——Portrait of a fund manager: Shanghai Investment Morgan Fund · Du Meng

When you think of long-distance running veterans with good performance, you may first think of Zhu Shaoxing, Fu Pengbo, Liu Yanchun, and Zhou Weiwen. Indeed, these managers are quite famous.

But fame does not necessarily equal strength, and low-key masters are even more respectable! I pulled down the data, and the strongest performance in the past 10 years is actually Du Meng from Shanghai Investment Morgan Fund!

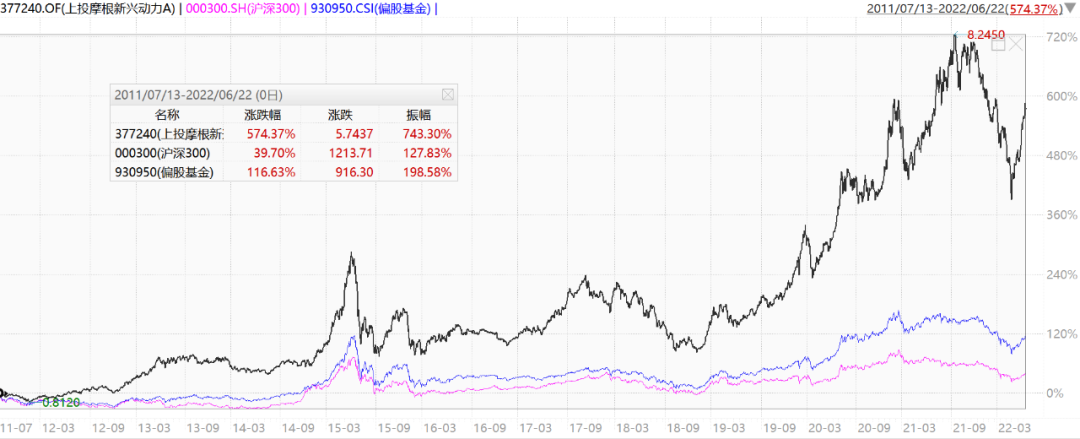

The following picture is a comparison of funds managed by some veterans who have been in the industry for nearly 10 years, starting from Du Meng’s tenure (2011-7-13 to 2022-6-22, data source: Choice)

Du Meng’s performance is far ahead, even better than many well-known top managers, but his current scale obviously does not match his strength and is underestimated by the market.

Such an excellent manager, in this issue of the [Portrait of Fund Manager] column, will give you an in-depth analysis.

Take a look at Du Meng’s characteristics:

·20 years of industry experience, nearly 11 years of investment experience, long-term fund manager

Long-term performance leads the veterans, and the performance in the past 5 years is also excellent

·Distinctive growth style, large ability circle, especially good at mining in the field of new energy

·Strong offensive, flexible, and innovative

· Good at digging out bull stocks, 10 times of A-shares in 10 years have mined more than 70%

·Insist on long-term holding and accompany the growth of bull stocks

·The current management scale is 17.3 billion, with a moderate scale

1. Basic situation

After graduation, Du Meng worked in Tiantong Securities, Zhongyuan Securities, Guosen Securities and Bank of China International Securities, responsible for industry research on many emerging industries. division.

He joined Shanghai Investment Morgan Fund in October 2007, and currently serves as deputy general manager and investment director. He has 20 years of experience in the industry, but industry insiders and old owners generally call him “Brother Meng”.

2. Performance

The representative work of Shanghai Investment Morgan Emerging Power, Du Meng has been independently managing the fund since July 13, 2011. It is a rare “long-term fund” in the market.

As of 2022-6-22, the rate of return is 574.37%, and the annualized rate of return is 19.04%, ranking 4th among the 432 partial equity hybrid funds in the same period. (Data source: choice)

The picture below shows the fund (black line) compared to the CSI 300 (red line) and the stock-biased fund index (blue line). (Data source: wind)

From the historical trend, it can be observed that Du Meng’s fund is characterized by strong aggressiveness. It performs well in bull markets, small and mid-cap markets, and growth styles, but not in value and bear markets. Its monthly winning rate relative to the CSI 300 is 54.55%.

