01 Summary

The streaming industry is experiencing intense competition.

Strong subscriber growth numbers are slowly fading as Disney (NYSE:DIS) and Netflix (NASDAQ:NFLX) hit the limits of the maximum subscribers they can have in the US.

Both streaming giants are shifting their focus to ad-supported tiers, which should generate a lot of revenue in the coming years.

02 Introduction

The streaming industry will face major changes in the coming years. So far, the growth trend remains strong, with investors prioritizing user growth over profitability. That trend has started to shift in recent months due to Netflix’s subscriber loss, Disney’s rising content costs and declining consumer sentiment data across the economy. This has shifted the focus to streaming companies’ profitability rather than subscriber growth.

This is a new trend in the streaming space, and we will see further development of this trend in the next few years, which is more suitable for the new trend.

streaming trends

85% of U.S. households subscribe to a streaming service. In addition, each household has 3 paid streaming services. Before 2022, the streaming media industry mainly focuses on user growth, and pays less attention to content fees and overall profitability. Markets and investors behave the same way, and one of the most important facts about each quarter is the growth in the subscription base and the number of new subscribers.

This trend will start to change in the second half of 2022, and this new trend will be with us for a long time. Disney’s stock took a beating after it reported its fourth-quarter subscriber growth numbers and higher fees, followed by a CEO replacement. Since the second half of 2022, the focus of streaming platforms is to grow revenue and maximize revenue per subscriber, rather than excessive growth in subscriber numbers.

They are all very focused on monetization and ad support layers. Originally Netflix’s CEO said they would never show ads, then reconsidered that stance after disappointing quarterly results, and then the new date was pushed from the initial plan to launch the ad-supported tier in the first quarter of 2023 It’s November 3, 2022. Disney’s ad support arrives in December, and their current plans have seen a huge price increase. This was due to slower overall growth in new users and increased revenue.

Almost every streaming platform spent a lot of resources on reboots, sequels, and big franchises in the 80s, 90s, and 2000s because people who grew up in the 1980s, 1990s, and early 2000s spent money on streaming. most time and money. This trend is likely to continue in the next 5-10 years.

Live sporting events and events are also growing in popularity and this market will experience significant growth over the next 5 years. The global online live video sports streaming market is expected to grow at a CAGR of 21.5% from 2022 to 2027. There are two main factors behind this extremely rapid projected growth. One reason is growing interest in watching live sporting events; another is the digital infrastructure already in place, high-speed broadband widely available, and multi-platform and device connectivity services emerging.

The biggest risk factor is the same as for almost all streaming services: slowing consumer spending. In the event of a severe recession, streaming will be one of the first services customers will cancel. They are not a necessity and due to easy access. So in a severe recession, customers might cancel for a few months and resubscribe when things improve. However, this means not only lost subscriptions, but also lost revenue for streaming service providers.

03 Highlights of Disney and Netflix

Disney has 235 million streaming subscribers, while Netflix has 223 million. Streaming services accounted for 45% of ad views, surpassing TV everywhere. Ad-supported video-on-demand (AVOD) revenue could exceed $69 billion by 2027. That’s nearly double the roughly $37 billion currently spent in 2022. To capitalize on this trend, both streaming giants are moving in this direction.

disney

Disney has started to focus on advertising on its platform, announcing an ad-supported Disney+ tier in August. Investors were not given a ton of information about its specifics, other than a Dec. 8 launch date. On the same day, Disney raised the price of its streaming service by 38%. In terms of subscriber growth, if we strip out external macroeconomic factors, Disney is in a better position than Netflix just based on the attractiveness of its produced content. Thanks to their well-known brands such as Star Wars, Marvel, Toy Story, and more, they are in an excellent position to produce content for every generation.

In the third quarter, direct-to-consumer expenses increased due to higher marketing and content creation costs. Starting next quarter, management expects those losses to dwindle, and the streaming service should break even by 2024 before starting to generate consistent profits for Disney. This is also the motivation behind the leadership change.

So the next phase of direct-to-consumer is to grow revenue (through increased advertising and subscription fees), rationalize spending like marketing and content creation costs, and deliver blockbuster programming to increase customer engagement on the platform. Disney’s biggest challenge is its lack of content revenue and monetization. Bob Chapek (former CEO) emphasized on the earnings call that Disney is well positioned to “win the streaming wars”:

“Building a streaming powerhouse required significant investment. Now, with its scale, incredible content pipeline and global reach, Disney+ is well-positioned to leverage our position for long-term profitability and success.”

