Original link: https://xqrp.com/660491.html

“Balanced Scorecard” is a brand-new performance measurement method and a strategic management tool. Enterprises need to design different Balanced Scorecards according to market conditions, product strategies, and competitive environments.

What is the Balanced Scorecard?

The concept of the “balanced scorecard”, first introduced in 1992 in the Harvard Business Review, provides managers with a comprehensive framework for translating a company’s strategic goals into a set of interrelated performance measures. Far more than a performance measure, the Balanced Scorecard is a management system that enables companies to achieve breakthrough progress in key areas such as production, processes, customers and market development.

The Balanced Score Card (BSC) is an indicator system carefully designed according to the strategic requirements of the enterprise organization .

According to Kaplan and Norton, “The Balanced Scorecard is a performance management tool. It decomposes the strategic goals of the enterprise into various specific and balanced performance appraisal indicators system by layer, and provides information on the realization of these indicators. Carry out assessments at different time periods, so as to establish a reliable execution foundation for the completion of the strategic goals of the enterprise.”

Business Success = Strategy + Execution

The Balanced Scorecard is a powerful tool for strategy implementation. The Balanced Scorecard is not a one-size-fits-all tool. Different market situations, product strategies, and competitive environments require different Balanced Scorecards. Different business units need to design different balanced scorecards to match the organization’s mission, strategy, technology and culture.

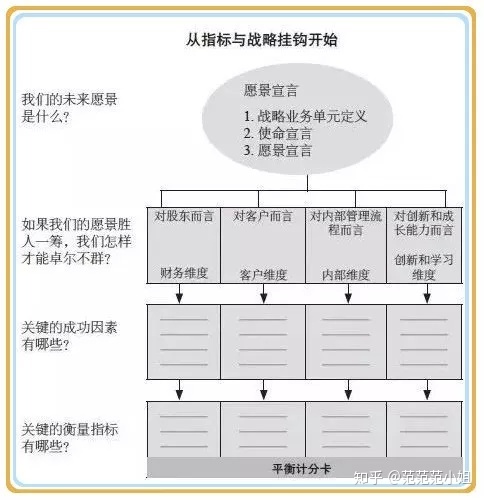

1. Prerequisites

- Vision : What kind of company a company wants to be. Where to go;

- Mission: How to achieve the vision How to go;

- Values: The company’s code of conduct.

2. Framework: “One Picture, One Card, One Table”

- Figure 1: “Strategic Map”

- One card: “Balanced Scorecard”

- Table 1: “Single Strategic Action Plan”

1) Strategic Map:

2) “Strategic Action Plan”

3. Implicit causal logic: the apple tree

- Soil: the ability, knowledge, system, and corporate culture of employees (only fertile soil can grow good crops);

- Trunk: capacity for internal operations (trunk transports nutrients);

- Prosperous: the customer benefits;

- Knot apples: financial results.

If you want to make money, you have to make customers pay. It starts with investing in employees, increasing capabilities, and improving internal operational efficiency with the right tools and systems, in order to provide customers with good products and services, satisfy customers, and finally achieve financial results.

4. Development Process

Typical project implementation steps: define scope → interviews/executive workshops (multiple rounds) → implementation → periodic review.

5. The Balanced Scorecard focuses on “balance”

The Balanced Scorecard contains five balances:

1) Balance between financial and non-financial indicators

The assessment of enterprises is generally based on financial indicators, while the assessment of non-financial indicators (customers, internal processes, learning and growth) is rare. Even if there is assessment of non-financial indicators, it is only a qualitative description, lacking quantitative assessment and lack of system. sex and comprehensiveness.

2) Balance between long-term goals and short-term goals of the company

The Balanced Scorecard is a management system for strategy implementation. If the implementation process of the Balanced Scorecard is viewed from a systematic point of view, the strategy is the input and the finance is the output.

3) Balance between outcome indicators and motivation indicators

The balanced scorecard takes the effective completion of the strategy as the motivation, and the measurable indicators as the result of target management, and seeks the balance between the result indicators and the motivation indicators.

4) The balance between internal and external groups of the enterprise organization

In the balanced scorecard, shareholders and customers are external groups, and employees and internal business processes are internal groups. The balanced scorecard can play the importance of balancing the interests of these groups in the process of effectively implementing strategies.

