Editor | Yu Bin

Produced | Chaoqi.com ‘Yu see column’

Skyworth has been a little “lost” recently.

On the eve of the National Day, Skyworth Electric withdrew its IPO application on the Growth Enterprise Market. Even if the sponsor was CITIC Securities, everyone thought it was a powerful alliance, but the final result was that it was withdrawn sadly. What happened to Skyworth?

When it comes to Skyworth, the first thing that comes to mind is definitely Skyworth’s color TV. As for Skyworth’s refrigerators and washing machines, I am afraid that there are not many really impressed.

What’s more, the home appliance industry is no longer a blue ocean, but a red ocean with intense involution. Skyworth’s basic position in the home appliance market cannot be maintained. In recent years, it has fallen into the predicament of increasing revenue but not increasing profits.

It’s no wonder that Skyworth founder Huang Hong has the idea of building a car, but other home appliance companies such as Midea and Hisense, which also build cars, mostly cooperate with car companies.

Skyworth’s idea is different. It does not want to be a parts supplier for car companies, but wants to eat a fat man in one bite, and wants to build a complete vehicle as soon as it comes up. So the question is, does Skyworth really have the strength to build a complete vehicle?

There is no doubt that building a car is very expensive. If the electrical sector is successfully split and listed, it may be a little emboldened to build a car, but now that Skyworth Electric’s listing application has been withdrawn, what else does Skyworth use to build a car?

Compared with building home appliances, it is obviously more difficult to build a car. Since Skyworth Electric has not been able to go on the market, the original intention of Skyworth to build a car is probably still to take advantage of the wind of building a car.

Deeply caught in the dilemma of gross profit margin

Skyworth Electric, which withdrew its IPO application this time, is affiliated with the well-known Skyworth Group. However, compared with Skyworth Group, which specializes in color TVs, Skyworth Electric, which specializes in white goods, is not only competitive in the industry, market share, or technology. In terms of innovation, I am afraid that it is difficult to meet the requirements of the GEM for “innovation and entrepreneurship”, which is why Skyworth Electric was rejected by the GEM.

What is the current status of Skyworth Electric’s survival? We can find out from the prospectus.

Skyworth Electric’s current main source of income is white appliances such as refrigerators and washing machines. In 2021, Skyworth Electric’s revenue exceeded 4 billion for the first time in the IPO reporting period of the past three years, but the contribution revenue from refrigerators and washing machines reached 3.379 billion yuan. The proportion has exceeded 80%.

According to the prospectus, Skyworth Electric’s revenue in 2019, 2020, and 2021 were 3.685 billion yuan, 3.739 billion yuan, and 4 billion yuan, respectively; net profits were 175 million yuan, 152 million yuan, and 124 million yuan; net profit after deduction They were 137 million yuan, 104 million yuan, and 69 million yuan respectively.

Comparing the revenue and net profit of the last three years, it is not difficult to find that Skyworth Electric has fallen into the dilemma of increasing revenue without increasing profits.

From the perspective of the general environment, the entry of the home appliance market into the Red Sea period is a common problem faced by the entire industry. With the disappearance of the demographic dividend, the home appliance industry is bound to be in a stage of downward growth. These are all problems that Skyworth needs to face.

However, what makes Skyworth Electric difficult to say is that its gross profit margin is even lower than the industry average.

Skyworth Electric’s comprehensive gross profit margins from 2019 to 2021 were 14.96%, 13.19% and 11.74%, respectively, lower than the 22.93%, 21.37%, and 18.41% of Hisense Home Appliances, Haier Smart Home, Aucma, Changhong Meiling, Whirlpool, Omar Electric, etc. average gross profit margin.

Haier Zhijia, which also chooses to build cars, has a gross profit margin of 31.23%, but Skyworth, as a “poor student” in the home appliance industry, has taken the lead in the car building business. This is why I am afraid everyone knows it.