ESPN+ is a strong player in the live sports streaming space. They were able to extend the agreement until 2025 to host one of the world’s fastest-growing live sporting events: Formula 1. Additionally, Disney is considering integrating sports betting on some live events into its platform in some way. I’m sure this won’t be coming for the next few months, management hasn’t provided any updates since Q3, but in the background, they’re working on:

Add some utility to sports betting and remove some friction for our guests. We’ve found that sports fans under the age of 30 absolutely need this type of utility in the overall portfolio that ESPN offers. So we think it’s important. We’re working on it, and we hope to announce something in the future.

App Economy Insights

Netflix

Netflix is about to test several new live shows in the coming months. The reason behind this is the further increase in broadcasting and streaming market share. One of the first live streams will be a Chris Rock comedy special in early 2023. Management stated that they will focus on this area in the future to take advantage of live streaming. I believe this is a consequence of Netflix pulling out of the bidding process for the rights to broadcast numerous live sports events.

Netflix may be able to win streaming rights to some live sports, but they’re far behind Disney. Disney already has such a competitive advantage in live sports streaming that it will either take years for Netflix to effectively compete with it, or abandon management’s plans to put live major sports events on Netflix.

Netflix is trying to leverage merchandising on its most popular shows, like Stranger Things. In this area, expect some additional revenue in the coming quarters, maybe $75-$100 million per quarter on average in 2-3 years, and maybe $3-400 million in a fiscal year. Disney confirmed that about 6.5% of its revenue comes from product sales and merchandise. At $300-400 million per year in additional merchandise sales, Netflix could increase its overall revenue by about 3.5-4%.

The reason I’m only using a fraction of Disney’s numbers is because of the brand and fan base Netflix has. Despite the success of “Stranger Things” or “The Witcher,” Disney’s all-time favorite “Star Wars” will still lead merchandising for years to come.

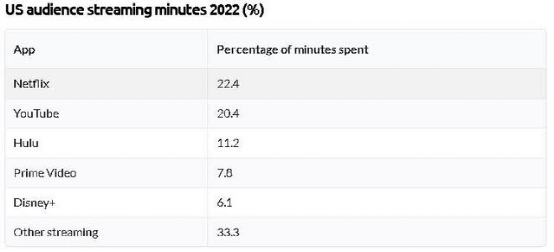

Since the platform has some of the longest viewing hours among its competitors, Netflix is well positioned to see a big jump in revenue from its ad-supported tier. Netflix remains the most popular streaming service in the U.S. in terms of total minutes watched, so if enough subscribers use the ad-supported tier, the platform will be able to generate significant ad revenue.

businessofapps.com

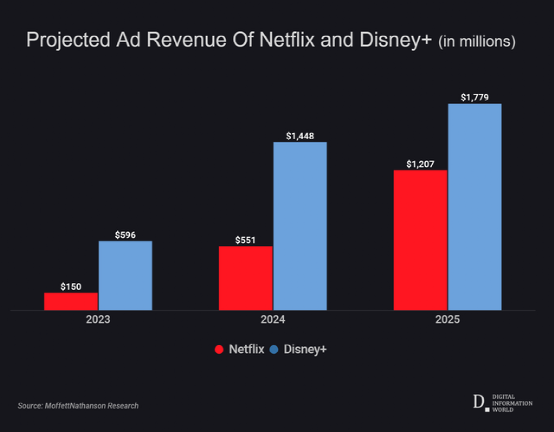

Disney is likely to win the ad spend race in the next 2 years as it already has all the advertisers and infrastructure and the ad-supported tier is being tested on HULU before being applied to Disney+.

digitalinformationworld.com

I like the way Netflix’s management reacted quickly to subscriber churn and declining revenue earlier this year. They work on solving the password sharing problem. However, I seriously doubt that this will work, and that the subscriber base will grow as a result of this management measure.

I’m comfortable with the ad-supported tier introduction because when management first talked about it, the target was for implementation in the first half of 2023, and then about two months later, the deadline was moved to the end of the first quarter of 2023.

After yet another disappointing quarterly performance, management took the initiative to decide to launch the ad-supported tier ahead of its rival Disney, so the date moved to early November 2022.

On the other hand, if we look back at January 2020, the company’s full year 2019 earnings call, the CEO was very clear and certain that they would never show ads on the platform, and they have no intention of changing that in the future.

