The “Black Question Mark Face” series has another major update today, and to be honest, the protagonist is a player who could have imagined but never thought of it before. It is a bit unclear whether it is a record or a long time to see .

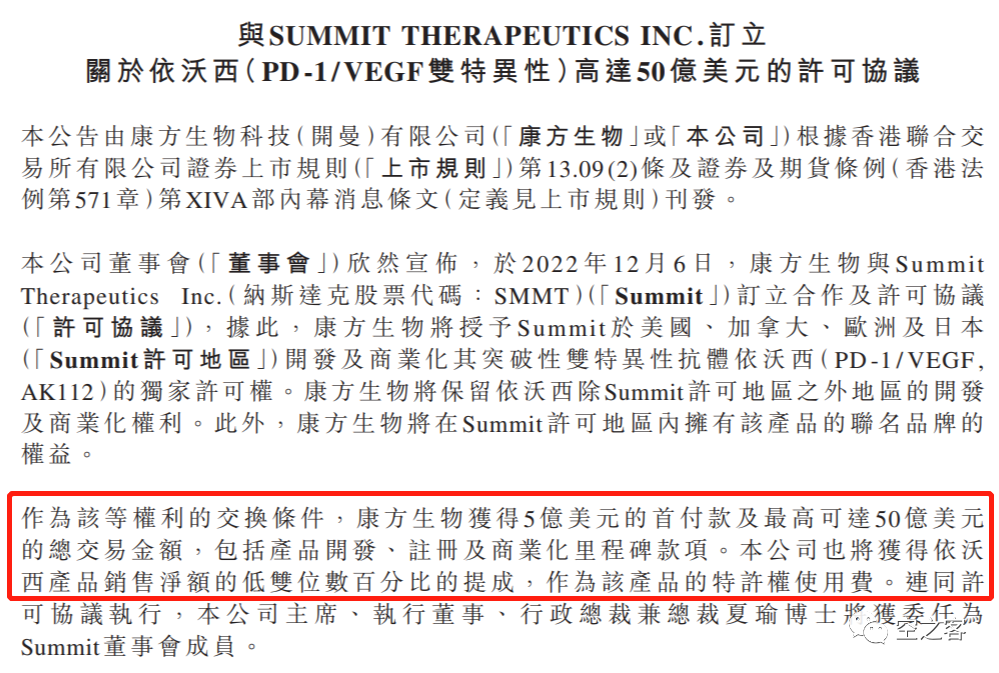

On December 6, $Akeso Bio-B(09926)$ announced that it signed an agreement with Summit Therapeutics to grant the other party’s PD-1/VEGF double antibody product AK112 North America, Europe, and Japan rights, and the consideration reached a jaw-dropping $500m upfront + up to $5b milestone payment + low-double-digit royalty . There is no doubt that this has definitely created a new record for overseas authorization of Chinese pharmaceutical companies. Whether it is the down payment or the total amount, it has taken all the previous Baekje TIGIT, Rongchang HER2 ADC, and the legendary BCMA CAR-T on the beach.

You have to stand upright when you are beaten, and I have little knowledge. I have never really recognized the marginal benefit of double antibodies over one of the two monoclonal antibodies or the combination. There will be such big news that shocks the past and the present. Therefore, it is necessary to review the protagonist of the story and improve the posture level again.