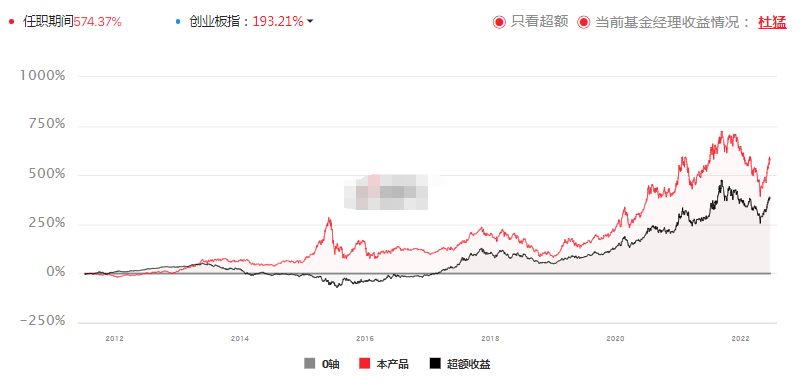

The picture below shows the excess return of the fund relative to the ChiNext (black line). After stripping out the growth style beta, the alpha return is also very strong! (Data source: Jiuquan’er)

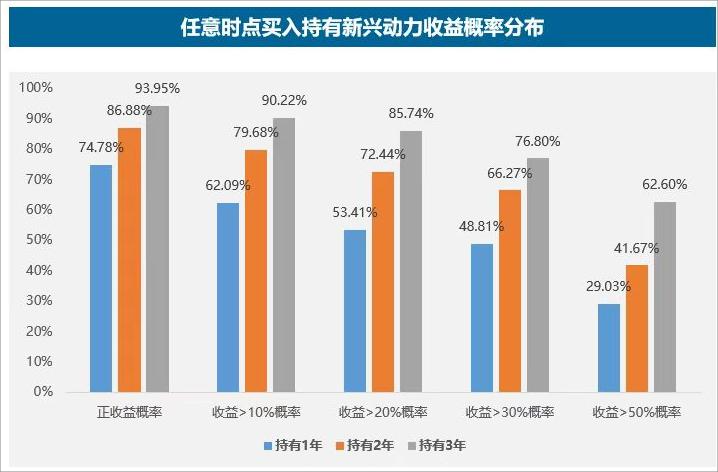

The picture below shows the return and probability distribution of buying the fund at any point in the past. The long-term return is very strong! (Data source: wind, as of 2022-6-22)

3. Horizontal comparison

At the beginning, we compared the performance of some veterans, the range is long, let’s compare the recent ones.

The picture below is a comparison of the performance of some growth-style funds (consecutive tenure) in the past 5 years. In comparison with these younger fund managers, Du Meng is also doing his part and ranking high.

We should also note that Du Meng’s volatility and drawdown are also relatively large in the same category, which is related to his [growth style] and [industry concentration] characteristics, which I will analyze later.

4. Quantitative analysis (the above investment in Morgan Emerging Power as an example)

1. Current position

The picture below shows the top ten holdings in 2022Q1

The average PE is 38.4, the average PB is 7.4, and the ROE is 19.2%, showing the characteristics of growth + high quality. The average market value is 217.14 billion yuan, which is relatively large. If the Ningde era is excluded, other positions are actually mainly mid-cap stocks. (Data source: Jiuquaner APP)

2. Historical positions

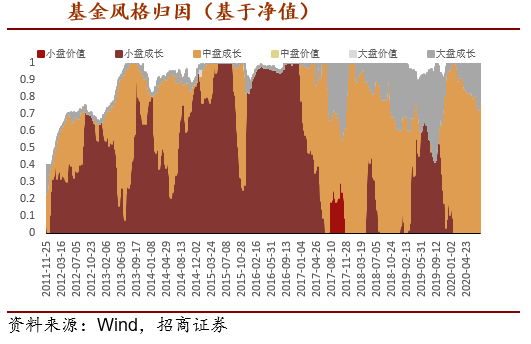

From the perspective of historical positions, Du Meng’s combination reflects an obvious growth style of small and medium-sized caps. The picture below shows the historical position style attribution of @中商業股份有限公司 statistics.

