Welcome to the WeChat subscription number of “Sina Technology”: techsina

Author | Kong Yuexin Editor | Rao Xiafei

Source: Ran Finance

The days of streaming media “carrying the handle” Netflix are also not easy.

In the early morning of April 20th, Beijing time, Netflix (NFLX.O) released its financial report for the first quarter of 2022, and the final result can be said to be an “epic rollover”.

Regarding Netflix’s most concerned core indicator “new global subscribers”, according to the financial report data, the net addition of subscribers in Q1 in 2022 is far from reaching the previous “lower” growth expectation of 2.5 million, and the data of new global paid users also A decrease of 200,000 compared with the same period last year, this is also the first time that Netflix has a negative net user growth in the past 10 years.

At the same time, Netflix also gave its expectations for the second quarter of 2022, with net additions of paying users reaching -2 million. Compared with the rapid growth in previous years, the slowdown in Netflix’s growth has foreseen the ceiling of platform users.

In addition, Netflix’s revenue in the first quarter of 2022 was US$7.868 billion, a year-on-year increase of 9.8%. The growth rate has also slowed down significantly compared with recent years. The Q2 revenue growth rate is also expected to be around 10%; net profit attributable to the parent is 15.97 The net profit margin also fell to 20.3% from 23.82% in the same period last year.

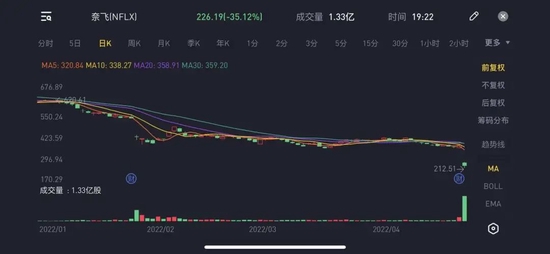

This “transcript” was obviously not acceptable to investors. Once the financial report was disclosed, the secondary market immediately gave negative feedback on it. On April 20, Eastern Time, Netflix’s stock price plummeted at the opening, during which it fell to US$212 per share, the lowest value since the end of March 2018, and the market value instantly evaporated by over US$40 billion, equivalent to hundreds of billions of RMB. As of the close of U.S. stocks on April 21, Beijing time, Netflix closed at $226.19 per share, down 35.12%, with a total market value of $100.4 billion.

Figure / Source of Netflix’s stock price trend / Screenshot of Tiger Securities Burning Finance

Figure / Source of Netflix’s stock price trend / Screenshot of Tiger Securities Burning FinanceAt the same time, Netflix’s competitors, such as YouTube, Amazon, Hulu, Disney+, etc., are also increasing their content investment, trying to “disrupt” the streaming media market, which has also brought more growth pressure to Netflix.

Under the “internal and external troubles”, Netflix announced that in the case of slowing revenue growth, it will aim to protect operating profit margins in the next few years, and will also reduce some content and non-content expenditures, which means that Netflix has also entered the market. The stage of “cost reduction and efficiency increase” has been reached. In addition, the earnings conference also showed that Netflix will no longer insist on “de-advertising”, and will try to develop an advertising model in the future to meet the needs of price-sensitive users.

Peak growth, involution from peers, cost reduction and efficiency enhancement, advertising… Netflix’s situation and various countermeasures make people feel that “soul wear” Aiyouteng, the Netflix membership payment model that China has been yearning for, seems to have been Unable to persist; and the parallel model of membership + advertising, Aiyou Teng has not been successful so far. Next, how should the long video platform go on?

The first negative growth in membership in ten years

Judging from Netflix’s 2022 Q1 financial report, its data performance is not useless, at least the revenue has maintained growth, but the return to “single-digit” growth after the slowdown also means the streaming media dividend brought by the epidemic is fading.

In this regard, Zhang Yi, CEO of iiMedia Research Consulting, believes: “The attitude of European and American countries to ‘lay flat’ on the epidemic will allow users in the region to engage in more outdoor activities, and audiences will return to the cinema to a certain extent. This will also lead to Netflix this year. It’s basically been like this throughout the year.”

Although Netflix in the financial report attributed the decrease in membership to a certain extent to the impact of the Russian market. But in Zhang Yi’s view, objective factors, the impact of the Russian market is very limited, because there are only hundreds of thousands of users in Russia, and the slowdown in the growth of streaming media in the post-epidemic era is the main reason.

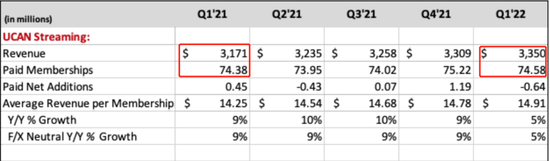

At the same time, in order to stabilize revenue growth, in January this year, Netflix again raised the “subscription price” for monthly users in the United States and Canada. Although from the financial report, Netflix’s North American market revenue rose to $3.35 million from $3.17 million in the same period last year.