5) Balance between leading and lagging indicators

For example, financial indicators are a lagging indicator, which can only reflect the situation of the company in the previous year, and cannot tell the company how to improve its performance and sustainable development. The focus on the last three leading indicators enables companies to achieve a balance between leading indicators and lagging indicators.

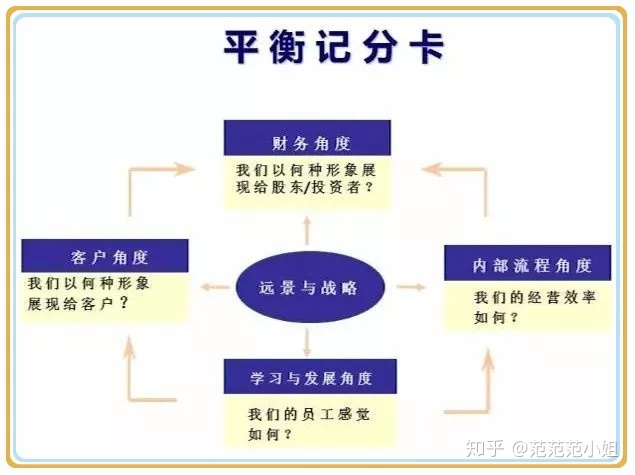

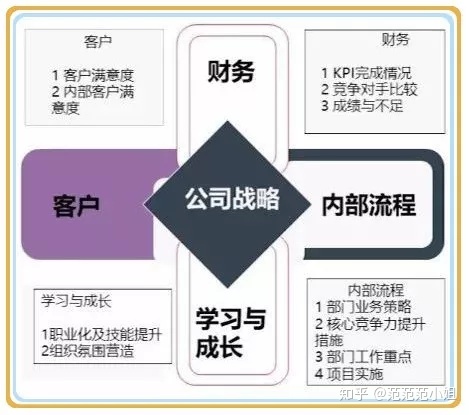

6. Designing the four dimensions of the Balanced Scorecard

The design of the Balanced Scorecard includes four aspects:

- financial perspective

- customer perspective

- Internal business process

- learn and grow

These perspectives represent the three main stakeholders of the company: shareholders, customers, and employees. The importance of each perspective depends on whether it is consistent with the company’s strategy.

1) Financial dimension

Financial performance indicators show whether a company’s strategy and its implementation and execution are contributing to the improvement of final business results, such as profits. However, not all long-term strategies produce short-term financial gains quickly.

Improvements and enhancements in non-financial performance indicators such as quality, production time, productivity, and new products are means to an end, not an end in itself.

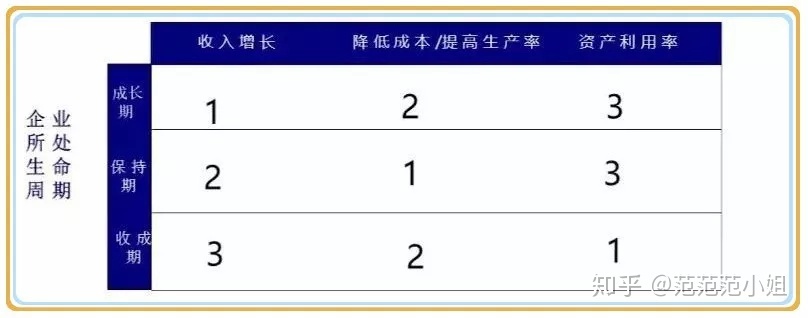

At different development stages of an enterprise, financial assessment indicators have different financial key indicators due to market environment and company strategy.

- Growth stage: income takes the first place;

- Retention period: After a period of development, reduce costs;

- Harvest period: The enterprise is developing very well, income and cost are not problems, they have been solved.

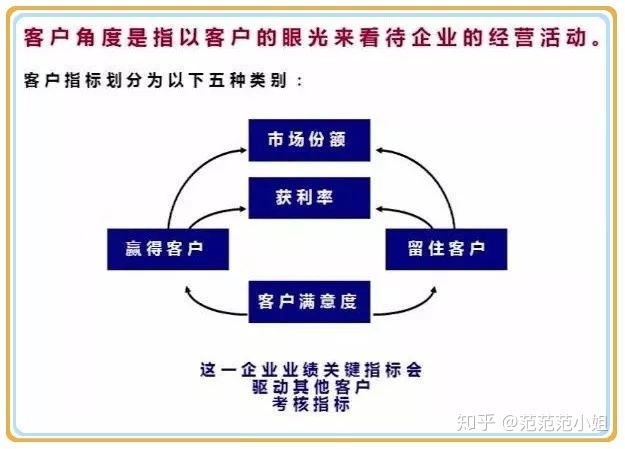

2) Customer perspective

Businesses should be target customers and target markets oriented and should focus on satisfying core customer needs rather than trying to satisfy all customer preferences. The customer’s needs are simply summed up in four points: correct, fast, cheap and easy.