Du Meng’s shareholding concentration is relatively high, 47.91% in 2022Q1, and an average of 54.9% since he took office. The number of combined positions is generally around 35. (Data source: choice)

Du Meng is very good at mining big bull stocks. As of March 31, 2022, in the past ten years, there have been 84 10 times A-share stocks, and Du Meng’s holdings have covered 61 stocks, accounting for over 70%, which is simply too fierce!

The stocks that appeared in the top ten times of the quarterly report (the holding time was relatively long) were: Muyuan Shares (13 times), Yiwei Lithium Energy (12 times), Changchun High-tech (10 times), LONGi Green Energy (11 times), Xinwei Communication (11 times), Oufeiguang (10 times), Tongwei Co., Ltd. (9 times), etc.

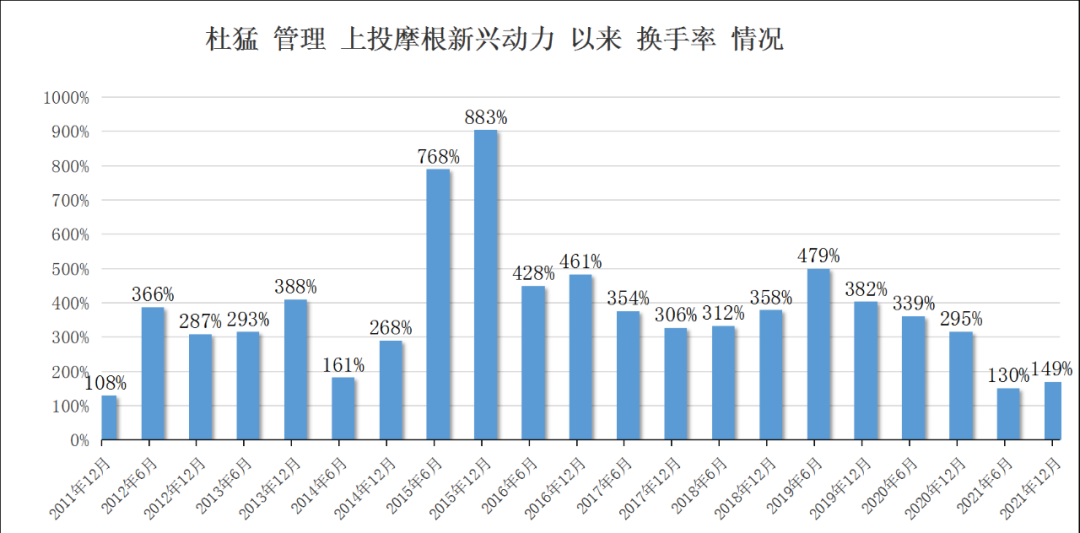

3. Change of hands

Since taking office, except 2015 (bull market), the turnover rate has been relatively stable at other times, with an average turnover rate of 353%, slightly higher than the market average.

(Data source: Tiantian Fund)

For cattle stocks, Du Meng is still relatively comfortable. Taking the positions held in recent years as an example, Yiwei Lithium Energy, Tongwei Co., Ltd., Tianqi Lithium Industry, Muyuan Co., Ltd., and Longji Co., Ltd. all intervened earlier, and the holding time was relatively short. long and able to withstand fluctuations.

