This article is at the invitation of a friend, and combined with the company’s annual reports over the years to sort out and analyze “Muyuan Shares”. I took the time to complete the writing of this long article this week. I hope this article can be a reference for all those who already hold or plan to hold the company’s stock.

The following analysis is my personal opinion and does not constitute investment advice

Henan Muyuan Food Co., Ltd. was listed on the Shenzhen Stock Exchange on January 17, 2014, and the IPO issued no more than 70.68 million shares. After nearly 9 years of development, the company’s total share capital is 5.322 billion, and the total market value has increased from about 6 billion before to the current 258.3 billion, an increase of about 43 times in 9 years, which can be described as an authentic “big bull stock”.

Industry basics

huge demand

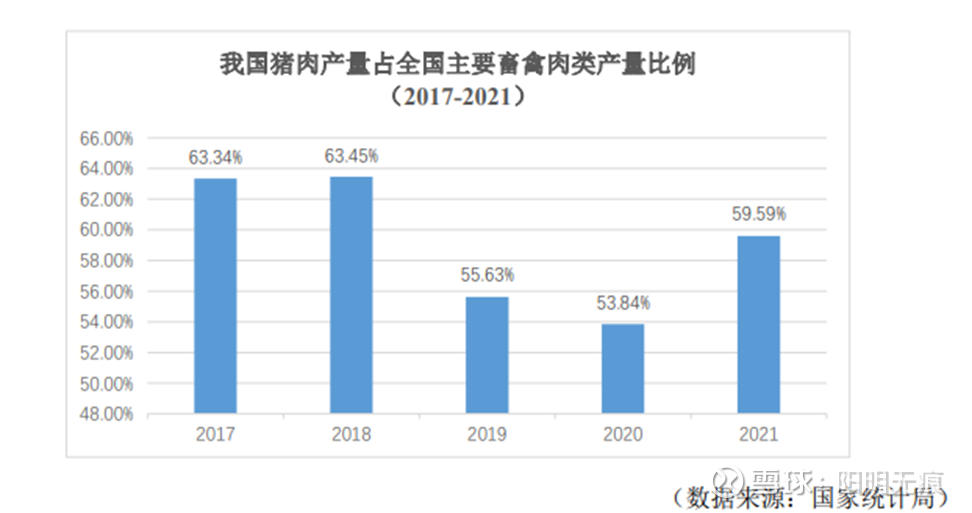

my country is the world’s largest pork production market and the world’s largest pork consumption market. According to data released by the Organization for Economic Cooperation and Development and the United States Department of Agriculture, my country’s pork consumption accounts for about 46% of the world’s pork consumption, and China’s per capita pork consumption is about twice the world’s per capita pork consumption. Pork is the most important source of animal protein for Chinese people, and it has long been the dominant player in meat consumption in my country. According to data from the National Bureau of Statistics, my country’s pork production in 2021 will be 52.96 million tons, accounting for 59.59% of the main livestock and poultry meat production.

According to the above content, it is not difficult to know why the price of pigs will make headlines almost every day when pork is rising wildly in 2020. The ups and downs of pig prices will drive CPI (resident consumption index) fluctuations. Compared with agricultural and sideline products such as beef, mutton and eggs, the weight of pork in the CPI is relatively high, and the large fluctuations in pork prices have a greater impact on the CPI. According to the data released by the National Bureau of Statistics, in the first three months of this year, the national pork price dropped by 41.6%, 42.5% and 41.4% respectively compared with the same period of the previous year, driving the CPI to drop by about 0.96, 0.95 and 0.83 percentage points respectively. The proportion of students in the daily life of residents. This is also the reason why the country releases pork to the market when live pigs are nervous, and stores pork when it is down.

In addition, through the above paragraph, we can also know that the demand side for the industry in which the company is located is huge, and it can be said to have unlimited potential (compared with other poultry, I think that there may only be “eggs”) can fight with one), but we can also know from the above picture that when the price is high (the proportion of pork dropped by about 5 points, in a market as large as China, the drop of 5 points is actually converted into The tonnage is also a very scary number.) Everyone will still turn to other poultry. For example, in 20 years, when the price of pigs was close to the highest level of about 45 yuan, classmate Yangming and I turned to beef. For the same price, why not choose beef that is usually reluctant to eat, why not do it). It’s important to keep this in mind, as it relates to our analysis of operating income later on .

cyclical

my country’s pig breeding industry is cyclical, and the price of pigs fluctuates significantly, generally 3-4 years as a cycle.

