Welcome to the WeChat subscription number of “Sina Technology”: techsina

Text / Ruonan Shuichi

Source: Bueryanjiu Research (ID:bueryanjiu)

This year’s Double Eleven, Hong Kong stocks will usher in the “first cross-border shoe and clothing stock” – Zibuyu is expected to be officially listed on the Hong Kong Stock Exchange on November 11, with the stock code 02420.HK.

Zibuyu Group Co., Ltd. (hereinafter referred to as “Zibuyu”) is one of the largest cross-border e-commerce companies in China. According to its new prospectus citing the Frost & Sullivan report, based on GMV in 2021, its It ranks third among all platform sellers in China’s cross-border B2C e-commerce apparel and footwear market, with a market share of 0.4%.

▲ Source: pexels

▲ Source: pexelsZibuyu announced that the IPO plans to sell 29.25 million shares globally, of which 2.925 million shares are offered in Hong Kong, accounting for about 10%; the international offering is 26.325 million shares, accounting for about 90%. Its offering price is HK$7.86-9.42 per share, with lots of 500 shares.

According to Zibuyu’s new prospectus, ‘Buer Research’ found that in the first half of this year, its revenue was 1.278 billion yuan, a year-on-year increase of 16.07%; in the same period, its adjusted net profit was 61 million yuan, a year-on-year decrease of 46.33%.

At the same time, Zibuyu has the operational risk of relying on a single platform. In the first half of 2022, its revenue from Amazon’s single e-commerce platform has reached 90.6%.

From 2019 to 2021, Zibuyu’s three-year cumulative revenue was 6.952 billion yuan, but its dependence on the Amazon platform increased year by year.

In an old article last October, we focused on the lack of diversity in Zibuyu and the unsolved “parasitic disease” of Amazon. Today, Zibuyu, who is about to become the “first stock of cross-border shoes and clothing”, still relies heavily on a single e-commerce platform, and the risk of “stuck neck” also makes the business full of hidden dangers. As a result, ‘Fuji Research’ updated some of the data and charts of the old article last October, the following Enjoy:

Have you ever heard of Zibuyu, who are often in “fast fashion”?

Zibuyu, which sounds more like a book title at first glance, is actually a cross-border trading company specializing in trendy women’s clothing, covering more than 80% of the world’s countries and regions. The boss started his business with cottage women’s clothing, and was once known as the “Chinese version of Zara” in the industry.

▲ Source: pexels

▲ Source: pexelsAs the king behind the scenes of more than 1,000 different overseas stores and more than 300 differentiated brands, Zibuyu is even more low-key in China.

After five years, Zibuyu once again stood in the spotlight of the capital market: From 2019 to 2021, Zibuyu’s revenue increased year by year, and the revenue in 2020 was nearly 1.9 billion; but the marketing expenses in the same period also increased year by year. Marketing and advertising expenses were 263 million yuan.

‘Buer Research’ found that by the end of the first half of 2022, over 90% of Zibuyu’s revenue came from third-party e-commerce sales platforms, and over 90% of its revenue came from footwear and apparel; at the same time, its revenue was highly dependent on US market.

Lack of diversity, how to make up for Zibuyu? When the new trend of cross-border e-commerce is gradually formed, the competition on the track is becoming increasingly fierce; listing is just a new beginning for Zibuyu.

The rise of copycat women’s clothing

The founder of Zibuyu, Hua Bingru, graduated from Chaohu College in Anhui Province. As a sophomore in 2009, he opened his own Taobao store in his dormitory to distribute clothes and shoes produced in Guangdong and Fujian.

After graduating in 2011, when everyone around him was worried about finding a job, Hua Bingru had achieved financial freedom and went to Hangzhou with his classmates to start Zibuyu in Binjiang District.

▲ Source: pexels

▲ Source: pexelsAt first, Hua Bingru was still in his old business, selling fake women’s clothing on Taobao, and within a year or so, he broke into the top ten of Taobao’s weekly transaction volume, with sales exceeding 100 million.

Realizing the risks of copycats, Zibuyu began to change his direction by virtue of his sensitive sense of women’s clothing, from buying goods from the market to self-design and factory OEM.

At this time, it is a period of rapid development of women’s fast fashion. Everyone is wearing this “meat”, the competition is becoming more and more fierce, and the cost is rising year by year. Hua Bingru chose a different approach, targeting the untapped overseas women’s clothing market such as Brazil and Russia, and selling the products on AliExpress, the “international version of Taobao”, which also contributed to Zibuyu’s transformation and concentrated on cross-border business .

On June 30 last year, Zibuyu Group officially submitted its listing application. In fact, as early as January 2017, Zibuyu hired an intermediary for counseling and established a corresponding shareholding platform, but due to many unstable factors, it was finally settled.

