Explanation of terms: SPAC: Special Purpose Acquisition Company is a special purpose acquisition company that has no business but is listed for the purpose of merging or acquiring companies.

$COSCO SHIPPING Holdings (SH601919)$ is more like a spac that already has a profitable business.

When everyone thinks that the economy is pessimistic, cash is undoubtedly the safest, and even Dalio believes that cash has become a neutral asset. Then the company splits the business into SPACs and other businesses, which may have more reference value.

1. SPAC part

At present, under the current economic environment, container shipping companies have basically broken net but not broken net cash (except for Haikong), and port stocks are basically below 0.5PB, but there is room for economic recovery in the future, then at the bottom of the economic cycle Carrying out mergers and acquisitions, on the one hand, reduces the cost of mergers and acquisitions, and on the other hand, can also reduce the cost of holding.

(1) If the economic downturn lasts for a long time

Low freight rates will kill small and medium-sized container shipping owners first. Currently, shipowners ranked after the 8th are all likely to lose money. Yangming and Wanhai are difficult to acquire due to political reasons. ZIM has almost no assets and high-priced leases. International and other shipowners who prefer regional business are likely to suffer losses due to the tariff conditions that are rolled up first in Southeast Asia.

If you pay attention to Haikong’s shipbuilding plan, you will know that he has not built a ship less than 10,000 TEU in recent years, and the future regional routes also need to update ships. At present, Haikong even uses small boats over 25 years old. However, shrinking development plans in loss-making areas and waiting for cash acquisitions during economic downturns will greatly improve the company’s asset structure.

Maersk and other giants have invested tens of billions of dollars in upstream and downstream freight forwarders and ports. If the economy is in a long-term downturn, these assets will be at risk of depreciation, while Haikong holds cash and can use lower valuations for acquisitions or equity swaps , In history, Haikong and Maersk have exchanged terminal rights many times.

(2) If the economy recovers quickly

The shipbuilding plan has been set by various companies, and the ranking order will not be changed in the next few years; and when making acquisitions in other fields, they can use the advantages of cash over Maersk, CMA CGM and MSC to quickly replenish the scale of assets.