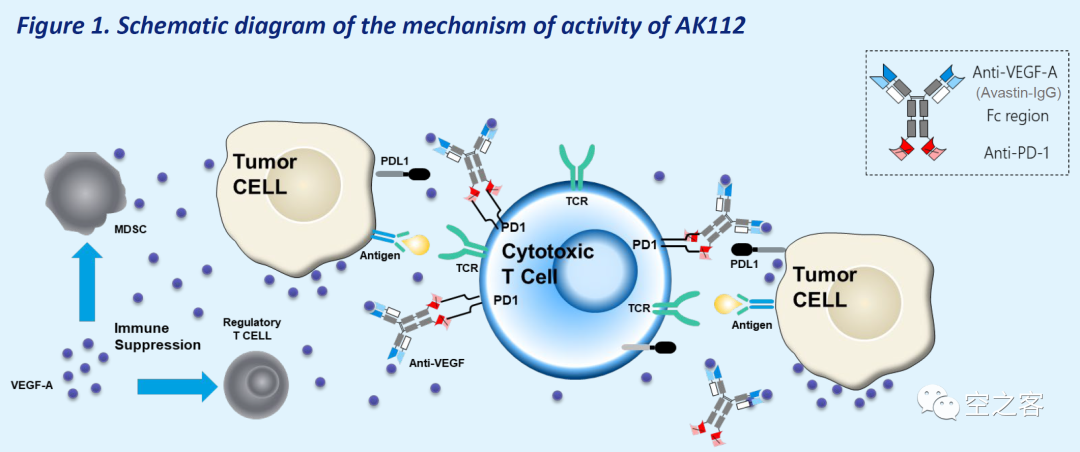

AK112 uses the anti-VEGF bevacizumab as the backbone, and connects the PD-1 antibody in the form of scfv at the C-terminus. VEGF can block immunosuppression, stimulate tumor angiogenesis, and promote T cell infiltration in tumor tissue, thereby improving the antitumor efficacy.

At present, AK112 has entered the third phase of clinical trials for non-small cell lung cancer, including the first-line therapy of single-drug head-to-head challenge K drug and the second-line therapy of EGFR TKI resistance combined with chemotherapy, and has the blessing of breakthrough therapy. Head-to-head K drugs to prove “2>1”, this is the touchstone of much attention, not only for AK112 itself, but also trying to lay the foundation for the entire dual-antibody mechanism. It must be admitted that this courage and execution are commendable .

We can look at the clinical data that has been published before, and how much support can be provided for this long-awaited goal. At this year’s ASCO, Kangfang announced the early data of single drug and combined chemotherapy in the treatment of NSCLC.

1) Monotherapy for 1/2L NSCLC (NCT04900363)

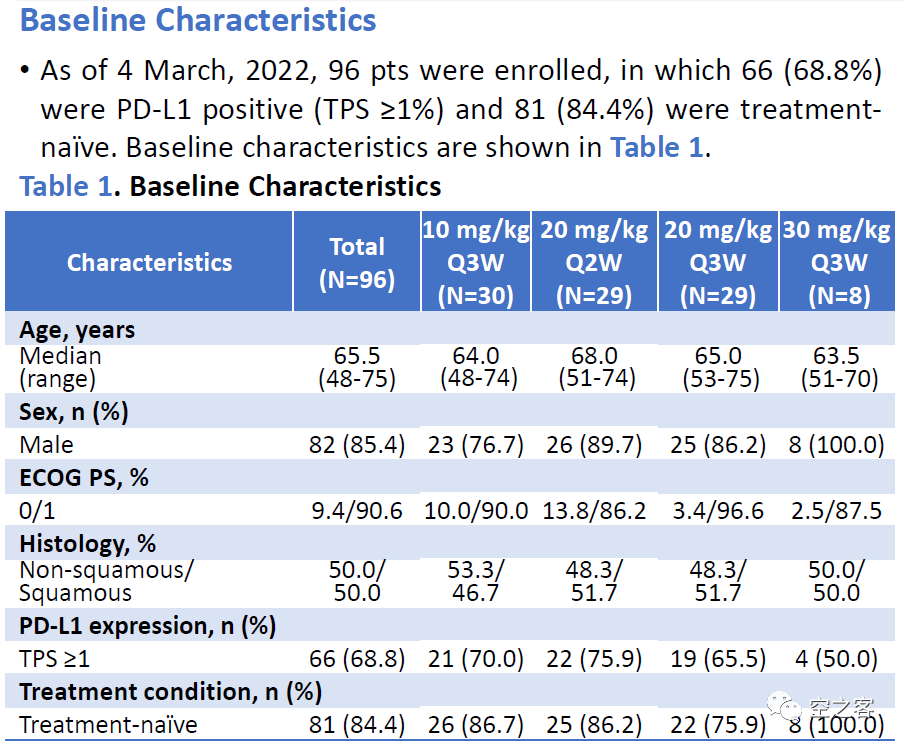

A total of 96 patients with advanced NSCLC were enrolled in the trial, of which 68.8% were PD-L1 positive and 84.4% were treatment-naive, and were assigned to four dose groups 10mpk Q3W, 20mpk Q2W, 20mpk Q3W and 30mpk Q3W.

