At the sales level, traditional car companies have begun to encircle and suppress the new forces in car manufacturing.

At the sales level, traditional car companies have begun to encircle and suppress the new forces in car manufacturing.Welcome to the WeChat subscription number of “Sina Technology”: techsina

Article / Articles

Source: Cyber Car (ID: Cyber-car)

It should have been the peak sales season of “Golden Nine and Silver Ten”, but the new energy vehicle market in October this year was slightly flat.

From the perspective of the broader market, both the terminal retail and the estimated wholesale growth rate are smaller than the level of the same period last year.

Among the ten mainstream new energy vehicle brands that have disclosed sales, nearly half of the car companies showed a downward trend from the previous month.

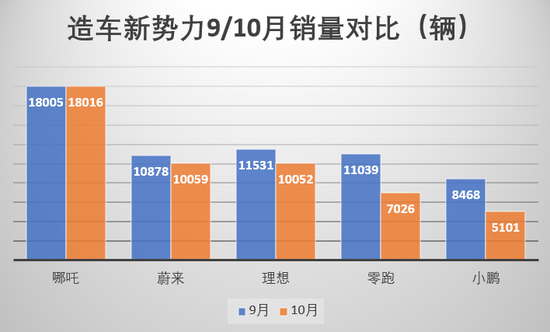

The worst is Xiaopeng Motors, which delivered only 5,101 vehicles in October, a 40% decrease from the previous month, and a direct cut from the same period last year.

Under the dullness, a new trend has also emerged in the domestic new energy vehicle pattern: at the sales level, traditional car companies are encircling and suppressing new car manufacturers.

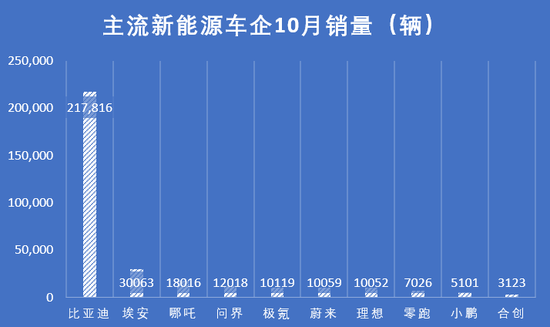

BYD, which occupies an absolute dominant position, sold 217,800 units in October, an increase of 8.38% from the previous month and a year-on-year increase of 168.8%. The results are still gratifying.

Among the top five car companies in terms of sales of new energy vehicles in October, Ji Krypton and Wenjie jumped to the top, and Nezha was the only one left in the new car-making force.

For details, let’s see together.

01

BYD’s sales exceeded 210,000, and Xiaopeng’s delivery was almost halved

The sales rankings of mainstream new energy vehicle companies in China in October are as follows:

Although the market is not so hot, BYD’s sales figures still did not disappoint.

Data show that BYD’s sales in October were 217,800 units, an increase of 8.38% from the previous month and a year-on-year increase of 168.8%. Among them, passenger car sales were 217,500 units, an increase of 8.2% from the previous month and a 239% increase from the same period last year.

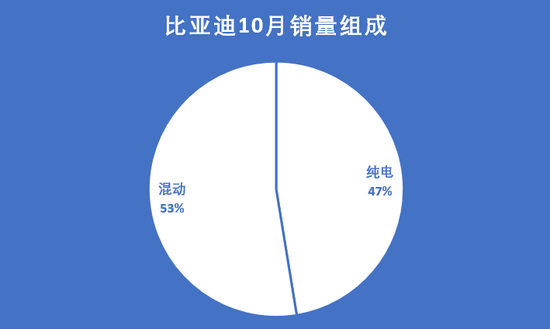

In terms of power, BYD sold 103,157 pure electric models in October, accounting for 47.4% of the total sales, and sold 114,361 hybrid models, accounting for 53.6%.

In terms of exports, BYD’s overseas sales in October were 9,529 units, an increase of 23% from the previous month’s 7,736 units.

In the main sales models, Song, Qin and Han are still the backbone of BYD’s sales. Among them, the Song family sold 56,843 cars in October, the Qin family sold 34,670 cars, and the Han family sold 31,614 cars. The sales of the three major families together accounted for 57% of YD’s total sales.

