———The fixed income fund classification method we created

Fund classification is the foundation of fund research.

We have published the classification method of equity funds before, see ” 8 Style Classifications of Partial Equity Funds “

Fixed income funds are more difficult to classify than equity!

From the perspective of product positioning, there are short-term bonds, long-term bonds, fixed-term bonds, primary bond bases, secondary bond bases, fixed income +, equity-debt balance, and flexible allocation of equity-debt, etc. However , under the same product type, the investment goals may vary greatly. For example, the same fixed income +, some pursue conservative and stable returns, while others boldly pursue excess returns.

In addition, there are partial debt FOF, quantitative hedging, REITs and other funds, which also aim at absolute returns and can also be regarded as fixed-income funds.

In terms of investment strategies, some funds mainly increase leverage, some use interest rate bonds for fluctuations, some for credit debt sinking, some for dynamic adjustment of large categories of assets, some for new investments, some for futures hedging, and some for convertible bonds . Funds of the same type may use very different strategies and risk exposures.

In addition, some fund managers also manage multiple types of funds, such as managing both pure debt and equity-debt balance funds; some funds have dual-manager configurations, and it is difficult to distinguish from the perspective of fund managers.

So how should it be classified? We thought in every possible way, and finally simply abandoned all the traditional classification methods, but from the perspective of investors, no matter what type of fund or investment strategy, we unified the risk-return (volatility rate and maximum return rate) of more than 5 years. Withdrawal) performance classification .

We believe that no matter what kind of investment constraints you face, as long as you are exposed to a certain level of volatility risk during a bull-bear cycle (more than 5 years) from the results, you should be classified as this risk level.

If you create the best return, or the best Sharpe ratio and Karma ratio in this risk level, you can be called excellent.

The following are the five fixed income categories we have created, which are classified according to the risk from small to large and the suitable holding period from short to long:

(1) Cash substitute

The annualized volatility is <1%, the maximum drawdown is <2%, and the historical annualized rate of return is 2.5-3.5%.

The closed period is preferably no more than one year, and no equity and convertible bonds are invested. Mainly monetary funds, bond index funds, interbank certificate of deposit funds, short-term bond funds, etc.

The following table briefly lists some representative funds of this category and their data performance (not recommended, the data is for the past 5 years, from 2017-12-27 to 2022-12-27, the same below)

