Welcome to the WeChat subscription account of “Sina Technology”: techsina

2023 is just around the corner, and spring will always come.

Source: Zinc Scale

Writer/Chen Dengxin Editor/Wen Zhizhou

2022 is coming to an end, and it is time to submit the answer sheet.

This year, the Internet giants have worked hard to improve their internal skills, and it has become the consensus of the industry to lose weight and lose weight. The performance of Baidu, JD.com, and Tencent has shown great resilience; new energy vehicles are still hot, and BYD, which stands out, has come from behind and competed with Tesla. ; Photovoltaics is booming, and all kinds of capital are eager to become “light chasers”…

However, there are also companies that are struggling.

Some companies had to bleed to go public, and were voted by the capital market with their feet; Instead, it became a laughing stock.

In 2022, the joys and sorrows of the world are not connected.

keyword 1

plummeted

Bleeding to the market, capital is ruthless

In 2022, the difficulty of “snowballing” is quite high, and the first to bear the brunt are Chinese concept stocks.

Due to the superposition of multiple factors such as the complex international environment, the global economic downturn, and poor financial report data, all companies labeled as “Chinese concept stocks” have been hit more or less, and have endured too much unbearable weight.

Under heavy pressure, Chinese concept stocks have stepped into the abyss.

According to Flush data, as of November 28, 2022 Beijing time, the annual declines of the Dow Jones, S&P 500 and Nasdaq were 5.48%, 15.53% and 28.24% respectively, while the annual decline of the Nasdaq China Golden Dragon Index It is 37.99%, which is embarrassing.

It should be noted that during the same period, the annual declines of the Shanghai Composite Index, Shenzhen Component Index, ChiNext Index and Science and Technology 50 were 15.42%, 27.11%, 30.81% and 28.99%, respectively, which also confirmed the desolation of Chinese concept stocks from the side.

In this regard, “Internet Phantom Thieves” said: “The capital market is most concerned about deducting non-net profit and cash flow. Companies that can do it can increase their valuation against the market, and companies that can’t do it can only continue to collapse.”

Against this background, well-known Chinese companies are less interested in IPOs in the United States.

The only ones that can be sold throughout the year are Polestar Automobile, one of the new car-making forces, and Atour Group, a mid-to-high-end hotel chain, and both have suffered from the cold reception of the capital market.

For example, the Polestar car is a Volvo, but it is Geely’s key weight to seize the opportunity of the new energy vehicle track and win the game. The new forces are overwhelmed, and the feeling is hard to describe. From this perspective, the importance of Polestar Automobile to Geely is self-evident.

Polestar Motors was listed on Nasdaq backdoor on June 24, 2022. The opening price was US$12.98, and the current stock price is US$8. The stock price has shrunk by 38.37%, and the market value is only US$16.88 billion. Before the listing, its overall valuation The value is around $25 billion.

Institutional ratings are bearish

Institutional ratings are bearishIn addition, Wanwuyun, Leap Motors, and SenseTime, which are listed in Hong Kong, are not optimistic.

Among them, Shangtang Technology is the most eye-catching. It once had a market value of 325 billion Hong Kong dollars, but it was abandoned due to continuous losses in performance: on November 8, 2022, Alibaba reduced its holdings by 80 million shares. Holding 73.25 million shares, the current market value is 57.96 billion Hong Kong dollars.

A private equity person told Zinc Scale: “These unfavorable companies have serious valuation bubbles before IPO. They either never make a profit, or jump repeatedly on the verge of profit and loss, and add up to the unfavorable international environment. Investors? So much patience to listen to their stories.”

Keyword 2

impetuous

Ambition up, reality down

In addition to the dust from the listing, the fierce game between strong expectations and weak reality has become a key factor for the continuous decline in the market value of some companies, and Wei Xiaoli is a typical representative of it.

In 2022, Wei Xiaoli’s ambitions are not small.

Nio CEO Qin Lihong said: “In the past year, the average monthly sales volume of BMW 3 Series has been more than 12,000 vehicles. With the delivery of ET5, the sales volume of ET5 will exceed 3 Series within a year.”

He Xiaopeng said: “Xiaopeng G9 has enough confidence in sales. We believe that next year it will exceed the scale of Q5, allowing G9 to reach a monthly sales of 10,000 units in the field of large five-seat luxury SUVs, representing China’s competition with the world!”

As for Li Xiang, he is even more high-profile: “Thank you for your expectations for the ideal L9, the best family flagship SUV within 5 million? Yes!”

Despite this, Wei Xiaoli did not stage a growth miracle again, but was a bit ill-fated.