However, from the perspective of user data, the rising membership fees make Netflix’s decline in the North American market particularly obvious. The number of new paying users in the US mainland and Canada market decreased by 640,000 compared with the same period in 2021. The number of new users in Europe, the Middle East, Africa, and Latin America fell year-on-year across the board. Only the Asia-Pacific region maintained a growth of 1.09 million.

Figure / Netflix Financial Report Source / Ran Finance Screenshot

Figure / Netflix Financial Report Source / Ran Finance ScreenshotSecondly, Netflix said that the current user group of the platform consists of paying users and unpaid groups who share other people’s accounts, and there may be more than 30 million accounts shared in North America alone. In the earnings conference, how to leverage consumers who share accounts has become an important topic of Netflix. “Our goal is to make members pay a little more when sharing with outsiders.”

Although Netflix has done account sharing tests in some regions before, it is not yet known whether this method will be accepted by users. Some netizens believe that the continuous decline of Netflix’s stock price is also related to the release of news to crack down on the behavior of sharing accounts.

“User habits have terrible inertia, from free to paid, never restricted to restricted, they will encounter a painful transition, coupled with the impact of short videos, high content copyright fees, and spoiler piracy, etc. The rampant, streaming media is naturally difficult to develop.”

In addition, Disney, Amazon, Apple and many other giants have all entered the streaming media track, which will also affect consumer choice and investor confidence.

According to Bloomberg, in terms of net new user data, Netflix may have its worst year in history since going public. “This means that investors need to adjust their expectations for the growth of streaming media platforms, and Netflix can no longer grow as fast as it used to.” Zhang Yi said.

There are popular models, but “Squid Game” is not very common

The peak of user growth has become an irreversible trend. All streaming media platforms, including Netflix, are faced with: how to activate the stock market and find new growth points.

After the global popularity of “Squid Game” last year, the rapid growth of subscribers perfectly proves the attractiveness of high-quality popular content to users, as well as the improvement of member usage, satisfaction and renewal rates.

The financial report shows that the second season of “The Bridgerton Family” is still the English-language drama with the longest viewing time in Netflix’s history, and “Creative Anna” also performed very well. The ratings of the documentary “Tinder Fraud King” and the movie “Adam Project” were not weaker than those of “Red Notice” and “Don’t Look Up” in the fourth quarter of last year. But these film and television works did not bring Netflix the same surprise (user growth) as “Squid Game”.

In addition, in the Korean market, which is highly valued by Netflix, several blockbuster works launched in the first quarter did not reproduce the glory of “Squid Game”. For example, “Juvenile Court” ranked 45th globally; “Twenty-Five, Twenty-One” ranked 44th, and its reputation collapsed due to forced BE later; It’s the bottom line of Netflix.

Figure / “Twenty-Five, Twenty-One” stills source / Douban

Figure / “Twenty-Five, Twenty-One” stills source / DoubanThis also means that in the content moat, the first Netflix does not have a complete lead. In Zhang Yi’s view, veteran content companies such as Disney+ and Warner have obvious advantages in content topic selection and resource reserves, and the audience’s recognition is also very high, representing their strong box office appeal. So for Netflix, his first-mover advantage will undoubtedly be challenged.

Since the fourth quarter of last year, Netflix’s relative weakness in content performance will make competitors unceremoniously continue to divide the cake of the streaming media market and grow rapidly. According to Disney’s 2022 quarterly financial report, the number of subscribers for Disney+ in the first fiscal quarter increased by nearly 12 million to 129.8 million. Netflix’s membership growth in the same period last year was 8.3 million, which means that in the last three months of 2021, Disney’s user growth has surpassed Netflix.

Parrot Analytics also shows that under the fierce competition in the streaming media market, Netflix’s content market share has dropped from 51.4% in the first quarter of 2020 to 43.6% in the fourth quarter of 2021, with rivals Apple TV, HBO Max and Disney+ Its market share increased from 13.5% to 21.4%.

“As for how to improve content, we’ve been improving big movies over the past few years. Things like Don’t Look Up, Red Notice, and Project Adam are examples of this,” Netflix said on its earnings call.

However, although Netflix has been making efforts in the film field for many years, its films are not as “satisfactory” as long-form dramas.

From the perspective of shooting cost and output effect, the “cost-effectiveness” of the film is obviously low. Last year’s Q3 episode “Squid Game” cost $21.4 million, while Q4’s “Red Notice” cost $200 million. When the difference in production cost is close to ten times, some media reported that the viewing time of “Squid Game” is ten times that of “Red Notice”; and “Red Notice” is not as attractive to members as possible. Ten times that of The Squid Game.

In addition, compared with other companies’ films, “Red Notice” also failed to stand at the top of the industry. In the “Top 10 Most Searched Movies in the World”, Netflix accounted for 2, and the remaining 8 were from companies such as Disney.

