If you read this article and understand its essence and implement it resolutely, you can at least double or even double your investment income in the next few years.

Those who are familiar with me know that my understanding of investment is that there are two important things, one is to accurately grasp the industry trend, and the other is to understand the art of valuation. Grasping the industry trend requires us to invest in the rising cycle of the industry on a good track of high growth. The understanding of the art of valuation requires us to choose the time and intervene when the valuation is suitable or even cheap.

From the perspective of the world, the pharmaceutical industry is a high-quality track worthy of lifelong participation. There are many superheroes in it. The fear of disease and the pursuit of health are the common goals of all mankind. In particular, the prospect of my country’s pharmaceutical industry is infinitely bright now. First, aging is the most irreversible thing in my country in the next 30 years, which means that the pharmaceutical industry is the most certain investment opportunity with expanding demand. Second, the status quo of the development stage of my country’s pharmaceutical industry determines that there is huge room for growth. In the future, there will be ten times or even twenty times the number of shares in the industry. Whether you can seize it depends on your ability.

From the perspective of timing alone, from the perspective of valuation art, the Internet industry and the pharmaceutical industry have reached the hitting zone where they can participate in heavy positions. Their industry indexes have fallen by 60 to 70 percent. The Internet reference is 156605 and 513050, and the pharmaceutical stock reference is 513060. The Internet has the disadvantage of anti-monopoly policy, and the pharmaceutical industry has the disadvantage of volume procurement. They have a lot in common, but from the perspective of industry trends and industry prospects, the Internet industry is more like a mature industry. The ceiling is very close, and the growth space is limited. The pharmaceutical industry is different, both from the perspective of short-term demand and from the development stage of my country’s pharmaceutical industry, it has unlimited potential and huge space.

From the perspective of industry trends and industry prospects, 513060 has a high probability of winning 513050. Of course, this is from a long-term cycle, such as more than ten years.

Regarding the development prospects and space of the pharmaceutical industry, I think everyone’s views should be very consistent and there is no disagreement, so the focus should be on the understanding of the art of valuation, which is timing. Is now the best time to plan?

Let me take the private and public offerings of major investors in this industry as an example. Their positions and earnings are very representative.

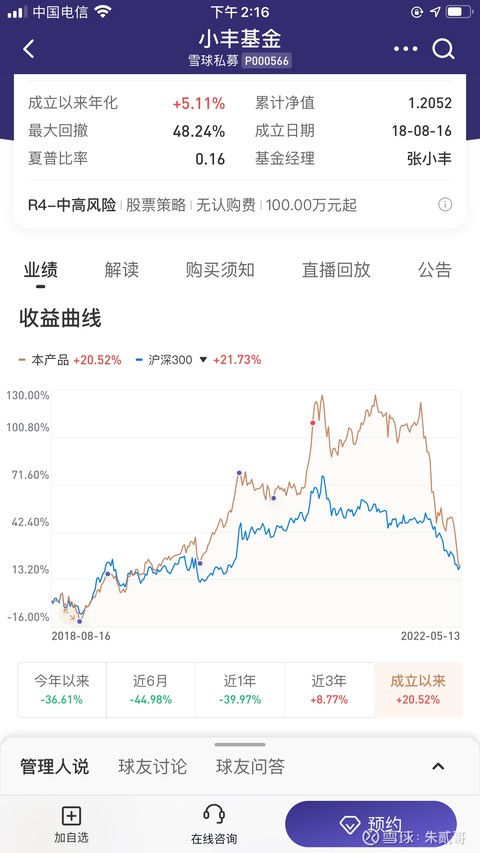

The private equity firms focusing on innovative drugs on Snowball include Huang Jianping, Qingqiao Sunshine and Xiaofeng. The trends of their products are as follows

Jianping Yuanhang has withdrawn 57% from the high point, basically falling back to the starting point of the pharmaceutical bull market. His product has a good time and a long time, and the total income seems to be okay, but it can be bought in the past year. Sadly, a retracement close to 60% is not something everyone can afford. This buddy is very extreme. He may have deep research on innovative drugs, but he will not talk about Chinese medicine, because I am also optimistic that Chinese medicine has been blocked by him for a long time haha.

