Welcome to the WeChat subscription account of “Sina Technology”: techsina

Text/Yu Songye

Source/New Entropy (ID: baoliaohui)

“I hope that the price of SHEIN clothes will not increase because of TikTok.” In May 2020, a girl from California, USA left such a sentence on social platforms.

At that time, SHEIN had set off a wave of cheap fast fashion in North America and Europe. Cheap prices, many styles, and fast new releases were SHEIN’s indomitable killers. SHEIN’s advertisements on social media such as TikTok helped SHEIN expand rapidly.

In August 2020, SHEIN completed the E-round financing with a valuation of US$15 billion. By the time of SHEIN’s F round of financing in April 2022, SHEIN’s valuation has exceeded 100 billion US dollars. As of now, SHEIN is already the third largest unicorn company in the world, second only to Bytedance and SpaceX.

But two years ago, the California girl’s message on social platforms became a prophecy. In the past year, there have been more and more complaints about the gradual price increase of SHEIN on overseas social media. “Whichever sells well, the price will increase.” Many overseas consumers have discovered this price increase law of SHEIN.

Profit pressure before listing, rising fixed costs, and ESG (environmental, social, and corporate governance) disputes have forced SHEIN to raise prices. However, the price of SHEIN products after the price increase is almost the same as that of fast fashion brands such as ZARA and the product prices of e-commerce platforms such as Amazon, and no longer has a price advantage.

To make matters worse, overseas products from Ali, Pinduoduo and Douyin Group are encircling and suppressing SHEIN in all directions. Among them, the fierce play of Temu, a cross-border e-commerce platform of Pinduoduo, forced SHEIN to speed up the pace of accumulating consumers.

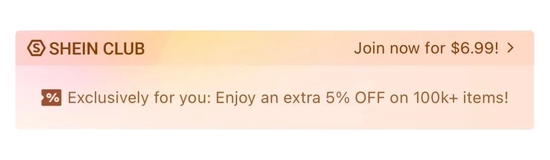

“New Entropy” exclusively learned that SHEIN has recently begun to test the membership system in the United States and launched the “SHEIN CLUB”. Users spend $6.99 per quarter and can enjoy exclusive 5% discounts on more than 100,000 items and other discounts. SHEIN has not yet launched a membership system in other countries and regions, but it is predicted that it will be gradually launched in the future.

Today’s SHEIN seems to have embarked on the old path of Taobao, that is, while the platform is being transformed and upgraded, it has encountered a battle to defend the sinking market. If SHEIN is not paying attention, its entrenched overseas sinking market will fall.

SHEIN has raised prices in an all-round way, starting with popular models

The price increase of SHEIN in various countries has certain inflationary factors. Since 2022, the exchange rate of most currencies in the world against the U.S. dollar has been declining, and the depreciation rate has exceeded the RMB, so the regular price increase of SHEIN is a normal phenomenon. But the problem is that even in the United States, consumers feel that SHEIN is raising prices.

In late October, an American consumer complained on social media: “This (explosive T-shirt) is almost sold out, and SHEIN raised its price.” On social media at home and abroad, many consumers invariably concluded that Out of SHEIN’s price increase law, that is, which product sales increase, which product will continue to increase in price. A number of Canadian consumers said that the prices of the products they have been fancy on SHEIN in the past year have increased by 1.5-3 times within a month. It can be determined that the price increase of SHEIN is actually higher than the global inflation level.

Consumers complain about SHEIN price increase on social media

Consumers complain about SHEIN price increase on social mediaIn addition to price increases, SHEIN has also gradually reduced user discounts and benefits. “New Entropy” learned from American consumers that the previous regular discounts were not limited to new and old users, but now only new users can enjoy them. SHEIN used to have no threshold for free shipping on Sundays, but now it needs to be over $9.9 to get free shipping. The return period has also been shortened, from 45 days to 35 days.

