I have been following the shipping industry for a while, and I have shared a lot of my combing content. This time, I will share the long and short logic of the container shipping industry. The part of personal long-term funds in the future dares to lock up positions, and the part of medium and short-term funds depends on the situation, and this will not be disclosed.

———————————————–

Let’s talk about a short-term logic that has been completed in the consolidation and transportation

As for the short logic of the first round, it is actually the most fertile. Since the epidemic has brought everyone’s pessimistic expectations of the whole market, the gradual recovery of market confidence has actually created a redirection of funds in the secondary market. Whoever has better certainty will be favored by the funds. Obviously, the label of the epidemic beneficiary stock is particularly conspicuous on Haikong, so it also attracted the first wave of pull-up. This wave of pull-up funds does not care how much profit you can bring after CCFI reaches 1600 points and breaks the historical high. Like the current oil transportation, most people don’t know how much the performance will be, no matter what the logic is, so it is estimated that the historical high of Haikong is more than 60 in the beginning of 21, and the maximum profit is close to 20 billion (you must believe it). Most of them are not able to distinguish the difference between container shipping and dry bulk. Just like the current China Merchants Steamship and COSCO SHIPPING Energy are both done by the conflict between Russia and Ukraine, who can figure out that China Merchants Steamship still has container shipping and dry bulk?), the stock price at that time It looks like 16-17, and I dare not continue to pull it, because after the CCFI exceeds the historical high, what kind of curve formula will be reflected in the performance of Haikong is uncertain for large funds, and for small scattered companies. It is said that it is the stage of waiting for the performance to show people.

If we resume the Dragon Ball stage at the beginning of 2021 now, from the quantitative point of view, the price limit before the announcement of the 20-year performance forecast in 3.8 can’t really be attributed to the wash, but the large funds are gradually withdrawing from the stage where they are reserved to safe positions. Because most people are unpredictable in the face of historic opportunities. After the announcement of the annual report, in fact, the big capital has been able to have the initial calculation formula in the CCFI index and its performance forecast, so it has gradually intervened and started to sprint after the first quarterly report on the 4.6th. This time, the sprint was very fast, because the main line of the epidemic is slowly disappearing, and the investors who came in again are all for performance. And the short-term clear cards that are getting harder and harder to play are left with the short-term band game.

———————————————–

Let’s talk about a short-term logic that is going or about to go in the shipping industry.

For the second round of short logic, does it exist? I have doubts. Here I have to add that the so-called second round of short-term logic refers to the stock price reversal, which can be pulled up by 30-50%, and then all rebounds. Because what a reversal needs is a strong divergence, what is needed is a new dawn after the disappointment of most people. But now whether it came out or not I can’t say. There are two reasons.

1. They are all defined as such a rubbish management, and they still scolded and voted against it without leaving the venue. Can this be called disappointment to the business?

2. This is the biggest and most tangled factor in my opinion. The epidemic that started in March did not bring the freight to the low point of this cycle, so it is difficult to say that the rebound in freight after the unsealing of the goods has a big magnitude. If there is no reversal of difficulties, there will be no major differences. The only remaining differences are whether the immediate stability exceeds the long-term association and whether the peak season can make CCFI reach a new high.

Based on the above two points, this second round of short logic, I look at it in terms of rebound. There are traces on the technical side, but no one can tell. In short, I have a hard time believing that the rebound can break the high of 20 at the beginning of the year.

But the reason why I always hold Haikong firmly is that it is difficult to fall below its PB, and the major shareholders of Haikong also want chips, and the buyback is like the sword of Damocles hanging in the short position. The bears and the management are actually tacitly testing each other to strive for greater benefits for themselves. But in the long run, whoever stands on the fundamental side will always win.

By the way, is there a third round of short logic? This is to be seen step by step. When I look back, I will release my performance estimates. When I make the calculations, I will make the calculations based on the decline in profits in 23 years and the return to normal in 24 years. As long as there is weakness in the fourth quarter of 2022 or a decline in early 2023, there are still poor expectations, and there may even be no expectations for a return to normal in 24 years. At that time, the two sides of Men Qing, who are now following the trend of stock speculation and OTC performance, will change hands fiercely. Anyway, it doesn’t matter to me whether short logic comes or not. Long-term funds are realized by the long-term logic of eating dividends. Even if there is a short-term logic in the middle, it depends on whether the individual can grasp this problem.