The performance of “rising stars” is not weak. This year, after Apple TV+ won the Oscar for best picture with “Listening Girl”, it became famous in the first battle, and it also caused “Netflix has worked hard for many years, but Apple TV+ took away the fruit of victory” dramatic situation.

This is also the embarrassing situation Netflix is currently facing. The market share of users is constantly decreasing, that is, the preferred platform of consumers is diverted by other companies. Before the film and television companies decided to do their own streaming media, the copyright of many film and television content was on Netflix, but after Disney, Warner and other content companies did their own streaming media, the copyright was naturally taken away.

“For Netflix now, it needs to produce better content and offer more favorable prices to compete with its peers.” Zhang Yi said.

Netflix wants an advertisement, and the long video “reverses”?

The collapse of Netflix’s performance and stock price due to peak growth is also the current situation faced by domestic long-term video platforms such as Aiyouteng. This also inevitably makes people question the commercialization model of streaming media platforms: paid subscriptions and advertising services are not enough to alleviate the cost and revenue pressure after user growth.

At the same time, the competition in the streaming media market has become increasingly fierce, mergers and acquisitions, increased investment, and become an important way for giants such as Amazon to break through. In this regard, Zhang Yi believes that the rapid growth of Netflix’s market value over the years has made it difficult to find new ways to generate revenue and stimulate investor growth; secondly, long videos can attract and retain these giants. Users, for their main business, are a cheap way to get traffic.

“For Netflix, the user growth peaked, and if it continues, it may be a negative growth from 100 to 99. But for other giants, it has developed from 0 to 80/90, and is currently in net growth. Incremental market stage.” Zhang Yi said.

This is not only an embarrassing stage for Netflix, but also a dilemma faced by domestic video platforms such as Aiyouteng.

However, compared with the advantages of Netflix’s high-quality content and de-advertising, domestic video platforms such as Aiyouteng have been criticized for their membership + advertising model.

According to Zhao Hongmin, an internet analyst and content creator, for non-members, the pre-video advertisements are continuously extended, some even up to 90 seconds, and there are also a lot of advertisements during the video playback. Undoubtedly, every user is inherently resistant to watching advertisements, but video websites are looking for a balance between advertising revenue and user experience, which has also led to the platform charging members again.

Therefore, Zhao Hongmin is not optimistic about the prospects of the advertising model, “I think the proportion of advertising revenue in long video platforms will become smaller and smaller, because users’ requirements for viewing experience are constantly improving, and they will become more and more unbearable to watch. If the advertisement pops up during the video, the proportion of paid members will continue to increase. In addition, I think the boundaries between long video and short video sites will become more and more blurred in the future, and long and short video sites will continue to seize each other’s market share. Content on video platforms In terms of production, the continuous integration of UGC and PGC is also a major trend in the future.”

But unfortunately, Netflix seems to be unable to stick to its “de-advertising” revenue model. From the current experience, attracting users to pay with high-quality content – subscription fees covering content production costs – avoiding advertising profit models cannot bring stable growth to Netflix in the future.

In this case, Netflix urgently needs to develop new ideas for business development. But whether it’s the game business that’s already underway, or starting to develop other businesses in the content field, it takes time and cost. To restore the confidence of consumers and investors, advertising should be the most “cost-effective” way to solve the current growth dilemma.

Netflix CEO Reed Hastings has previously said that Netflix is now “pretty open” to a lower-priced subscription plan that offers ad-supported subscriptions, and he doesn’t rule out the possibility of launching an ad-supported version. At this earnings conference, Netflix also stated that in the next few years, it will gradually promote the realization of the advertising model and provide lower price plans for consumers in need.

And Zhang Yi agrees with Netflix’s test of the advertising model, “When it is difficult for the user market to fundamentally change, it may be a good way for Netflix to try advertising. Because I think Netflix and You Aiteng’s advertising model There should be a difference. Because most of Netflix’s high-quality content attracts members with strong payment ability and very clear entertainment portraits. For advertisers, this is Netflix’s seller’s market; not domestic video platforms buyer’s market.”

References:

“Plummeted 25% overnight, Netflix’s logic collapsed”, source: Long Bridge Dolphin Investment Research;

“Compromise to the advertising model? Netflix handed over the worst report card in a decade”, source: True Detective AlphaS;

“Netflix and You Aiteng share the same disease”, source: Institute of Value;

“Streaming movies, the battlefield is far more than Oscar”, source: Poison Eyes;

“Disney’s Q1 earnings report was better than expected, Disney+ added subscribers, and Netflix’s stock price rose 8% after the market.” Source: Financial Associated Press.

*The title image and some of the accompanying images are from Visual China.

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-04-21/doc-imcwiwst3118164.shtml

This site is for inclusion only, and the copyright belongs to the original author.