The huge changes in the industry environment, and even the consumption and investment environment of the entire country are currently the biggest impact on several leading companies of new forces.

Xiaopeng: The “sense of technology” brought by autonomous driving technology has entered a period of fatigue, and the expansion of production of intelligent mid-range models has been hindered, and the huge losses are incomprehensible.

My perception of Xiaopeng can be said to be repeatedly reversed between the two extremes.

After experiencing the Xpeng G3, I don’t want to experience Xpeng’s car again. There are problems in the design and manufacturing of the entire model, and the design and development mode of Xpeng that many supply chain personnel related to Xpeng are also disgusting.

But Xiaopeng P7 completely subverted my perception. P7 is like a new species for Xiaopeng models. After I tested the P7 at the test track, I was basically disgusted to amazed. This is the electric car I am most satisfied with in terms of handling and chassis response among self-made electric cars.

Later, I learned that the general person in charge of the development of Xiaopeng P7 is Dr. Xu, who originally came from Weilai’s US headquarters, and he was originally an expert and executive of automobile development in Ford North America.

Including from a technical point of view, the adaptability of Xiaopeng’s automatic parking algorithm to the characteristics of parking spaces under the conditions of the Chinese market at that time was basically the best in China. Of course, the technology of other domestic companies has also come up.

After my test drive, I recommended Xpeng P7 to at least 5 friends who asked me what model to recommend as long as they only made domestic electric vehicles, and all of them finally bought P7.

However, the achievements of Xiaopeng P7 have not been inherited. Xiaopeng’s entire G series models have always been relatively bad (my personal experience), and the logic of the P5 model is correct. The main slots in the market are all concentrated in the shape. Many car owners who pay attention to P5 first prefer P7, and then find that the functions of P5 are similar and the actual interior space of the car is not much smaller than that of P7. Considering the price, they choose P5.

At the same time, Xiaopeng spent too much money, especially the high sales and management fees that are incomprehensible.

Xiaopeng Motors has a cumulative loss of 4.402 billion yuan in the first half of 2022, which is comparable to Weilai’s -4.57 billion loss. In the third quarter, the cumulative loss of Xiaopeng Automobile expanded to 6.778 billion yuan, with an average loss of 2.06 billion yuan per quarter.

Further digging into the financial data, we found that Xiaopeng’s biggest problem is the high sales and management fees.

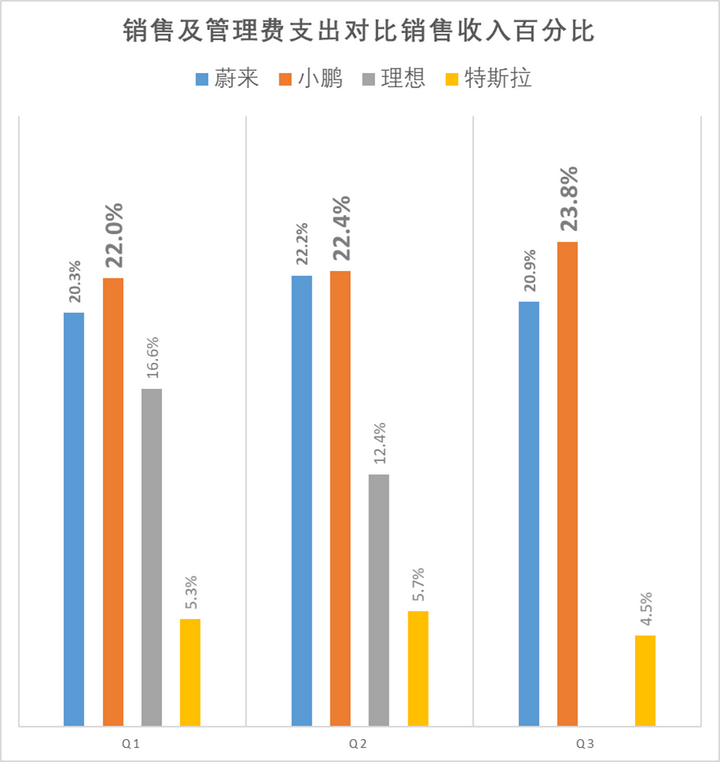

Xiaopeng’s sales and management fees were as high as 22% in the first half of this year, and even as high as 24% in the third quarter. This proportion is even higher than that of NIO, which has high sales and service specifications as a gimmick. The sales and management fees of Weilai Automobile account for only 20%-22%. In contrast, Li Auto’s sales and management fee ratio is around 15%, while Tesla’s is only around 5%.