The development path of the pig industry cycle is generally as follows: first, the rise in pig prices drives farmers to make profits. With the expansion of profits, farmers will supplement the pigs. In addition, the price of piglets will increase. As a result, the supply has also increased sharply, and finally the price of pigs has begun to fall. It usually takes about 3 months for the price of pigs to rise to profit, and it takes about 3 months for the profit to rise to the increase in the amount of supplementary pens, plus the breeding and production cycle of about 10-11 months, about 1.5 to 2 years. The up cycle is over. The decline cycle is analogous, and it is estimated that the cycle time is 3-4 years.

Since 2000, the national pig breeding industry has experienced the following fluctuation cycles: 2002 to 2006, 2006 to 2010, 2010 to 2014, and 2014 to 2018 are a complete cycle, and there are also several large cycles. small cycle. In 2019, due to the superposition of factors such as the pig cycle and the African swine fever epidemic, the number of live pigs dropped, and the price of pigs showed a trend of low before and high. In 2020, the industry’s production capacity shows a gradual recovery trend, but due to the large reduction in production capacity in the early stage, the supply of live pigs is still in short supply, and the price of live pigs is basically maintained at a high level. In 2021, the industry’s production capacity will basically recover, the market supply will rebound significantly, and the price of live pigs will show a downward trend.

Supply side controllable

In addition to production facilities, pig animal husbandry is divided into two main categories according to cost: breeding pigs and feed, because I personally came out of the countryside. When I recalled the scene of feeding pigs at home when I was a child, it was a house built with brick walls. It is enough to feed 2-3 pigs, and then just use the leftovers to feed. I liked it very much when I was a child because I knew this was one of the sources of my pocket money. However, piglets and sows (breeding pigs) are purchased from outside, which means that for ordinary pig farmers, breeding pigs or piglets are the supply side. In order to speed up the growth cycle of pigs, it is necessary to buy nutritious feed for feeding. Therefore, feed is also one of the supply ends.

The 2014 prospectus of “Muyuan Shares” disclosed that the company is fully capable of independent production of breeding pigs, and also has mature formulas for self-production in terms of feed.

1. Breeding pigs: In terms of breeding pigs, the company has established a propagation system of great-grandfather-grandfather-parental-commercial generation, and breeds breeding pigs and commercial pigs by itself.

2. Feed: In terms of feed formula, the company’s feed formula adopts an advanced net energy evaluation system based on the specific efficiency of nutrient utilization and a truly digestible amino acid model, which accurately measures the content of effective protein in the formula and improves the digestion and utilization of feed. Rate;

According to the disclosure in the annual report, feed accounts for nearly 60% of the total cost, while the cost of piglets and fattening pigs is very low. There are advantages.

By sorting out the basic situation of the industry (demand side, supply side and cyclicality), we can see that the company is in a huge industry blueprint. Pork accounts for a very high proportion of Chinese people’s poultry consumption, but it is also relatively sensitive to prices. Spend. This industry is obviously cyclical, and operating profit or gross profit margin will be greatly affected by industry cyclicality. The company has a completely controllable advantage on the supply side, especially for breeding pigs, which is why feed accounts for about 60% of operating costs.

After analyzing the supply side and the demand side, we have to look at the quality of the company’s operating income and net profit. Mainly based on the comprehensive analysis of the company’s three major financial standards.

Basic financial report

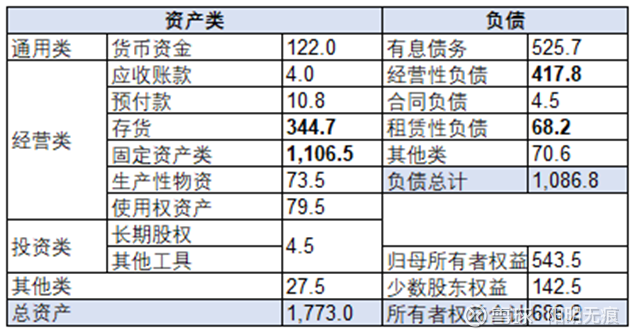

According to the 2021 annual report, the balance sheet is simplified as shown in the figure below. According to the contribution to net profit, it is mainly divided into operating and investment assets. Investment assets: After the merger, the company’s investment is very small, but this does not mean that the parent company’s investment in the subsidiary is small. According to the corresponding items in the parent company’s balance sheet, the parent company’s investment in subsidiaries is around 76 billion yuan (long-term equity investment + other receivables). It’s not surprising at this scale. However, because this piece is mainly invested in subsidiary/grandson companies, the net profit will be reflected after the merger, and according to the disclosure in the financial statements, this piece will not generate any income in 2021, but will generate about 10 million yuan. Losses (all associates), because the amount involved is relatively small, this section will not be elaborated.

