloud used real-time holographic interactive technology to break the limitations of time and space, and brought the IOC President Bach and Alibaba Group CEO Zhang Yong together in a distant cloud, attracting industry attention.

However, the metaverse that the capital touted didn’t translate into actual cloud service revenue in time. Industry insiders from the video cloud field told Zhishi, taking holographic interaction as an example, in fact, such applications are more dependent on local hardware facilities, and the actual incremental market brought by video cloud PaaS and SaaS is insufficient. Taking the popular digital people as an example, the amount of a project may be about 1 million yuan, which is only the icing on the cake in the package of 100 million yuan projects of many financial and government customers. In the VR/AR field that Metaverse focuses on, there is no demand in the C-end market.

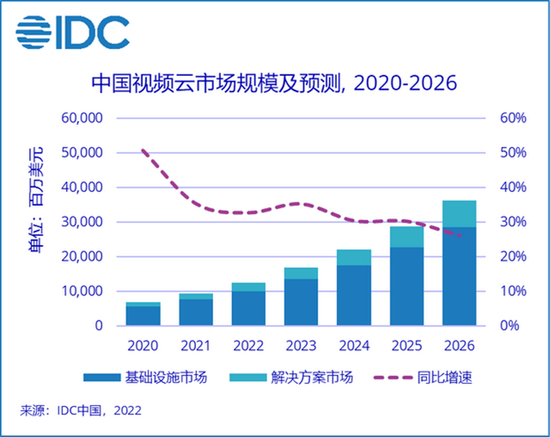

IDC predicts that from 2021 to 2026, China’s video cloud market will continue to grow rapidly, with an average annual compound growth rate of 31.0%, and it will reach US$36.4 billion (about 260 billion yuan) in 2026. According to data from iResearch, a research and consulting firm, as of April 2022, 69% of China’s Top 100 APPs have video-on-demand, live broadcast or real-time audio and video functions.

However, judging from the development trend in the past two years, the demand for real-time audio and video under the new crown pneumonia epidemic in 2020 rebounded rapidly, increasing profits but not increasing income; the Metaverse outlet in 2021 is far from the stage of scale landing.

The two waves of wind in three years have not really brought fire to the video cloud, allowing the industry to see a particularly obvious incremental market.

Why are Bytes and Kuaishou “involved” in the video cloud Red Sea?

So why did Byte and Kuaishou choose to enter the video cloud track at this time?

From live broadcast e-commerce to Feishu collaborative office platform, from VR/AR to cloud computing, Byte is becoming the rival of Alibaba Cloud, Tencent Cloud and other Internet giants.

First of all, starting from the development of short video manufacturers themselves, the development of video cloud has become an agenda on the arrow.

From the perspective of the overall environment, the current weak growth of consumer Internet has become very obvious, and the traffic of short video platforms has peaked. Taking Douyin as an example, the latest data shows that its current daily activity is 600-700 million, the traffic has peaked, and the dividend is basically over. To develop the industrial Internet blue ocean market, the selection logic of Byte and Kuaishou is no different from that of other Internet companies. The best entry point to focus on the To B business, Bytes and Kuaishou are undoubtedly the best at audio and video services, which can be called “cats that can hold mice”.

In recent years, Douyin and Kuaishou have jumped out of the original social media framework and developed various businesses such as e-commerce and finance. For example, the Douyin e-commerce platform has sold 10 billion items in the past year, and Kuaishou’s GMV (gross e-commerce transactions) in the first two quarters of 2022 increased by 31.5% year-on-year to 191.2 billion yuan. Behind these transactions, Byte and Kuaishou have accumulated years of experience in e-commerce live broadcast, video interaction, video AI and other technologies. According to the Wall Street Journal, Byte will spend 103.9 billion yuan on research and development in 2021. It can be speculated that the audio and video technology team shoulders the new mission of realizing its technology.

The official launch of the video cloud service is only a matter of time.