Xiaopeng’s gross profit in the first three quarters was only 2.643 billion, and the R&D expenses in each quarter were about 1.2-1.4 billion. The R&D expenses in the three quarters were 3.985 billion, which is quite satisfactory, but the sales and management expenses reached 4.932 billion, which is too exaggerated. , especially considering that such a large investment in sales channels only supported the main business income of 21.715 billion. In contrast, Ideal Auto’s main business income of 18.295 billion only spent half of Xiaopeng’s sales and management fees (2.578 billion). If it is Tesla’s efficiency, it only needs a little over 1 billion to achieve a main business income of 20 billion+.

So it is hard for you to imagine that Xiaopeng, whose average price is not high, can spend more money in sales channels than Weilai Auto, and the gross profit of the model is similar to that of Weilai.

Behind this may be the problem of Xiaopeng’s current direct sales + authorized dealer model.

The financial report of Q3 has not yet shown the recent sales decline. It is conceivable that the financial report of Q4 is expected to be even more messy, because the total amount of many fixed investment is basically unchanged, and the sales volume is less, and the expenditure allocated to bicycles will be more. Profit return is more distant.

To sum up, Xiaopeng’s development problems are as follows:

- Excessively overestimating the continuous improvement of the customer attraction of intelligence to its own products, and the continuous loss of enterprises, forced Xiaopeng to try to increase the premium on G9, hoping to solve the problem by increasing gross profit. As a result, the pricing and positioning confusion caused by the listing of G9 The media stomps. Due to the narrow positioning of Xiaopeng’s models and the failure of G series models one after another, it is hopeless to increase the gross profit in the short term, and the gross profit rate has even narrowed further due to the decline in sales.

- Xiaopeng’s direct sales + authorized dealer model has too high investment in sales channels and management and operating costs, which is the biggest problem in Xiaopeng’s financial report at present, and the company is running wildly amidst continuous blood loss.

- At present, Xiaopeng’s liquidity situation is still good, which is the confidence for Xiaopeng Motors to make subsequent adjustments. The debt ratio in the Q3 financial report is 45.06%, and the total amount of cash and short-term investments that can be quickly realized is 31.986 billion yuan. The financial status is still relatively good. status.

- However, it should be noted that Xiaopeng models are currently facing the greatest competition challenges. The 200,000+ models have already been attacked by existing models such as Tesla, BYD and even Jikrypton, and will even face mature manufacturers directly in the future. The challenge of electric vehicles. In terms of intelligence and automatic driving of Xiaopeng Motors, the former has not shown a leading technical solution in the context of the current electronic architecture upgrade, while the latter is about autonomous driving. On the one hand, the actual utilization rate of NGP is not as expected. So high, according to the data released by Xiaopeng on the National Day in 2022, the mileage of Xiaopeng Expressway NGP during the National Day only accounted for 1.4% of the cumulative mileage; The brand premium brought by it must not be overestimated. As more and more car companies adopt L2+ assisted driving as standard equipment, and at the same time continue to increase gross profit by controlling manufacturing costs, Xiaopeng Motors, which has been criticized as a manufacturing cost and has high sales expenses, will reverse in the future. The challenge of the situation will be the biggest one.

According to the current state, Xiaopeng’s crisis is expected to not really affect the company until the end of 2023, and the management still has a year to go.

NIO: The biggest risk is that under the background of economic depression in the future, investors’ challenges to NIO’s business model may lead to the outbreak of internal problems.

Weilai’s problems are more serious than Xiaopeng’s.