———————————————–

It’s the turn of the most important long logic

Speaking of long logic, it’s actually not easy to do at all. Because the gap between the performance center and the peak performance may be too large , if the DCF valuation after the steady state or the conventional PE valuation after the steady state may result in less money than the current earnings in the past few years, he is a high risk and low return things.

Since it is a high-risk and low-reward thing, differences will naturally exist, and there will inevitably be excess returns. It’s just that this time process is a bit long. I look at it according to the 24-year return to the center and firmly believe this. Will the market believe that it will go to the next level in 25 years? Or is it stable for 25 years? Perhaps the signing of the long-term association at that time and whether it will be lower than the long-term association in the past few years has become the key watershed for the differences to turn to consensus at that time.

In short, Long Logic may go out of the trend of Long Niu, but there are indeed great risks , including the risk of whether the money earned by Haikong will be shared with small and medium shareholders. Without the reinvestment of dividends from peak profits in recent years, the return of valuation after transferring to central profits will eventually be a general rate of return.

Here is a statement, no matter how this cycle goes, whether it is OOCL or COSCO SHIPPING Holdings. The container shipping industry is still a good industry, and it is also a good company. The quality of the enterprise itself is good, and there are no major problems. The industry has also passed the stage where the end of the bayonet will kill you, and it will be a good choice to be a long-term valuer. In the future, if other links in the supply chain can be better integrated, then the upstream and downstream of the entire industrial chain will not have mutual constraints and games, then it will not only be a good business, but a unique business. If it really happens in the next cycle, the steady-state PE of Haikong will be much higher than that of OOCL.

———————————————–

Pros and cons of OOCL and COSCO SHIPPING Holdings (long-termists only need to pay attention)

1. OOCL dominates in terms of dividends. COSCO SHIPPING Holdings holds 71% of OOCL, SIPG holds 9% (China COSCO holds 15% of SIPG), and Silk Road Fund holds 5% (Belt and Road Fund), these alone are enough to support The logic of long-term stable dividend distribution in the future. Haikong’s financial structure is weaker than that of OOCL, and it needs to increase its holdings and repurchase, and gradually increase dividends.

2. The domestic trade business makes the profit margin of Haikong less than that of OOCL. What I am most worried about is the rise in oil prices and the cost of cargo handling eroding the profits of Haikong. Due to the low gross profit margin of domestic trade, its cost sensitivity is particularly high. The rise in cargo handling costs caused by congestion and high oil prices will make Haikong’s income very low. Whether the domestic trade will lose money and how profitable it is, it can be compared with the grain logistics in the bid. The two have the same capacity and the same revenue. The operational efficiency of Haikong is still higher, so Zhonggu is the lower limit of the profit of Haikong’s domestic trade.

3. The tax rate issue, no matter what the EBIT is, it is still net profit as an investor. Haikong’s tax rate is high. Under the circumstance that the operating efficiency of the two is similar, a company with a low tax rate is always better.

4. Most of the invisible capital investment (terminal construction) is in Haikong, but the resources of the two companies are shared, and the settlement of related transactions is only the normal price, so OOCL takes advantage.

Based on the above points, OOCL is more advantageous for long-term holding.

5. In terms of ship leasing cost, Haikong has an advantage. OOCL’s short-term charter ratio is close to 15%. To maintain capacity, the high-priced charter in the next 1-2 years will increase the cost. And Haikong does not need to worry about this problem.

6. The proportion of shipping capacity over 20 years old is dominated by sea control. Most of the content shared on the forum is the average age of the ship, but the age of the ship based on the capacity caliber is rarely known. According to my own statistics, before 2003, Haikong’s shipping capacity accounted for less than 1%, while overseas accounted for 7.5%, so the replacement cost of this part is also high overseas.