Compared with 2020, the simplified assets and liabilities in 2021 have the following findings:

1. Inventory scale : reached 34.47 billion, an increase of about 13.5 billion compared with 2020. The increase is mainly concentrated in the production of consumable items (about 97% increase), and the competitors have accrued inventory depreciation. In this case, “Muyuan Shares” did not accrue inventory.

Because the inventory is converted into operating costs (material + labor + depreciation, etc.) as long as it is sold according to financial accounting, the following data shows that the company’s inventory and operating costs in recent years have increased at a significantly higher rate than operating costs. trend. In addition, based on the sales level of the previous year, the inventory has increased from 4.19 billion yuan at the end of 2017, which can support the company to sell for about 7 months, to 34.47 billion in 2021. 19 months, this shows that the company has some problems with inventory management, which is not an easy signal for a conservative like me.

As for the provision for impairment losses on inventories, I personally think that the company has a tendency to relax monitoring losses. It’s also not a very safe signal.

1. Cash : Monetary cash has decreased by about 2 billion compared with last year. Looking at the annual report, it can be seen that other types of monetary funds have increased by about 2.4 billion, and no additional explanation has been made. The value of assets such as bank exchange and other assets is similar, but it is not a restricted fund. If I personally see a situation like this, I will directly put a question mark on such assets.

2. Fixed assets : The increase is also very large, accounting for about 63% of the total assets. The bulk is caused by the transfer of fixed assets from the construction in progress. The company’s long-term equity investment scale shows that the rise in fixed assets is within an understandable range, but the depreciation policy also needs to be comprehensively considered.

3. Operating liabilities : The operating liabilities are about 41.8 billion yuan. Checking the annual reports of competitors such as New Hope and Wens shares all have a similar situation. In particular, there are other payables with huge data. It is speculated that it may be from the pig industry. Common situation. Operating liabilities, such as various types of payables, are not like interest-bearing debts that require interest. They can be considered to be generated with the expansion of the company’s own business, and the safety is relatively controllable. If If the company’s operating income and profits are of high quality, it is one of the ways (provided that the quality is high) that the company reflects its strong position in the upstream and downstream.