The net worth of Qingqiao Sunshine products has returned to the starting point of this bull market in pharmaceutical stocks. To be honest, their professional knowledge of pharmaceutical stocks is indeed very strong. I am very grateful for their articles and opinions. The income situation of an investor with such strong medical expertise, especially such a large drawdown of 60%, is really worth thinking about. Is it really reasonable to invest at the wrong time? A few days ago, I read the article they wrote about the valuation of innovative drugs, and they wrote very well. In 2020, the valuation of innovative drugs was more than 40 times ps at the craziest time. Now many of them are lower than 10 times ps, which is a normal and reasonable valuation. Even if it is 15 times ps, it is indeed time to be very undervalued and worth a heavy position. However, the valuation of more than 40 times ps is so obvious that it is so foamy. Why not lighten up the position? ps valuation? To be honest, I really don’t understand those who promote untimely propaganda. If the whole market is crazy, crazy, frothy, and frothy, wouldn’t it reduce the position? If the market is extremely pessimistic and extremely undervalued, shouldn’t it be overweight? Is it really that difficult to choose the right time? It is really difficult to make accurate tops and bottoms, and it is not difficult to judge relative highs and lows. There are too many indicators and valuation methods.

Xiaofeng Fund has the smallest retracement among the three, with 48%, but the last wave of the medical bull market did not rise as much as the previous two, which may be related to his stock selection. He is also very professional in medicine, especially innovative drugs, and I often benefit from reading his articles.

In terms of expertise in the pharmaceutical industry, the three of them are estimated to surpass 99.9% of the golfers on Snowball, just as Yunmeng and Guzidi outperform most golfers in terms of expertise in the banking industry. From this perspective, they are worthy of our study and respect. Anyway, I often read their articles and am very grateful.

But they don’t seem to have such a strong understanding of investment, especially the understanding of the art of valuation. It is worth thinking about why many industry experts and industry experts are not good at investing. An understanding of valuation, perception of the market, and insight into human nature are also important.

The above is the situation of several private equity companies, and then look at the public offering representative Ge Lan.

Although Sister Ge has also undergone a huge backtest, it is still relatively good in terms of overall returns and drawdowns, especially in the case of the decline of the pharmaceutical industry in the past year or so. I don’t pay much attention to other public offerings in the pharmaceutical industry, and it seems that the drawdown is also quite large.

The picture above shows Sister Ge’s main holdings now. In her impression, she used to like medical services such as Aier Ophthalmology, Tongce Medical, Changchun Hi-Tech, and CXO WuXi AppTec, Tigermed, Asymchem, etc. Although she also holds Hengrui Medicine, but there are not many innovative drugs in general, especially Hong Kong stock innovative drugs.

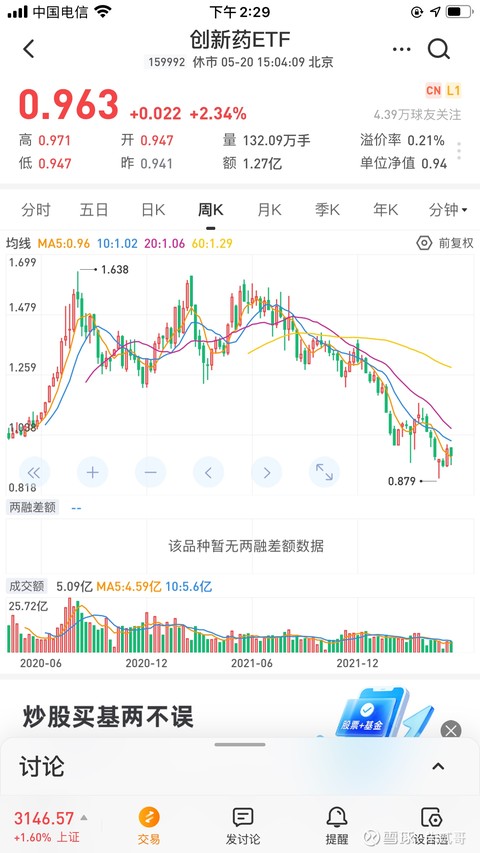

The picture above shows the trend of innovative drug ETFs and their top ten holdings.