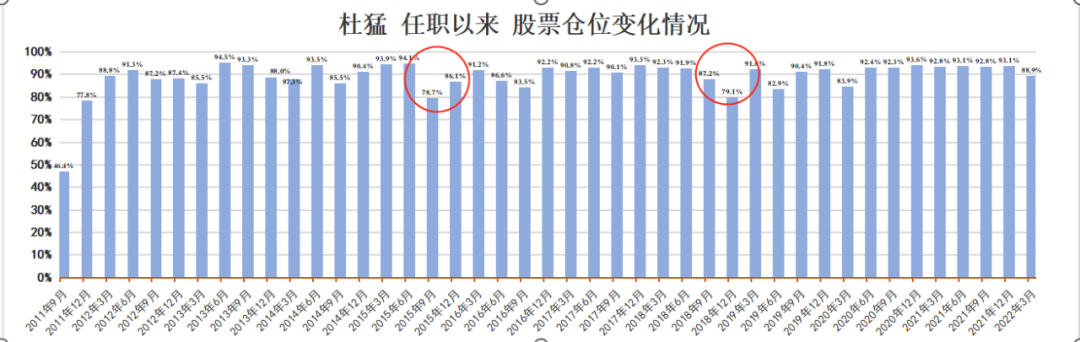

4. Position changes

The stock ratio of Shanghai Investment Morgan Emerging Power is 60%-95%. Since Du Meng took office, he has basically maintained a high position operation, with an average position of 89.6% after opening a position.

Only reduce positions when there is a clear bear market (the 2015 and 2018 bear markets are circled below).

(Data source: choice)

5. Competence circle and industry configuration

As a 20-year veteran, there is no doubt that Du Meng’s ability circle is wide enough. According to the data of @owl research institute (see the picture below), there are 18 industries where Du Meng is often matched in history and has a winning rate of over 50%!

Emerging growth sectors, such as TMT, pharmaceuticals, and midstream manufacturing, all have long-term allocations, and periodic allocations, agriculture, forestry, animal husbandry, and fishery, and consumer sectors are also periodically allocated. Relatively speaking, there are less allocations in traditional industries such as transportation, steel, coal, and banking. In line with the fund’s positioning, the growth style characteristics are stable.

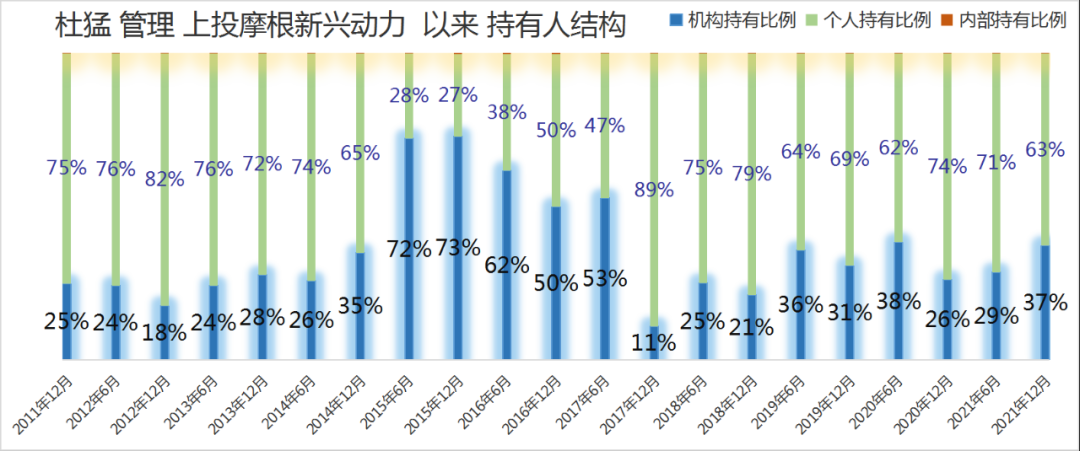

6. Holder structure

Since Du Meng managed the fund, it has been widely recognized by institutions. Shanghai Investment Morgan Emerging Power has long-term institutional funds. According to the 2021 annual report, institutions account for 37%.

(Data source: choice)

According to the 2021 annual report, Du Meng himself also holds 4 funds of his own. Among them, when Shanghai Investment Morgan Woxiang Vision was issued at the beginning of the year, Du Meng invested 5 million yuan to subscribe for the fund, which was fully bound to the interests of investors.