The sales of BYD Yuan and Seal series also exceeded 20,000 units.

From January to October this year, BYD’s cumulative delivery reached 1.4029 million vehicles, an increase of 158% over the same period last year. So far, BYD has achieved its annual sales target of 1.2 million units in 10 months.

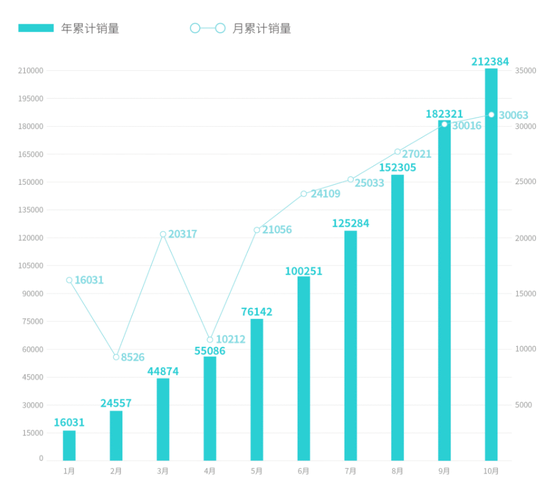

GAC Aian, which ranked second, sold 30,063 vehicles in October, an increase of 149% over the same period last year, and an increase of 0.16% over September, almost the same.

This is also the second consecutive month that Aeon’s sales have remained above 30,000 units.

From January to October this year, the cumulative delivery of Aeon also officially exceeded the 200,000 mark, reaching 212,400, an increase of 134% over the same period last year.

In the long-term trend, compared with the new forces of car-making and the new brands born out of traditional car companies, Aian’s advantages are further expanding.

However, it is worth noting that in the sales structure of Aian, the sales volume of the online car-hailing market is still relatively high.

According to the data on insurance coverage, in September this year, 8,771 new cars were registered as rentals in Aian’s sales, accounting for 38% of the monthly insurance coverage.

Limited by the sales structure and product price range, the tonality of the Aian brand has been difficult to improve. However, Aion’s high-end road is taking a different approach, and its newly released product series Hyper (Haobo) will undertake the task of Aion’s brand upwards.

According to the plan, Hyper (Haobo) will launch three high-end models of 300,000 yuan in succession next year, covering sedans, SUVs and MPVs.

As for whether this new stove can finally carry the banner, we will wait and see.

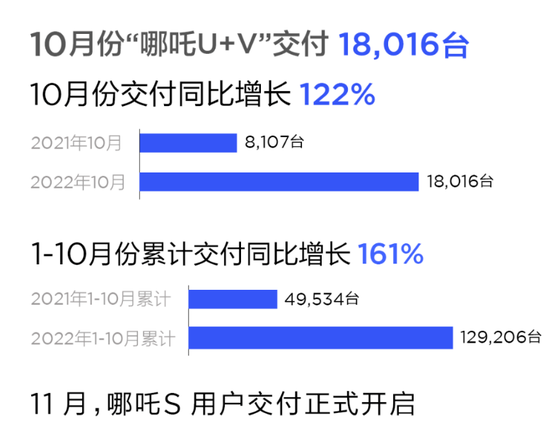

Nezha, which ranked third, delivered 18,016 vehicles in October, an increase of 122% over the same period last year and almost the same as last month’s 18,005 vehicles.

In the first 10 months of this year, Nezha delivered a total of 129,206 new cars, an increase of 161% over the same period last year.

In the long run, Nezha has already occupied the top of the sales volume of the new car-making forces, leaving Wei Xiaoli and Leipao behind.

In addition, according to Nezha Auto, its latest model, Nezha S, will be officially delivered to users in November. So far, Nezha has finally ushered in a change in the product structure that has long relied on the impulse of a 100,000-yuan car.

In addition to the two stable players Aian and Nezha, Wenjie and Ji Krypton can be said to be the biggest winners in October.

Let’s talk about the industry first. The delivery volume in October reached 12,018 units, an increase of 18.5% from the previous month, and the ranking jumped from the seventh place last month to the third place in one fell swoop.

Since Wenjie officially started delivery in March this year, Wenjie has delivered a total of 57,750 new cars.

