This article is only for discussion, let’s consider it a possibility, I don’t expect it to be right.

Before 2021, the rapid growth of the cxo industry has brought about a strong wealth effect. For example, Asymchem, WuXi AppTec, Tigermed, and Hillhouse Capital have basically held them for a long time, but they have been liquidated one after another. The topic we discuss is whether the cxo industry is cyclical.

First, the operating characteristics of the industrial chain.

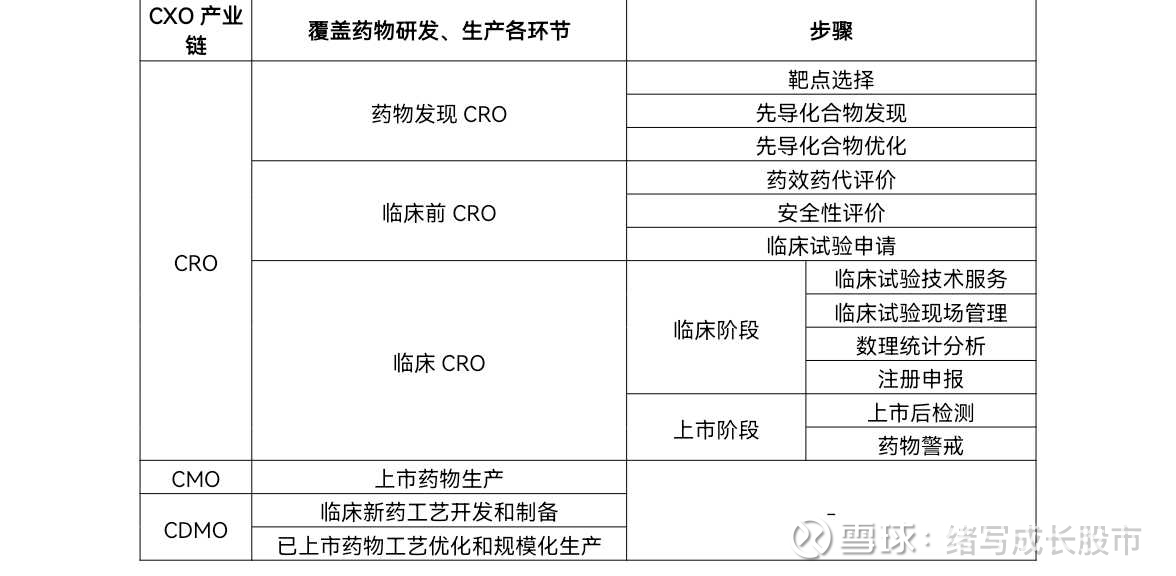

Drug research and development roughly follows the following chain: drug discovery → preclinical research → investigational new drug application (IND application) → clinical research → new drug application (NDA application) → marketing. Due to the high R&D expenditure, high failure rate, and long R&D cycle (usually 10-15 years) of new drugs, a large amount of capital needs to be invested in the construction of production lines after new drugs are launched. In order to save costs, improve R&D efficiency, and reduce R&D failure losses, pharmaceutical companies will Some R&D and production are entrusted to CXO manufacturers.

CXO is a pharmaceutical contract outsourcing service provider covering the entire industrial chain of drug R&D and production. According to different responsibilities, it is further divided into: CRO, CMO, CDMO. CRO, that is, contract research and development organization, is mainly responsible for new drug research and development and clinical trials, and can be subdivided into drug discovery stage CRO, preclinical stage CRO, and clinical stage CRO.

Among them, drug discovery CRO is the starting point of new drug research and development. The core patent of the drug is the compound development patent, which has high technical requirements and relatively strong bargaining power. It is mainly responsible for target selection, new drug discovery, new drug design, drug screening, etc.;

Preclinical CRO is mainly responsible for drug pharmacokinetics, pharmacology and toxicology, animal models and other research; clinical CRO is mainly responsible for clinical trial technical services, data management, statistical analysis and registration applications.

CMO, that is, contract manufacturing organization, is mainly responsible for providing pharmaceutical companies with large-scale/customized services for pharmaceutical products.