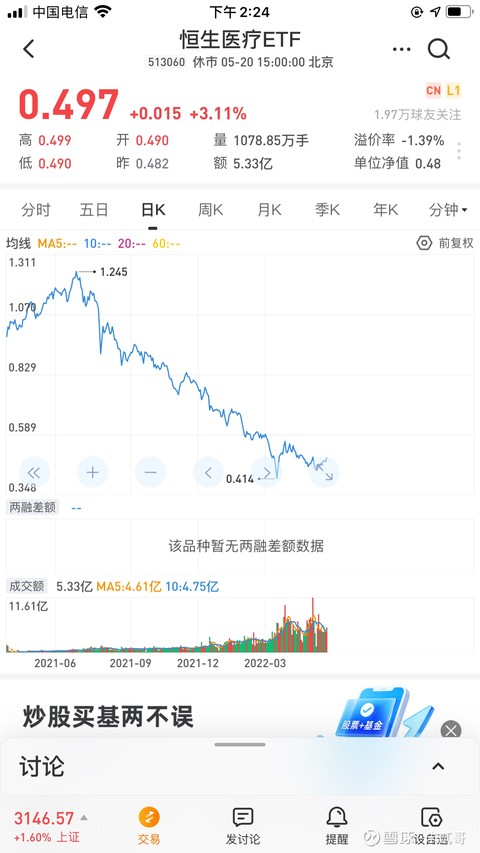

The picture above shows the trend of Hang Seng Medical ETF and its top ten holdings.

Above we briefly talked about private equity and industry ETFs. What do we want to explain? That is now the industry is probably in an underestimated range and the necessity of timing. Looking at the highs and lows of industry valuations through the pullbacks of major industry investors is only one perspective of valuation understanding. Falling too much is not necessarily an undervaluation, but may also be value destruction, such as education and training. Needless to say about the prospects and growth space of the pharmaceutical industry, now everyone is most worried about policy factors such as insufficient medical insurance and purchasing in large quantities. Of course, this will suppress the overall valuation of the industry, but it will not kill the industry, and we must also take into account the industry. The healthy development of my country’s pharmaceutical industry will not stop, and the truly outstanding enterprises will definitely come out. This is inevitable, and there is no need to worry too much.

The pharmaceutical industry is actually very large, and there are many subdivisions. Let’s briefly summarize it below. Sort by industry prospects and growth space.

CXO: WuXi AppTec, Tigermed, Asymchem, Pharmaron

Medical services: Aier Ophthalmology, Tongce Medical, Changchun High-tech

Innovative drug A shares: Hengrui Medicine, Betta Pharmaceuticals, Fosun Pharma

Innovative drug Hong Kong stocks: BeiGene, Innovent Bio, WuXi Biologics

Medical equipment: Mindray Medical, Yuyue Medical, Kaili Medical

Traditional Chinese Medicine: Tongrentang, Jichuan Pharmaceutical, China Resources Sanjiu

Blood products: Shanghai Laishi, Hualan Bio, Boya Bio

Internet healthcare: JD Health, Ali Health, Ping An Good Doctor

Pharmacy: Yifeng Pharmacy, Dashenlin, Yixintang, Common People

There are so many sub-fields that I can think of for the time being, and others are welcome to add. Among them, I am most optimistic about cxo, innovative drugs, medical services and medical devices.

Five times the growth space: WuXi AppTec, Hengrui Medicine, BeiGene

Tenfold growth space: Innovent Bio, Betta Pharmaceuticals, Ali Health

WuXi, Hengrui, and Baekje are the hope of the current pharmaceutical industry in my country. They have their own advantages and disadvantages, because they are large enough, and the five-fold space is more certain. It may take a long time to verify whether they can go tenfold. It has been verified for ten or even twenty years.