Xiaopeng’s problems, Weilai has, but Weilai’s Q3 financial report performance is even worse. The cumulative loss of net profit in the first half of the year was comparable to that of Xiaopeng, which was RMB 4.57 billion (Xiaopeng lost RMB 4.4 billion). In the third quarter, it lost RMB 4.142 billion in one quarter, which made the accumulated loss of net profit in the first three quarters reach an astonishing amount. 8.712 billion yuan.

According to this rhythm, it is not a dream to reach a loss of 13 billion yuan for the whole year in 2022.

At present, the debt ratio of Weilai Automobile has reached 66.08%. This is of course different from the debt ratio of Weilai when the debt ratio exceeded 100% when Weilai was the most difficult, but this cannot be called healthy.

More importantly, Weilai may have concealed its actual more serious losses and liabilities through the financial report number game.

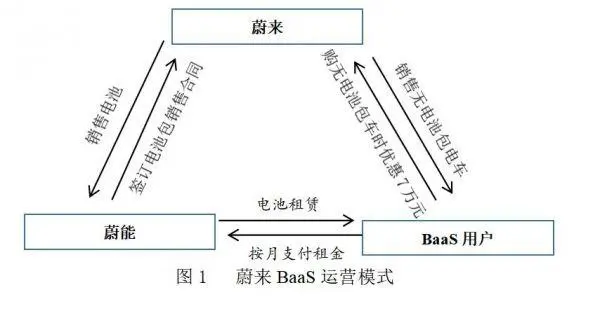

In the middle of this year, the Grizzlies issued a short-selling report, which was subsequently refuted by Weilai, which brought short-term fluctuations to Weilai’s stock in the middle of the year, but the stock price rebounded later. However, the financial report analysis in the Grizzly report directly pointed out one of Weilai’s core models: the huge financial game loopholes that may exist in the battery swap model.

Weilai’s battery replacement model supports the development of its BaaS (Battery as a Service) model, and plays a role in reducing the first-time purchase price of new car owners. For example, the price of ET5 before the subsidy is 328,000 yuan, but the price before the subsidy of the BaaS scheme is reduced to 258,000 yuan, and then the car owner will rent the battery at a monthly fee of 980 yuan.

So logically speaking, Weilai’s business income in the month of sales should be the actual income after deducting taxes and other sales of 258,000 yuan, and then included in the income of 980 yuan per month in the subsequent financial report. Then the income corresponding to 258,000 yuan, after deducting the actual various costs of the whole vehicle of 328,000 yuan, is the gross profit of this car.

However, in fact, Weilai first sold the battery to a company named Wuhan Weineng, so in fact Weilai’s BaaS users signed a battery lease contract with Wuhan Weineng. Although Weilai Automobile only received 258,000 yuan for the car without the battery pack version from the user, it also received a one-time purchase contract for the complete battery pack from Wuhan Wei Neng.

Therefore, in the financial report of Weilai Automobile, the model of the BaaS solution is still included in the business income of the current month with the income corresponding to the complete model with a price close to 328,000 yuan, and the gross profit is calculated based on this. And Wuhan Weineng, which needs 6 years to offset the principal investment by collecting rent, may have incurred huge losses that have not been included in Weilai Automobile’s financial report!

It is not known whether this operation is also used in other backup batteries in the power exchange business.

Considering what we mentioned above, NIO’s own financial report this year’s annual loss may reach a record 13 billion yuan, so is there a bigger reason behind the “financial game” mentioned in the Grizzlies short report? We don’t know the loss black hole.

The bigger problem is that under the background of new technology and market, the value of battery replacement mode is constantly weakening:

- The battery replacement mode requires an independent battery pack structure, which conflicts with CTB or CTC technology and prevents NIO from reducing battery costs ;

- The cost of battery cells continues to rise. Due to the further deterioration of key elements such as lithium, which are relatively scarce, due to the further deterioration of geopolitics and international situation, the cost reduction of batteries is difficult to achieve. And as more and more power stations are replaced, the larger the flow battery reserve is required, and the debt-like losses will be more serious;

- The most serious problem is that the market has run out of money. If the financial report game can be used in the past to beautify the financial report and continue to support the money-burning activities through stocks and financing, but if there is no audience, is the performance still meaningful?