In other countries, some consumers also said that the threshold for free shipping has become higher and the return period has been shortened. Some consumers in Singapore even said that SHEIN now needs to deduct $3 for each item of return, which greatly reduces the attractiveness to consumers. There are indications that SHEIN has accelerated the pace of increasing profit margins.

According to research data, the net profit rate of SHEIN in 2021 will be around 6%. According to the report of Guosheng Securities in November 2021, the net interest rate of SHEIN is 5%-10%. The net interest rate of clothing industry giants is generally above 10%. The net interest rate of Inditex, the parent company of Zara, is about 11.7% in fiscal year 2021. The net interest rate of Fast Retailing Group, the parent company of Uniqlo, is about 12.37% in fiscal year 2022. 12.9%. On the whole, the profit margin of SHEIN is at a relatively low level in the industry.

For SHEIN, the low net interest rate means that its profitability is doubtful and its ability to resist risks is poor. More importantly, the growth rate of SHEIN has slowed down in 2021, dropping sharply from 250% growth in 2020 to 60%, which is about to peak. In the context of seeking to go public, SHEIN’s continued low profit margins make it difficult to meet the requirements of the capital market.

On the other hand, the rising costs of production, warehousing, logistics, and advertising, as well as the ESG controversy, have forced SHEIN to raise prices.

On the production side, SHEIN’s extreme pressure on suppliers has caused many suppliers to give up cooperation with SHEIN. A former supplier of SHEIN told “New Entropy”: “SHEIN only allows the factory to earn 1-3 yuan for each piece of clothing. If the sales of which one is not good, the merchant needs to digest the inventory by itself, and the manufacturers can only sell the clothes that cannot be sold. Switch to domestic sales and put them on domestic e-commerce platforms for sale. However, because the clothing is more European and American, many styles cannot be sold in China at all, and the manufacturers can only bear the losses themselves. Cooperate again and stop losses in time.”

It is understood that most factories with little experience and few orders are willing to place SHEIN orders. SHEIN’s reputation among suppliers has deteriorated, which is bound to affect its bargaining power. Since the beginning of this year, SHEIN has focused on attracting investment in the fields of men’s clothing and children’s clothing with higher average prices and profits, and has also begun to develop mid-to-high-end lines, which will be transmitted to the supply side. Suppliers’ profit margins will also increase, which is bound to increase SHEIN purchase cost.

In addition, the shooting cost of SHEIN is also a production cost that is difficult to optimize. SHEIN launches thousands of new SKUs every day, but the inventory of each model is very small, and the inventory of a single SKU is mostly within 100 pieces, and non-explosive models do not make up orders. But each model has to be photographed, and more foreign models with higher salaries are used for shooting. On conventional e-commerce platforms, there are cases where multiple stores share a set of pictures, and the cost of shooting each garment is extremely low. However, SHEIN has fallen into a situation where it relies on a large number of fast new releases to win, but the marginal cost of shooting remains high.

SHEIN releases a large number of new products every day, and it is difficult to reduce the cost of shooting

SHEIN releases a large number of new products every day, and it is difficult to reduce the cost of shootingIt is worth noting that due to the extreme compression of suppliers’ profits, many products have poor quality and a high return rate, which also increases SHEIN’s storage costs.

In terms of logistics, SHEIN is facing a more restrictive logistics policy. According to an international agreement, the cost of mailing small packages from China to the United States is much lower than that of other countries, and even the cost of domestic logistics in the United States is almost the same, and the United States does not impose import duties on goods worth less than $800. Similar regulations exist in many other countries. The extremely low cost of cross-border logistics is also an important factor for SHEIN to achieve the ultimate low price. However, in 2022, the United States will introduce a new bill. Once the bill is implemented, SHEIN will lose its tax-exempt status. Many Canadian consumers have said that shopping on SHEIN is often taxed, and the price advantage of SHEIN products after the tax increase is greatly reduced.

