©️True Detective AlphaSeeker Original

Author | Li Jinglin

You may not have played “Blue Moon”, but you must be familiar with this name. “Hi everyone, I’m Zha Zhahui, if I’m a brother, come and kill me.” Hong Kong movie star Zhang Jiahui’s advertising slogan has appeared on computer pop-up windows or webpages many times. If you accidentally click on it, you will be heavily criticized Earthy brainwashing.

Five years ago, this brainwashing advertisement became a phenomenal marketing event. Five years later, the company responsible for operating “Blue Moon” is heading for an IPO. Recently, Zhongxu Future officially submitted a prospectus to the Hong Kong Stock Exchange, intending to list on the Hong Kong Main Board.

Relying on “Playing Blue Moon”, Wu Xubo, the founder of Zhongxu Future, made a lot of money. In 2021, Wu Xubo will become one of the four richest entrepreneurs in Shangrao, Jiangxi Province with a net worth of 5.56 billion yuan. Wu Xubo, who was a policeman, started an Internet game business early in the morning. In 2006, he founded the 91wan web game platform and acted as an agent for the game “Three Kingdoms”.

In 2015, Wu Xubo established Zhongxu Future, focusing on the distribution and operation of legendary games. According to the prospectus, Zhongxu Future has marketed and operated 259 interactive entertainment products, including 225 game products and 34 online literature products. Among them, 9 interactive entertainment products have been operated in depth for more than 5 years, and 27 interactive entertainment products have been operated for more than 3 years.

Games and brands under Zhongxu Future | Source: Tanwan Blue Moon Official Weibo

Relying on earth-flavored legendary games such as “Playing with Blue Moon” and “Legend Overlord”, Zhongxu Future has won batches of middle-aged men between the ages of 30 and 45 in fourth- and fifth-tier cities, and it is precisely this group of users , Pushing Zhongxu Future to the secondary market.

Earthy, legendary game, how much charm and money-absorbing ability does it have?

The pattern is mature

In the field of Internet games, making legendary games is an excellent business model. R&D costs are low, users are willing to pay krypton gold, a game can be operated for a long time, and the method can be replicated and quantified. These advantages can be seen from Zhongxu’s future operating data.

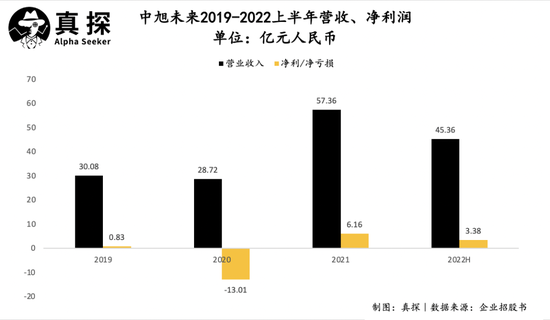

According to the prospectus, from 2019 to the first half of 2022, Zhongxu’s future revenue will be 3.008 billion yuan, 2.872 billion yuan, 5.736 billion yuan and 4.536 billion yuan respectively. Except for the decline in 2020, the overall growth has maintained a good momentum, and a certain scale advantage has been formed. According to data from Jefferson & Sullivan, in terms of revenue, Zhongxu Future will be China’s fifth largest mobile game product marketing and operation platform in 2021, and China’s second largest non-self-developed mobile game product marketing and operation platform.

In the overall revenue scale, Zhongxu even surpassed the game business revenue of listed companies such as Bilibili and Sohu in the future, which is enough to rank among the top ten in the revenue list of Chinese listed game companies.

Let’s look at the specific business of Zhongxu in the future.

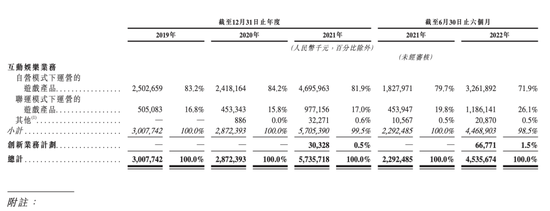

The company’s business is mainly divided into two major categories, interactive entertainment business and innovation business. Among them, the innovative business is dominated by the fast food brand “Zhazhahui” and the trendy toy brand Bro Kooli. Although in the first half of 2022, the revenue of this business has increased by more than 120%, but it only accounts for 1.5% of the total revenue. It is still the interactive entertainment business that holds up the banner of Zhongxu’s future.