The main content measured by customer-side indicators: market share, old customer retention rate, new customer acquisition rate, customer satisfaction, and profit margin from customers.

- Market share: how much share the company has in the market, KPI general market share;

- Profitability : the profitability of customers, how do we help customers succeed;

- Win customers: how to acquire customers, what is the cost of acquiring customers, how do we come and go, new customers, and the growth of new customers;

- Customer retention: the retention rate of old customers;

- Customer Satisfaction: Most Important. Whether customer satisfaction is 90% or 95%, is there a customer complaint rate, and how many complaints are there?

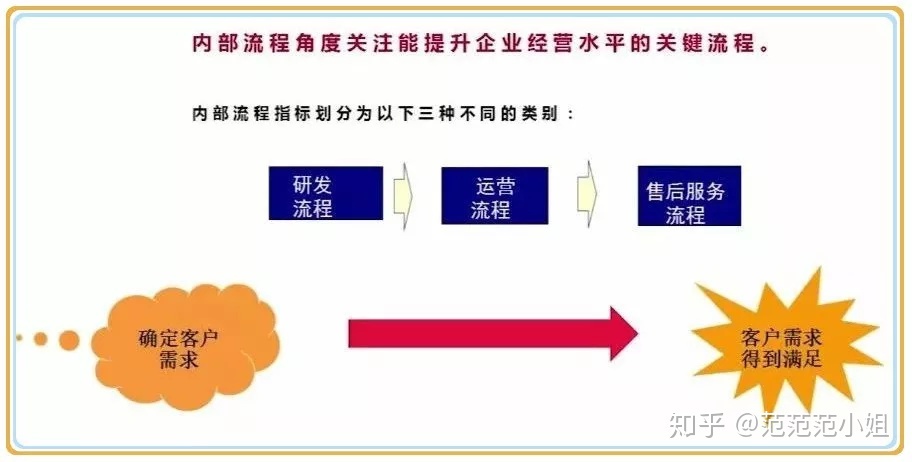

3) Internal process

Usually, the objectives and indicators of financial and customer aspects are formulated first, and then the objectives and indicators of internal process aspects of the enterprise are formulated. This sequence enables the enterprise to grasp the focus of management.

- R&D: new R&D projects, R&D cycle, R&D costs;

- Operation: procurement, production, design, quality, yield, pass rate, efficiency, etc.;

- After-sales service process: service response speed, problem solving time, etc.

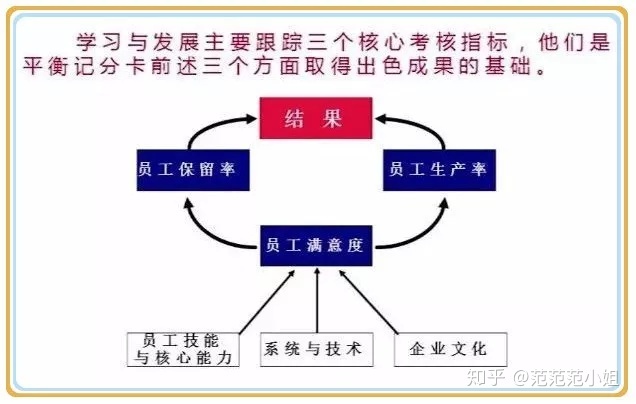

4) Learn and grow

The goal of learning and growth provides the infrastructure for the ambitious goals of the other three areas and is the driving force behind the achievement of excellence in all three aspects of the scorecard above.

- Employee retention rate: retention rate, turnover rate, voluntary turnover rate, and key employee turnover rate in the field of human resources ;

- Employee satisfaction: We conduct employee satisfaction surveys every year, in addition to core competency training, skill training, corporate culture creation, and new system construction;

- Employee productivity : sales per employee, number of orders per employee.