- The eternal risk of changing the power station: It only takes one vicious explosion accident of the power changing station, which may lead to the comprehensive supervision of the power changing station in the whole country! Note: There has already been a fire incident at the power station this year, but because this incident is another electric vehicle, the energy density and size of the battery itself are relatively low, so the fire was quickly extinguished.

There is also a fatal pitfall. While positioning ET7 and ET5 too high, the management refused to make Alps bigger, and missed the opportunity of high-end driving mid-range models to achieve net profit. Unless Weilai gets another 20 billion in financing, it has lost the opportunity to build a mid-range brand.

The ET series, which appeared in the planning as early as 2018, kept skipping tickets and constantly deviated from the original planning path. In the end, ET7 became a luxury model that rivals the BMW 7 Series.

In my January 2021 article I wrote:

“a. The cost of materials cannot be diluted due to too late, and the cost of basic hardware is too high; b. The cost is more abnormal due to too large; The batches are piled up with mobile eyes 4 chips that are useless at all (only the chip adds 1000RMB to the material cost). Again, ES8 had imported model X and FF91 from LeTV back then to endorse the rationality of its own price, ET7 What’s there? No wonder the imported BMW 7 Series is used as a benchmark.” – JackyQ article, January 2021.

Alps (Alps) is the product of a compromise that NIO’s investors forced NIO’s management to make. On the one hand, NIO did recruit a lot of actual R&D personnel for Alps, but on the other hand, the core management obviously didn’t have Alps. matter. Now what is the third brand Himalaya going to do?

ALPS is too slow. The current estimated time to market is the second half of 2024. The cooperation agreement with Hefei was only signed in May this year. From a manufacturing perspective, it is impossible to advance. With Weilai’s financial report losses so severe, the progress of ALPS will only be continuously delayed.

Personally, I think that for Li Bin, he personally doesn’t like the idea of establishing a second and third brand including ALPS, but there must be some second and third brands in NIO’s management who want to develop real volume. The actual controller and group of the brand. Because using the high-end appeal of NIO, an existing brand, to convert it into sales and make money as soon as possible is a problem that Weilai Group needs to face directly.

Weilai is still losing blood, and cash flow is constantly being diluted. The US stock market is affected by the economic environment and the development environment of the US stock market. It can no longer provide Weilai with more room for imagination, and the future may even be negative. . Whether the construction of the second and third brands represented by ALPS is honey or poison for NIO, and whether it will become a tool for internal business philosophy conflicts for NIO’s management, in fact, needs to be closely watched .

One problem that Weilai’s current hardware platform does not solve is that the cost of conventional materials is too high. NIO is currently relying on its own service system, high-end brand image and the advance layout of some typical new technologies to support a relatively high selling price, and then only when the sales volume exceeds a certain amount can the gross profit become positive.

According to the previous calculation results in 2020, the dividing line for Weilai’s gross profit to become positive is that the quarterly sales volume exceeds 8,800 vehicles, and the net profit should exceed 26,000-30,000 units. Due to the rapid development of Weilai’s sales in recent years, the dividing line of gross profit has already broken through, but it is still far away from the positive net profit. The reason behind this is actually that the cost sharing effect brought about by the increase in quantity has long since disappeared, and the gross profit Can’t go up.

ALPS once considered the development of a cost-effective new platform, but in the end due to the limited resources allocated, it will still be modified from the existing platform, so the cost reduction and profit expectations for ALPS can be said to be basically empty. ALPS has become a tasteless.

Weilai will fall into crisis earlier than Xiaopeng. According to the current development trend, it is expected to deteriorate significantly after September 2023. The bigger challenge lies within Weilai.

As for what Weilai wants to make batteries, chips, etc., it is recommended to wash and sleep. Still the same sentence: The industries mentioned above must have a super-large-scale effect to achieve cost reduction, and it is clear that they are used to brush traffic and act. But the economic forecast for 2023 is so bad that all the theatergoers will run away, so why are those who just yell and sing? Quickly find a class to make money is the kingly way.

Ideal: The financial situation is the most stable. The main challenge is the low technical threshold. It is expected to encounter real difficulties after the first half of 2024, and the management still has about one and a half years.

