Is there a kind of stock that can be ignored after buying it, and can realize retirement by means of fixed investment? In 2017, I got to know about the Yangtze Power at that time. It has the four largest hydropower stations in China, and the other two giant power stations (Wudongde and Baihetan) under construction will also be included. That is to say, the business of Yangtze Power is very pure, that is, the pure hydropower business. This kind of business is relatively simple. As long as the annual inflow of water remains stable, the power generation can remain stable; and the cost of hydropower is basically depreciation, amortization and operating expenses, and the gross profit margin can remain stable; with strong cash flow, the company Huge financial expenses will also decrease year by year. That is to say, the company’s profitability will remain stable for a long time. Under the guidance of the national dual-carbon strategy, hydropower will definitely be used first. At the same time, as the upstream cascade hydropower stations are gradually put into use, the power generation of these hydropower stations will also increase. According to the company’s dividend ratio, as long as the stock price is low enough after the dividend, you can continue to use the dividend money to continue to buy, thereby further increasing the income. $Yangtze River Power(SH600900)$

When in 2017, you can only read the annual reports before 2016, and it is normal to have this kind of thinking. From the income statement, the investment income of 1.334 billion accounted for only 6.3% of the net profit of the entire listed company of 20.94 billion. Although the non-operating income is as high as 2.912 billion, it can be seen from the financial notes that this is basically from the VAT rebate. The high tax rebate ended in 2016, and it became very low after 2017, which does not constitute a major change factor. At the same time, the company’s investment assets are mainly available-for-sale financial assets of 7.115 billion and long-term equity investment of 13.1 billion, which is relatively low compared to operating assets of more than 200 billion. The company’s financial expenses are as high as 6.679 billion, accounting for a large proportion of profits, mainly because the company’s interest-bearing debt is relatively high. From the balance sheet, there are 16.3 billion short-term loans, 26.85 billion long-term loans and 27.66 billion bonds payable. On the surface, there are only 70.8 billion interest-bearing debts, but in fact, through the notes on long-term payables, 52.69 billion of payable projects Payments are also interest-bearing. Although the interest-bearing debt is so high, the company’s net operating cash flow is as high as about 39 billion yuan. If no dividends and no other investments are made, the interest-bearing debt of more than 120 billion yuan will be repaid in a few years. Finally, from the perspective of the company’s revenue structure, the four major hydropower stations contributed almost all of the revenue. Therefore, it was correct to judge Yangtze Power as a pension stock at that time.

Time comes to 2022, and we looked at the annual report of Yangtze Power in 2021 and found many changes. This change seems to be somewhat different from our initial setting, and Changjiang Power is not absolutely stable, because there are more and more investment projects, and the fluctuation of investment income will cause certain disturbances to Changjiang Power’s net profit.

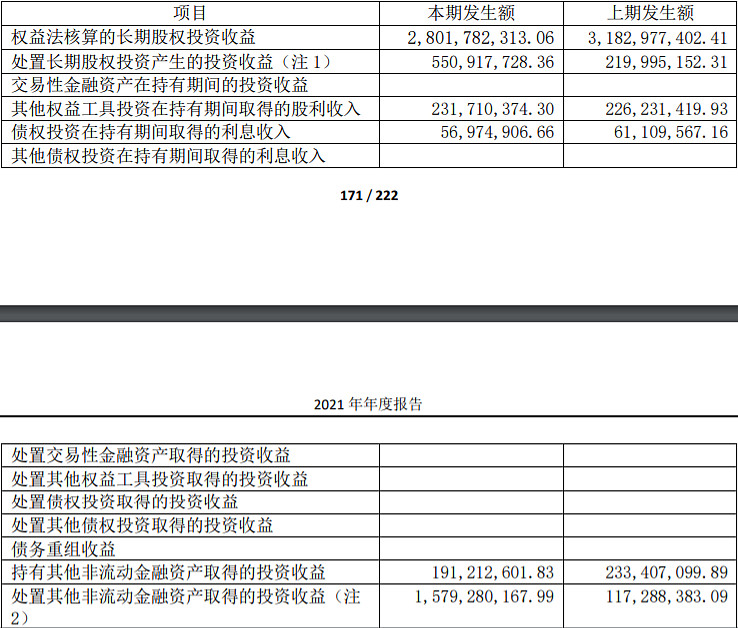

In 2021, Yangtze Power’s investment income will be 5.426 billion, accounting for 20.5% of the company’s net profit of 26.49 billion. Investment income has become an important part of the company’s net profit. From the perspective of the balance sheet, the company’s long-term equity investment as high as 60.72 billion accounts for the proportion of the company’s assets can not be ignored. In five years, the balance of long-term equity investment has increased by nearly 50 billion. If the increase in other equity investment instruments, debt investment and other non-current financial assets is added, the increase in investment assets in five years has exceeded 50 billion. In easy-to-understand terms, Yangtze Power is no longer a pure power generation company, but a company that pays equal attention to both power generation and investment.