According to the prospectus, in the first half of 2019-2022, Zibuyu’s operating income was 1.429 billion, 1.898 billion, 2.347 billion and 1.278 billion respectively. During the same period, the net profit was 81 million, 114 million, 201 million and 61 million respectively.

However, Zibuyu’s performance growth rate does not seem to have kept pace with the industry and is lower than the overall growth level of its domestic peers. Data from the General Administration of Customs shows that in 2021, my country’s cross-border e-commerce exports will reach 1.98 trillion yuan, a year-on-year increase of 15.0%; in the first quarter of this year, my country’s cross-border e-commerce import and export scale was 434.5 billion yuan, a year-on-year increase of 0.5%.

It looks like a good performance, but there is a big hidden danger behind it. In 2019, Zibuyu’s asset-liability ratio was as high as 86%. Although it will drop to 73.2% in 2020 due to financing and performance growth, it is still at high risk.

Zibuyu officials attributed the high debt to the relatively slow repayment speed of third-party platforms and relatively heavy asset operations, which required continuous capital investment, resulting in a high debt ratio.

The analysis of ‘Fuer Research’ believes that although Zibuyu’s performance seems to be clear on the surface, it is in urgent need of listing and financing or to ease the pressure of its high debt.

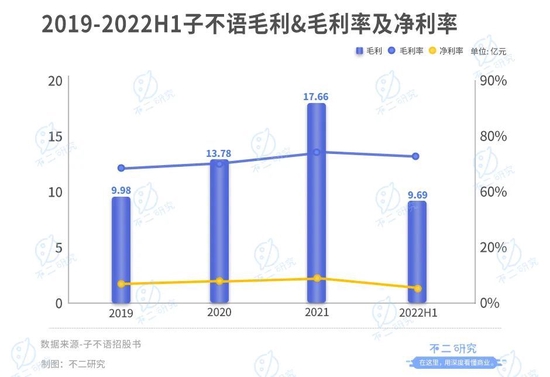

Looking at the gross profit of Zibuyu, in the first half of 2019-2022, it was 998 million, 1.378 billion, 1.766 billion and 969 million respectively, with a gross profit margin of 69.8%, 72.6%, 75.2% and 75.0%.

In contrast, its net interest rate has only been 5.7%, 6.0%, 8.5% and 4.8% in the past three and a half years. Zibuyu said that due to the excessive growth of general and administrative expenses, the increase in administrative costs affected the net profit.

In addition, the prospectus shows that in the first half of 2019-2022, its marketing and advertising expenses were 116 million, 263 million, 319 million, and 192 million respectively; the proportion of total sales expenses in the same period was 8.1%, 13.9%, 13.6%, 15.0%.

According to ‘Buer Research’, Zibuyu’s increasing marketing and advertising expenses may be eating away at its net profit. If Zibuyu wants to go a long way in the women’s clothing industry, he must first jump out of the dilemma of burning money for marketing and growth, and build his own brand moat.

Escape from “dependency”

According to Zibuyu’s prospectus, its revenue sources are divided by sales channels, which are mainly divided into third-party e-commerce platforms and self-operated websites (and others). In the first half of 2019-2022, revenue from third-party e-commerce platforms accounted for 91.9%, 79.3%, 87.4% and 94.0%, respectively.

Although Zibuyu consciously began to cultivate self-operated websites, the proportion of revenue from third-party e-commerce platforms has been declining year by year; but by the end of 2020, nearly 80% of the revenue came from third-party e-commerce sales platforms, and only 20% of revenue from self-operated websites.

Zibuyu’s over-reliance on third-party e-commerce platforms makes its operation risky.

Taking a closer look at the revenue of third-party e-commerce platforms, the prospectus only lists specific data from Amazon and Wish; eBay and AliExpress are classified as others, and the revenue share is not high.

As of the first half of 2022, the revenue from the Amazon platform accounted for 90.6% of the total revenue, and the revenue from the Wish platform accounted for 1.7%. Over-reliance on third-party platforms has multiplied Zibuyu’s risks; nearly 90% of them bet on Amazon and Wish, and the hidden danger of over-dependence is undoubtedly “worse”.

There are even pessimistic industry insiders who call the marketing e-commerce model that relies too much on third-party platforms as the “parasitic e-commerce” economy.

From a regional point of view, Zibuyu products are sold to end customers in more than 80% of the world’s countries and regions, but from the prospectus, it is mainly cultivated in the European and American markets, with the United States as the top priority.

As of the first half of 2022, Zibuyu’s revenue in North America accounted for 95.5% of the total revenue, of which the United States accounted for 95%; the revenue from Europe accounted for 3.6% of the total revenue; and only 0.3% from Asia, which shows that its contribution to the United States The preference of the market, but on the other hand also exacerbates the risk of “rebellion” in the single market.