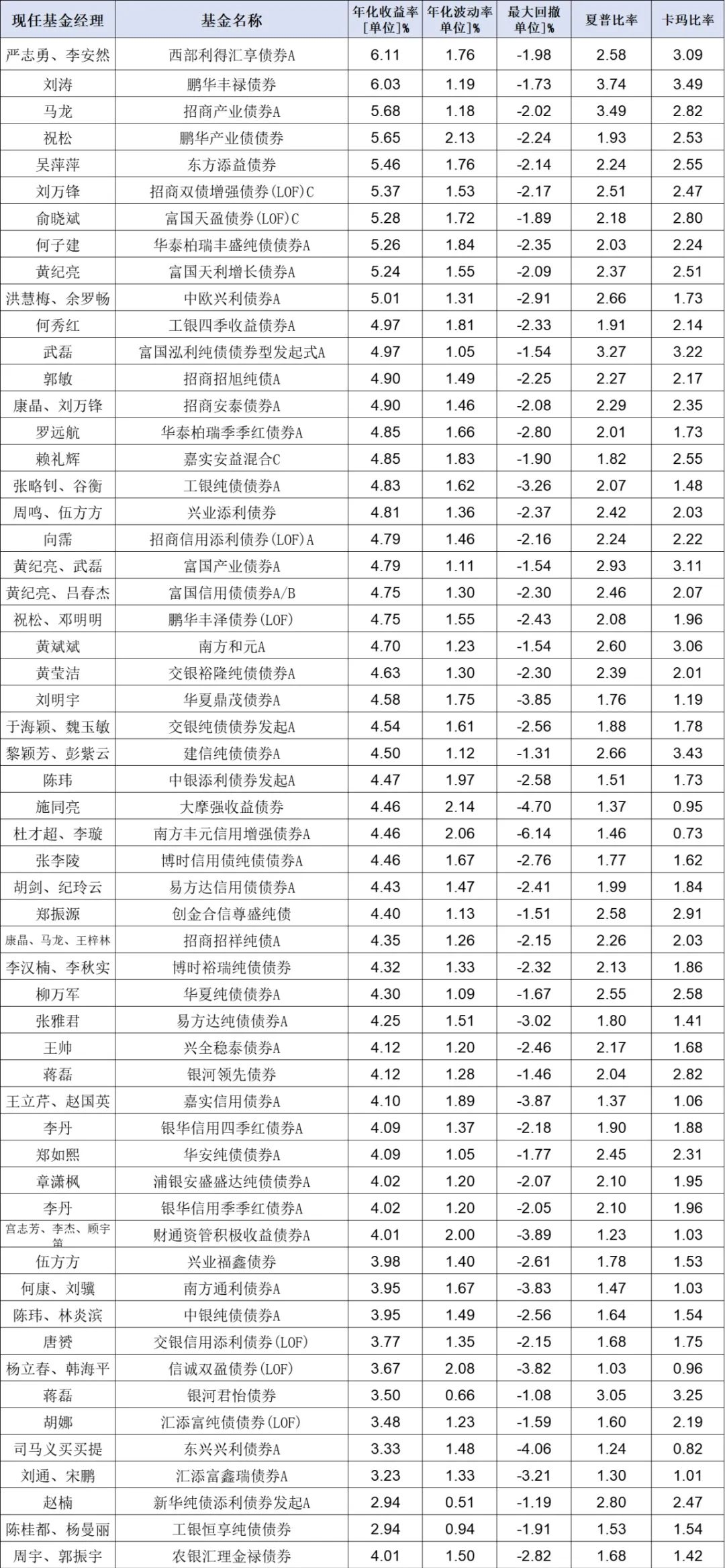

(2) Conservative income category

The annualized volatility is <2.5%, the maximum retracement is <4%, and the historical annualized rate of return is 3.5-5.5%.

The closed period is preferably no more than 1.5 years. Generally, medium and long-term bonds are the mainstay, and no equity is invested, and convertible bonds may be invested. Mainly long-term bonds, fixed-term bonds, and a few primary and secondary debt bases.

The following table briefly lists some representative funds of this category and their data performance