V. Investment Philosophy

Du Meng believes that investment is to select companies with strong competitiveness in emerging industries or growing industries that conform to social development trends, and obtain medium and long-term returns from individual stocks through long-term holding.

1. Industry selection: select companies in industries that are in line with social changes, economic development trends and rising prosperity

Du Meng pays attention to the combination of bottom-up and meso-track selection. He believes that more opportunities for growth come from social changes, economic development, and changes in industry trends.

Du Meng likes industries that cannot see the ceiling in the short term. The ceiling of the industry determines the expected return on investment. He will not pay attention to those industries that are obviously contrary to the trend of the times. Industry prosperity is also an important indicator in the investment framework.

Although he is a veteran, Du Meng has always maintained his attention to and learning from emerging industries. Every major wave of the times will see his leading layout. He is one of the first batch of people in the market to hold heavy positions in the Apple industry chain, and also the earliest A group of people who hold heavy positions in the electric vehicle industry chain.

In Du Meng’s view, growth is a broad definition, which is not opposed to value. There are investment opportunities for growth stocks in all industries, even companies with strong growth potential in the cyclical and agricultural sectors.

When building a portfolio, Du Meng dared to focus on a few promising industries in the portfolio, which is the reason for his good performance and the reason for the high volatility. Du Meng bluntly pointed out that Alpha should not be lowered in order to reduce volatility.

Du Meng: “My investment system is to find out the industries that really benefit from economic and social development by understanding and learning the laws of social and economic operation and development trends, and then looking for high-quality companies with long-term growth prospects in these industries.

There are two kinds of growth. One is the generation of a large number of new demands, which promotes the growth of the industry. The best companies in the industry will definitely have the best growth. The other is that in a traditional stable industry, the company gains long-term growth through its own ability to continuously increase its market share.

Keeping an open mind and persevering in learning new things is what a qualified investor must have.

Judging from the characteristics of the A-share market, the prosperity of the industry is a very important driving force for the upward movement of stock prices. Through the analysis of the upstream and downstream of the industry and the relationship between supply and demand, we will estimate the extent or trend of the upward trend of the industry’s prosperity, and share the opportunities for profitable growth brought about by the upward trend of the industry’s prosperity. “

Du Meng said in a recent roadshow that he is still optimistic about new energy vehicles and new energy, and there is still a lot of industry space, and this is also an area he is very good at.

Du Meng:

“Investment must keep up with the changes in the economic cycle, the real estate cycle in the past 20 years, the development of the Internet in the past 10 years, and the development of the new energy cycle in the next 10 years.

The long-term growth space of the new energy vehicle industry is very large, and the upstream, midstream and downstream may have more than 10 times the demand, or even greater growth space.

The recent volatility has mostly come from investor risk appetite rather than from changes in industry demand. The most pessimistic point has passed, and it has become more cost-effective after adjustment.

From the perspective of demand, whether in Europe or the United States, the sharp rise in the price of traditional energy sources highlights the cost-effectiveness of photovoltaic energy.

From the perspective of industry prosperity, these two industries are far ahead of all industries. The domestic and overseas market demand for new energy vehicles is also growing rapidly. From the history of A-shares, there is not much risk in industries with leading prosperity.

From a risk point of view, the market is mainly worried about whether the increase in upstream costs will inhibit downstream demand. We have observed that the impact of rising upstream prices, whether for photovoltaics or electric vehicles, is not as high as market expectations.

Photovoltaics and electric vehicles have established advantages in the global industrial chain, and this industrial chain is difficult to transfer. For some industries, such as electronics, Vietnam may be able to undertake part of it, but photovoltaics and electric vehicles have no rivals in the world.

The whole vehicle also began to iterate and develop rapidly. It is foreseeable that in the near future, China will begin to export its own automobile platform, and the proportion of China’s automobile industry in the world will reach a very high level. The electric vehicle industry may have the largest amount of value and the fastest growth rate in the next five years and ten years. Fast, and one of the most competitive emerging industries in the world. “

2. Individual stock selection: select high-quality leading companies, favor high ROE and product standardization

After selecting the industry, in terms of individual stocks, Du Meng favors high-quality leading companies, and pays attention to indicators such as competitive advantages, corporate governance, and product standardization.