According to a report from China Business News in September last year, last year Amazon took a large-scale action against Chinese sellers on the platform. The official response process has totaled 3,000 accounts of 600 brands in the past five months. These sellers have multiple, Repeated and serious abuse of comments, many of which are large buyers such as Aoji, Pattonson, and Zebao. And Amazon is one of the most important platforms.

Although it is different from other cross-border sellers’ “distribution” model, in the context of Amazon’s severe rectification, Zibuyu’s “boutique” model is also facing tests.

The hidden risks of lack of diversification are not only hidden in sales channels and regions, but also extremely unbalanced in business planning.

Although the product structure has been adjusted in recent years, according to its prospectus, sales of apparel products will account for 70.5% of total revenue in 2020, and footwear products will account for 21.1%, and the combined revenue of the two will account for more than 90%, which also means Its category dependence is also at high risk.

According to ‘Buer Research’, Zibuyu has certain hidden risks in terms of sales channels, regional planning, and category division. Although it adjusts its product structure and tries to diversify its revenue structure, its competitors are running out of time.

Competition for new outlets intensifies

Different from the cross-border e-commerce clothing brand SHEIN, Zibuyu is more like an invisible brand kingdom.

If you visit overseas websites, you may easily find SHEIN, but “Zibuyu” is not easy to appear – the latter exists behind the scenes in the form of more than 300 differentiated brands and more than 1,000 different stores.

Many people in the industry regard Zibuyu as the “Chinese version of Zara” – it is also a fast fashion line with low price and volume, which may allow it to quickly occupy the market; but the hidden dangers cannot be ignored: if you can’t grasp market changes, keep up with Fashion trends, Zibuyu’s future profitability may be affected.

Explosion is not easy, and there are risks. Although the multi-brand strategy brings opportunities, it also increases the risk of stockpiling. After all, not every brand can sell well.

▲ Source: pexels

▲ Source: pexelsPreviously, the state’s “Opinions on Accelerating the Development of New Formats and New Models of Foreign Trade” has clearly pointed out that the pilot work of cross-border e-commerce retail imports should be carried out steadily. The Opinions clearly encourage eligible enterprises of new foreign trade formats and new models to raise funds through listing, issuance of bonds, etc.

Zibuyu is taking advantage of the new cross-border e-commerce market to accelerate its sprint for IPO.

On the other side of the coin, the entry of a lot of capital into new outlets has suddenly increased Zibuyu’s competitors; it may face the risk of dividing up traffic and compressing market share.

According to data from Tianyancha, in the first half of 2022, a total of 25,090 cross-border e-commerce-related enterprises were added across the country, a year-on-year increase of 367.49%. Among them, 2,593 were added in the second quarter, a year-on-year decrease of 18.79%.

At the beginning of last year, ByteDance announced its entry into cross-border e-commerce, which made waves in the industry. Previously, big companies such as Ali and JD.com entered the game one after another, and other players such as Yangquan, Dunhuang.com, and Koala E-commerce have long been on the hills; even the national trendy brands such as Perfect Diary and Huaxizi have also opened up cross-border battlefields.

Under the new trend of cross-border e-commerce, the giants bring the “Matthew effect”, and the competition on the track is also intensifying. Even after Amazon’s “banning tide”, it does not seem to have damaged the confidence of Chinese sellers.

‘Buer Research’ believes that when the new trend of cross-border e-commerce is gradually established, a large number of sellers flood into the track, or push up the cost of cross-border marketing, etc., Zibuyu will face more challenges. When there are more and more competitors in this cross-border dispute, can Zibuyu still stabilize his “jianghu” status?

BUFF bonus or challenge added?

As a key node for cross-border e-commerce exports, Amazon launched “Black Friday Worth Deals” on October 4 last year to kick off a holiday shopping season expected to be disrupted by shipping and supply chain issues.

In the post-epidemic era, the test of supply chain logistics for cross-border e-commerce is evident.

When the competition in the new cross-border e-commerce market intensifies, compared with the Internet giants entering the game, Zibuyu still needs to “make up lessons” in supply chain logistics, digital management, big data analysis, etc., and will still face many challenges in the future.

At the same time, it has become a trend for cross-border e-commerce to land on the secondary capital market: some of them were broken when they went public; In the capital market that votes with feet, how does Zibuyu make investors believe and favor its story?

Some references for this article:

1. What good stories can Zibuyu tell? “, BT Finance

2. “Apparel e-commerce “Zibuyu” IPO again after 4 years, as high as 86% debt ratio, what does Hua Bingru think? Operator Finance

3. “Amazon starts Black Friday deals ahead of schedule, and courier fees also increase due to energy issues”,

Cross-border logistics has long known

4. “Amazon’s first response to “banning”: expelled 3,000 accounts from 600 brands”, Yicai.com

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: https://finance.sina.com.cn/tech/csj/2022-11-10/doc-imqmmthc4037596.shtml

This site is for inclusion only, and the copyright belongs to the original author.