Today’s research is Gartner, which frequently appears in the report data source. This company, known for its IT market research and consulting services, has a history of more than 40 years. Its revenue has achieved an annualized growth rate of 15% in the past 10 years, and its stock has an annualized rate of return of more than 20%. Another invisible bull of the year.

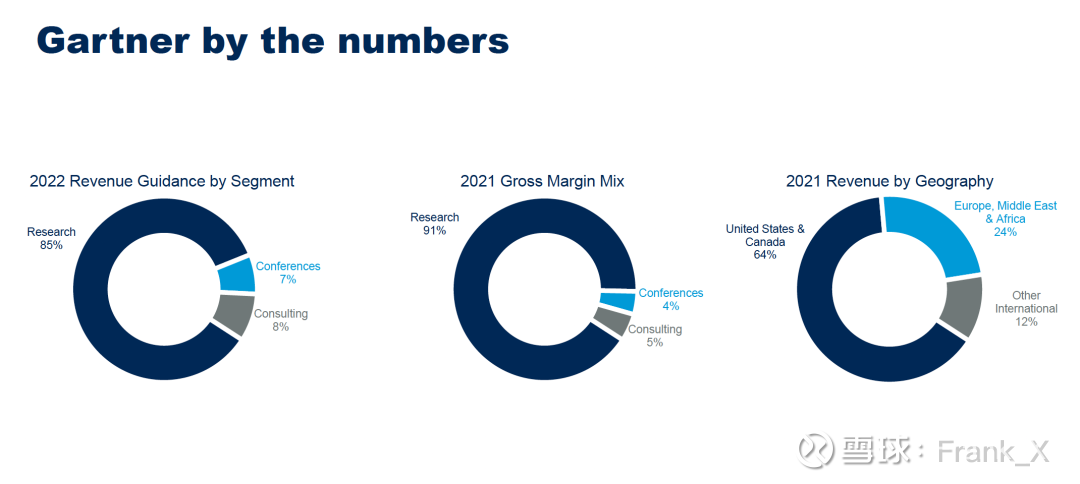

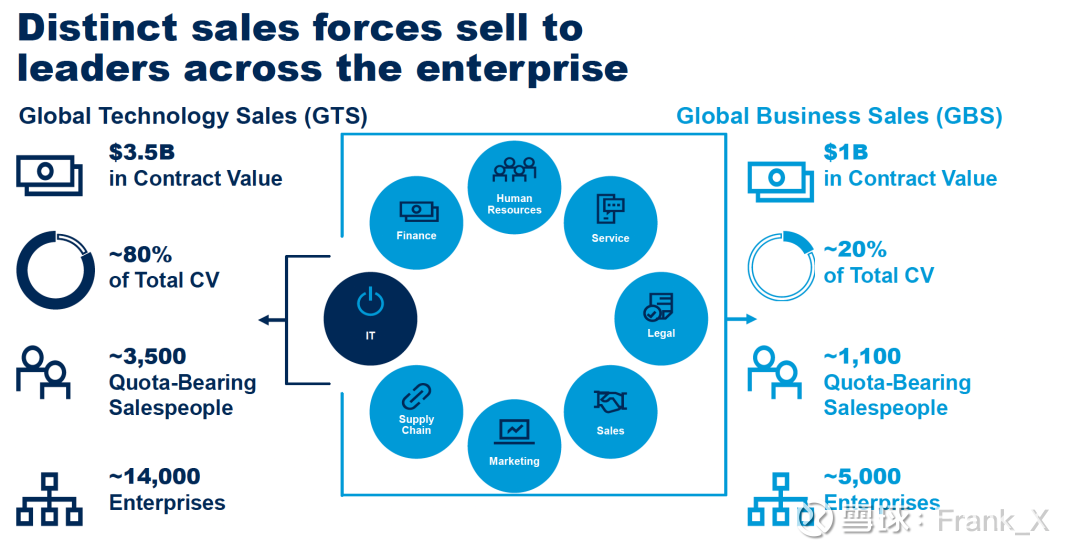

More than 80% of Gartner’s revenue comes from research business with higher gross profit margin, and the rest is conference (industry summit) and consulting (consulting project). The latter two are more business extensions of research around customer scenarios. North American market revenue accounted for more than 60%. The research business is to provide decision-making data information and key insights for corporate executives in different industries. More than 90% of Research services are subscription-based recurring revenues, the customer renewal rate is 80%-90%, and the retention rate calculated by contract value exceeds 100% (ARPU increase and new subscription contracts). Gartner’s famous IT business accounts for 80% of research revenue, and is called GTS (global technology sales) internally. The remaining 20% is contributed by the faster-growing GBS, including consulting services for sales, marketing, supply chain and other functions, which is the second curve of the company’s key expansion.