Look at the quality of revenue

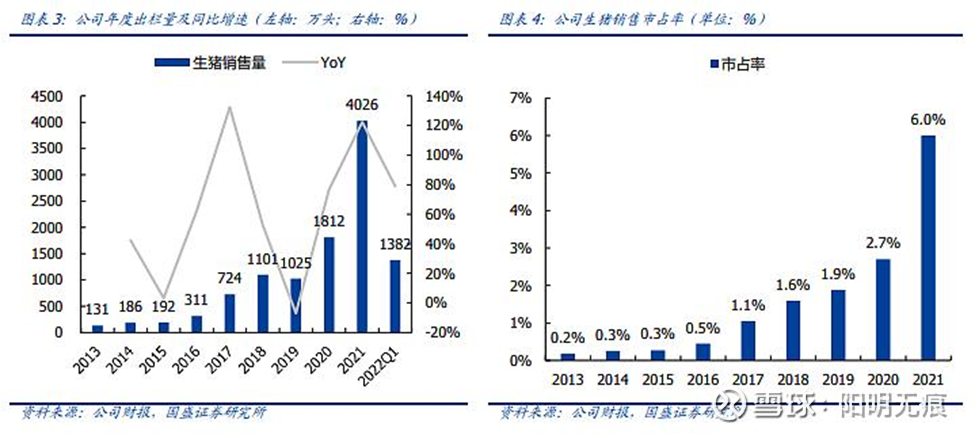

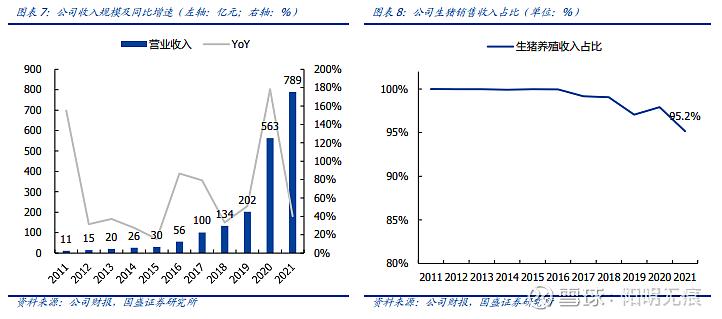

The company’s slaughter volume of live pigs in 2021 The company’s live pig slaughter volume totaled 40.236 million last year, accounting for almost 45% of the entire industry. It can be described as the absolute leading enterprise in the industry, followed by Wen’s 13.21 million and New Hope’s 9.98 million head. The total revenue is about 78.89 billion yuan, and both the slaughter volume and the total revenue have reached a record high. It can be said that it is a milestone year, and through 2021, it will secure the throne of the global pig enterprise.

As can be seen from the figure below, when the pig price or the market cycle declines in 2021, the main source of the company’s operating income increase is to seize market share by expanding the slaughter volume. However, considering the characteristics of the pig industry, the pig enterprises will not be able to increase the price by strengthening brand building like other companies. The Chinese people will not pay different prices because this pig is produced by Muyuan and that pig is a new hope to produce. Price, in other words, the industry does not drive prices up because of brands.

And the breeding industry is not like a company with large-scale production costs. As long as there is a market, increasing the production volume can reduce the cost per unit of product, because after the piglets are reproduced, they need fixed feeds to grow normally. , the unit cost after birth can be considered almost fixed. In addition, if the sow can increase the output, but I understand that even if the output is increased, the feed cost in the later period is fixed, so there is generally no obvious scale cost advantage in animal husbandry.

Regarding the question in the inquiry letter about why the slaughter volume continues to increase when the price of live pigs is falling, I personally guess that on the one hand, the market demand side is enlarged. After all, when the price of pigs is falling, it will stimulate more people to choose to consume pork instead of pork. Chicken or duck meat, on the other hand, may be due to the fact that there will be a large enough inventory in 2021 (recall that the data of productive consumables is about 27.1 billion), and the growth cycle of commercial pigs is 10-11 months. These piglets, Fattening pigs will not stop growing. Since they are grown up, they will occupy warehouses if they do not buy them and require additional costs to raise them, so they will simply increase the number of slaughtered pigs. This assumption is based on two preconditions, one is that the stock is genuine, and the other is that the live pigs are not. The cost of slaughtering is higher than the cost of selling.

To sum up: when the cycle is down, especially when the sales price is lower than the production cost, the quality of the operating income obtained by expanding the slaughter volume to seize the market is not high.

Look at profit quality and free cash flow

As mentioned above, once the inventory is sold, it is the operating cost. Therefore, we will combine the company’s main business and net cash flow to examine the company’s profit quality. The table below is compiled from the company’s annual report data.

In addition, according to reports, the level of domestic breeding profits is generally expressed by the pig-grain ratio, and the positive correlation between the pig-grain ratio and the profit of live pig breeding is as high as 90%. From the comparison between the pig-grain ratio trend and the price trend of live pigs, we can see that the two are basically the same, indicating that the profit of breeding is directly affected by changes in the price of live pigs. Of course, raw materials also have an impact on the profitability of pig raising, but the key is the price trend of live pigs themselves. . When the pig-to-quantity ratio declines, the company’s future profitability will definitely be greatly affected.

According to the scale of accounts receivable in recent years, it can be seen that the company’s collection is normal. Although the net cash flow in some years is less than or slightly greater than the core profit, it shows that the company does generate a certain amount of net profit. It can be seen from the consolidated income statement that the company’s free cash flow in 2021/2020 is about -28 billion/-25 billion, and the early annual reports are all negative. Combined with the parent company’s investment in subsidiaries and free cash flow, this also verifies why the company should continue to issue bonds or borrow debt.

