Original link: https://tumutanzi.com/archives/16950

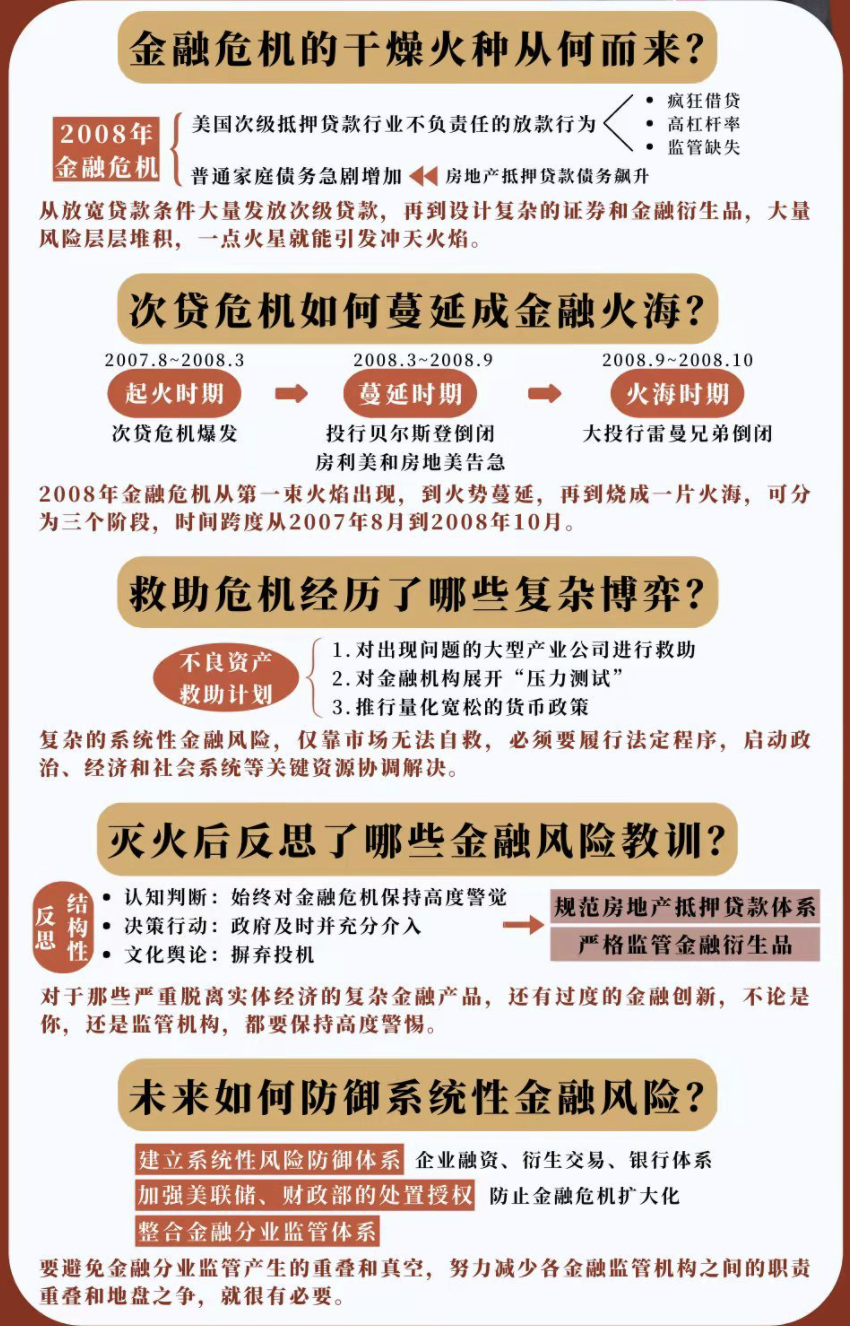

It took me some time to finish reading the book “Fire Fighting: The American Financial Crisis and Its Lessons”. There is a well-summarized mind map on the Internet, as shown in the figure. In addition to these contents, I also have some thoughts after reading it.