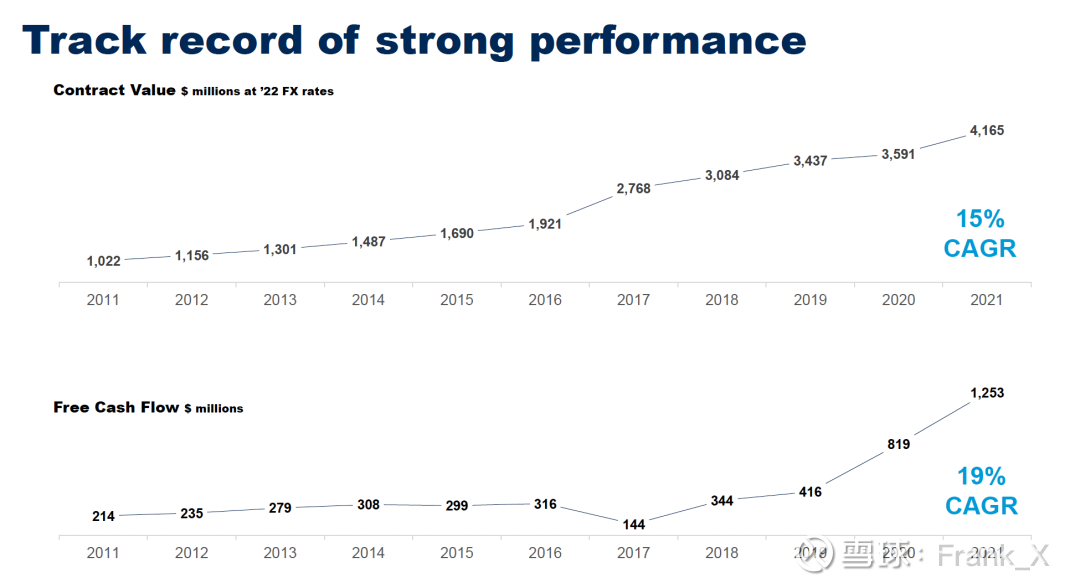

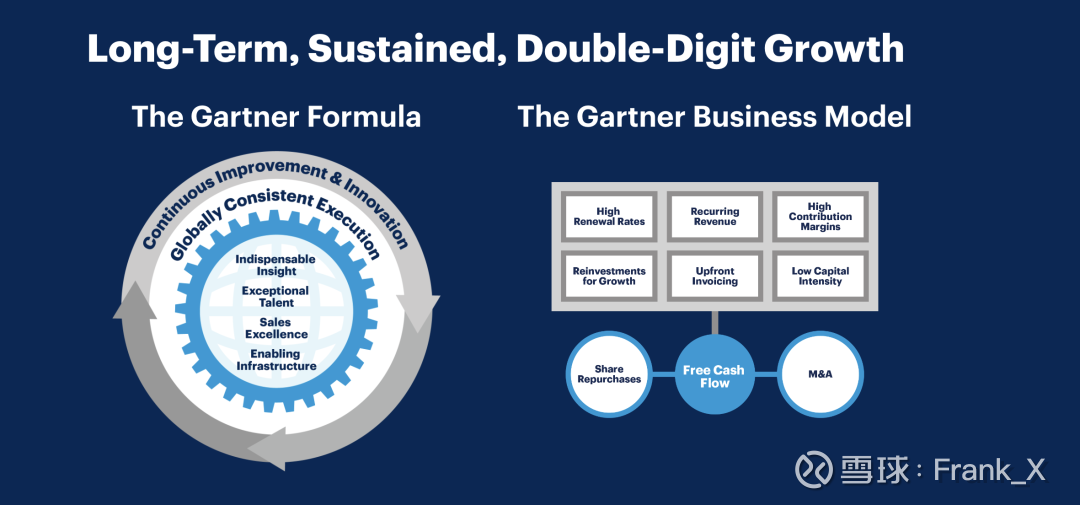

The annualized growth rate of the research business in the next five years is targeted at 12-16%, driving total revenue and contract value to maintain double-digit growth. Under the effect of economies of scale and operating leverage, profit margins are expected to continue to improve moderately, and free cash flow will also exceed the growth rate of net profit. The company further increased EPS through repurchases and increased returns to shareholders. The latest 22Q3 financial report shows that under the adverse impact of the exchange rate, the company’s revenue and contract value have achieved a year-on-year growth of about 15%, and the growth rate of EPS has reached 19%.

Gartner’s number of employees in 22Q3 increased by 18% year-on-year, mainly supplementing sales staff. The company’s explanation is that the recruitment progress in the past two years of the epidemic has significantly lagged behind the growth rate of the contract value. Now the expansion of recruitment against the trend is to match the performance growth, provide better services and increase sales appropriately. Subsequent hopes to maintain the growth rate of the contract value is 5-6% higher than the headcount growth rate. The price increase of products is expected to be controlled at 3-4% to cover the salary increase of employees brought about by inflation.

As of September 2022, YTD has repurchased $1 billion in stock. If calculated from the end of 2020, the repurchase has reduced the outstanding share capital by 10 million, accounting for about 11%. The company’s capital allocation strategy is to give priority to buybacks, supplemented by business synergy mergers and acquisitions, and rarely pay dividends.

Looking at past performance, Gartner’s performance is quite stable. Its business can also be regarded as a water seller in the IT industry, enjoying the dividends of the rapid development of the industry, and living a peaceful life with this signboard. However, affected by liquidity and the macro economy, the information industry will enter a down cycle, and Gartner’s business model will face greater challenges. At this time, it is more worthwhile to use a magnifying glass to test its resilience.