CDMO, contract research and development production organization, provides pharmaceutical companies with clinical new drug process development and preparation, as well as marketed drug process optimization and large-scale production services, that is, the production of preclinical and clinical trial research drugs, as well as commercial drug production . For ease of understanding, the industrial chain is as follows:

With the steady growth of global pharmaceutical R&D investment, the increase in the outsourcing ratio of large pharmaceutical companies, and the rapid growth of demand from small and medium-sized pharmaceutical companies, the global CXO industry market has shown a steady increase from US$70.3 billion in 2013 to US$160.4 billion in 2021. The compound growth rate from 2018 to 2021 will reach 11.72%.

Benefiting from cost advantages, global CXO production capacity continues to shift to my country. At the same time, driven by multiple factors such as domestic pharmaceutical policies encouraging innovation and engineer bonuses, my country’s innovative drug R&D and production market demand continues to grow, further promoting the development of the CXO industry. According to the 2021 Frost&Sullivan The report predicts that the global outsourcing service market (excluding macromolecular CDMOs) provided by Chinese pharmaceutical R&D service companies will grow from RMB 98.5 billion in 2021 to RMB 300.6 billion in 2026, with an average annual growth rate of 25%.

2. Key factors affecting business operation

The CXO industry plays a role in improving R&D and production efficiency and reducing costs by helping pharmaceutical companies in R&D and production. Common key operating data are the number of customers, order volume, production capacity, R&D and production personnel, and human efficiency.

1. Customers, look at the number of customers and the year-on-year growth rate of the number of customers.

2. The order status depends on the order completion status and future order volume. For the order completion, it mainly depends on the project completion volume (such as IND application volume, clinical phase 1, phase 2, phase 3 volume, commercialization volume, etc.), and the year-on-year growth rate of completed orders. For the future order volume, it is judged from the two dimensions of advance receipts and the number of new customers.

3. Production capacity depends on the scale of existing laboratories and factories.

4. R&D and production personnel, judged from the number of R&D and production personnel.

5. The situation of personnel efficiency depends on the sales revenue created per capita and the profit created per capita.

Due to the different business functions of CRO and CDMO, the CRO industry needs to pay more attention to human efficiency, while the CDMO industry should focus on the income brought by unit fixed assets, that is, the turnover rate of fixed assets.

3. What is the difference between the CXO industry a few years ago and the future

A few years ago, benefiting from the cost advantage, the global CXO production capacity continued to be transferred to my country. At the same time, under the policy dividend of the domestic pharmaceutical listing license holder system, the industry penetration rate increased rapidly, and the industry exploded rapidly. Undoubtedly, that period belonged to the golden period of industry development.

However, after 2021, as the penetration rate reaches a certain level, the supply-side reform of pharmaceutical R&D and orders will focus more on foreign countries, and the growth rate will gradually decline.

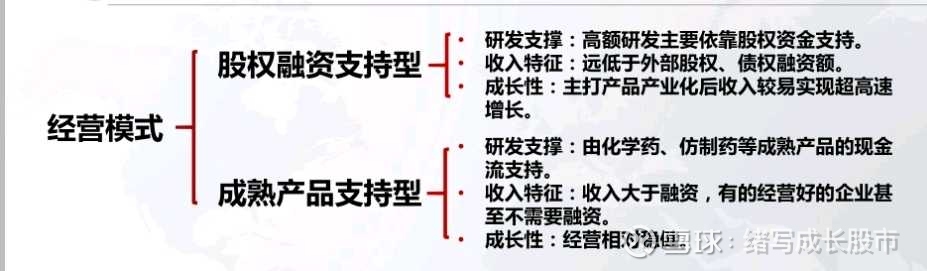

4. I think there are two main business models in the pharmaceutical industry

5. I think the cycle conduction path

More and more pharmaceutical companies choose equity financing support. I think the incentive for the cyclical transmission path is the capital support after the profit increase.

The conduction path is as follows:

Policy balance encourages innovation—increased pharmaceutical profitability—capital support—more R&D investment and clinical trials—increased cxo orders—improved cxo profitability

Intense drug competition—decreasing prices—decreasing profits—capital winter—reduced R&D investment—decreased cxo orders—decreased cxo profitability

6. The current cycle position

The winter of capital, the position of the bottom, the sign of recovery is the growth of various financing events.

@今日话论@雪球创作者中心$ WuXi AppTec(SH603259)$ $Asymchem(SZ002821)$ $Hengrui Medicine(SH600276)$

This topic has 1 discussion in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/1676034855/239611755

This site is only for collection, and the copyright belongs to the original author.