We are all mortals, as long as we enter the stock market, it is inevitable to make mistakes. The important thing is how do we learn from these mistakes? This starts from 2015 after my retirement.

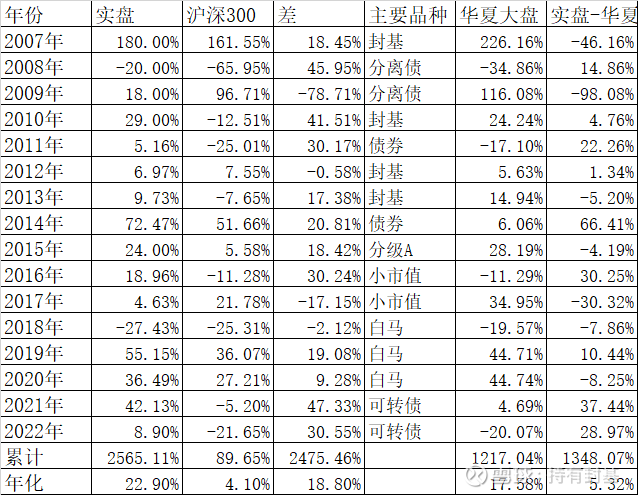

In the first half of 2015, due to illness, I did not trade a penny in the stock market. Although the stock market plummeted in the second half of the year, I chose the full position rating A and beat the market by a large margin. At that time, I considered multi-strategy diversification of risks, learned about Nut.com, which does not require programming, and researched day and night, and finally determined the small market value strategy.

In 2016, starting from the circuit breaker, the Shanghai and Shenzhen 300 fell by 11.28%, which continued the bear market in the second half of 2015, but because I fully invested in the small market value strategy, I even made a profit of 18.96% that year.

Outperforming the market by a large margin twice in a row is unavoidably high-spirited, and because of the many quantitative articles I wrote on Xueqiu, the number of fans has increased greatly, and it feels like the sun is shining all the way. Unexpectedly, in the next 2017, because Liu Shiyu cracked down on shell resources, the small market capitalization strategy would fail. In 2017, the Shanghai and Shenzhen 300 Index rose by 21.78%, but my annual return was only 4.63%.

2017 was a big blue-chip white-horse style. At that time, I mistakenly learned the lesson of small market value and turned to white-horse blue-chip. What’s more, I misunderstood value investing. When the big bear market came, I was always full of positions, and the final account totaled for the whole year A loss of 27.43%, not only created the highest loss ratio in history, but also created the highest loss in history.

What is even more ironic is that if I stick to the small market capitalization strategy, the loss and loss ratio in 2018 will be much smaller. At this time, the test is coming. Should we continue to stick to the white horse strategy, or switch back to the small market capitalization strategy?

I remember very clearly that in 2018, I bought Moutai for about 500 yuan, but not long after I bought it, in October 2018, I encountered the only lower limit in Moutai’s history. Moutai fell by 24.81% that month, almost a quarter of its value one.

In other words, should a strategy that seems to have failed should be persisted? A successful strategy is easy to stick to, and a failed strategy is easy to give up, but is this failure short-term or long-term? This requires our investors to calmly judge.

At that time, I judged that there was still a market for white horse stocks based on the fact that A shares rose too much and fell too far. As a result, starting from 2018, I held white horse stocks led by Moutai for 3 years, especially in 2019 and 2020. achieved good returns in the year.

So when did Moutai’s valuation become high? By the middle of 2019, Moutai was already close to 1,000 yuan, and some people said that 1,000 yuan was a top, because the PE at that time was close to 40 times, which was already at a high level historically. But I firmly believe that the characteristics of A shares will definitely rise too far. As for where the top is, I don’t know, so I can only wait for the right side.

As a result, everyone knows that Moutai will rise to 2,600 yuan at the beginning of 2021. The funny thing is that when some people said that 1,000 yuan was the top, when it rose to 2,600 yuan, someone actually saw 3,000 yuan.

I have been getting it in the middle of 2021. At that time, it took a month to backtest a large amount of convertible bond data. I judged that the annual yield center of convertible bonds was about 35%, and Moutai had already fallen by about 2,000 yuan at that time. Now, it is almost impossible to increase by 30% to 2600 yuan. So in the end, I made up my mind to clear all the white horse stocks led by Moutai, and exchanged all positions for convertible bonds.

In the end, Moutai, which I held heavily in, fell from 2,000 yuan to the current 1,600 yuan, China Merchants Bank fell from 51 yuan to 34 yuan, and Longji fell from 63 yuan to 48 yuan, which fell by 20%, 33%, and 24% respectively. It has increased by 43% in more than 1 year. The difference between one in and one out is astonishing.

Summing up the experience of failure and success, I strongly feel that successful strategies in the past do not represent future success; but strategies that failed in the past do not represent future failures. The failure of a white horse in a bear market does not mean the failure of a white horse in a bull market, and the success of a white horse in a bull market does not mean the success of a white horse in a bear market.

Most of the successful strategies that ordinary people encounter are dependent on the inertial thinking path, which is the root cause of the failure of many people’s white horse strategies in the past two years.

This time, I was able to hold Moutai and other white horse stocks for three full years from the middle of 2018 to the middle of 2021 and convert them into convertible bonds until today. Many people are very envious. Among them, I have a few experiences: 1. Stick to Moutai Three years is not a valuation. If you look at the valuation, the valuation has reached a historical high when Moutai was around 1,000 yuan in the middle of 2019, but the highest has reached 70 times. This is what most people did not expect of. When I fell to 2,000 yuan, I concluded that it would not be possible to return to 2,600 yuan in the short term. In addition, the results of backtesting convertible bonds strengthened my confidence in changing positions. 2. The quantitative model I use requires a large amount of data to be “fed”, which is also an important reason why I did not take a heavy position in convertible bonds early. I am not very good at analyzing personal debts using traditional methods. There are advantages and disadvantages, and the disadvantage is that you have to wait for the accumulation of a large amount of data before you can analyze it, and the more data, the better the effect. 3. Comparing white horses with convertible bonds requires familiarity with different varieties. The cross-variety comparison is a concrete manifestation of my investment thinking of “replacing depth with breadth”. On the one hand, there must be a sufficient circle of competence, and on the other hand, the proficiency in the use of quantitative tools is also required. These are exactly what I have. Of course, success also has a certain chance. Don’t be discouraged when you encounter failure. You must carefully analyze the reasons and accumulate experience.

At the same time, don’t give up easily when you encounter a failed strategy. The most typical one is the small market value strategy. Although it failed seriously in 2017, the effect in the next few years is actually quite good. In the past few months, I allocated about 7% of the small market capitalization for new development. I did not expect that the recent performance of the small market capitalization not only far exceeded the convertible bond strategy, but also outperformed most of the indexes in November.

Therefore, no matter whether it was a successful strategy or a failed strategy in the past, whether it can be used in the future, or just looking at historical performance, the most important thing is to predict future performance, make relative comparisons, and finally determine which ones are heavy positions, which ones are light positions, and which ones to give up.

There are 30 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/6146592061/236985044

This site is only for collection, and the copyright belongs to the original author.