Compared with Xiaopeng and Weilai who lose 2-4 billion yuan in a quarter at every turn, ideally a quarterly net profit loss of 600 million yuan is considered a bad sale, and even a loss of only 10 million yuan in the first quarter of 2022. Considering the investment situation of the ideal new investment model, this figure is actually very good.

The ideal debt ratio and cash flow are also the best. The debt ratio in the second quarter was only 41.16% (the financial report for the third quarter was not released when I wrote this), and the total cash and short-term investment in the second quarter reached 50.442 billion.

The ideal problem is that the product field is single and the technical threshold is low. Compared with Xiaopeng, which can be called a technology-oriented enterprise, Ideal is more like a product manager-oriented enterprise.

Compared with Weilai and Xiaopeng, the ideal vehicle is typically the ideal one, and the best state is the static evaluation. After driving, the state is actually still a certain distance from the two companies, and it is actually not as good as the extended range. Lots of mature players on this line, especially NVH control of feeds. But it is really “a big cover-up”, which has no reason at all.

Of course, this year’s good brother of Ideal, a partner like a crouching dragon and a phoenix, the birth and hot sale of Wenjie further refreshed our new understanding of the thinking of customers in the Chinese market. In comparison, Ideal has also become cute. After all, Ideal The most is to whitewash peace with indiscriminate use of vocabulary. 90% of Wenjie’s product power is supported by one person’s bragging. “Premium customers” who place orders.

However, in the field of 7-seat large MPV, whether it is plug-in or range-extending, there are also hybrids, including car-machine interaction that is more Chinese and closer to customers. At present, from mature car companies to various independent companies There are also start-ups, all of which are being done, and the ideal one must be listed on the benchmarking PPT: this can also succeed.

At present, in terms of the progress of major car companies, it will basically take shape by the end of 2023, and the first half of 2024 will be a dumpling-like car.

Of course, the ideal is not without action. First of all, I think it is really unnecessary to start rolling pure electricity now. There is no difference between playing pure electricity and burning money directly. At present, the market trend of pure electric solutions for start-up brands is extremely pathological. It is impossible for you to make money. You are just playing stocks and piled up costs. You can’t survive a large-scale manufacturing like Tesla with a large number of sales and cost sharing. stage. Weimar, whose management team was born in the supply chain, will be beaten to death by this group of competitors who don’t speak martial arts. In 2022, it is the most typical example.

The ideal countermeasure on the range-extending route is to completely develop the power system by itself. More than a year ago, the chief engineer of Geely’s 1.5T engine was recruited to form his own 1.5T 4-cylinder R&D team, and a large number of engine R&D personnel were recruited in Shanghai. The first generation was to continue to purchase the new 1.5T engine of Mianyang’s Xinchen Power model, and the second generation is a self-developed high thermal efficiency model.

In fact, the follow-up ideal is to continue to make continuous efforts in the self-development of the range-extending system. With the help of the development of the trend of large-scale battery-extending range, in addition, it is also necessary to deepen the relevant algorithms of vehicle-road coordination to penetrate the point of range-extending and continue to strive for government support. . Generally speaking, Ideal still has plenty of time to develop and fine-tune the team and product line, as long as the person in charge does not mess around with his brain, it will be ok.

Finally, the trend of the next wave of economic crisis is a huge wave that all car companies will face, and it will permanently change the market structure in the next 5-10 years.

In my opinion, the tech dream period, or the golden age of the flashy tech bubble, is on the verge of its end. The cusp of the wave of consumer culture in the era of realism and low desire has appeared at the beginning of the sea and the sky. The era as we know it is coming to an end. Views on all issues in 2023-2024 must be re-examined from this perspective.