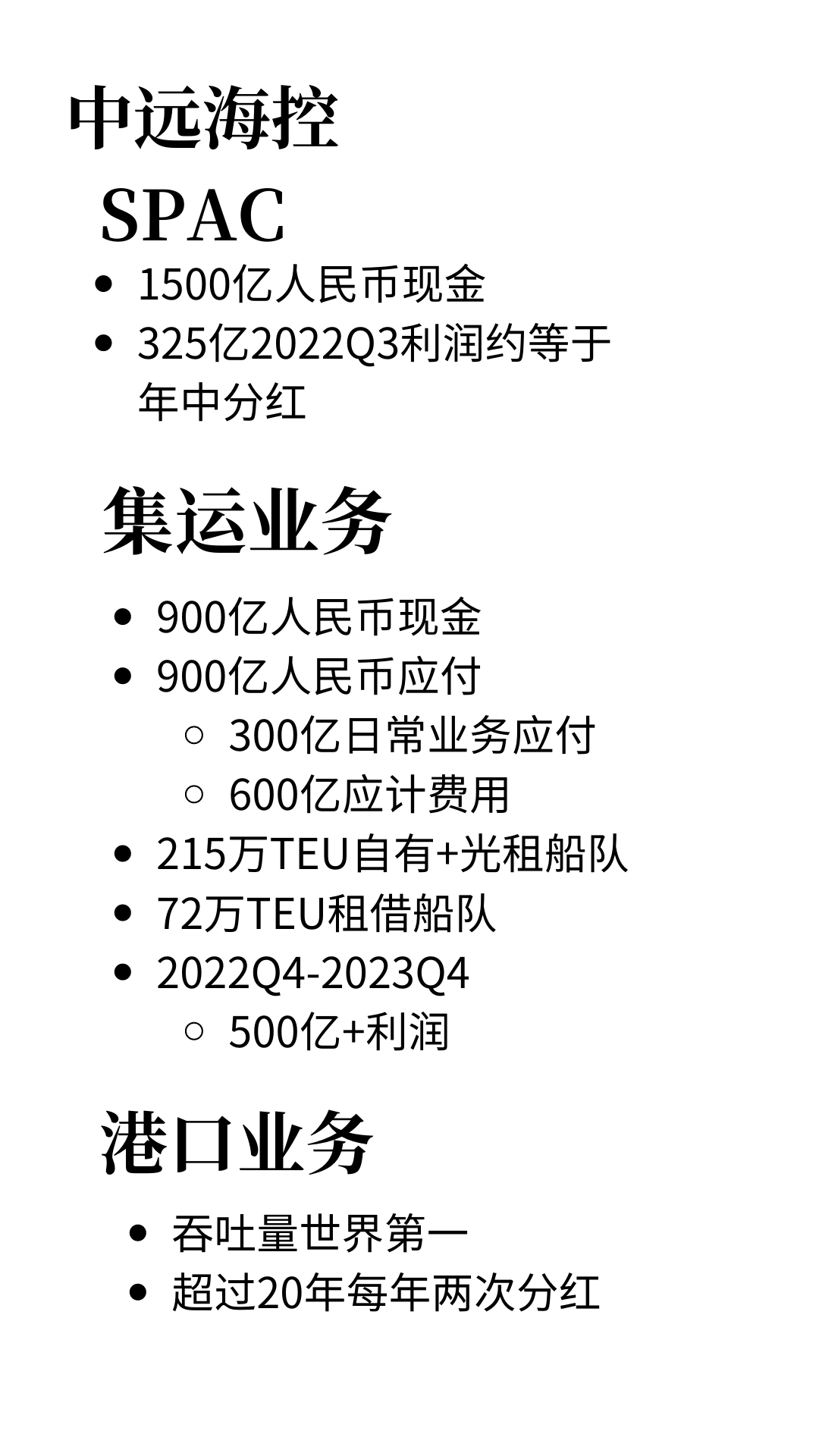

Haikong’s current cash is 247.8 billion, and it earned 32.5 billion in the third quarter. This part of the cash can be divided into three parts, (1) a virtual SPAC with 150 billion in cash plus 32.5 billion in the third quarter profit as a mid-year dividend Cash expenses; (2) Although Haikong is still generating cash flow, it has reserved RMB 90 billion as expenses payable and long-term borrowings of RMB 21.5 billion; (3) Ports, according to the interim report, COSCO SHIPPING Ports has cash of RMB 7.5 billion, And start to pay dividends in the middle of the year.

2. Consolidation business

A lot of related things have been said before, so here is another conservative assessment.

Because many people think that Haikong’s payment will be paid in the future, we reserve 90 billion cash outside the SPAC:

i. Because there are payables for business operations, 30 billion of which are trade payables with specific payment objects, which can be considered as normal turnover in the process of operation, and the remaining 60 billion or more are accrued expenses, and Haikong uses cash Full coverage risk is not a problem either;

ii. The short-term liabilities of the container shipping part are 0, with 21 billion long-term liabilities; 9.4 billion long-term liabilities due within one year.

iii. Among the lease liabilities of Haikong, the ships are only 38 billion RMB, and more than 20 billion of them are low-priced leases from Haifa. The corresponding other ship leases are only about 15 billion RMB and 720,000 TEU. There is no need to worry about the loss of lease liabilities. .

90 billion in cash is enough to cover all future risks.

At the same time, I have predicted that there will be 80 billion profits in the next four quarters. At present, the 32.5 billion in 22Q3 has been released. Then I continue to predict that there will be more than 50 billion profits and higher cash flow in the next five quarters, which is enough to offset the next five years. Capital expenditures.

Then there is full cash deduction for all possible debts, in addition to the container shipping business with its own fleet of 2.15 million TEU, may it be a negative valuation?

3. Port business

The port business has paid dividends twice a year for 20 consecutive years. After the Asian financial crisis in 1998, the IT bubble burst in 2000 and the subprime mortgage crisis in 2008, it is still strong. It cannot be a negative valuation business that pays dividends and loses money every year. Moreover, the company continues to distribute dividends, does not require Haikong to provide cash support, and will not consume Haikong’s cash flow.

in conclusion:

So, let’s not regard Haikong as a container shipping company, but as a SPAC with two additional profit machines. Do we still think his current valuation is reasonable?

The net cash content of foreign giants is far below the company’s market value. Whether it is the giant Maersk (cash is less than one-third of the market value) or the small company ZIM (his long-term lease liabilities are less than cash), these companies’ The net cash ratio is completely inferior to that of Haikong, and basically it cannot cover interest-bearing liabilities and capital commitments.

There are 68 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/9070764642/232783421

This site is for inclusion only, and the copyright belongs to the original author.