Research, like other SaaS, is all about retention and contract value growth. Subscription business has the advantages of light assets, pre-paid, low leverage, and strong economies of scale. The marginal cost is extremely low, the requirements for capital investment are not high, and the profit can be efficiently converted into free cash flow. Capital expenditures with large fluctuations are mainly divided into two parts: 1) sales manpower expenditures, which increase operating leverage through personnel expansion that matches performance growth; 2) research and development expenditures on product tools, including related mergers and acquisitions. The overall investment in these two areas is relatively controllable, and Gartner’s operation is also relatively stable, which can be confirmed by the 70% gross profit rate of the research business and the 80-90% customer retention rate.

I think there are two main flaws in the company’s fundamentals:

1) The essence of business is to provide C-level tracking research on industry and technology trends for the enterprise, and more to provide long-term, forward-looking advisory, rather than consulting to respond to specific needs and solve current problems, and rarely enter into delivery and implementation . The value of information provided by Gartner lies in its breadth and completeness, but its depth is insufficient. In the down cycle, enterprises mainly face the problem of cost reduction and efficiency increase, and the CTO’s IT expenditure will also be limited. The demand for such services does not seem to be rigid. The 12-16% growth rate given by the company should have taken into account the impact of industry penetration and cycles. I still have doubts about its ability to resist fluctuations. The sluggish 2023 is a good observation window.