“We want to be a safe resting place where you can seek thrills, have fun, and not have any controversy about exploiting users through advertising” – CEO Reed Hastings.

Obviously a lot of things have changed in the last 2 years but it looks really bad when the CEO has a clear statement on a topic and then the whole company suddenly changes position due to external shareholder pressure , in addition, dropped its values.

In my opinion, Netflix is a great place to drive revenue through advertising and potentially attract new customers through its low-priced ad subscriptions. It also minimizes subscriber churn in case of a deeper recession, people decide not to pay $9.99/mo or $15.49/mo but the $6.99/mo ad-supported package is acceptable to them .

By my calculations, the wide spread of merchandise will add 3-4% revenue growth to its total revenue over the next few years. The biggest risks Netflix faces are its already top-up customer base, its inability to further expand its subscriber base in North America, and the platform’s decline in satisfaction among its subscribers.

HBO Max leads the industry in customer satisfaction, with 94% of respondents saying they are “satisfied” or “very satisfied” with the service; Netflix, which ranks second overall in 2021, drops to fourth place in 2022 (80 %), behind Disney+ (88%) and Hulu (87%).

App Economy Insights

04 Valuation

If we look at the DCF model, Disney’s valuation is reasonable, while Netflix’s current price is overvalued. However, this reasonable overvaluation is only true when we consider events and profitability in 2023, but if we look further, both stocks are undervalued.

Based on an EPS of 4.9 and a growth rate of 6%, Disney’s fair valuation is around $96-$97 per share. However, the streaming business won’t add any net income until 2023, but by the end of 2024, the streaming business will add to the company’s net income and thus earnings per share. We don’t know the exact numbers, but what we do know is that once the streaming business becomes profitable, it will continue to generate substantial net income for Disney. Analysts’ average target price for Disney is $121, which implies a 20% premium to the current price.

If we look at long-term growth, revenue, and net income estimates, Netflix is less undervalued than Disney. Based on an EPS of 11.2 and a growth rate of 6%, Netflix is overvalued and its fair price is around $220-225 per share. If EPS grows to $15-16 per share by the end of 2024, the fair value would be around $330. This suggests an upside potential of 4% from its current share price. Analysts have an average target price of $293 on Netflix.

If investors look at the future profitability of the two streaming giants, Disney looks more attractive to long-term investors. Investors can’t forget that Disney has several different revenue streams, so this comparison isn’t exactly equal, because if we invest in Disney, we’re not only investing in its streaming business, but in the entire entertainment industry.

05 Conclusion

I believe Disney is better positioned to differentiate itself in the streaming industry due to its ability to generate more cash when it starts running ads on its platform. Merchandise sales could be years ahead of Netflix, while Disney+ still has room to grow its subscriber base.

I don’t see a severe recession in 2023, so I think both streaming giants will be able to generate subscriber growth. However, Disney is better positioned to generate more revenue from its subscribers over the long-term.

This article is from the WeChat public account “Wall Street Events” (ID: WallStreetNews) , author: DanielP.Varga, 36氪 authorized to publish.

media reports

White Whale Going to Sea 36Kr Sina Technology Sina IT Home Pinwan

Event Tracking

- 2022-12-08Disney ‘s streaming media service Disney+ launches ad-supported version to open up new revenue-generating channels

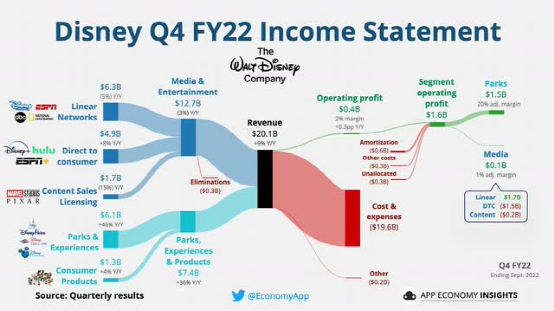

- 2022-11-09Disney released its financial report for the third quarter and its revenue reached 20.15 billion US dollars

- 2021-08-12 Disney: The total number of global subscribers in the streaming media business is close to 174 million

- 2021-05-13 Disney’s Disney+ paid subscribers in the second quarter of fiscal year 2021 were 103.6 million, less than expected

- 2020-11-12 Disney+’s paid subscribers in the fourth quarter exceeded expectations, and Disney’s stock price rose 6% after hours

This article is transferred from: https://readhub.cn/topic/8lzxH00l0kd

This site is only for collection, and the copyright belongs to the original author.