Zhongxu’s future interactive entertainment business mainly has two major models, namely the self-operated model and the joint operation model. From 2019 to the present, the revenue of Zhongxu Future under the self-operated model is 2.503 billion yuan, 2.418 billion yuan, 4.696 billion yuan and 3.262 billion yuan respectively, accounting for 83.2%, 84.2% and 81.9% of the total revenue respectively. % and 71.9%. The income of the intermodal mode was 505 million yuan, 453 million yuan, 977 million yuan and 1.186 billion yuan, respectively, accounting for 16.8%, 15.8%, 17.0% and 26.1% of the total revenue for the current period.

The main criterion for distinguishing these two models is to see whether the end-user acquisition of its agency products utilizes the delivery and intelligent analysis tools developed by Zhongxu in the future——Hetu and Luoshu platforms.

Zhongxu’s future business revenue | Source: Corporate Prospectus

It can also be seen from this business model that Zhongxu will not make games in the future, they are just the “porters” of games, and helping agent game launch and purchase volume is their main business.

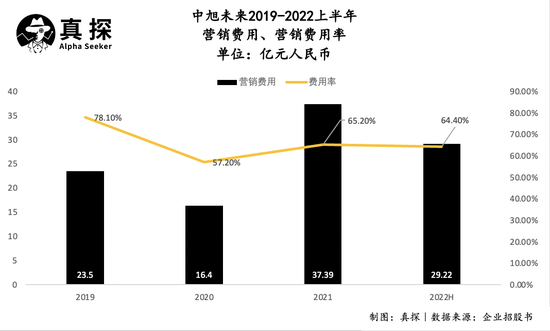

The high marketing expenses are the evidence. From 2019 to the first half of 2022, Zhongxu’s future sales expenses will be 2.350 billion yuan, 1.643 billion yuan, 3.739 billion yuan, and 2.922 billion yuan, accounting for 78%, 57%, 65% and 64.4% of total revenue respectively. %, the prospectus shows that these expenses are mainly spent on online traffic acquisition fees, offline marketing expenses and celebrity endorsement fees paid to cooperative online media platforms.

For users, the most intuitive is naturally the spokesperson that Zhongxu will invite for the game in the future. According to the prospectus, in recent years, the company has more than 30 spokespersons for its products. Hong Kong and Taiwan stars such as Zhang Jiahui, Chen Xiaochun, Zhu Yin, Donnie Yen, Aaron Kwok, Nicholas Tse, etc. have all appeared in its game advertisements. However, Liu Yang, head of Zhongxu’s future brand business department, once mentioned at the Huge Creative Festival that the annual cost of spokespersons accounts for 0.4%-0.6% of his budget—that is to say, the purchase volume is Zhongxu’s future spending. largest sum of money.

According to the prospectus, Zhongxu will rank fourth in the amount of advertisements for domestic game products in 2021.

Net profit margin is lower than peers

Crazy relying on marketing to obtain traffic, the result reflected in the financial data is “high gross profit, low net rate”.

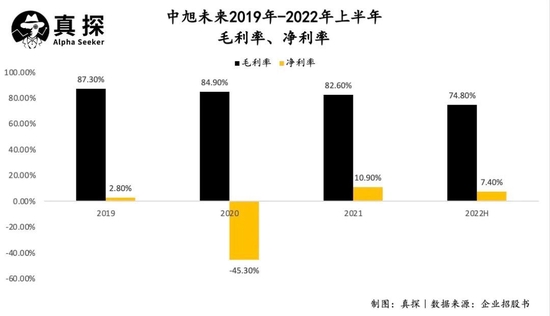

According to the prospectus, from 2019 to 2021, Zhongxu’s future gross profit margins will be 87.3%, 84.9%, and 82.6%, respectively. In the first half of this year, the company’s gross profit margin declined to only 78.4%. Zhongxu explained this in the future, mainly due to the increase in the percentage of revenue generated from game products operating under the intermodal mode to total revenue.

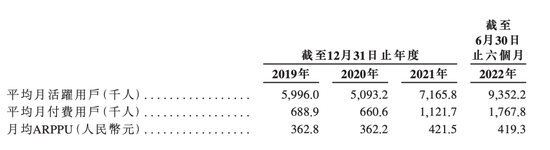

The overall high gross profit stems from the super gold-absorbing ability of legendary games. According to the prospectus, as of the six months ended June 30, 2022, Zhongxu Future has a cumulative registered users of 274.2 million, an average MAU of 9.4 million, and an average monthly contribution of 397.4 yuan per paying user. In comparison, in the first half of this year, the ARPPU of Celadon Game, the developer of the cultivating mobile game “The Strongest Snail”, was 209 yuan, and the ARPPU of Feiyu Technology, which also belongs to the field of leisure technology, was 42 yuan. The earning power of legendary games can be seen.