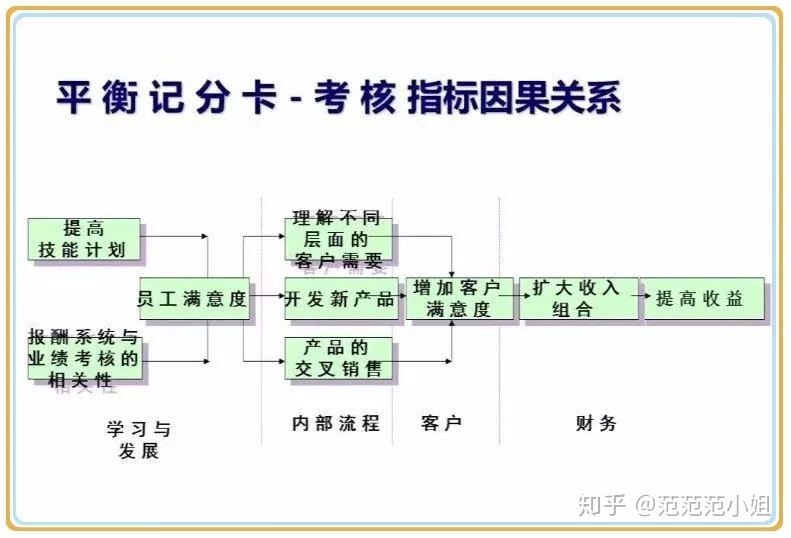

The causal relationship between the indicators is the causal relationship of the entire balanced scorecard, just like the apple tree diagram in the previous article, which is supported from bottom to top.

7 Implementation of the Balanced Scorecard

China has introduced the Balanced Scorecard since 2001, and some well-known enterprises have begun to try to use it. For example, Lenovo, China Mobile, and Ping An Insurance have been relatively successful, and some enterprises have failed in their application.

case

A company in Guangdong (with 2,000 employees and an annual output value of several hundred million yuan) uses the Balanced Scorecard as an evaluation system for the company. After a year has passed, the implementation of the Balanced Scorecard has not been successfully implemented, but has been received by the company. Lots of complaints and doubts. Someone said: “The original assessment method was like one rope. Now I want to use four ropes, why not just tie it tighter and make an excuse for less bonuses?”.

Reason for failure:

- Lack of high-level support, firm support;

- It is just that the goals are simply decomposed layer by layer (the decomposition of strategic objectives, the support and correlation of each dimension should be very strong);

- The employees do not recognize the company (there is no consensus);

- Simple as an assessment tool;

- Obstacles in information systems, particularly many forms, procurement of specialized software.

Suggest:

- Linking corporate strategy to performance management, above all the determination, drive and engagement of top management;

- Do not use the Balanced Scorecard only as a performance appraisal or KPI system;

- Expert guidance with experience in implementing the Balanced Scorecard;

- Effective IT systems to reduce administrative and manual operations and increase communication and transparency;

- Balanced scorecard managers must be promoted to a strategic level, making them the partners of the top management of the enterprise to ensure the successful implementation of the balanced scorecard;

- Infiltrate the BSC concept (balance) into the company’s existing performance management system;

- When designing performance appraisal, refer to the four dimensions of BSC;

- Use of BSC in senior management.

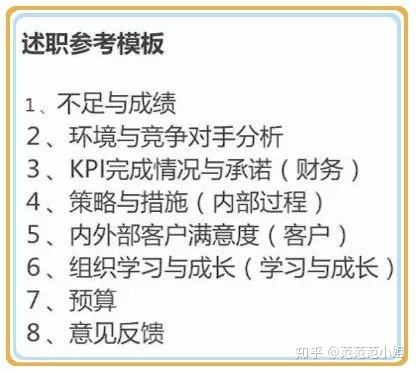

Huawei also uses the Balanced Scorecard for middle and senior management. When they do their debriefing, they will mention the four dimensions of BSC:

-

- Achievement of financial targets

- customer satisfaction

- Departmental business strategy (internal process)

- Organizational Learning and Growth

The Balanced Scorecard is one of the tools that may be used in strategic management. In Huawei, the most important thing is the system of strategic thinking and systematic management. In Huawei’s 2017 annual report, there is a separate presentation titled “Strategy to Execution”, which highlights the role of Huawei’s DSTE (Development Strategy to Execution) management system:

-

- Support the realization of the company’s strategy and business objectives;

- Ensure the effective implementation and implementation of company strategies.

See the original text: Understand at a glance: Balanced Scorecard BSC Operation Guidelines and Cases

This article is reprinted from: https://xqrp.com/660491.html

This site is for inclusion only, and the copyright belongs to the original author.