Welcome to the WeChat subscription number of “Sina Technology”: techsina

Text | He Jinyi, Zhang Ranran, editor | Fu Xiaoling, Cao Binling

Source: outside and inside

Data Support | Insight Data Research Institute

The day before yesterday, the ideal 22Q1 financial report was released, and the data was outstanding: revenue increased by 167.5% year-on-year; the overall gross profit margin was 22.6%, continuing the high level of 22.4% in the previous quarter.

The expectations were fulfilled, and the market was also very satisfied – on the day of the earnings report, the single-day increase exceeded 10%.

Does this scene seem familiar?

Two months ago, in the 2021Q4 financial report, the performance of the ideal “Swordsman” – the only one that is profitable among the new forces with a single model, has won the market’s optimistic expectations that it exceeds the “threshold”.

And we have analyzed in the article “Ideal “Flaws”, “The limitations of ideal ONE’s success have changed, and the new product positioning may not be realized” and other hidden risks, which cannot support such extreme optimism.

In this season, Ideal has clarified that the future realization support is: to carry out the route of the milk dad car to the end, and by 2025, it will create a “big explosive product combination” logic within the price range of 200,000-500,000 yuan.

However, such a corporate strategy is contrary to the trend of structural changes in the overall demand of the new energy vehicle industry – the gradual strengthening of cost performance and the decline of high-end prosperity.

In other words, in the current new energy tram sector, the year-on-year sales growth rate is faster than the “price butcher” cost-effective models, and the allocation of capital is also here. After all, the structural α is obvious.

It is difficult to have any capital that will betray its own “class” – rejecting the relatively high sales growth of Volkswagen trams, and deploying high-end trams with low prosperity.

From harvesting the new middle class to “sinking”?

From last year to this year, there have been some interesting changes in the sales rankings of the new energy vehicle industry:

For example, the sales volume TOP15 in April last year showed that “Wei Xiaoli” was on the list, and the ideal ONE was ranked 5th;

However, in March of this year, Weilai had no such person in the TOP15, and the sales of Ideal ONE also dropped to No. 8.

The BYD Qin plus DM-i and BYD Song Plus Dmi, who squeezed out the ideal ONE position, were ranked 12th and the other was not on the list.

The reason why they were able to catch up from behind was in fact, to a certain extent, it was because of the light of “Wei Xiaoli”.

According to the data, BYD Qin plus DM-i and Song Plus Dmi are technically the same as the ideal ONE, both of which are oil and electric dual-use models. However, their price ranges are all between 100,000 and 200,000; the ideal ONE is around 330,000.

That is to say, they are equivalent to the “ideal cost-effective ONE” route.

So, why do the new forces of “high force” actually want to give way to “cost-effective”?

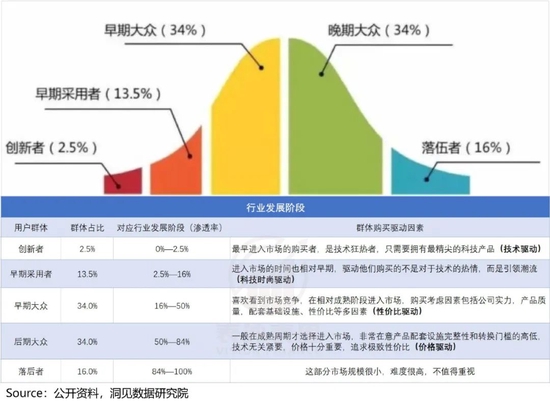

In fact, this is in line with the law of industry development. The book “Innovation Diffusion Theory” has demonstrated that in the process of the gradual popularization of new products, the speed of user acceptance is different.

According to the acceptance speed, the expansion stage of the user group can be divided into five stages. The specific evolution process is as follows:

At present, from the perspective of the popularization process of new energy vehicles, the expansion of user groups is also in line with this theory.

In the early penetration stage, most of the main users who buy are “early adopters”. This group of early adopters will have one characteristic: they have the ability to think independently, are not easily influenced by the outside world, and have the attributes of public opinion leaders.

Based on this, it is often the characteristics of trendy, advanced and other products that drive their purchasing decisions.

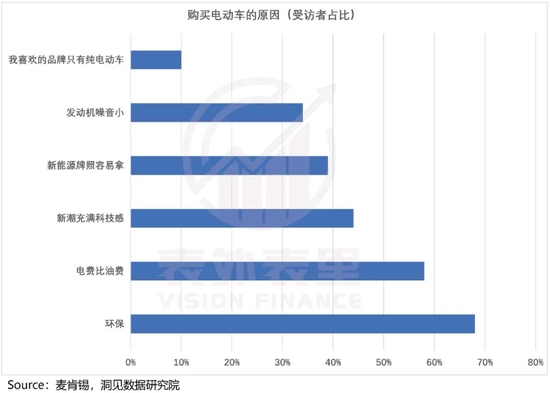

For example, a Hangzhou ES6 owner shared that he was going to replace the BMW 5 Series with NIO ET7, just because: “ET7 can bring me more freshness, I am still young, and I am willing to accept new things.”