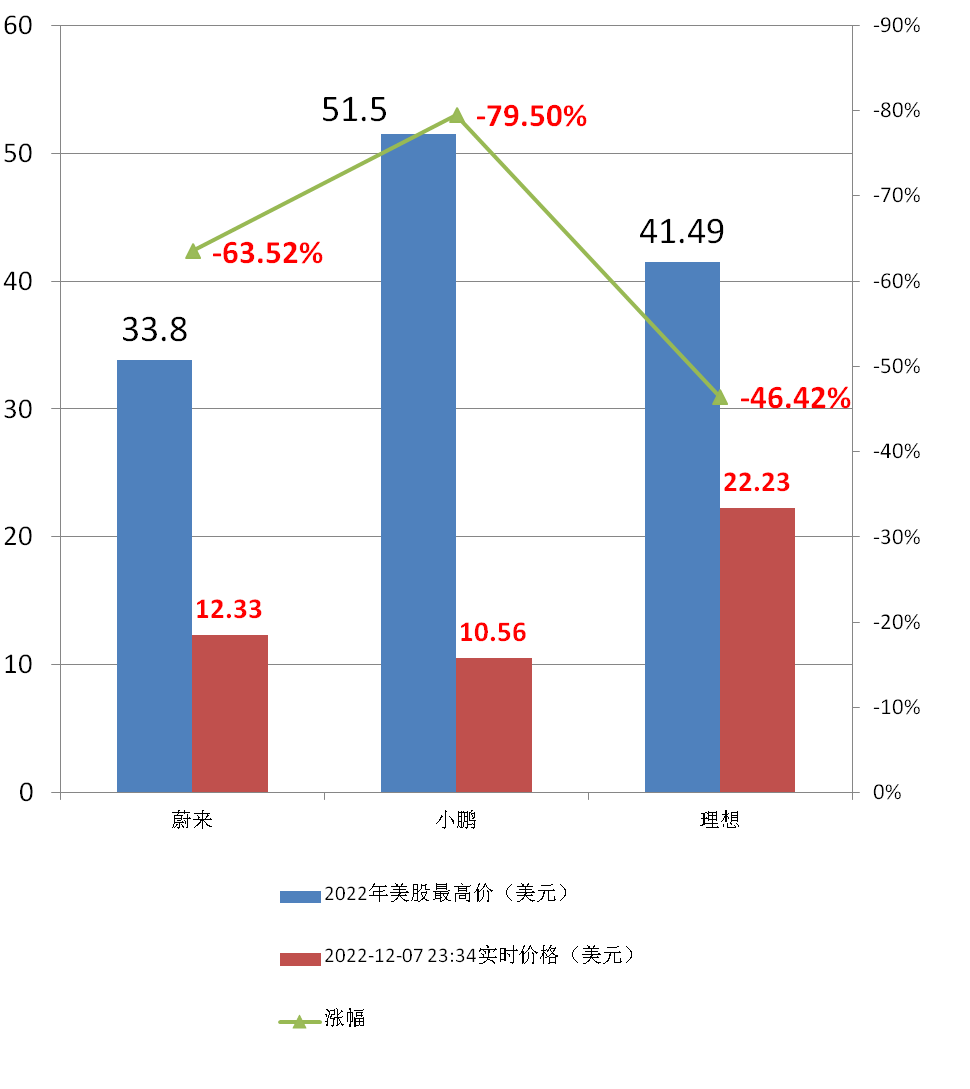

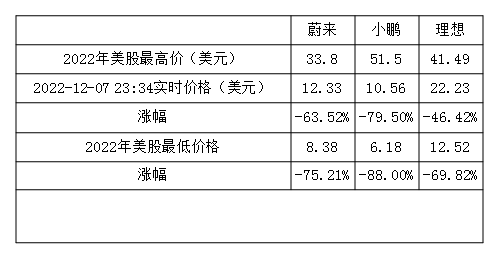

Finally, the 2022 US stock situation of the three companies that are currently beating:

Source: Zhihu www.zhihu.com

Author: JackyQ

[Zhihu Daily] The choice of tens of millions of users, to be a big cow to share new things in the circle of friends.

click to download

There are 456 answers to this question, see all.

Further reading:

What are the highlights of each of the three new car manufacturers, NIO, Ideal, and Xiaopeng?

This article is reproduced from: http://www.zhihu.com/question/436315339/answer/2792046412?utm_campaign=rss&utm_medium=rss&utm_source=rss&utm_content=title

This site is only for collection, and the copyright belongs to the original author.