Judging from the growth trend, from the start of delivery to the monthly delivery of over 10,000 vehicles, to the cumulative delivery exceeding 50,000 vehicles, the growth rate of Wenjie is astonishing. The jump in word of mouth may be the core factor.

In addition, bypassing the controversy of whether the technology is advanced, the power model of the extended program, the market competitiveness in terms of energy supplementation and energy consumption have been confirmed in the ideal car, and the world can quickly win a place in the new energy vehicle market. Not open for this reason.

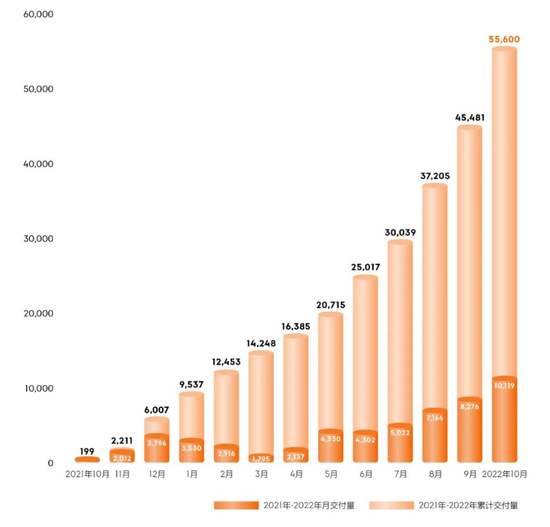

Also maintaining a high growth momentum in Hewenjie is Jikr, which delivered 10,119 new cars in October, an increase of 22.27% from September. This is also the first time that the monthly delivery has exceeded 10,000 units since the delivery of the Jikr brand.

Looking at the time line a little longer, Ji Krypton has officially started large-scale delivery of its first model, Ji Krypton 001, and it will be exactly one year until October this year. During the year, Jikr 001 delivered a total of 55,600 vehicles. As a high-end pure electric model with a price of more than 300,000 yuan, this performance is indeed remarkable.

Perhaps this kind of delivery performance has also accelerated the capital and product movements of the Jikr brand.

In terms of capital actions, the independent listing of Jikr A proposal to allow Ji Krypton to split.

The new product also accelerated the landing speed. On November 1, the second new car of JK, the JK 009, which sells from 500,000 yuan, was officially launched. According to the plan, this pure electric MPV will arrive in stores one after another on November 8, and delivery will begin in January next year.

At that time, whether the Krypton brand can take the delivery level and competitiveness to a higher level with the blessing of external capital, we can look forward to it here.

02

The new car-making forces are collectively weak in October

Combined with the market market and the internal competition of new energy vehicle brands, the sales pattern in October showed two obvious characteristics.

First of all, the so-called “Silver Ten” peak season did not arrive as scheduled, but appeared slightly mediocre.

According to data from Shanghai Insurance, in the four weeks of October this year, the terminal retail volume of the domestic new energy vehicle market was 410,000, a year-on-year increase of 44.36% and a month-on-month decrease of 17.6%.

In contrast, in October last year, the terminal retail sales of new energy vehicles in the domestic market was 321,000 units, an increase of 141.1% over the same period of the previous year and a decrease of 4% month-on-month.

According to the estimated wholesale volume disclosed by the Federation of Passenger Transport Associations, the estimated wholesale volume of the new energy vehicle market in October this year was about 680,000 units, an increase of only 1% from September and an increase of about 80% from the same period last year. Last year’s year-on-year growth rate was 148%, and the month-on-month growth also reached 6.3%.

Therefore, whether it is retail or wholesale, the growth rate is far from the level of the same period last year.

As for the reason for the lacklustre peak season, Cui Dongshu, secretary-general of the Passenger Federation, said in the sales analysis that it was mainly affected by the multi-faceted epidemic at the beginning of October, which led to a sharp drop in sales during the November Golden Week.

Secondly, under the chill, some people are happy and some are worried. Specifically, the new forces in car manufacturing are weak across the board, and new brands that have escaped from traditional car companies are gaining ground in the process.

The most obvious manifestation is that almost all of the new car-making forces have shown a downward trend from the previous month. For example, Ideal, delivered 10,052 vehicles in October, down 12.83% from September.

There is also Weilai, which delivered 10,059 vehicles in October, down 7.53% from September, and delivered a total of 92,493 new vehicles this year, an increase of 32% over the same period last year.