2) Competitive landscape and core competitiveness. Gartner believes that its own competitiveness is reflected in its 40 years of deep cultivation of the industry’s accumulated advantages in database, talent pool and infrastructure capabilities, as well as its global customer relationship network and brand influence. These are of course its advantageous assets, but the exclusivity of its competitiveness seems to be mediocre, and it is difficult to widen the obvious status or even intergenerational gap with its opponents. When it comes to payment and clearing, Visa and MasterCard can be called a duopoly; when it comes to index compilation, S&P Global and MSCI have the only advantages. But when it comes to market research and information consulting, Gartner can only be in the first camp with players such as IDC, Forrester, F&S, and Nielsen. The competitive landscape of the industry is general, Gartner’s brand mind cannot be monopolized, and its industry status is not “The One”. Extending from IT business to other functions, Gartner also needs to prove its competitiveness to gain wider recognition, which is directly related to the ceiling of GBS business.

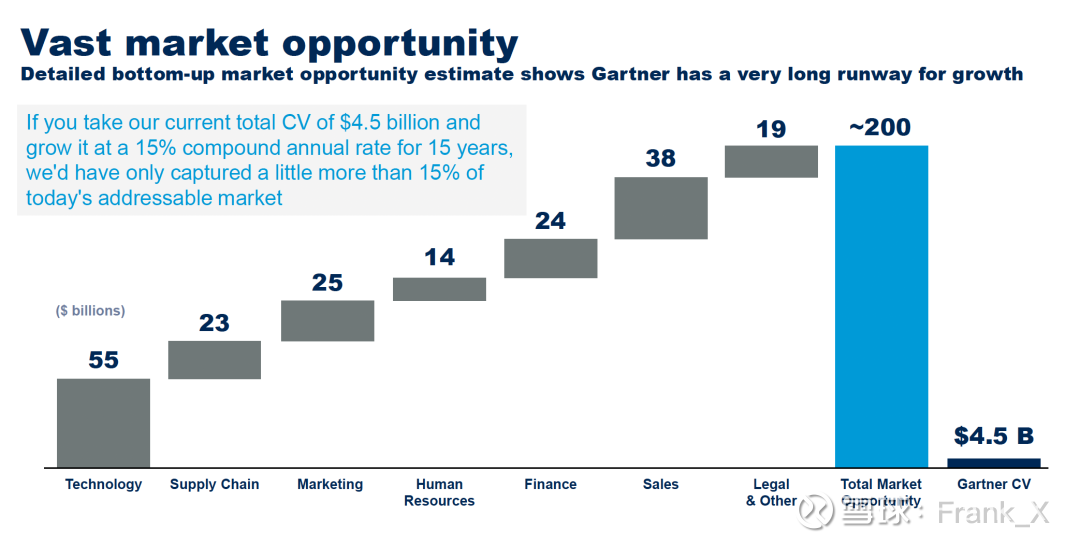

In addition to demand cycles and competitive landscape, Gartner seems to pay more attention to the improvement of industry penetration. Let’s take a look at the estimates of research experts on their own track: the total amount of TAM is as high as 200 billion US dollars, including the 55 billion IT market. At present, the company’s size of about 5 billion accounts for only 2.25%. Assuming that the business can achieve a compound growth rate of 15% in the next 15 years, the penetration rate will increase to more than 15%. I estimate that Gartner’s confidence in maintaining long-term medium and high-speed growth mainly comes from the prediction of the overall increase in industry penetration and concentration. On this basis, Gartner can continue to enjoy the beta of the industry’s structural growth without worrying about competing for alpha in the first camp. I still don’t quite understand this logic: If the next wave of technology such as AI and Metaverse cannot take over the mobile Internet and cloud services soon, can Gartner use the existing value proposition to get more customers to pay? If the rigidity of business needs is not enough, the differentiation advantage is not significant enough, and whether it is necessary to invest a lot of manpower to educate and convert customers, then the capital-light model mentioned above will not hold water.

The To B industry is separated by a mountain, and without in-depth first-hand research on the industry, the above problems may not be fully understood for a long time. But this does not prevent you from taking a closer look at Gartner’s performance in the headwind this year. It is best to drop a good price at the bottom of the cycle. I will buy a ticket and get on the bus to observe.

Statement of interest:

There is currently no $Gartner(IT)$ position, and trading plans are not ruled out in the next 72 hours. This article is only used to record phased thinking, not as a reference for investment advice.

There are 4 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/2233590663/240631718

This site is only for collection, and the copyright belongs to the original author.