Taking Volcano Engine as an example, the industry generally knows that its video cloud has been prepared for about two years. In 2020, it will begin to explore the commercialization of To B in the video platform. But in fact, when its short video platform Douyin APP was launched in 2016, the video center was built that year. In 2018, Douyin surpassed 100 million DUA (daily active users) in February. On the one hand, the team began to reduce its dependence on suppliers such as Shengwang; on the other hand, it also began to build video team capabilities.

2020 is a key node. In this year, ByteDance successfully undertook the first related To B customer, the “Know Ball Emperor” football community APP. In the next two years, the Volcano Engine supported the CCTV Spring Festival Gala with over 70 billion red envelope interactions and nearly 5 million live online users for two consecutive years. In essence, it has taken the lead in entering the video cloud market from the bottom up.

But as we all know, cloud computing is an industry with high investment and slow realization. Therefore, Volcano Engine and Kuaishou obviously do not expect to make quick money in this field.

The big short video companies have at least the following four long-term plans when they land on the video cloud:

1. Show technical strength and consolidate the status of the first echelon of Internet giants. Alibaba’s revenue in 2009 reached nearly 4 billion yuan, and the launch of Alibaba Cloud, a To B service platform, became the carrier of its technology moat and second growth curve. Bytes and Kuaishou are just retracing the road of Internet giants, transforming from Internet leaders to innovative technology leaders.

2. Comply with the development of the national digital economy to obtain more policy support. At present, the scope and depth of Internet anti-monopoly is deepening, and big Internet companies need to assume more social responsibilities to promote the digital and intelligent transformation of the industry, and the combination of virtual and real has become the general trend.

3. Preparing for an IPO and raising the valuation. ByteDance, which has an annual revenue of more than 400 billion yuan, will be reported every few months about its listing progress. In April this year, Gao Zhun, a former senior partner of the American law firm Starr who has worked on hundreds of mergers and acquisitions and listing projects, took office. Byte’s new chief financial officer (CFO) revealed the signal that its IPO is near. The cloud computing business sector will undoubtedly add points to its valuation at the IPO from the level of flow and concept. The video cloud is the best entry point to open up the cloud computing industry.

4. Reduce costs and increase efficiency for the long-term development of your business. The technology accumulated through its own business practice is continuously iterated in the process of empowering external customers, so as to further feed back the technology and experience to the internal business.

The relatively abundant capital and talent scale make short video companies have more sufficient conditions to cross the valley of death in entrepreneurship and seek long-term value.

The spoilers are involved, and the three-way players are close to each other

Although the growth of the video cloud market still lacks the wind, before Byte and Kuaishou entered the game, there were already two players in this industry. It can be said that these two players have been fighting for nearly ten years. After bloodbath, it has long become a “winner takes all” situation.

Specifically, the first type of leading players are Internet cloud computing companies, represented by Alibaba Cloud, Tencent Cloud, Huawei Cloud, and Baidu Smart Cloud. The second type of leading players are vertical PaaS players, represented by NetEase Yunxin, Shengwang, and Qiniuyun.

An industry insider in the video cloud field told Wisdom that the market of volcanoes, Kuaishou and these two types of players overlaps a lot, but the cards in their hands will be different.

Let’s take a look at the Internet cloud computing companies.

According to IDC data, Alibaba Cloud, the largest domestic cloud computing company, has ranked first in the overall market share of video cloud in China for four consecutive years, accounting for 26.9%. In fact, since the integration of Youku’s CDN and video cloud businesses and teams in 2017, Alibaba Cloud has already started to harvest the video cloud market. At that time, Zhu Zhaoyuan, general manager of Alibaba Cloud Video Cloud, announced that the CDN official website will reduce the price by up to 35%, and the unit price of traffic is as low as 0.17 yuan/G. It can be said that a wave of “bloodbath” has been carried out on the industry. Waves of price wars have swept many small and medium players out of the game.