Cinda, Betta, and Ali are healthy and healthy. Innovent and Betta are mainly innovative drugs in the field of anti-cancer. The flexibility is ten times larger. It is possible within ten years. Innovent now has seven commercialized innovative drugs, and there will be seven or eight companies in the next four to five years. With a planned revenue of 20 billion yuan, Betta Pharmaceuticals currently has three commercialized innovative drugs. By next year, there may be five. There will be about 10 in the next few years, and more than a dozen have been ind. There are more than 40 in the future. Re-research production lines, the company plans to generate 8 billion revenue in 2025. If the next big bull market for innovative drugs comes again in the next few years, let alone 40 times the ps valuation, if it can have a 20 times ps valuation, both Cinda and Betta have the possibility of hitting ten times the stock, at least three or five times. The possibility is great. It mainly tracks whether the follow-up innovative drugs can meet expectations. Now talking about the five-fold or even ten-fold increase of Innovent Bio and Betta Pharmaceuticals in the future, many people may dismiss me and call me bragging B. In fact, the innovative drug industry is developing rapidly and is flexible enough to be imaginative enough, and the innovative drug bull market will come. Everything is possible. Let’s just talk about Betta Pharmaceuticals. In the one year from 2019 to 2020, how fundamentally has the company’s fundamentals changed, but the stock price has risen from less than 27 to more than 160, and then the company is Whether it gets better or worse, in fact, the fundamentals are getting better and better, but the stock price has dropped from more than 160 to 40. Let’s talk about Cinda Bio, it took less than two years to rise from 14 to more than 100 yuan and then fell back to more than 18 yuan. Therefore, innovative drugs are highly volatile and elastic. The bull market of the last wave of innovative drugs was more of an expected hype, and the next bull market may require the realization of performance. It is very important whether their innovative drugs can meet expectations in the later stage. The properties of innovative drugs are like this, so when the next bull market comes, don’t make a fuss if it will increase five or six times or even ten times in just one or two years. The stock market is like this. Sometimes the performance has increased several times in a few years. The stock price may still not rise sideways. Once it breaks out, it may rise many times in just one or two years. This is why many industry experts fail to do well in the stocks of companies in their industry. They lack understanding of the market, insight into human nature, and the art of valuation.

It may be difficult for Alibaba Health to take into account the current market value of ten times the stock, but five times is very likely. It mainly depends on the future development of Internet medical care. I also know that JD Health has more advantages, but JD Health’s current market value is definitely not as flexible as Ali. Healthy big. Yifeng, Yixintang pharmacy chain may still have opportunities for industry concentration in the next three to five years. After a longer period of time, there is a high probability that it will not be able to beat JD.com and Ali Health. This is one of the reasons why I am optimistic that Ali Health will have a chance to hit ten times the stock.

This is generally the case. If you focus on certainty, focus on leading companies such as WuXi AppTec, Hengrui Pharmaceutical, and BeiGene. If you focus on flexibility, focus on targets with higher odds such as Innovent Bio and Betta Pharmaceuticals. If you are willing to take the risk of thunderstorms in individual stocks, it is best to choose industry ETFs such as $Hang Seng Medical ETF (SH513060)$ and $Innovative Drugs ETF (SZ159992)$ . Buying ETFs may be the best choice for most amateur investors.

I just bought some Betta Pharmaceuticals recently. I originally made short-term speculation from the logic of innovative drugs oversold and rebounded. After in-depth research, I found that it is also a good target for long-term holdings. I read a lot of old Betta fan posts over the weekend. I feel that in the long run, Betta has five times or even ten times the potential. When you have time, I will write a separate article on my understanding of Betta Pharmaceuticals.

My focus is on a wide range of industries, and I focus more on capturing investment opportunities from two aspects: entrepreneurial trends and the art of valuation (including market and timing). Others that have long-term investment value to be tracked are the new energy vehicle industry chain and photovoltaic industry chain, but I feel that their valuations are still a bit expensive. I hope that as the US stock market plummets, especially Tesla’s halving, new energy can be smashed. It would be great if it could fall like the Internet and innovative drugs. It is definitely a good opportunity to buy the bottom.

This topic has 8 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/2299425930/220607504

This site is for inclusion only, and the copyright belongs to the original author.