- Economic crises (or financial crises) will definitely occur again. If the 1930s was the first large-scale economic crisis, 2008 would be the second. The author of the book calls it Great Depression 2.0. Maybe the third and The first two times are not exactly the same, just like: history will not simply repeat itself, but it often rhymes.

- Because finance is inherently fragile. Modern finance is based on credit. Financial institutions are vulnerable to runs, although modern banks are backed by central banks. However, once the irrational people in the vast majority of branches have distrust of financial institutions, the credit problems of financial institutions will spread rapidly like infectious diseases, triggering runs and forming a vicious circle. Especially in the traditional regulated financial system, such as shadow banks and non-bank financial institutions, this problem will be more serious, playing with money, lack of supervision, and the evil of human nature will definitely play with funds to the point of insolvency.

- All financial crises follow the trilogy pattern of “mania, panic, crash (mania panic crash)”, but people, including financial practitioners and politicians, often mistakenly believe that the current state will last forever, Whether it is in a state of frenzy or a rout, so you can’t see that the risk is coming after the frenzy, and you can’t see that after the crash, spring will always come.

- It is generally believed that once institutions and companies reach a certain scale, they will be “too big to fail”, but some large institutions and enterprises have closed down. The real problem is not that it is too big to fail, but that the relationship between large institutions and other enterprises is too intricate, and it affects the whole body. The United States took this systemic factor into consideration before taking action to rescue the market, but the rescue will also make these enterprises and institutions pay the price.

- The U.S. does not have sufficient supervision of traditional financial institutions, which is due to its decentralized authority. Especially when singing and dancing are on the rise, government agencies are not willing to deal with difficult problems. Coupled with the low efficiency of the democratic system, it is impossible to take precautions for the things that should be managed, and it is impossible to prevent the emergence of systemic risks. Even after experiencing the subprime mortgage crisis in 2008, the author believes that the current situation is only better in terms of prevention. If the crisis recurs, there may not be corresponding resources to put out the fire.

- The financial industry is inherently greedy, and there is nothing wrong with that. Those venture capital institutions and the investment banking industry will use their own resources to lobby policy makers and influence the introduction of corresponding policies. This is also likely to reduce the danger to zero, and thus slowly accumulate until it explodes one day, because the risk is not Complete elimination is only to temporarily avoid the supervision of the policy. And people are often short-sighted, focusing more on immediate interests than long-term interests.

- Practitioners of investment banks and venture capital institutions may be the smartest people in the world, and they may also be the ones who have comprehensive and fast access to information, but they are not always reliable. The big investment banks and financial institutions mentioned in the book all have examples of encountering problems and failing to end. The reason is due to the greedy nature of practitioners in financial institutions. The other side of high profits is high risk, increased leverage, and lack of sufficient buffer ammunition. If you want to make every dollar in the market, you will not end well in the end.

- System crashes don’t happen overnight. There are already signs in the early stage of its outbreak, and there must be a period of risk accumulation. Those who can detect the signs during this period of risk accumulation are the most powerful. In this matter, as early as 2016, the richest man in Hong Kong, Li, believed that the credit bubble in mainland China was relatively high based on his business sense for many years, so he withdrew from the real estate industry in mainland China, thus avoiding the real estate industry in recent years. decline.

- It is a normal capital market to properly let companies go bankrupt, just like metabolism, and eliminate those unqualified participants. Otherwise, just like there is no hell in Christianity, people who do evil will not be punished.

- It is the nature of human beings to filter out their own memories, forget the pain of the past, and recall the beauty of the past. Therefore, even if we know these lessons, we will make the mistakes we should have made again, and we are personally powerless to change the trajectory of history, but wise people should know these laws, and try to avoid its harm as much as possible when the disaster of historical torrent comes.

Reading history can be a mirror, knowing the past can learn from the present. The same is true for economics. The subprime mortgage crisis in 2008 is indeed a good mirror for us to reflect on these lessons.

This article is transferred from: https://tumutanzi.com/archives/16950

This site is only for collection, and the copyright belongs to the original author.