SHEIN’s advertising costs also continued to rise. In 2021, SHEIN’s revenue will be about 15.7 billion US dollars. Regarding the proportion of marketing, industry insiders generally speculate that it will be between 10% and 20%. As TikTok has become popular around the world, TikTok has gradually become one of SHEIN’s important advertising channels. According to VidIQ data, SHEIN’s participation rate on TikTok is 4%, which is much higher than the industry average of 1.45%. According to reports, SHEIN invests US$100,000 in advertising fees on TikTok every day. In addition to the content of the advertisement, bloggers’ evaluation videos are also invisible advertisements for SHEIN. However, with the maturity of TikTok Shop and Fanno, the overseas e-commerce companies of Douyin Group, TikTok is destined to be difficult to become a fertile field for SHEIN to grow.

The controversy over ESG also forced SHEIN to increase production costs. In the ESG criticism of SHEIN by overseas consumers, environmental pollution, clothing safety, labor protection and design plagiarism are still the most acute issues.

In the past two years, on foreign social media, more and more fashion bloggers and consumers have begun to promote sustainable clothing brands, that is, clothing mostly uses degradable or recyclable fabrics to reduce environmental burdens. However, fast fashion brands mostly use cheap polyester fabrics, which have a short lifespan and induce consumers to update their wardrobes quickly, resulting in a large amount of clothing waste that cannot be degraded quickly by nature. Therefore, they are frequently criticized by environmentalist consumers.

Posts criticizing SHEIN’s environmental protection and labor protection issues (translation is for reference only)

Posts criticizing SHEIN’s environmental protection and labor protection issues (translation is for reference only)Based on related disputes, well-known fast fashion brands have devoted certain resources and energy to respond and improve. For example, ZARA and Uniqlo are increasingly using biodegradable fabrics and energy-saving and emission-reducing manufacturing processes, as well as using more environmentally friendly paper packaging. Uniqlo’s in-store broadcasts will even specifically emphasize the brand’s achievements in environmental friendliness to improve user favorability.

However, SHEIN is still immature in terms of environmental protection and clothing safety. Not only are many of the clothes poor in quality and accused of being disposable, but they have also been exposed to multiple safety issues. In 2021, some of SHEIN’s children’s clothing was recalled for violating US federal flammability standards; children’s and pregnant women’s clothing accessories were also found to contain excessive lead in Canada and other countries.

After the Swiss Public Eye organization visited SHEIN’s foundry in Panyu, Guangzhou in 2021, it found that problems such as overtime work, fire hazards, and opaque carbon emissions still existed in the foundry. At the beginning of 2022, in the sustainability and social impact report released by SHEIN, it also admitted that among the nearly 700 audited suppliers, 83% of the suppliers had “significant risks”. However, SHEIN is committed to using more sustainable textiles in the future and disclosing its greenhouse gas emissions. Some suppliers also revealed that SHEIN has raised the threshold for suppliers this year, which will help reduce ESG-related disputes. But the selection of high-quality suppliers and sustainable fabrics is also destined to be accompanied by higher production costs.

Controversy over plagiarism is actually a common problem for fast fashion brands, but SHEIN is particularly prominent. “New Entropy” concluded that SHEIN’s clothing styles are mainly inspired by independent designers, original brands, designer websites and luxury brands, so copyright disputes continue. However, SHEIN has to maintain hundreds of thousands of SKUs on the shelves every year and keep up with the trend, so there is almost no solution to the problem of originality. And every step of increasing the original design requires a lot of design costs.

Several overseas designers accused SHEIN of plagiarizing their designs

Several overseas designers accused SHEIN of plagiarizing their designsA person in charge of a fast fashion brand foundry told “New Entropy”, “SHEIN actually earns money from the supply chain. If SHEIN really wants to solve ESG issues, it needs to be more complete with production standards, labor rights, and higher production processes. However, the production cost will rise sharply, and the selling price will approach the level of Zara and Uniqlo.” But in this way, SHEIN completely lost its low price advantage.

SHEIN’s next major task is undoubtedly to find a balance between costs, profit margins and improving ESG. At present, SHEIN is trying to achieve a balance by launching mid-to-high-end terminal brands and improving the e-commerce ecosystem.