Zhongxu Future User Data | Source: Corporate Prospectus

The gross profit margin difference between Zhongxu’s two businesses in the future is also huge. In the past three years and the first half of this year, the gross profit margins of Zhongxu’s self-operated model in the future were 95.1%, 95.6%, 94.9% and 95.2%, respectively, and the gross profit margins of game products operated under the joint operation mode were 48.9%, 27.8%, and 24.1% respectively. and 20.1%. The reason for this difference, Zhongxu Future explained: Mainly because of the impact of cost, in the first half of this year, the sales cost of the intermodal mode accounted for 82.5% of the total sales cost. Under this mode, Zhongxu Future needs to pay a large amount to the cooperative distribution channel. commission.

In the operation of legendary games, the degree of krypton gold of users mainly depends on the settings of the game, and the number of users mainly comes from the amount of purchases. In the future, Zhongxu has accumulated a large number of users by purchasing volume, but this mode of operation has also led to a low level of its net profit margin.

According to the prospectus, the net interest rate of Zhongxu Future has been 2.8%, -45.3%, 10.7% and 7.4% since 2019, which is far lower than that of its peers. In the first half of this year, the net profit margin of Sanqi Mutual Entertainment was 20.94%, Gigabit was 27.40%, and Perfect World was as high as 30.43%.

The difference between gross profit rate and net profit rate of more than 10 times reflects the disadvantages of Zhongxu’s future business model. Moreover, in the case of continuous increase in purchase volume, the cost continues to rise, and its gross profit rate has continued to decline in the past three years.

Legendary games are not good

Although from an ideal model point of view, legendary games are a good business model, but the current market is not optimistic.

According to the report released by Gamma Data in 2020, the legendary IP has been born for 20 years, with a cumulative registered user of more than 600 million, an annual turnover of more than 10 billion yuan, and a cumulative value creation of more than 90 billion yuan. There will be 40 billion yuan in the next three years potential value. Although the cake is big, there are too many people who can’t stand the cake.

In 2021, DataEye Research Institute released the “Special Research Report on Legendary Games”. The report clearly stated that under the trend of fierce competition, legendary games have become a red sea. The data shows that the purchase volume of legendary games accounted for nearly one year. 15% of the broader market, ranking first among mid-to-heavy mobile games in terms of buying volume. The huge buying volume is supported by game companies flocking to them. According to the statistics of DataEye Data Research Institute, nearly half of the top 100 game purchase companies in the main list in 2020 have purchases involving legendary products. Sanqi Mutual Entertainment, China Mobile Games and other major game companies are all competitors of Zhongxu in the future, and many small companies are also enough to cause headaches.

Moreover, the cost of advertising for Legendary is also increasing, and the future trend of Zhongxu’s marketing expenses also proves the status quo of the industry. DataEye Data Research Institute uses CPA (cost per action, CPA=total cost/number of conversions) to judge the cost of advertising. The results show that from November 2021 to May 2022, the CPA value of legendary games will continue to remain high. The CPA on the iOS side remains above 150/A, and the peak value can exceed 200/A. The increase in launch costs will further increase, mainly relying on the future pressure of Zhongxu, which mainly relies on buying volume to acquire customers.

The industry’s broader market is involuntary, and Zhongxu’s own situation in the future also has pitfalls. In the prospectus, Xu Future disclosed that as of November 18, 2022, the company still has five pending intellectual property-related lawsuits. Complete legendary IP authorization. A series of issues such as defense and compensation will have an impact on Zhongxu’s future business and financial status.

In addition, the acquisition of the game version number will further restrict the future prospects of Zhongxu. Among the six batches of 384 game version numbers that have been issued this year, Zhongxu only got one version number in the future.

In the item of risk factors in the prospectus, Zhongxu Future has a clear idea of the above-mentioned problems. Regarding the future, Zhongxu Future stated that it will launch 30-50 games by the end of 2023, and the types involved include RPG and casual game console SLG. Expanding the business plate is a way to share risks, but to what extent it can be achieved and whether it can be done still needs to be tested.

Relying on the magic and textbook version of brainwashing marketing, Zhongxu Future has entered people’s sight and entered the capital market. The listing is the recognition of the “miracle” of the past. But in the 500-plus-page prospectus, the company’s weaknesses are also clearly revealed. In order to continue to advance in the capital market, Zhongxu still has a very difficult way to go in the future.

(Disclaimer: This article only represents the author’s point of view, not the position of Sina.com.)

This article is reproduced from: https://finance.sina.com.cn/tech/csj/2022-12-14/doc-imxwrusp7418435.shtml

This site is only for collection, and the copyright belongs to the original author.