It is not difficult to see from the prospectus that even the existing profits of Skyworth Electric are inseparable from government subsidies and tax incentives.

edit

The prospectus shows that Skyworth Electric’s other income has a relatively high risk.

During the reporting period (2019-2021), other income was 18.66%, 42.51%, and 53.33%, and last year was more than half of the total profit.

Home appliances are already a mature industry, and if Skyworth still relies mainly on subsidies, it is no wonder that its IPO was rejected.

The real purpose of Skyworth’s car building, the answer is probably ready to come out.

OEM cannot save Skyworth

Is it possible for Skyworth to reverse the trend?

Skyworth Electric itself gave the answer in the prospectus, that is: Skyworth Electric will further deepen the cooperative relationship with Xiaomi Group.

Skyworth Electric provides OEM for Xiaomi and other Internet home appliance brands through ODM/OEM, which is also one of the main culprits of Skyworth Electric’s low gross profit.

Obviously, Skyworth Electric does not have an advantage in the competition with the leading companies in the home appliance industry. Without Xiaomi’s thigh, Skyworth Electric’s revenue is not guaranteed.

As the largest customer of Skyworth Electric ODM, Xiaomi contributed 536 million sales, accounting for 13.4% of the current sales.

What is embarrassing is that in 2001, Skyworth’s color TV sales ranked the top three in my country’s color TV industry, breaking the 7 billion mark, but now the subsidiary Skyworth Electric has been reduced to OEM for the younger generation Xiaomi.

Skyworth Electric also explained that its current main production and operation is based on the ODM/OEM (OEM) model, and the revenue of this type of business in 2021 will reach 2.28 billion yuan, accounting for 58.22%.

That is to say, Skyworth Electric’s business is not mainly from the sales of its own brand, and more operating income comes from the OEM processing model.

Under the ODM/OEM-based business model, the continuous decline in gross profit margins far below the comparable peers is an iron proof that Skyworth’s own “growth” and “innovation” are insufficient.

The gross profit margin is too low, and it is inseparable from the OEM model that Skyworth relies on to survive.

The production and operation mode of Skyworth Electric Appliances is its own brand and ODM/OEM (OEM). From 2019 to 2021, the proportion of ODM/OEM business revenue will be 49.53%, 56.18%, and 58.22%, respectively, and gradually increase.

It is precisely because of the over-reliance on the OEM business that Skyworth Electric’s R&D investment is not high, which further restricts the market performance of Skyworth Electric.

From 2019 to 2021, Skyworth Electric’s R&D investment was 136 million yuan, 137 million yuan and 151 million yuan respectively, and its R&D investment accounted for 3.70%, 3.66% and 3.78% of its operating income, respectively.

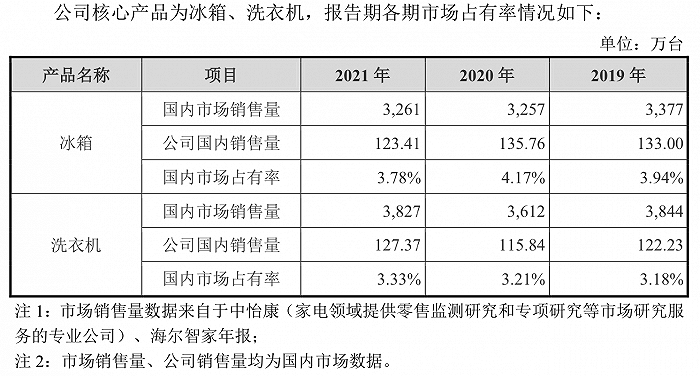

At the same time, the trend of head-to-head in the ice washing industry makes Skyworth Electric’s market share currently lower than that of top competitors. According to the disclosure of Skyworth Electric, the market share of Skyworth Electric refrigerators and washing machines in 2021 will only be 3.78% and 3.33% respectively.

