Welcome to the WeChat subscription number of “Sina Technology”: techsina

Text / Wuzhou

Source: Node Finance

“After cutting in half, you can cut in half again.” Joe, the owner of the pet store, became angry when he saw a white pedestal sweeper placed in the corner. A year ago, she spent nearly 4,000 yuan to start this treasure on a certain Dong.

The product is really easy to use. It is very clean after sweeping off twice. After finishing the work, it can automatically return to the base station to automatically collect dust and clean the mop. All of a sudden, Joe’s hands are greatly freed, and he no longer has to worry about pet hair floating all over the floor and messy footprints of customers.

Soon, Joe, who had studied finance, began to rise from satisfaction with the product to an interest in the company behind the product. She found that the target company not only has obvious leading advantages, but also the penetration rate of the sweeper category in China is still quite low. Unable to resist the urge in his heart, Joe bought some observation positions.

However, this impulsive behavior made Joe suffer for more than a year.

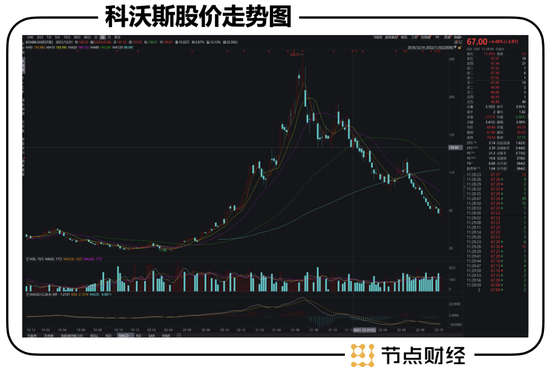

Just a week ago, the stock price of the target company in which Joe held a position once fell below 60 yuan per share, making Joe’s floating loss more than 75%. There is also the above exclamation.

Node Finance believes that in the past year, there have been many investors who have fallen on the sweeper track like Joe. Up to now, Ecovacs and Stone Technology, the two major domestic listed clean electrical companies, have retreated by 63% and 64% respectively in the past year, which is significantly higher than the 15% of Wind All-A in the same period.

What we are curious about is why the share price of the leading clean electrical appliance, which was once regarded as a “category opportunity”, fell so badly? Secondly, the two companies continue to increase revenue but not profit. Does it indicate that the industry pattern is beginning to be disturbed? Finally, after the slowdown in the expansion of the entire clean electrical appliances, is the investment logic of the low penetration rate of this track still valid?

share price Waterloo

After losing 75%, Joe still has no idea.

Fortunately, the early torment made her greatly reduce her expectations for this position, and she didn’t even have any hope of unwinding, but under the “broken window effect”, she was not in a hurry to clear the position and accrue losses.

Let’s review how Joe’s favorite target company, Ecovacs, fell from the altar?

Going back to the end of April 2021, the first quarterly report released by Ecovacs showed that the company’s revenue increased by 131% year-on-year, and the net profit attributable to the parent increased by 727% year-on-year.

The performance that exceeded expectations immediately ignited the company’s share price. In just 80 days, Ecovacs’ share price rose from 120 yuan per share to 250 yuan per share in mid-July, more than doubling.

Since then, although the stock price of Ecovacs has adjusted somewhat, it has remained above 160 yuan per share under the catalyst of the company’s strong performance in the second and third quarterly reports.

In the next 10 months, the trend of Ecovacs’ share price has become a nightmare for investors. The company’s stock price has almost plummeted, from 160 yuan per share to the recent 65 yuan per share, with a maximum retracement of more than 60%.

Why is the faucet of the sweeper not fragrant?

Performance performance may explain more than half of the problem. In the four quarterly reports that Ecovacs has released since the beginning of this year (Q4 in 2021, and Q1-Q3 in 2022), the year-on-year growth rate of the company’s net profit attributable to the parent is: 73.8%, 27.2% %, -12.3%, -48.9%.

That is to say, not only has the profit growth rate that was doubling at every turn disappeared, but it has also gone to the other extreme—continuous negative growth.

For growth stocks like Ecovacs, the capital market usually gives a certain valuation premium for its eye-catching performance growth rate, and when the high growth rate is no longer, the speed of capital abandonment is also fast.

And retail investors like Joe will be immersed in the company’s high growth rate expectations, and they will forget that Ecovacs’ previous three consecutive quarters of high performance growth were partly based on the company’s low performance base of divesting its foundry business in 2019. An unsustainable fact.

The decline in performance is usually accompanied by a shrinking valuation. As of now, the price-earnings ratio of Ecovacs has plummeted to 20 times, further in line with home appliance stocks.

The same troubled brother is Stone Technology, a company that was once dubbed a “sweeper” because its share price exceeded 1,000 yuan. In just ten months, its share price plummeted by 65%, and its market value evaporated by more than 36 billion yuan.

Compared with Ecovacs, Stone Technology may be even worse.