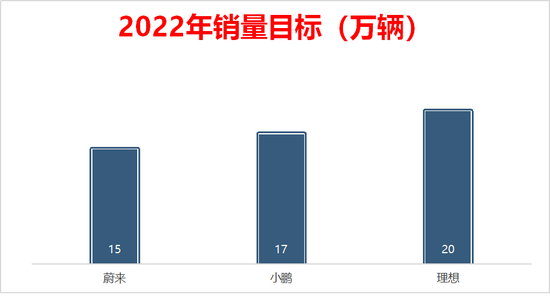

According to public data, Wei Xiaoli’s sales in 2021 are 91,400, 98,200, and 90,400 respectively, and the sales targets for 2022 are 150,000, 170,000, and 200,000 respectively. As of the end of November, Wei Xiaoli’s deliveries were 106,671, 109,465, and 1,120.13 million, with sales rates of 71.11%, 64.39%, and 56%, respectively.

The data comes from “Yuanchuan Automobile Review”

It can be seen from the above that Wei Xiaoli’s life is not easy.

Correspondingly, traditional car companies have accelerated the pace of catching up and staged a good show of overtaking.

Aion under GAC, Wenjie, a cooperation between Celes and Huawei, Shenlan under Changan Automobile, and Polestar under Geely Automobile have all gained momentum, eroding Wei Xiaoli’s market share.

More importantly, BYD’s sudden emergence has overwhelmed Wei Xiaoli’s voice.

Once upon a time, BYD was at the bottom of the chain of contempt for cars, and its reputation has always been low. The outside world ridiculed BYD car owners in an endless stream, and there were even malicious slanders.

Right now, it is the most popular new energy car company. Not to mention the early completion of the annual sales target of 1.2 million vehicles, it has become the only opponent who dares to challenge Tesla.

After all, Tesla cut prices to promote sales, and BYD raised prices to lock in orders.

The reason for this has a lot to do with Wei Xiaoli’s “moat” not being wide enough.

An industry insider told Zinc Scale: “The entry threshold for new energy vehicles is not high, which attracts everyone’s covetousness. Although traditional car companies turn around slowly, Wei Xiaoli’s first-mover advantage gradually fades as more players enter the game. Some players overtake it. Sooner or later.”

The above-mentioned industry insiders further stated that the scale effect of traditional car companies is more obvious, the supply chain is more stable, the technical background is deeper, the bargaining power is stronger, and the cost of trial and error is lower. In-depth cooperation naturally has the basis for latecomers and first comers.

Keyword 3

jealous

The second curve, hard to find across borders

Compared with blind optimism, cross-border is more worrying, and it is often a waste of energy to achieve nothing. Even so, it still cannot stop the enthusiasm of enterprises, because they are eager to find the second curve.

In 2022, three tracks will become the main positions for crossovers.

The first is the coffee track, which attracts drug sellers, clothes and shoes sellers, tea sellers, etc., and is dubbed by the industry as “Three Hundred and Sixty Lines, All Lines Sell Coffee”;

The second is the photovoltaic track. Those who dig coal, make paper, raise pigs, sell milk, and sell electrical appliances have poured in, causing the supply and demand of the industrial chain to become unbalanced;

The second is the new energy track. Those who sell black sesame, titanium dioxide, iron ore, and tourism are betting on it, eager to get a share of it.

Finding the second curve has become the consensus of most enterprises crossing borders.

Taking Midea Group as an example, the operating income in the first three quarters of 2022 will be 271.775 billion yuan, a year-on-year increase of 3.36%; the net profit will be 24.47 billion yuan, a year-on-year increase of 4.33%, which is still positive growth at first glance.

But if you look deeper, the problem becomes serious.

In the first quarter of 2022, Midea Group’s operating income growth rate was 9.54%, and net profit growth rate was 10.97%; in the second quarter, operating income growth rate slowed down to 0.97%, and net profit growth rate slowed down to 3.24%; In the third quarter, the growth rate of operating income further slowed down to 0.02%, and the growth rate of net profit further slowed down to 0.33%.

Midea’s performance slows down

Midea’s performance slows downThe trend of the chain going bad is visible to the naked eye.

Ever since, Midea Group has set its sights on breaking through the ceiling of the industry to photovoltaics, trying to inject new impetus into its performance.

A market participant told Zinc Scale: “There is nothing wrong with cross-border, but the underlying logic of cross-border is to continue the core competitiveness to a new track. If this logic fails, cross-border becomes a trial and error, and in the end it will either end without a problem, Either the marketing is greater than reality, or it tells a story to the capital market.”

All in all, 2022 is coming to an end, and some companies have not found a methodology for performance growth and market value growth. Most of the methods of listing, cross-border, and innovation that carry the ambitions of companies have failed, and instead paid a lot of tuition.

Fortunately, 2023 is just around the corner, there is no winter that cannot be overcome, and there is no spring that will not come.

(Disclaimer: This article only represents the author’s point of view, not the position of Sina.com.)

This article is reproduced from: https://finance.sina.com.cn/tech/csj/2022-12-04/doc-imqqsmrp8542320.shtml

This site is only for collection, and the copyright belongs to the original author.