In the next few years, Alibaba Cloud gradually introduced 4K and video intelligent production technology, and jointly developed audio and video communication services with DingTalk. In the field of e-commerce live broadcast in the new market, it has won major customers such as Lazada, the largest e-commerce platform in Southeast Asia, and short video. The solution has also landed on Kumu, the leading mobile social platform in the Philippines, supporting the cloud video services of multiple educational organizations such as Xuexin.com… It can be said that Alibaba Cloud has superimposed technologies step by step, consolidating its leading position in the industry.

Also strong are cloud computing companies such as Tencent Cloud, Huawei Cloud, and Baidu Smart Cloud. Taking Tencent Cloud as an example, it also has a dedicated audio and video team, launched a fast live broadcast program in 2019, announced the official establishment of the Tencent Cloud audio and video brand in May 2021, and integrated Tencent Cloud Real Time Communication Network (TRTC), instant messaging network (IM), streaming media distribution network (CDN) three networks, released three-in-one RT-ONE network. At that time, Li Yutao, vice president of Tencent Cloud, said that this is the most complete audio and video communication PaaS platform in the industry, meeting the video needs of various industries such as education, retail, and pan-entertainment.

In terms of corporate positioning, Volcano and Tencent are the most similar, both entering the market with entertainment and games as entry points, and from IaaS to PaaS and SaaS. But in terms of time, Tencent Cloud is a full year earlier. And jumping out to play in the financial, medical and overseas markets, Volcano Engine is obviously head-to-head with Alibaba Cloud.

Let’s take a look at the video cloud vertical PaaS players.

NetEase, which is also an Internet giant, has a different way of deploying video cloud than giants such as Alibaba and Tencent. NetEase did not develop the IaaS field, but mainly focused on the PaaS track. Founded in 2015, NetEase Yunxin is a positioning communication and video cloud service provider. Its service scope has gradually covered from the earliest IM (Instant Messaging Network) services to video services, live on-demand and real-time audio and video technology services.

NetEase’s cloud services focus on communications and video clouds, giving it more freedom. Since there is no IaaS sales indicator, such players will pay more attention to the services of the PaaS platform itself, and can flexibly cooperate with more IaaS, AI and other manufacturers. For example, a professional from NetEase Yunxin told us that if customers need it, NetEase Yunxin will also cooperate with the AI teams of other big Internet companies. After nearly ten years of development, NetEase Yunxin has begun to jump out of the comfort zone of entertainment and games, and has won projects in many traditional fields such as finance, medical care, and logistics.

Founded in 2014, Shengwang is the leading real-time audio and video interactive PaaS service provider in China. At that time, Google’s WebRTC open source project allowed developers to realize real-time communication on the Web side based on API, and RTC PaaS service providers represented by Shengwang came into being. As the earliest domestic manufacturer to invest in the real-time audio and video field, Byte’s short video social software Douyin was also a major customer of Shengwang. After the outbreak of the new crown pneumonia, Shengwang’s online education customers at that time soared more than 7 times, and the stock price soared to $114.97/ADS in February 2021.

Afterwards, despite being affected by the double-deduction policy, Shengwang deployed the increasingly popular metaverse field in a timely manner, and launched MetaChat meta-language chat, MetaKTV meta-karaoke, and MetaLive meta-live three solutions for the fields of interactive social, karaoke and live broadcasting. Bringing new business highlights to it. According to industry insiders, players such as Shengwang and NetEase Yunxin have invested a lot in R&D in the audio and video field. Although their brand awareness is not as good as that of big manufacturers, their reputation in the industry is good, and they have won many big customers.

It can be seen that large cloud computing companies sell video cloud services when they sell IaaS services, and vertical PaaS manufacturers provide more professional services by virtue of their technology focus. After seven or eight years of competition, the two players have made a full wave of fighting in the head customer market.

In general, the remote video outlet under the new crown pneumonia epidemic in 2020 and the Metaverse outlet in 2021 have not brought a visible incremental market to the video cloud market. The newly entered Volcano Engine and Kuaishou, the new players, have created a new three-way player confrontation situation, which has intensified the “involution” in the video cloud field.