Transformation and upgrading are imminent, strictly guard against new opponents

In the past two years, SHEIN has launched more than ten sub-brands, including young fast fashion ROMWE, high-end clothing MOTF, European and American fast fashion EMERYROSE, Korean clothing Dazy, sports fashion GLOWMODE, underwear brand Luvlette, makeup brand SHEGLAM, shoe brand CUCCOO, pet Brand PETSIN and many more.

Currently SHEIN official website has 11 sub-brands

Currently SHEIN official website has 11 sub-brandsAmong them, mid-to-high-end brands such as MOTF and Dazy have won the favor of consumers who have high requirements for clothing quality. Clothing with a higher premium is the best way for SHEIN to solve its weak profitability, and it can also attract high-consumption groups for SHEIN. Therefore, it is almost inevitable that SHEIN will gradually transform and upgrade in the future.

Although SHEIN has reached the critical point of transformation and upgrading, the influx of new cross-border forces has forced SHEIN to prepare for defense, including but not limited to Temu, TikTok Shopping, Fanno, IfYooou of the Douyin Group, Alibaba’s Allylikes, Lazada, Miravia and other cross-border e-commerce companies.

At present, Temu, which was just launched in September this year, poses the greatest threat to SHEIN, because Temu has continued Pinduoduo’s gene of focusing on sinking markets, relying on extremely low prices and the ultimate after-sales service such as allowing refunds and non-returns. quickly swept across the United States.

Today’s SHEIN is in a similar situation to Taobao ten years ago, that is, the foundation for moving to the mid-to-high-end market has been laid, but how to avoid sinking markets from being eaten by competitors while transforming and upgrading has become the biggest problem.

Taobao failed to defend the sinking market well, so that Pinduoduo rose rapidly in just a few years. But for SHEIN, in the battle to defend the sinking market of overseas e-commerce, it must not lose, because SHEIN itself is an independent station, does not invite merchants to settle in, and bears all risks by itself. Although SHEIN tested the platform model in Brazil this year and introduced independent merchants and brands, for SHEIN, which has been cultivating the supply chain for many years, the independent station is the best solution for cross-border sinking e-commerce that it has explored in the past, and it cannot be easily given up.

SHEIN started as an independent station, essentially because the brand does not have much meaning among low-priced and low-quality products. SHEIN cuts out the middleman and puts its own brand on the goods in the factory, so that it can eat all the profits and maintain the low price advantage. However, with the escalation of cross-border e-commerce involution, SHEIN also began to complain. The most obvious manifestation is that many suppliers said that SHEIN began to order suppliers not to cooperate with Temu. In the past, SHEIN did not interfere with the cooperation between suppliers and other platforms.

Temu is not an independent station, but an e-commerce platform, and merchants can apply to settle in by themselves. “New Entropy” understands that Temu merchants only need to upload their products and ship them, and there is no need to hire cross-border customer service, which is handled by the platform. Temu currently has 0 commissions and 0 deposits, allowing individual merchants to settle in, and the entry threshold is extremely low. Faced with Temu’s lazy store opening process and the temptation to master autonomy, many manufacturers have begun to tilt their balance towards Temu. If SHEIN continues to require merchants to “choose one of the two”, it may be disadvantageous to itself.

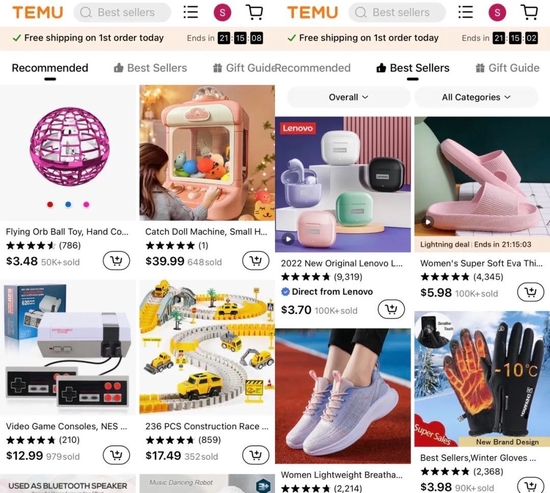

At present, the best-selling product categories on Temu are children’s clothing, toys and small commodities. Although Temu has not yet formed a direct competition with SHEIN, but as SHEIN is also making efforts in all categories, it is only a matter of time before the two become rivals. Therefore, SHEIN will definitely speed up its platformization in the future, introduce a large number of diversified merchants, and improve its competitiveness.