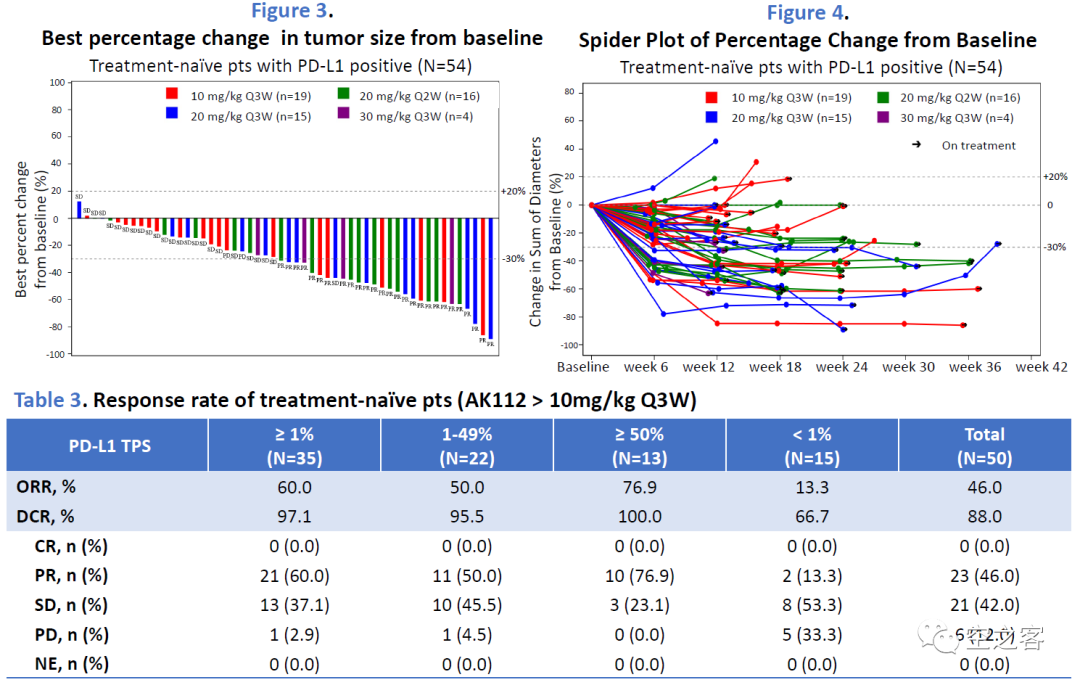

In terms of effectiveness: Among 90 evaluable patients, the ORRs of the four dose groups were 21%/50%/38%/50%, and the DCRs were 93%/92%/90%/83% respectively; Among PD-L1 positive patients, the ORR and DCR of the four dose groups were 32%/63%/53%/75% and 95%/100%/93%/100% respectively; Among the treated patients, the ORR was 46%, and the DCR was 88%. In contrast, in the single-drug first-line NSCLC phase III clinical study KN-042 of K drug, the ORR of PD-L1 positive patients was more than 36%. On paper, AK112 may indeed have the power to fight the first battle, but after all, the three Long-term OS and PFS are king .