The company’s “recession” time was earlier. In the six single quarters from the second quarter of 2021, four quarters of Roborock Technology’s net profit attributable to the parent fell into negative growth, and even in the third quarter of this year, even revenue also experienced negative growth.

It can be seen that the slump in the leading stocks of clean electrical appliances is not an exception. The reasons behind this are many of the weak domestic macroeconomic effects and the impact of high inflation in overseas markets on the demand side. But the most important thing that cannot be ignored is the phenomenon of increasing revenue but not increasing profits in the industry.

Relative to the forced slowdown of the demand side, the supply-side changes caused by intensified competition may rewrite the story of the track.

Roll to new heights

“We still hold high-quality companies with excellent business models, clear market structure and strong competitiveness,” said Zhang Kun, a well-known fund manager, in the fund’s third quarterly report.

These short three sentences are also a measuring stick to test whether our investment can make people sleep at ease.

But it’s easier said than done. An investor like Joe who has no confidence in his heart, how should he evaluate the market structure and profitability of the leader in cleaning appliances in the next three to five years.

At present, these three sentences correspond to Ecovacs and Stone Technology. If the first two sentences can barely be matched, then I am afraid there will be a big question mark on the compatibility of the third sentence “competitiveness”?

What is “strong competitiveness”, in Node Finance’s view, is the monopoly of consumer minds brought about by a broad moat, such as Moutai for high-end liquor, iPhone for smartphones, and even Gree air conditioners for air conditioners.

Due to the obvious product differentiation of these companies and the consumer mentality priority formed by years of word-of-mouth communication, the risk of share decline brought about by industry competition is almost locked.

Corresponding to Ecovacs and Stone Technology, do you dare to say that when you mention sweepers or floor scrubbers, you can think of them both? If you think about it further, if other brands of products are cheaper, will you still insist on buying Ecovacs or Stone Technology?

The reason for the concern of “lack of competitiveness” is that in the third quarter of this year, Ecovacs and Roborock Technology both increased their revenue but not profits.

Specifically, Ecovacs’ revenue increased by 14.4%, but its net profit attributable to its parent company showed a negative growth of nearly 49%; in the same period, Stone Technology’s revenue increased by 0.65%, and its net profit attributable to its parent increased by 34.5%.

The common reason behind this is all “surge in marketing expenses”. Among them, the marketing expenses of Ecovacs in the third quarter increased by 47.3% year-on-year, which has exceeded the revenue growth rate for four consecutive quarters; Stone Technology’s marketing expenses in the third quarter increased by 49.9% year-on-year, which has exceeded the revenue growth rate for six consecutive quarters. revenue growth.

Marketing expenses growing faster than revenue growth means that sales conversion rates are lower, and as a result, marketing expenses erode net profit. In the third quarter, Ecovacs’ net profit margin was 7.42%, a decrease of 9.21% from the same period last year, and Stone Technology was 16.2%, a decrease of 8.41% from the same period last year.

The implication is that due to the need for advertising, the net profit margin of both companies is close to halving.

As for why you spend so much money on marketing?

Some investors believe that the clean electrical circuit is in the growth stage, and it is worth spending money to grab market share. In fact, it is not. From the point of view of Node Finance, the two companies are forced to spend money on marketing.

The reason is simple: cleaning the electrical track is currently very curly.

Taking the sweeper as an example, in the sweeper evaluation video of a certain station of Node Finance research, the flagship machines of many brands, including Ecovacs and Stone Technology, are very similar in terms of product technical functions and price selling points. Consumers’ purchase of products is mostly in a state of uncertainty.

Source: Pippi Ai, the main UP master of station B, measures the sweeper

Source: Pippi Ai, the main UP master of station B, measures the sweeperIf the sweeper has established certain competition barriers due to lidar and software algorithms, then for the hand-held sweeper, the entry threshold of the category is lower, and it has only been two years since the development of this category has been superimposed. The melee was brutal.

According to the data of Aowei Cloud, in 2020, there were only 15 brands engaged in the washing machine business. By the first half of this year, this data has exceeded 100. Moreover, compared with the sweeper, the market share of the head brand of the washing machine has also declined significantly.

According to Aowei Cloud.com, in the third quarter of this year, Ecovac’s Timco brand accounted for 48.5% of the share of online sweepers (in terms of sales), ranking first. However, due to competition, the market share fell by 13.9% compared with the same period last year. percentage points, which is a far cry from about 70% in 2020.

The good news is that in the field of sweepers with high competition barriers, the leading position is temporarily stable. According to data from Aowei Cloud.com, in the third quarter of this year, Ecovacs still maintained the first online listing share with 40.6% (by sales), and Roborock Technology ranked second.

Node Finance believes that the future pattern of the sweeper category will tend to be stable, but the category growth rate is not optimistic; and the brand pattern of the scrubber category is very likely to change.

hopeless

Back to Joe’s investing experience.

What moved Joe to invest in Ecovacs was not only the performance of the all-around sweeper that frees his hands, but also the logic of the growth stock with low penetration rate of the sweeper category.