To sum up: in the stage when the pig volume ratio is declining, the company’s gross profit and net profit will definitely be affected. In addition, although the company has a certain net profit, the company’s free cash flow situation is very bad.

look at risk

According to the company’s latest 2021 financial report, the total amount of interest-bearing debts (short-term borrowings, long-term borrowings, non-current liabilities due within one year, and bonds payable) is about 52.6 billion, accounting for about 30% of total assets (25% in the same period last year). %), competitors New Hope, Zhengbang, and Wen’s shares are about 48%, 50% and 40% respectively. Compared with their competitors, it seems that the ratio of interest-bearing debt is not high.

However, if we analyze the changes in the total assets of the above-mentioned companies, we will find that the growth rate of Muyuan ‘s total assets last year was 45%, while the other companies were 21%, -20%, and 20%. Although the total assets of Zhengbang shares decreased by 20%, the shareholders’ equity increased by 1 billion yuan, which is the largest increase among all companies. Among the total assets of Muyuan Shares of 177.3 billion, shareholders’ equity only increased by 200 million, of which about 52.3 billion was formed through borrowing (total assets increased by about 52.5 billion in 2021), in addition to the company’s 2020 level. In comparison, the size of the company’s interest-bearing debt tends to increase.

The total asset-liability ratio in the CSRC’s inquiry letter is 61.30%, which includes operating liabilities such as various payables. Operating liabilities such as various payables do not require interest as interest-bearing debts. The security is relatively controllable due to the expansion of the company’s own business. If the company’s operating income and profit are of high quality, it is one of the ways for the company to reflect its strong position in the upstream and downstream (provided that the quality is high).

In addition, the various indicators mentioned by the CSRC, such as the interest coverage ratio and other indicators that characterize the level of debt, can be queried online and then calculated based on the data in the income statement, because this content is calculated by formulas, and I believe that the CSRC The computing power of the professionals in the meeting will not be repeated here, but the indicator I often use is the use of the company’s cash assets + notes receivable (total about 84 100 million, not 12.1 billion, the specific reason is because the space is limited today, which will be explained in a later article) and the interest-bearing debt is compared. From the above cash/interest-bearing debt, we can see that the ratio of the two is 16% (Interested friends can compare the proportions of other companies mentioned above), which is far below the ideal location that can be covered by 100%. Therefore, this type of business is not my personal favorite (personally more conservative, because it varies)

In addition, according to the interest of nearly 2.2 billion in the annual report, and simply calculating it with the interest-bearing debt of 52.6 billion, it can be known that the overall loan interest rate is about 4%, considering that the company has issued a large number of bonds. , the interest rate is not too high.

Conclusion: Financial security is a personal opinion that the scale of interest-bearing debt is not large compared with the same industry, but one of the factors to be considered may be caused by the large change in the total asset increase in 2021, resulting in a larger denominator. The comparison has a tendency to magnify; the company’s cash assets are not enough to cover the company’s interest-bearing debt

2022 business forecast

Based on the sales data given by the slaughter volume in April, the main operating income in 2021 and the price of commercial pigs, it can be roughly calculated that the average price range of commercial pigs in 2021 is between 16-18 yuan/KG (with The possible reason that the price disclosed by New Hope in the second half of 2021 is 12-18 yuan/KG is that the price in the first half of the year is in the high range), and the weight of the pigs for slaughter is about 110-120KG. According to the company’s disclosed target sales target for 2022, which is between 50 million and 56 million heads, and on the premise that the price of commercial pigs is unlikely to rise sharply, it can be roughly estimated that the annual turnover in 2022 should be In the range of 86.2 billion to 96.6 billion .

Valuation

The core link of all the analysis has come again, that is, the question of whether or not Muyuan shares can be invested at this moment or what position can be invested.

Based on the above analysis, the company’s inventory assets, related transactions, and total assets in 2021 are mainly completed by borrowing for growth. Combined with the current increase in pork and raw material prices and the company’s reproduction costs that are already higher than the price of pigs The situation continues to expand the slaughter volume of live pigs, etc. Although it is possible to roughly predict the range of operating income in 2022, it is difficult for me to give an estimated range of its net profit in 2022. Just like I analyzed the situation of Zhejiang Longsheng before, Muyuan shares belong to a company that I do not understand very well, so it is difficult to give a valuation advice.

Here, the analysis of Muyuan shares has come to an end, and it can be regarded as a matter entrusted by a friend.

The above analysis is my opinion and does not constitute investment advice

There are 58 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/3187608717/220935068

This site is for inclusion only, and the copyright belongs to the original author.