In general, with the ODM/OEM business model as the main business model, revenue, net profit and gross profit margin have declined to varying degrees, and R&D investment is inefficient. growth-oriented enterprises” requirements.

Skyworth Group’s spin-off and listed subsidiaries are not only Skyworth Electric.

Coocaa Technology was established in 2006 and began to operate independently in 2014. It is the technology platform of Skyworth Group responsible for the operation of smart TV systems.

In March 2018, Coocaa Technology became a unicorn company with a valuation of nearly 10 billion in the OTT industry.

In the second half of 2020, Skyworth Group decided to spin off Coocaa Technology and go public independently. However, Coocaa Technology has not yet completed the listing.

Behind Skyworth Group’s busy “demolition and demolition”, it is inseparable from the weak growth of stock prices in recent years and the “insensitivity” of home appliance companies in the Hong Kong capital market.

As for why Coocaa Technology is mentioned, it is because it is a key part of Skyworth’s car manufacturing.

Building a car is not the antidote

The halfway through making mobile phones makes Skyworth more persistent in building cars.

However, its sales are not convincing. The EV6, which was delivered last year, has been on the market for more than a year. According to data from the Passenger Association, the cumulative sales of EV6 from January to August this year did not exceed 10,000.

The newly launched Skyworth HT-i has set a “military order” to sell 100,000 units in 2023.

But in the core technology of new energy vehicles, Skyworth HT-i uses the ready-made BYD DM-i hybrid system.

If Skyworth wants to stand on the shoulders of the giant BYD and take shortcuts, it may be questioning the ability of consumers to vote with their feet. After all, it is better to buy BYD directly than to buy Skyworth.

Skyworth Electrical Appliances, a subsidiary of Skyworth Group, is unable to guarantee the basic market, and he has not been able to take advantage of the trend of smartphones. Now he is directly building a car. I am afraid that he is wishing to go to the sky in one step. This step is really too big. Skyworth’s car sales have clearly given the answer.

Although Skyworth has Coocaa technology, it is difficult for Coocaa to empower Skyworth cars. Therefore, the main car-home interconnection function of Skyworth EV6 is difficult to imagine, and I am afraid it is just a gimmick of Skyworth Automobile.

After all, a cruel fact that Skyworth has to face is that its current car sales are too low, the number of car users is small, and car sales are far from supporting Skyworth’s smart car ecosystem.

Moreover, it is also unknown how much commercial value Skyworth’s high hopes can be released from the car home ecology.

Epilogue

By 2022, Skyworth Electric’s revenue will decline. In the first half of the year, Skyworth’s revenue was 1.622 billion yuan, a year-on-year decrease of 16.38%; net profit was 58.31 million yuan, a year-on-year increase of 0.83%; net profit after deduction was 43.185 million yuan, a year-on-year increase of 0.83% %.

Obviously, Skyworth did not excel in the electrical appliance business. Its profits depend on government subsidies, and its sales depend on brands such as Xiaomi. It can be said that it has not yet achieved the first place in the industry in the field that it is familiar with, and wants to make a bet on a new line. .

For Skyworth, the road of spin-off and listing does not seem to work at present, and there is a question mark as to how far Skyworth can go.

On the one hand, Skyworth’s white goods businesses such as refrigerators and washing machines have no bright spot in terms of market share and product competitiveness, both domestically and overseas.

On the other hand, the home appliance industry is a sunset industry, and neither capital nor the market is optimistic. In addition, the net profit of Skyworth Electric has declined year-on-year.

In this case, even if Skyworth Electric is forced to go public, it will be difficult to gain the favor of investors, and it is even less possible to have an ideal valuation. This is why Skyworth Electric chose to withdraw its IPO application.

On October 10, Skyworth Group responded, “Skyworth Electric will continue to promote the IPO in the future.”

But whether the next listing will be successful, I am afraid it is still unknown.

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-10-13/doc-imqmmthc0684766.shtml

This site is for inclusion only, and the copyright belongs to the original author.