The traditional leading players are not “non-fuel-efficient lamps”. If Volcano Engine and Kuaishou want to conquer such a market, it is tantamount to taking food from the tiger’s mouth.

An industry insider from the video cloud field told Wisdom that Volcano Engine and Kuaishou are currently mainly focusing on entertainment, games, and social platform markets, which have strong intersections with Tencent Cloud, Shengwang, and NetEase. The volcano engine previously used the services of real-time audio and video head PaaS enterprises. If the volcano engine really wants to start this market, it needs to get customers from Shengwang first.

This means that Volcano Engine and Kuaishou are entering the hinterland of the two leading players in the industry, fighting with them and grabbing food from their mouths.

Two major directions for cracking involution: new scenes and going to sea

“In the past three years, Chinese video cloud service providers have worked closely with Internet video platforms, witnessing the second upsurge of China’s video cloud market; looking at the second half of video cloud, in addition to the in-depth development of high-definition Internet video, Chinese video platforms Going overseas and the new ‘fight between the virtual and the real’ have also brought a broad space for imagination to the market.” Wei Yunfeng, research manager of IDC China’s industry cloud services, recently talked about his prospects for the long-term development space of the video cloud market.

A video cloud industry insider told Zhishi that there are two main directions for cracking the “involution” of the video cloud, which has also become the field of competition for three-way video cloud players.

One is to seek innovation in updated scenarios such as finance, medical care, mobile social networking, as well as smart cockpits and metaverses.

For example, the current electric vehicle pays more attention to user experience, which cannot avoid real-time service technology, such as group voice service, which used to require walkie-talkie or WeChat voice, but now can add group voice service to the smart cockpit; in addition, through the video cloud The technology to see the situation around the car is also an innovative application of the video cloud in this scene; in the field of Metaverse, although the C-end self-financing Metaverse products are still uncommon in the market, in the exhibition and other scenes, you can already see some Clients are willing to invest money to transform existing scenarios into metaverse scenarios. At the same time, some enterprises need to conduct structured analysis of video content and carry out intelligent transformation of production and operation, including intelligent security, video banking, and remote court hearings.

It is foreseeable that the application scenarios and requirements of video cloud will change accordingly – the scenarios extend from traditional audio and video applications to e-commerce, cloud video conferencing, Internet communities and other scenarios; In the future, there will be higher-dimensional requirements such as intelligence and differentiation.

On the other hand, it mainly expands its business to overseas markets such as Southeast Asia, Europe and the United States.

From these two directions, cloud computing companies such as Alibaba Cloud and Huawei Cloud have taken intensive actions. For example, Alibaba Cloud recently announced that it plans to invest 7 billion yuan overseas within three years. Relatively speaking, the global short video business of Byte and Kuaishou may provide a lower entry base for its video cloud business and provide native video advantages.

Conclusion: spoiling the video cloud, the key battle of the “fourth cloud”

In 2022, the cloud computing market will be lively due to the entry of Byte and Kuaishou, and the video cloud has become the first step in cloud computing thrown by these two short video companies.

In many people’s minds, this is a Red Sea market. Although e-commerce live broadcasts to video conferencing, to the popular metaverse and digital people have made the market lively, there is still a big gap in the conversion of hot spots into sales. This is also a market first occupied by big companies such as Alibaba, Tencent, Shengwang, Baidu, and NetEase, accounting for nearly 70% of the market. If the volcano engine and Kuaishou remain in the competition in the stock market, it will only cause more extreme involution.

In the long run, ultra-high-definition, low-latency, immersion, and strong interaction will become the new direction of video cloud development. According to the report of IDC, a well-known research organization, from 2021 to 2026, China’s video cloud market will continue to maintain rapid growth, and the market compound annual growth rate is expected to reach 31.0%. If there is no rush to increase revenue, Byte and Kuaishou may be able to successfully disrupt the game with a lower video business foundation.

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-10-10/doc-imqqsmrp2102015.shtml

This site is for inclusion only, and the copyright belongs to the original author.