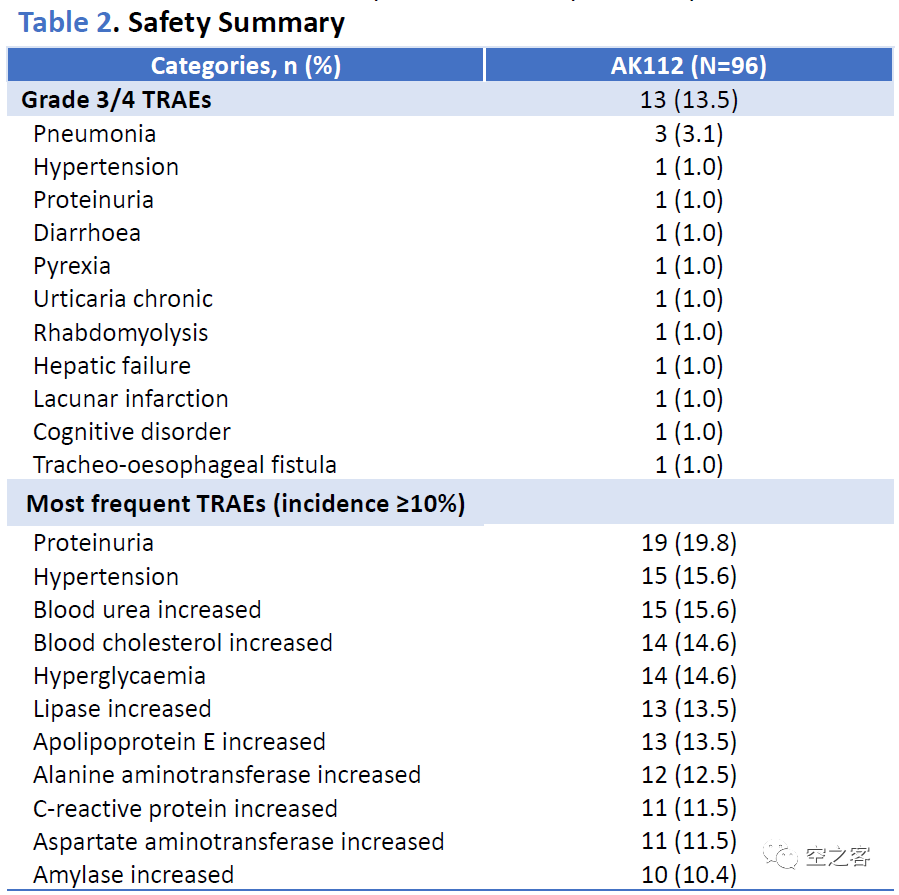

In terms of safety: the incidence of TRAE was 88.5%, of which grade 3/4 was 13.5%, and there was no drug withdrawal due to TRAE, which was still within the acceptable range initially, and there was no significant toxicity superposition of the two arms.