7. It is still the issue of invisible capital investment. Due to the high profitability of container shipping, the benefits of infrastructure are often ignored by investors. But if the central profit margin of the container shipping industry drops in the future, then the benefit contribution of the basic income is also worth looking at.

How to choose depends on the individual investor, good and bad are relative. For most investors, the lack of financing overseas and the high dividend tax cannot be ignored. The more important thing is that it is expensive now. If you buy expensive, you will take the risk of underperforming similar products for a period of time.

———————————————–

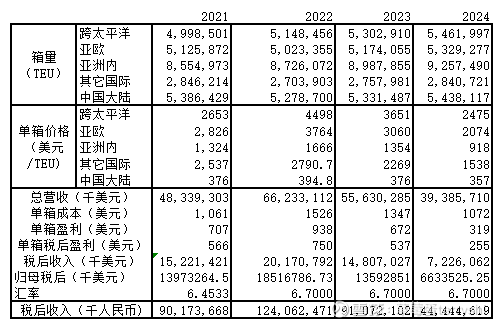

Attachment: Performance Forecast (take COSCO SHIPPING Holdings as an example)

The calculation assumptions are as follows –

A. The new long-term association of the US line in 2022, the one-year price is mostly $9,000/FEU

B. The new long-term association of the US line in 2022, the two-year price is mostly $7,000/FEU

C. In 22 years, the spot price is the same as the long-term agreement, and the spot price from 23 years onwards is 500 USD/FEU higher than the long-term agreement

D.CCFI peaked at 3600 points in Q1 of 22 years in the current container shipping cycle, and the subsequent trend fluctuations were basically in accordance with the adjustment range I mentioned in the top article. In the calculation, it is estimated that Q1 in 2024 will return to the low point of the normal freight center range, which is roughly close to the level in Q1 in 2021.

E. If there are no other black swan events, return to the center of container shipping performance in 2024

F. The average price of oil price is US$110 per barrel in 22 years, US$100 per barrel in 23 years, and US$90 per barrel in 24 years (COSCO SHIPPING Holdings, according to the existing capacity allocation structure, consumes less than 2 barrels of oil for each TEU transported on average)

G. The biggest point of disagreement is that the cost of a single box of Haikong in the first quarter of 2022 rose too fast, which led to deviations in cost estimates. The adjustment of parameters may need to be observed according to its subsequent reports.

H. Terminal business income + cash management in hand can roughly offset the annual financial expenses, which are not included here for the convenience of calculation.

i.

J. Considering that OOCL is relatively low, the overall tax rate is 20%

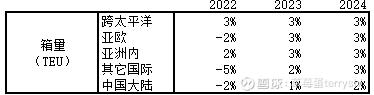

K. 22-24 year box volume change

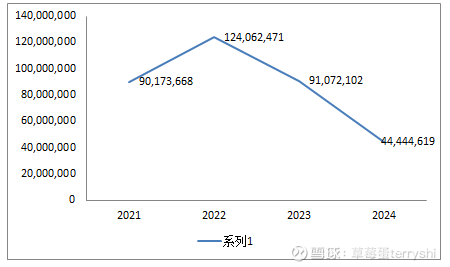

Based on the above assumptions, I attach my performance measurement table. Those who are interested can adjust the parameters by themselves.

To sum up, I predict that the performance will return to the central level in 2024, and the profitability of the shipping industry in the future should fluctuate between 37 billion and 50 billion. The reason for the fluctuation is that the average oil price increases or decreases by 10 US dollars, which will affect the profit of about 3.5 billion.

In the future, the revenue will basically remain in the range of around 40 billion US dollars (on the premise that Haikong does not open up new routes)

Since then, most of the logic of Haikong has been shared. In the future, I will study other industries. I wish all sailors share the future. $COSCO SHIPPING Holdings(SH601919)$ $COSCO SHIPPING Holdings(01919)$ $Orient Overseas International(00316)$

There are 48 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/9810354164/221947968

This site is for inclusion only, and the copyright belongs to the original author.