The same is true abroad. For example, McKinsey’s 2019 Auto Consumer Report shows that 44% of respondents are most concerned about “trending and full of technology” when purchasing electric vehicles.

Auto companies such as Ideal, which are positioned in the high-end market, either rely on high-quality experience or relatively advanced technology to take up the “early adopters” needs of early adopters. While their own sales volume is considerable, they also drive the penetration rate of new energy vehicles to continue to break through.

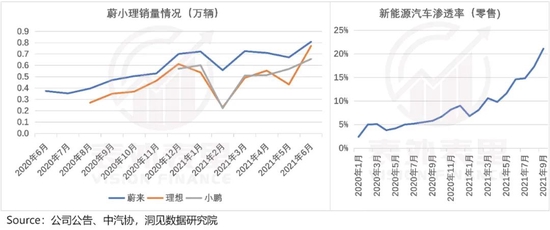

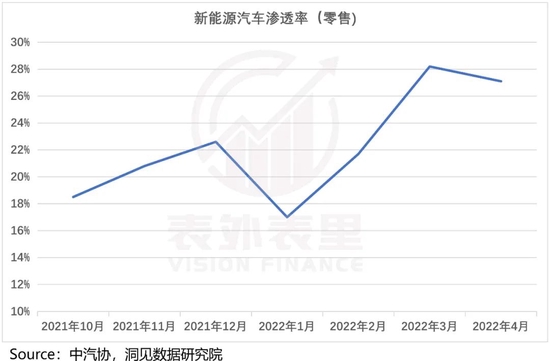

As shown in the figure below, as of September 2021, the penetration rate of new energy vehicles has reached about 20%.

With a group of mainstream early adopters and good sales growth, Wei Xiaoli’s stock price has risen rapidly since mid-2020.

But the “early adopter” group is not infinite, accounting for only 13.5%. To usher in a larger number of users, it is necessary to cross the chasm and enter the “early mass” stage – this group accounts for 34% of the market.

The objective rule is that the purchasing decisions of these groups are driven by strong practical ideas. The factors they care about include company strength, product quality, supporting infrastructure, and cost-effectiveness.

However, the imperfect charging infrastructure of electric vehicles in the early days brought mileage anxiety and restricted practicability; coupled with the high price, this group was blocked out.

In this way, it is not difficult to understand why BYD Qin plus DM-i and BYD Song Plus Dmi, which are taking the “cost-effective version of the ideal ONE” route, are able to catch up in sales compared to the ideal ONE.

And as mentioned above, the penetration rate of new energy vehicles exceeded 20% in September 2021, which means that the industry as a whole has crossed from “early adopters” to “early public”.

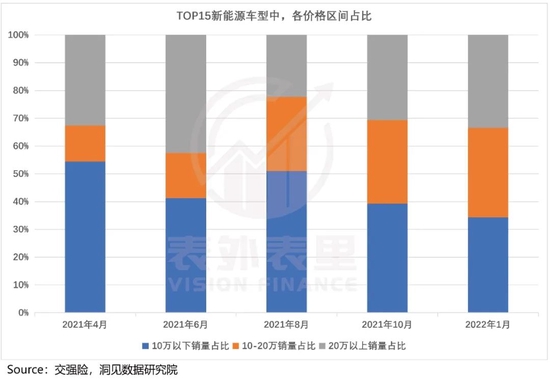

This is also reflected in the market structure – the proportion of products that cater to the needs of the “early public” is increasing.

As shown in the figure below, among the TOP15 new energy models, in April 2021, the sales volume of 100,000-200,000 models accounted for only 13%; in January 2022, this proportion increased to 32.2%.

Benefiting from the shift in demand, BYD’s sales even surpassed Tesla (China) in the second half of 2021.

The sales growth space is released, and the market is also looking good. As shown in the figure below, even in the headwind stage, BYD’s share price performance is relatively stable.

At present, the penetration rate of new energy vehicles is close to 30%. With the in-depth development of the industry, terminal consumption will further penetrate into the “post-mass” consumer group.

This part of the group will be more sensitive to price and pursue the ultimate cost-effectiveness.

This means that in the future, the new energy tram market, with structural opportunities, will be in the mass market penetration stage.

That is, what we said at the beginning, the relatively high-growth sector.

Changes in the structure of consumption preferences will inevitably lead to different “relative growth rates”, which will inevitably affect investment decisions in the capital market. So, how did the former leader ideal deal with the situation?

Can the explosive combination strategy “magic defeats magic”?

In fact, the ideal does not want to be a practical “Nokia”, but to be an “Apple”.

In the latest Q1 conference call, the management looked forward to product planning and said: Li Auto’s product portfolio is similar to the iPhone, and will launch an explosive product in the price range of 200,000-500,000 yuan, and every 100,000 yuan price range.