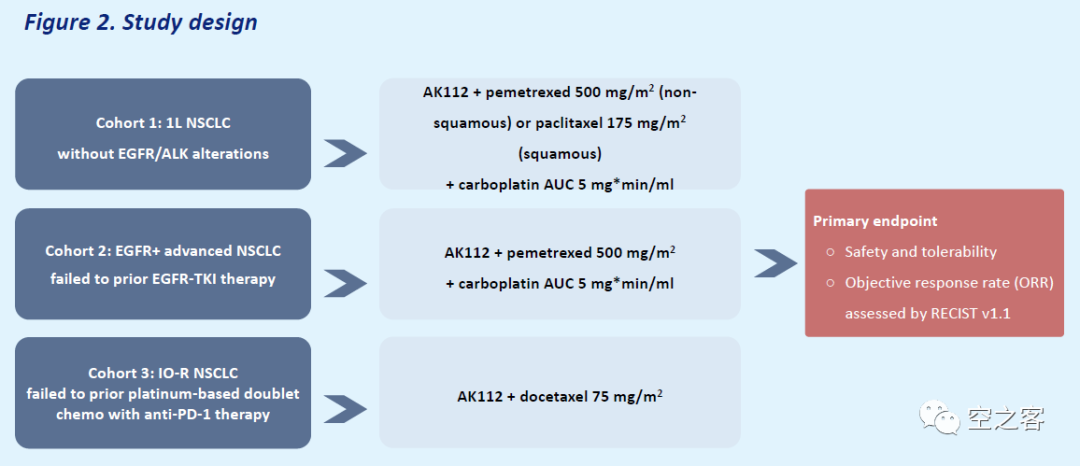

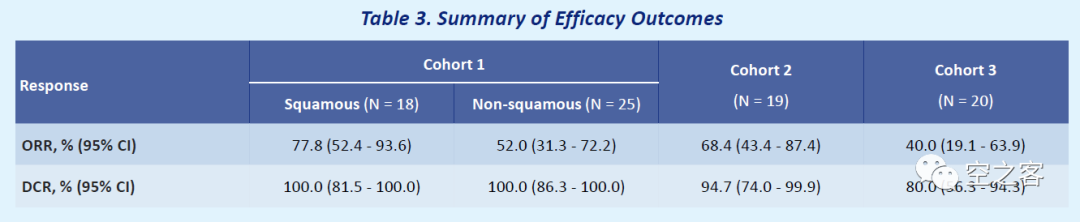

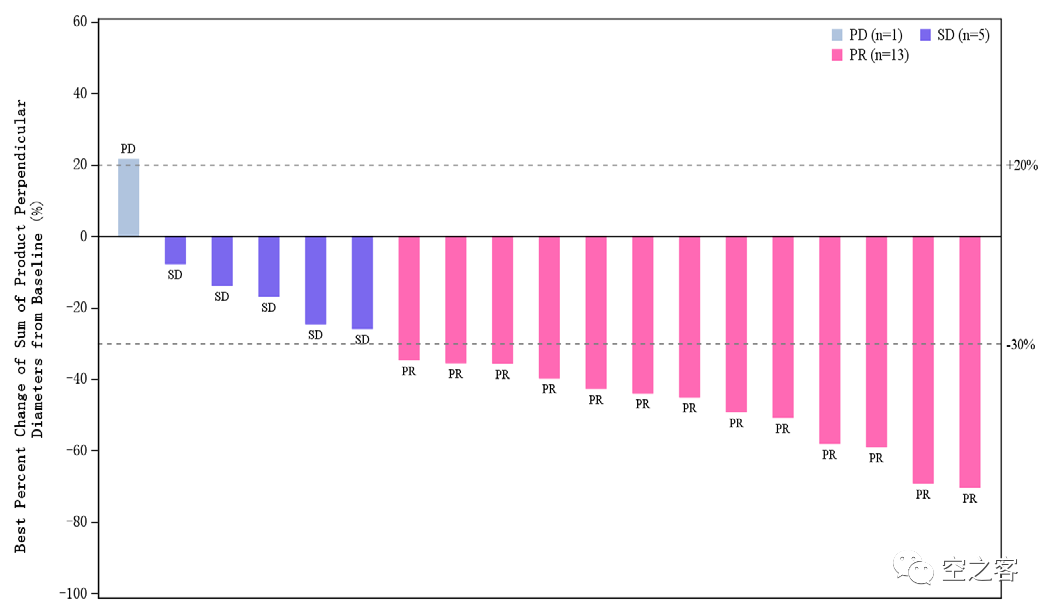

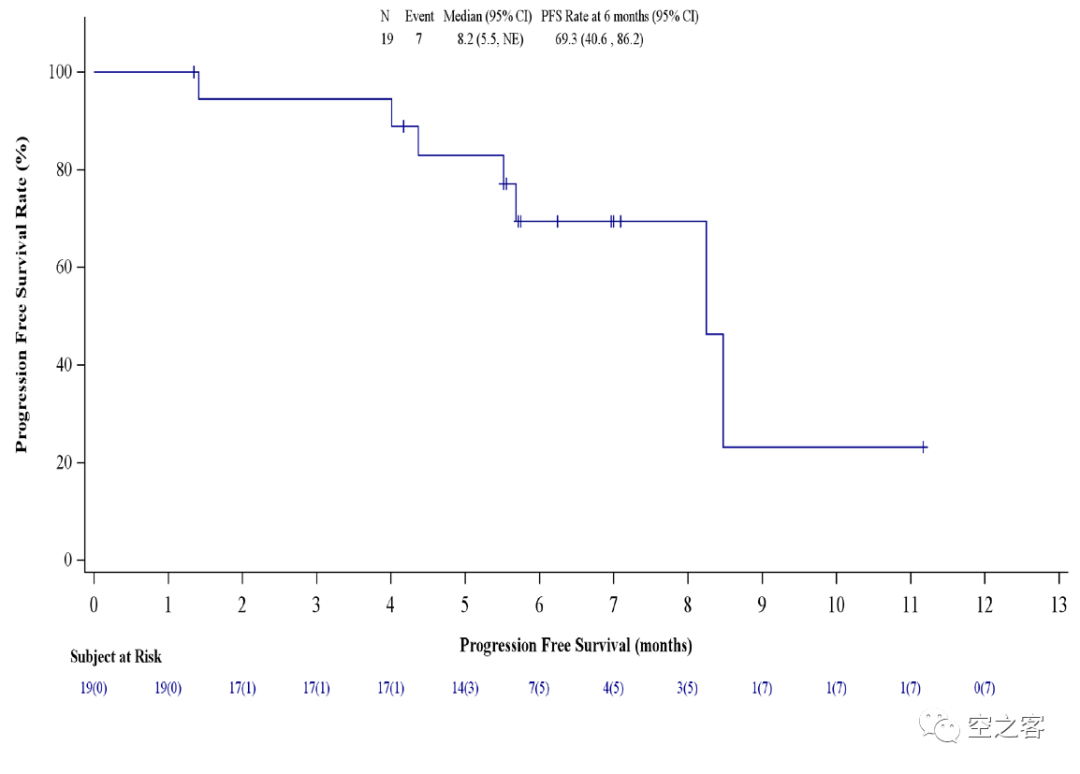

2) Combined chemotherapy for NSCLC (NCT04736823)

A total of 83 NSCLC patients were enrolled in the trial, divided into three Cohort, 1L EGFR/ALK wild-type patients, EGFR-TKI-resistant advanced patients, and PD-(L)1 plus platinum-based treatment progression patients.

The effectiveness of the three Cohorts is quite interesting. Among them, the ORR of EGFR-TKI resistant patients was 68.4%, the DCR was 94.7%, the PFS was 8.2 months , and the 6-month PFS rate was 69.3%.

In parallel, these early data can be said to be remarkable, and the practice of daring to fight head-to-head against K medicine is quite admirable. Coupled with Kangfang’s consistent pragmatism and high-execution personality design, people still have doubts about this Shuangkang has considerable goodwill and expectations . The above is what I said at the beginning of the article, AK112 as the protagonist of today’s story makes me ” want “.

The following is the ” unexpected ” plot.

The object of external authorization is of course MNC as the first choice, followed by Biotech with strong industrialization capabilities. Taking a step back, it must be a partner who can assist in development and sales. Let’s take a look at the authorization selected by Akeso today. Which side does Fang Summit stick to?