According to Li Bin’s previous goal of delivering 150,000 vehicles per year, it will take nearly 30,000 vehicles for NIO’s monthly delivery KPIs in the last two months of this year. The pressure is great and the difficulty is high, unimaginable.

If it is said that the decline of Weilai and Ideal has been very large, then looking at Leapao and Xiaopeng, it is insignificant.

Data show that Leapmotor delivered 7,026 vehicles in October, down 36.35% from the previous month. This figure also hit the lowest value in nearly 8 months.

At the same time, this is also the first delivery report card that Leaprun has come up with after its listing. Leapmotor’s share price also plummeted after its listing. As of the close on November 2, Leapmotor’s share price was reported at HK$18.52 per share, and its market value had evaporated by more than 60% compared with the time of issuance.

On Xiaopeng’s side, the delivery volume in October was 5,101 vehicles, a drop of 40% from the previous month, almost a halving trend. It is worth noting that this is also the fourth consecutive month of negative growth for Xpeng.

Looking further apart, Xiaopeng should be the one who can feel the crisis the most among the new car-making forces that are in deep trouble.

According to the data, among the models delivered by Xiaopeng in October, 2,104 units were delivered for the P7, 1,665 units for the P5, 709 units for the G3i, and 623 units for the Xiaopeng G9 in October.

The trend that can be clearly seen here is that the P7, which was once supported by Xpeng’s sales, is declining at a speed seen by the naked eye, and the Xpeng P5, which has been given high hopes, has not been responsible for the main sales force. As a flagship born G9, it is difficult to say what the future potential is.

In the final analysis, the decline is already present, accompanied by great future uncertainty.

In addition to the above four companies, Nezha, the only one that achieved positive month-on-month growth, also has a crisis looming.

First of all, in terms of product structure, Nezha’s long-term dependence on the impulse of two 100,000-yuan U+V cars still exists. As mentioned above, Nezha S, which is priced at 200,000-300,000 yuan, will be delivered this month. .

In other words, Nezha’s low-end product structure is about to change, but the question is, can Nezha S support the mid-to-high-end market?

Judging from the previous order volume, as of September 30, the order volume of Nezha S was 15,000. It is hard to say whether these order data can fundamentally change the reality that Nezha relies on the low-end market.

Each of the new car-making forces has its own difficulties in reciting scriptures. In contrast, the new brands of traditional car companies represented by Aian, Wenjie, and Jikr are afraid to laugh out loud.

Leaving aside Aian, who has already taken the lead, Wenjie and Jikr have been catching up faster and faster in the last 3 months, and there is already a trend of bucking the trend.

Taking Extreme Krypton as an example, after upgrading the Qualcomm 8155 cockpit chip in July this year, the growth in delivery has accelerated significantly. Within 4 months, the monthly delivery of less than 4,000 vehicles has quickly crossed the threshold of 10,000 vehicles.

The phenomenon is such a phenomenon, and the driving factors behind it are roughly as follows:

First of all, in terms of product strength, traditional car companies are making up for the shortcomings.

In terms of intelligence, since the beginning of this year, traditional car companies have adopted self-research + outsourcing solutions. On high-end models, like the new car manufacturers, they are equipped with intelligent core functions such as voice interaction, pilot assistance, and automatic parking. The leading edge of the new forces in intelligent driving and digital cockpits has been gradually weakened.

Secondly, in terms of product structure, the market segments that the new car-making forces were originally working on, and traditional car companies are also eager to move. Counterpoint.

Finally, in terms of product cost control, traditional car companies also have the strength to vertically integrate the supply chain and reduce production costs. In this regard, BYD is the one with the most experience.

In addition, in the wave of epidemics, we can also see that traditional car companies have also highlighted stronger crisis handling capabilities in response to such black swan events.

Taking BYD as an example, it has multiple production bases across the country, and it can still ensure that the market does not collapse amid a wave of regional epidemics, but new auto companies lack this confidence. Compared with the most obvious Weilai, it has been strangled by the epidemic more than once. This time in October is the most obvious example.

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: https://finance.sina.com.cn/tech/csj/2022-11-04/doc-imqmmthc3220130.shtml

This site is for inclusion only, and the copyright belongs to the original author.