Obviously, such a product portfolio strategy does not follow the objective development law of the industry. The Li Xiang team did not succumb to market preferences, but instead firmed up on their own line.

Based on this, we have reason to worry that the year-on-year sales game after the ideal may not be able to compete with car companies that play the “cost-effective” card, thus affecting the performance of the company’s capital market.

Of course, this is only a theoretical deduction, not an absolute fact. After all, the ideal explosive logic also has feasibility support:

As discussed in the article “The “Defects” of Ideals, ideals have always been anchored by the needs of fathers, and the “beautiful” of the ideal one in the field of family cars originates from this.

And the evolution of “single big explosive product” to “big explosive product combination” is to “catch all” the incremental space of the target group.

For example, according to this performance meeting: by 2025, the company’s strategy is still to serve family users with children, so we will launch products that match the space size needs for them.

To put it bluntly, we will further subdivide families with children. In the mid-to-high-end range, every 100,000 price range, make a hit product, and then replicate the record of the hit ideal ONE in the price range of 300,000-400,000 – 2021 , the Ideal ONE occupies more than 30% of the market share of new energy vehicles at this price.

From the current point of view, the L9 (ie X01), which will be delivered in the third quarter, is priced at 450,000-500,000, which is a product with a price increase; while the product in the price range of 200,000-300,000, the medium-sized car, will be listed next year.

So, switching to the perspective of consumption, is such an arrangement reasonable?

According to data from the China Automobile Association and estimates by Industrial Securities, the demand for family vehicles in 2021 has reached 5.71 million units. After that, with the release of the three-child policy and the escalation of demand, this part of the market may continue to increase.

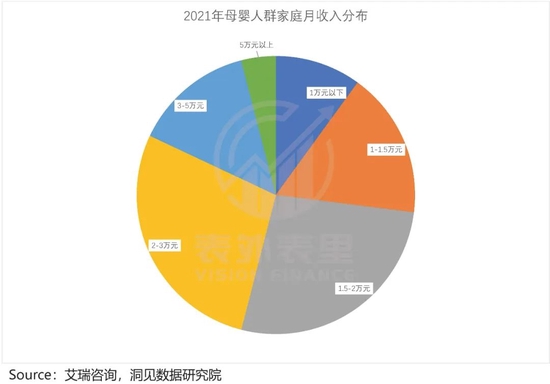

According to iResearch, in 2021, more than 75% of mothers and infants will have a monthly income of more than 15,000 yuan; more than 70% of second-child families will have an annual income of more than 200,000 yuan.

That is to say, the demand space and consumption level of family cars have considerable potential.

However, the market is currently in supply, and demand is dislocated.

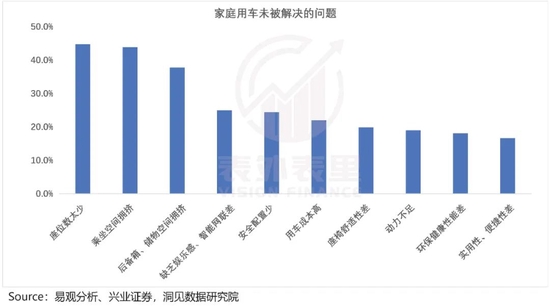

On the one hand, there are not many options for family cars. As shown in the figure below, more than 70% of households believe that many vehicles have a lot of trouble in terms of space (number of seats, cockpit space and cargo space), safety (assisted driving functions) and riding experience (comfort and smart cockpit).

On the other hand, models that can better solve the pain points of demand have relatively high prices:

From this point of view, the ideal price range combination strategy can theoretically solve this contradiction between supply and demand, and has the possibility of “realization”.

It has to be said that Li Xiang’s team has strengthened its strategic positioning and entered a relatively blank spot in the selection; its attitude towards the objective laws of the industry seems to be that it is a secondary contradiction or relatively unimportant.

This is obviously a wonderful unknown game.

If the L9 and the new model that will be launched next year can replicate the success of the ideal ONE as expected, then of course there is not much problem.

But this is only an optimistic expectation, and it depends on the actual situation.

summary

The “early adopters” of the new middle class who have raised the market position of the new power in car manufacturing are actually limited in scale and cannot withstand several rounds of harvesting.

If the new energy industry wants to usher in a larger number of users, it is bound to cross the gap and expand to the “early mass” group, which accounts for 34% of the market; and the industry itself, the expansion of the scale will inevitably experience a drop in product prices .

In the context of such an industry turn, Ideal insists on the strategy of using “big explosive product combination” to capture all the needs of dads in the mid-to-high-end market. Can it “defeat magic with magic”? It can only be said that there is a possibility, and the probability is a matter of opinion.

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-05-12/doc-imcwipii9441848.shtml

This site is for inclusion only, and the copyright belongs to the original author.