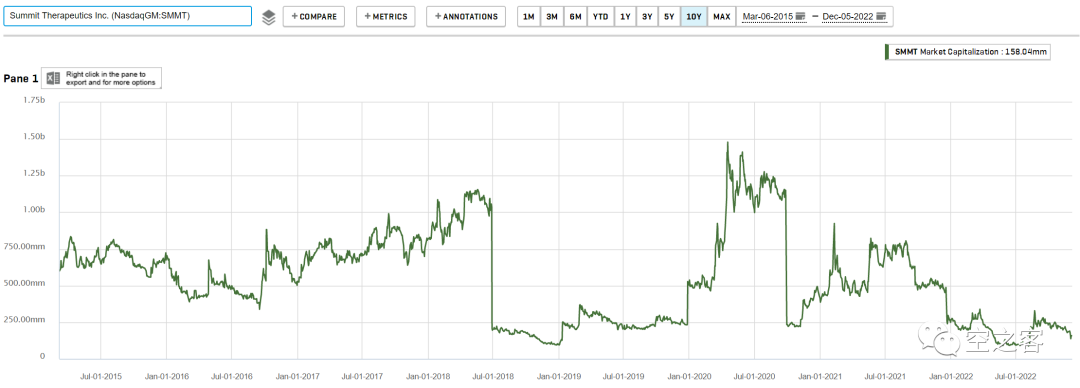

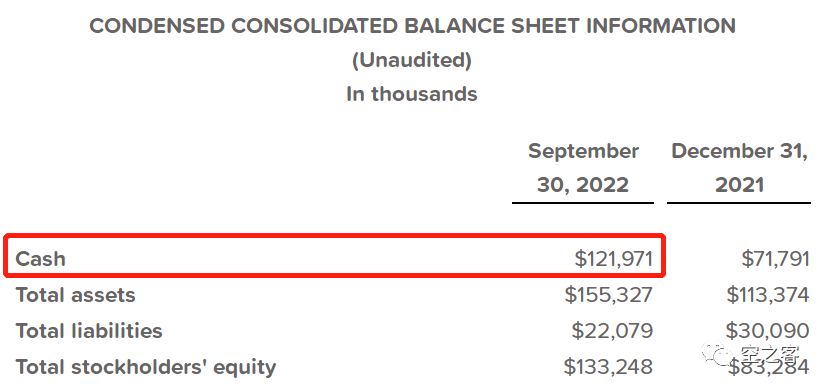

This is a small pharmaceutical company that once developed antibiotics and then failed. Its current market value has fallen to about 150 million US dollars (the top of the shareholder list is also buried with big names such as Vanguard, BlackRock, MS, GS, etc.), the latest financial report The cash balance is $120 million.

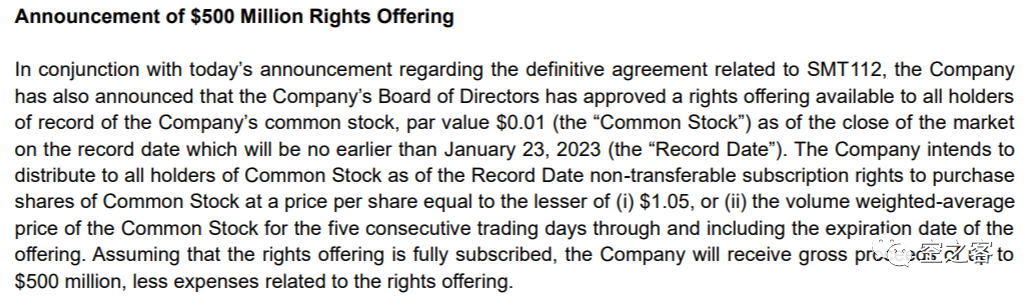

Looking at Summit’s announcement, while introducing this product, the two co-CEOs, Robert Duggan and Maky Zanganeh, first borrowed $520m from the company (how else would they pay the down payment), and then the company issued an additional $500m .

These two names are no strangers. They are the former CEO and COO of Pharmacyclics , and they are also the main promoters of the super-blockbuster Ibrutinib and the sale transaction. It is really not a big deal to spend 500 million.

So the question is, what kind of help can Summit provide to Akeso? Development, sales, money, bigwigs, or whatever. . . ? (I didn’t say anything, I didn’t know anything)

Let’s not engage in the theory of killing people’s minds. Product highlights are one thing, and transaction value is another. One yardstick equals one yardstick. I can only say: This product and the mechanism behind it are at least worth looking forward to; at least I don’t understand the transaction and the motivation behind it .

$Baekje (BGNE)$ $Innovent (01801)$

There are 43 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/1335311504/237215761

This site is only for collection, and the copyright belongs to the original author.