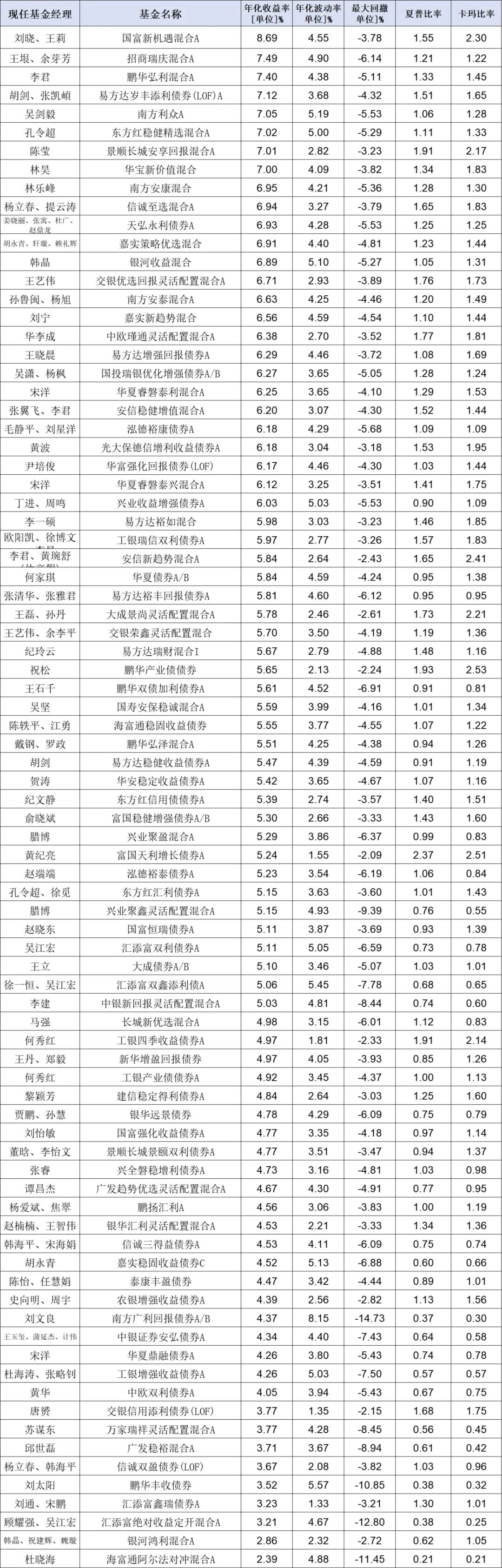

(3) Steady “fixed income +”

The annualized volatility is 2.5%-5%, the maximum retracement is <8%, and the historical annualized rate of return is 5-8%.

The closed period is best not to exceed 2 years, and generally invest in long-term bonds, equity and convertible bonds, mainly primary and secondary debt-based, fixed income +, flexible allocation funds.

The following table briefly lists some representative funds of this category and their data performance