Further analysis of the source of the company’s investment income, 2.8 billion of the 5.426 billion is mainly generated by the profits of the invested companies, while 550 million is from the investment income generated from the disposal of long-term equity investments. The specific form is to sell the corresponding stocks in the secondary market. In 2021, some stocks of Sichuan Investment Energy and Shanghai Electric Power will be sold. In 2021, these two stocks will have good gains. By significantly increasing its holdings of Guiguan Power, Changjiang Power has become the third shareholder of Guiguan Power, resulting in an investment income of up to 1.579 billion. This income is only the income generated by the change in the valuation method of assets. The returns generated by the sell-off after the stock rises and the change of the latter pricing method are not very sustainable and are more volatile. The stable part of the investment income depends on whether the profits of these joint ventures and joint ventures are stable.

It is worth mentioning that although Yangtze Power conducts trading operations in the secondary market, it is all involved in the power field, not cross-border investment like Yunnan Baiyao. However, from a structural point of view, we have not invested in stable assets such as hydropower on a large scale. By the end of 2021, it has invested a lot in thermal power. The investment balance of SDIC Power is 11.8 billion and Shanghai Electric Power 1.3 billion is almost all thermal power business, Hubei Energy 8.8 billion, Guangzhou Development 3.9 billion and Shenergy 3.6 billion also have a large part of their assets in thermal power business. When coal prices rise sharply in 2021, SDIC Power and Shanghai Power will still be profitable, and they are considered high-quality assets. However, the corresponding thermal power business of Hubei Energy, Guangzhou Development and Shenergy Co., Ltd. fell into losses. In particular, the gross profit margin of the thermal power business of Guangzhou Development has reached -9.45%. I really don’t understand why the company invested in such a stock. Of course, there are some companies with good potential, such as Hubei Qingneng, Sichuan Investment Energy, and Guiguan Power, which have a good proportion of Qingjian energy. There is also a Yunnan Huadian Jinsha River Middle Reaches Hydropower Development Co., Ltd. with an investment of 5 billion yuan, accounting for 23% of the equity. From the perspective of development planning, there may be several large hydropower stations. Investing in this business is based on the understanding of the power industry. The probability of error is still not large, but it may bring certain fluctuations.

From the perspective of revenue structure, the company has added billions of dollars in other industries since 2020, and will continue to increase in 2021. Judging from the company’s annual report, there is no specific indication that by checking the changes in assets, it should be the increase in revenue from the acquisition of Peruvian assets. Other industries should correspond to the electricity distribution and sales business, and other possible overseas hydropower businesses. These two assets are also relatively high-quality and stable assets. Looking forward to the future, the injection of Wudongde Hydropower Station and Baihetan Hydropower Station is already in the process, but the corresponding assets have not yet been priced. According to past practice, shareholders of listed companies cannot suffer losses.

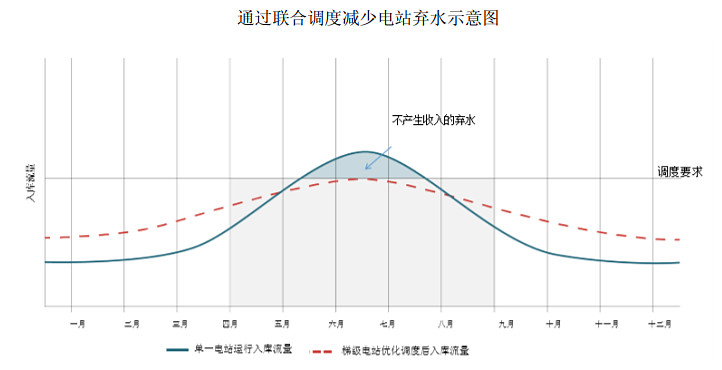

That is to say, in the near future, Yangtze Power will be composed of the six largest hydropower stations in China, plus power distribution and sales in Peru and a small amount of hydropower business, which is the basic disk of Yangtze Power. These businesses are less volatile, but are subject to changes in power generation due to changes in upstream water. However, with the completion of the upstream cascade development, the utilization of water energy will be more efficient! The principle can refer to the figure below, and for a more detailed explanation of the principle, you can also refer to this video . Under the circumstance that the basic stock is kept, the company will have a large amount of cash flow back, and on the one hand, it can distribute dividends to shareholders. From the perspective of the company’s fixed assets depreciation, the main assets can be depreciated within 50 years, and hundreds of billions of fixed assets will gradually be converted into cash flow, so the company’s net operating cash flow is far more than the net profit. While maintaining a good dividend ratio, gradually reduce the asset-liability ratio to further reduce financial costs. This basic logic has not changed. But we need to keep track of his investment business, and with the completion of the company’s acquisition of two other giant power plants, the company will have more cash flow and more cash for investment. As long as no major mistakes are made in investment and the fundamentals can be maintained, Yangtze Power is a typical pension stock.

It is not easy to analyze and organize. You need your likes, attention and encouragement. Follow me to get more information!

There are 30 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/8743289683/220737638

This site is for inclusion only, and the copyright belongs to the original author.