This year, we will talk less about specific market issues. What should come will always come back. Let’s talk more about common sense of market analysis.

In addition, the comments are opened, which belonged to the fact that I was too lazy to manage some time ago and just took a break for a few days.

This article discusses the recession caused by the Fed’s interest rate hike. There is a question that many people often ask, why does the U.S. bond yield curve invert after the Fed raises interest rates sharply, which often indicates a recession.

For example, at present, the overall yield curve shows a deep inversion, with an inversion of 100BP in 1-10 years.

You can think about it this way.

First of all, what is the short-term rate of return? It is the financing capital cost of enterprises, etc. If you want to produce and operate, you must invest first if you want to have output. This interest rate is the capital cost of investment. The long-term U.S. bond yield is an anchor point for long-term risk-free return expectations.

So what does it mean to combine the current US debt inversion? It means that you are financing at 4.7% of the cost of capital now, and you can only get 3.7% return on investment in the future…

The purpose of investing is to expect to obtain income in the future, and this is obviously a high-risk investment while paying back money. It is simply “charity”. If it were you, would you make this money-losing investment?

So if you don’t invest, I won’t invest either. Without the current investment, there will be no output in the future. Isn’t this a recession?

Of course, from another perspective, if the Fed suppresses inflation by raising interest rates, it must use recession to “fight poison with fire”.

Still the above principle, if you do not invest, I will not invest, which means that the demand for upstream raw materials is low, the demand for employees is low, the overall demand side has declined, and there has been an oversupply. Will inflation go down?

Of course, the price of doing this is that the market, like a pendulum, often “can’t stop the car” and has a strong reverse collapse.

For example, the Federal Reserve raised interest rates in the past two decades to curb overheating. From June 1999 to May 2000, the benchmark interest rate was raised from 4.75% to 6.5%, which directly led to the bursting of the Internet bubble, and the S&P fell sharply for 3 consecutive years.

From June 2004 to July 2006, a total of 17 interest rate hikes were made, and the benchmark interest rate was raised from 1% to 5.25%, which directly pierced the subprime mortgage bubble, so that the market continued to relapse in the following ten years.

But now, the intensity far exceeds the previous two times, and there is often a delay of about half a year from the inversion to the recession. In other words, in the first half of this year, there is a high probability that the Federal Reserve will come up with a “black swan”.

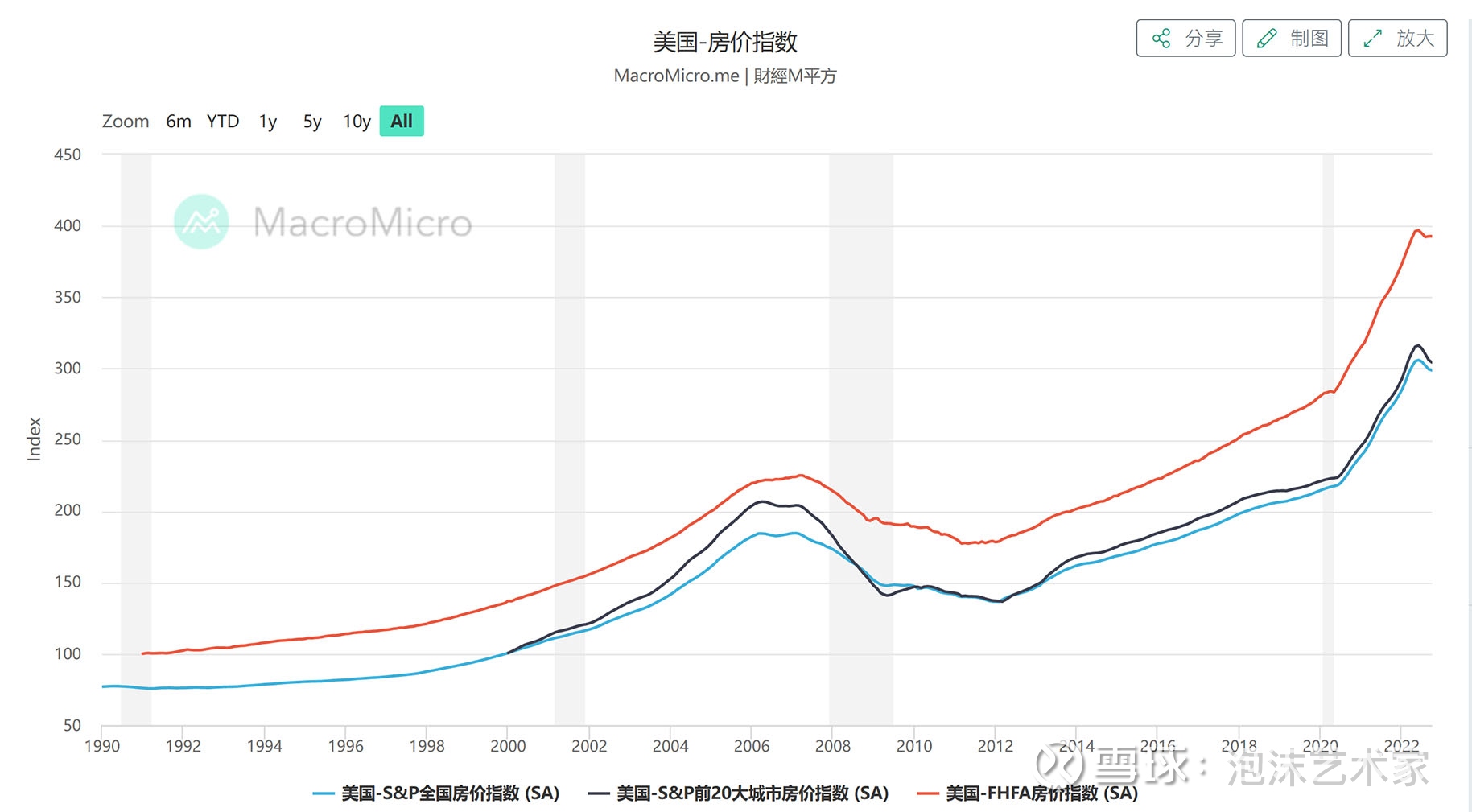

And as shown in the figure below, US housing prices have already begun to turn around. The last time the turnaround was before the subprime mortgage…

In general, the sequence of interest rate hike suppression is:

Liquid speculative assets such as pancakes and growth stocks → real estate demand → non-essential consumer goods → corporate reproduction investment → employment and wages

After raising interest rates, assets with liquidity premiums first fell → then high interest rates suppressed housing prices → consumption of durable goods such as automobiles and home appliances decreased → enterprises with high interest rates reduced investment → wages and non-agricultural data deteriorated

This means that the complete cycle of interest rate hikes will end with poor non-agricultural data. Of course, this is also in line with the two key elements of the Fed’s regulation-inflation and employment rates.

Therefore, it is too early to talk about the inflection point of the Fed, and based on past tests, even if the Fed turns around, the market will continue to decline for a long time because of the inertia of recession that cannot be hedged even if interest rates are lowered.

There are 42 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/9222280625/239181777

This site is only for collection, and the copyright belongs to the original author.