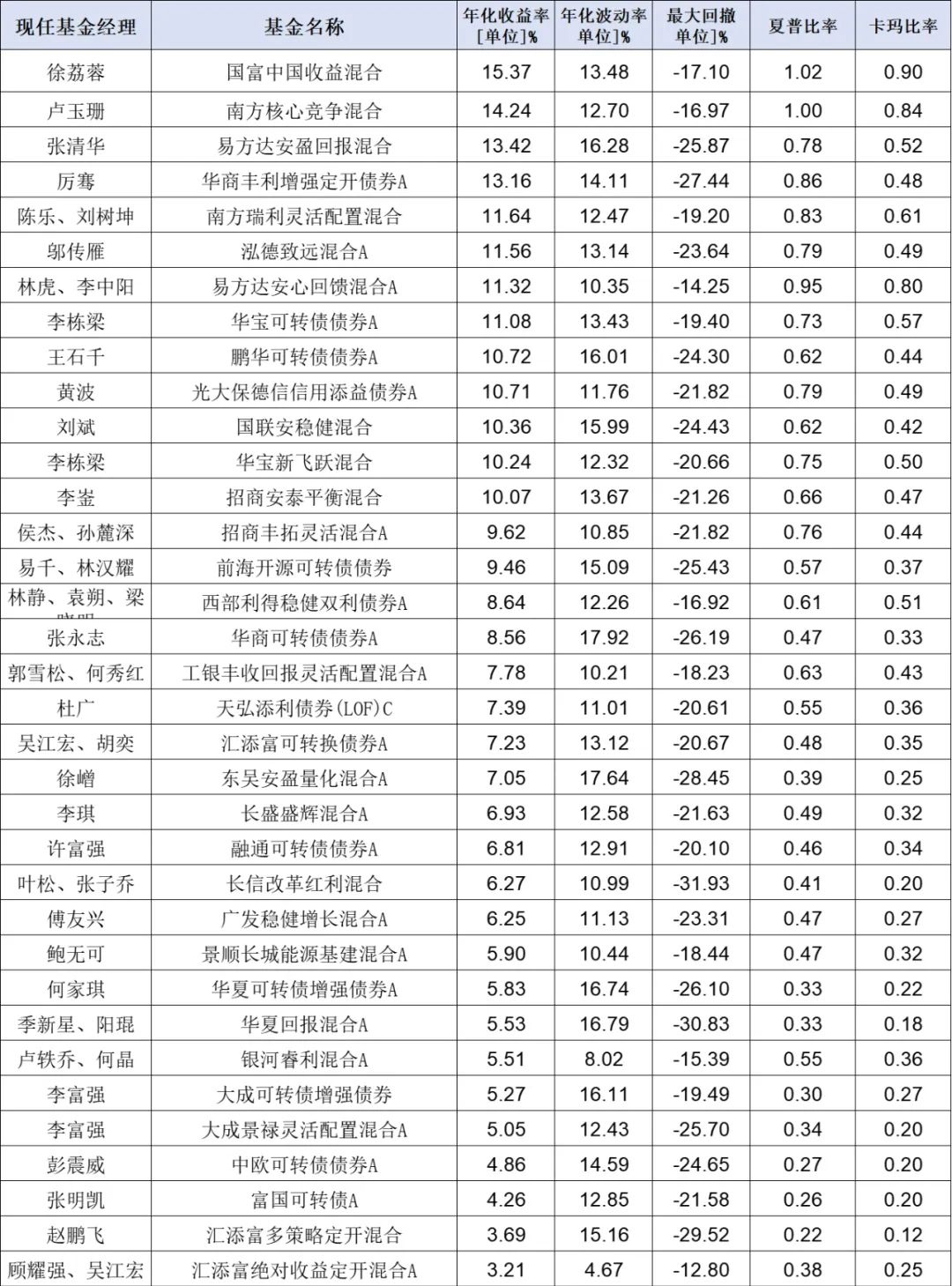

(4) Actively “fixed income +”

The annualized volatility is 5%-10%, the maximum retracement is <15%, and the historical annualized rate of return is 6-12%.

The closed period is preferably no more than 3 years, and equity and convertible bonds will definitely be invested. Mainly secondary debt base, fixed income +, flexible allocation funds.

The following table briefly lists some representative funds of this category and their data performance

(5) Equity-debt balance category

The annualized volatility is 10%-15%, the maximum retracement is <25%, and the historical annualized rate of return is 8-16%.

Generally, at least 30% of positions are invested in equity, and equity positions may be adjusted flexibly. Mainly flexible configuration funds and convertible bond funds.

The following table briefly lists some representative funds of this category and their data performance

Category description

①Using the weekly annualized volatility data, the historical data is generally required to be more than 5 years, and the short-term debt is slightly relaxed (because most short-term debts have been established for a short time).

②If the annualized volatility > 15% and the maximum drawdown > 25%, we don’t think it can be regarded as a fixed-income fund, and should be regarded as an equity fund.

③We compare the fixed-term bond and open-end funds separately, because the fixed-term bond position can reach 200%, and the open-type fund can only reach 140%.

④ We have certain requirements for the closing period, because we believe that the closing period of a good fixed-income product should not exceed the matching reasonable fund duration by a large margin, without sacrificing the liquidity of investors.

⑤ We have not taken REITs, FOF and fund investment into consideration for the time being. First, these products generally have not been in operation for a long time; second, some funds are positioned for retirement, and risk exposure will change.

⑥ At present, the most funds on the market are mainly (2) conservative income and (3) stable and fixed income +, and the stock-debt balance fund is the least.

⑦The classification of some funds may jump. For example, some secondary debt funds may be classified as conservative income by me due to their extremely conservative operation. Exposure to risk is suddenly magnified.

Conclusion: I am a non-professional, and the classification method may not be very scientific, it is for reference only.

After the classification is clear, you can make better horizontal comparisons and select excellent funds. In the next article, I will jointly launch [2023 Fixed Income Fund Manager TOP50] with @点拉投资. Welcome everyone to pay attention to the gz account @点拉Investment and @直城投资

Related reading:

8 major style classifications of partial stock funds

2022 Top 100 List of Equity Fund Managers

$E Fund Anxin Return Bond A(F110027)$ $Penghua Fengrong Fixed Open Bond(F000345)$ $Bosera Credit Bond A(F050011)$

There are 9 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/9290769077/238691633

This site is only for collection, and the copyright belongs to the original author.