Best Selling Items on Temu

Best Selling Items on TemuAfter the price increase of SHEIN products, the mismatch is that the quality of the products has not improved, which makes consumers increasingly dissatisfied. Coinciding with the launch of Temu, consumers flowed to Temu. “Recently, I have been shopping at Temu. If SHEIN raises the price again, I will not buy it.” “If SHEIN does not offer free shipping, I will switch to Temu.” Many overseas consumers left similar words on social platforms.

Some consumers expressed that they began to switch to Temu

Some consumers expressed that they began to switch to TemuIn the face of Temu’s aggressive approach, SHEIN accelerated the pace of improving user stickiness before completing the platform transformation. There are three main ways to increase the stickiness of consumers in sinking markets: one is to fight price wars; the other is to promote membership benefits; the third is to improve the ecology.

For SHEIN, which urgently needs to increase profit margins, there is not much room for maneuver in direct price wars, not to mention that some suppliers of Tume used to be suppliers of SHEIN, and blind price wars are very detrimental to SHEIN. The benefits of membership and the improvement of the ecology may, while ensuring profit margins, give consumers the illusion of discounts and prompt them to consume frequently.

In the past, in order to increase user stickiness, Taobao launched a membership product called “family bucket discount benefits”, namely 88VIP. As of June 2022, the number of 88VIP members has reached 25 million, and the per capita annual consumption has reached 57,000 yuan. It can be seen that membership discounts have a stimulating effect on user stickiness and customer unit price.

And SHEIN recently launched a membership product “SHEIN CLUB” in the United States, which is undoubtedly similar to 88VIP. But just a membership system is far from enough to fight against Temu. After all, Pinduoduo is also very good at increasing user stickiness with membership system. Temu needs to create a moat with absolute advantages in the sinking market, that is, like 88VIP, it is difficult for opponents to recover. engraved consumption ecology.

SHEIN recently launched the second-hand trading platform SHEIN exchange in the United States, which can be regarded as the first step in building a consumer ecology. The role of this platform to SHEIN is like that of Xianyu to Taobao. When consumers have psychological expectations about the whereabouts of unsatisfactory products, they can reversely promote consumption. The second is to conform to the consumption habits of Americans, because many Americans will send unwanted clothes to offline second-hand stores, and there is a basis for second-hand transactions. By the way, SHEIN exchange can also reduce some environmental disputes for SHEIN, killing three birds with one stone.

In addition, SHEIN has also opened pop-up stores in overseas cities such as Barcelona and Osaka this year. Some Japanese consumers told “New Entropy” that SHEIN’s pop-up store cannot directly buy products. If you want to buy after trying them on, you can scan the code and place an order online. SHEIN’s pop-up store has undoubtedly played a role in advertising, awakening consumption, strengthening brand image, and further improving the consumption ecology.

SHEIN pop-up stores in Osaka and Barcelona

SHEIN pop-up stores in Osaka and BarcelonaHowever, with the saturation of the cross-border e-commerce market, a more difficult situation has emerged before everyone’s eyes, that is, in the confrontation between multiple giants, various costs of cross-border e-commerce have been raised.

SHEIN will also “open source and reduce expenditure”

Many giants are fighting fiercely in the red ocean of cross-border e-commerce. The final result is bound to be an endless “arms race” of suppliers’ voice and bargaining power, advertising and discounts.