According to this logic, the 30% and earlier 10% penetration rate nodes are important investment opportunities. The supply of this level of products is in short supply, the performance of related companies has continued to grow rapidly, and the capital market has given a higher valuation premium.

New energy vehicles are a clear example. Before 2021, the penetration rate of new energy vehicles in China is less than 15%. The biggest problem faced by new car manufacturers is insufficient production capacity. In the context of continuous losses, the company’s market value is so high.

Today, the penetration rate of new energy vehicles still climbs to nearly 29% (October 2022). The main contradiction of new car manufacturers is no longer production capacity, but sales volume, and the market value has returned a lot from the high point.

According to estimates, the penetration rate of domestic sweepers in 2021 will be between 6% and 10%, which is in the stage of introduction and outbreak. Another major category of washing machines, which was born in 2020, is expected to exceed 10 billion yuan in sales this year. According to the estimated sales volume of 3.7 million units at the end of this year, the penetration rate is less than 4%, which is also in the introduction period.

However, what is interesting is that the category of scrubbers is still continuing the blowout growth trend, but the category of sweepers has returned to calm early.

According to CMM data, in the first half of this year, the growth rate of retail sales of floor washing machines was 83.9%, while that of floor sweepers was only 16.2%. Going back further, in the three years from 2019 to 2021, the year-on-year growth rate of retail sales of floor cleaning machines The score is 2.4%, 18% and 28%.

Although referring to the permeability theory, the sweeper category is in the introduction period, but the actual growth rate has not followed the “script”. The reason behind this is that there are two points in Node Finance’s thinking. First, the sweeper is a non-just-needed product that belongs to consumption upgrades. Its purchase necessity is not as necessary as the white-electricity products that are just-needed, such as the ice washing machine, and the penetration rate logic should be discounted; , There is a substitution effect between the two categories of scrubbers and sweepers, and the rise of scrubbers will suppress the volume of sweepers to a certain extent.

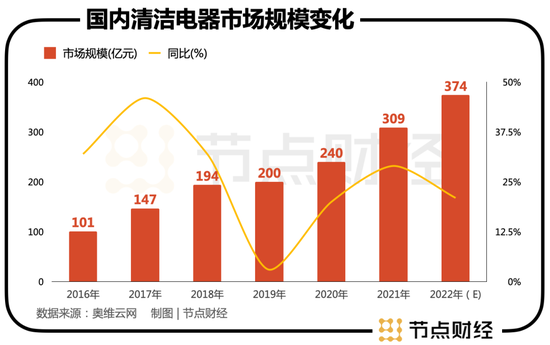

In addition, from the perspective of the expansion trend of the entire clean electrical appliance sector, from 2016 to 2021, the total industry scale will increase from 10.1 billion yuan to 30.9 billion yuan, with a compound annual growth rate of 25%. This growth rate is related to cosmetics and some new consumption. The speed of the track is not much different.

Investors deserve to see opportunities in this industry, structural opportunities in categories to be exact.

Specifically, among the 30.9 billion yuan of cleaning appliances in 2021, sweepers occupy the first place with a share of 38.8%, wireless vacuum cleaners occupy the second place with a share of 26%, and floor washing machines occupy the third place with a share of 18.7%. , but the growth rate of the washing machine is the highest.

According to the forecast of Aowei Cloud, in 2022, the industry scale of clean electrical appliances will rise to 37.4 billion yuan, of which washing machines will exceed 10 billion yuan, and the annual growth rate will exceed 70%. The part that exceeds the industry growth rate is actually It is eroding the share of other categories, such as cordless vacuums and sweepers.

From this point of view, there are huge flaws in the investment logic of the low penetration rate of sweepers.

Returning to the specific company, Ecovacs has now formed a dual-category matrix of “Covacs + Timke” for sweeping and washing. In the future, in the environment where the competition of floor washing machines is uncertain, the position of floor washing machines will stabilize and risk hedging will be carried out. . On the other hand, in the context of the difficulty in breaking through the bottleneck in the field of sweeping machines, Roborock Technology has higher uncertainty to impact the share of washing machines.

What is certain at present is that it will become more and more difficult for the two to make money in the future.

As of the first three quarters, Ecovacs’ net profit attributable to its parent has fallen by 15.65%, and Stone Technology has fallen by 15.85%. Considering the sluggish consumption environment and the lower sales net profit rate in the fourth quarter due to the Double Eleven promotion, it is expected that both parties Net profit for the year fell by more than 15%.

This means that the net profit of both parties this year is not as large as last year. Combined with the background of the limited overall growth rate of the industry and the surge in marketing expenses, it is difficult for investors like Joe to get involved in the short term.

Node Finance Statement: The content of the article is for reference only. The information or opinions expressed in the article do not constitute any investment advice, and Node Finance does not assume any responsibility for any actions taken due to the use of this article.

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: https://finance.sina.com.cn/tech/csj/2022-11-04/doc-imqmmthc3325108.shtml

This site is for inclusion only, and the copyright belongs to the original author.