At the beginning of its launch in September, Temu’s advertising budget reached 1 billion yuan, while SHEIN’s monthly marketing expenses are now around 1 billion yuan. The advertising channels of the two are also highly overlapping, mainly search engines and social media. As the user bases of the two become more and more overlapping, the investment in marketing between the two will inevitably continue to rise. However, preferential competition and low-price competition test their respective cash-burning capabilities and supply chain price-lowering capabilities. Under multiple pressures, SHEIN had to seek to increase revenue and reduce expenditure.

SHEIN’s “open source” means that it needs to open up more markets and win more consumers. The “New Entropy” inventory found that among the 224 countries and regions in the world, SHEIN has been launched in 174 countries and regions. A billion Chinese and Indian SHEINs are not doing business.

It’s not that SHEIN has never been launched in India, but was blocked and taken off the shelves by the Indian government in 2020. Looking at the world, China is almost the only market that SHEIN can develop.

As for why SHEIN is not launched in China, the reason is obvious, because SHEIN is like a fish in water in cross-border e-commerce, and it earns money from “poor resources” and “poor information”, but in China, it no longer has such poor resources. What’s more, many suppliers of SHEIN will clear their inventory through domestic e-commerce platforms, resulting in many SHEIN products of the same origin and same style on e-commerce platforms such as Alibaba and Pinduoduo. In the domestic fast fashion consumer market, Uniqlo, Zara, and UR are very mature, and SHEIN does not have quality and design advantages, so SHEIN did not have the conditions to land in China in the past.

However, as SHEIN reveals the trend of high-end and platformization, it has the foundation to go online in the Chinese market. The emergence of Dazy, a sub-brand in line with the aesthetics of Asian women, also paved the way for SHEIN to enter the Chinese market. It can be predicted that if SHEIN enters the domestic market, it will also focus on mid-to-high-end terminal brands with higher prices and better quality, such as Dazy, MOTF, and GLOWMODE. Even if it is difficult for SHEIN to reach the popularity abroad in the Chinese market, it will still help its sales growth.

Dazy, MOTF, GLOWMODE products have higher prices and better quality

Dazy, MOTF, GLOWMODE products have higher prices and better qualityIn terms of “throttling”, SHEIN’s main action is to expand the supply chain in domestic provinces and overseas countries where labor costs are cheaper. In the past, SHEIN’s suppliers were mostly concentrated in Guangdong, Jiangsu, Zhejiang and other places with developed industrial belts. However, as giants such as Pinduoduo and Douyin Group also take root in these places, the production capacity and cost performance of the supply chain will not be as good as before.

At present, SHEIN has gradually opened up supply chains in Fujian, Shandong, Hubei, Jiangxi and other provinces, and no longer relies on a single production area; secondly, SHEIN has also begun to prepare for the construction of supply chains in overseas countries. It is reported that SHEIN has signed contracts with two factories in Brazil non-disclosure agreement. Some people in the industry also said that if other domestic giants raise the cost of the supply chain, SHEIN may also develop supply chains in Southeast Asian countries where the fast fashion foundry industry is also developed.

With the popularity of SHEIN all over the world, the business of cross-border e-commerce and independent websites has entered a critical juncture, and basically every pixel that may have business opportunities has been filled by one party. When SHEIN launched the brand matrix, Temu also launched a brand strategy, planning to create 100 overseas brands; when SHEIN moved towards mid-to-high-end, Alibaba also launched a mid-to-high-end e-commerce platform Miravia to compete. Cider, Revolve, Fashion Nova, Boohoo and other independent e-commerce sites at home and abroad have also identified their respective subdivision positioning, captured a loyal customer base, and are looking forward to growing into the next SHEIN.

For SHEIN, which was the first to eat the “crab”, the first half of cross-border e-commerce is a tailwind, sailing recklessly, and returning with a full load; the second half is a headwind. It is difficult to continue the myth of growth, and in the process of platformization and mid-to-high-end transformation, SHEIN needs to continue to cut through the wind and waves.

This article is reproduced from: https://finance.sina.com.cn/tech/csj/2022-12-06/doc-imqmmthc7259101.shtml

This site is only for collection, and the copyright belongs to the original author.