For different stages of growth stocks, different strategies are adopted: diversify investment in the budding stage, focus on unique competitive advantages in the growth stage, and focus on industry leaders in the mature stage.

Du Meng: “Quality companies have the same characteristics, high capital operation efficiency, high return on equity, and long-term growth without or with only a small amount of capital leverage. The most important thing is that they will all have certain barrier.

In an industry with fierce competition, emerging industry, and long-term space, the management of the company is very important, and sometimes even occupies the first place. Entrepreneurship may be the most important factor in determining whether a business can go on or not.

The company’s products are relatively simple, and it is the most direct logic for the long-term growth of a company to be able to simply replicate and promote it and expand at a low cost. It’s not that I do this one today and I’m going to do another tomorrow and face a lot of problems. “

3. Valuation point of view: good companies are not cheap, growth is more important, but also avoid high valuations

Growth stocks generally have relatively high valuations. Du Meng believes that this is reasonable. He is more concerned about whether there is enough growth to digest valuations and avoid high valuations.

In the previous quantitative analysis, we also found that when Du Meng is optimistic about the overheating of the new energy vehicles and photovoltaic sectors, he will sell to realize the income.

For example, Du Meng laid out the Ningde era in 2019Q4. With the rise, he gradually reduced his holdings in 2021, and in the callback in early 2022, he took the opportunity to increase his positions again.

Du Meng: “In general, high-quality growth stocks have higher valuations, and targets with lower valuations are often difficult to see development prospects, which also confirms the effectiveness of the market.

The level of valuation is not the most important factor in long-term investment, the most important thing is the selected industry and company. The good growth of the company is one of the important sources of continuous excess returns. The continuous development and growth of high-quality companies will lead to lower and lower valuations.

If you are optimistic about a company, you can evaluate the target market value that can be achieved in the next 5-10 years, and then compare it with the current market value to see if the rate of return can meet your requirements. “

4. Trading hands: take a long-term view and firmly hold high-quality growth stocks

Buy and Du Meng tend to hold for a long time. He believes that high-quality companies have a lot of room for growth and cannot be easily sold because of short-term fluctuations.

Du Meng: “If I choose a company, I will definitely expect to get at least three to five years. The money I make from investment does not come from the ups and downs of the market, but from the income brought by the company’s continuous growth. I am more Choose to research industries, research companies, rather than judging bottoms and tops.

Bull stock volatility is huge, but so are the long-term gains. Sometimes you have to live with volatility, which tests your mindset and research depth.

I have a lot of stocks that I have held for many years. During this process, I have encountered fluctuations of more than 30%, but if you look at it in a long-term perspective, it has risen 10 times, so a 30% drop is nothing. . So I suggest that investors stretch the time dimension and ignore this small fluctuation.

There are several situations for selling: First, the stock has risen so much that it is also seriously overvalued in the medium and long term. Second, the industry and company operations have deteriorated significantly. The third is to find more cost-effective varieties. “

5. Risk control: volatility is not a risk, the risk of investing lies in choosing the wrong company

Du Meng believes that the risk of investment does not come from volatility, but from choosing the wrong asset or company. Especially in emerging industries, there is often a big wave to wash away the sand. Therefore, when exploring growth stocks, Du Meng always remembers to “remove the false and preserve the true”, and constantly track research, analysis and verification.

Du Meng: “No matter how good a company is, there will definitely be ups and downs in the development process. Fluctuation itself is not a risk. What I care about is whether the judgment of the company and the industry is accurate. The focus of attention is shifted from whether the stock is rising or falling to the company. Whether the operation is good or not, whether the growth is good or not.”

6. My analysis

From the perspective of performance, qualifications and ability, Du Meng is definitely the top level of today’s public funds. And experienced and deterministic. Judging from his current management scale, he is not too big. He is definitely an underrated boss. I recommend everyone to pay attention!

Of course, in the holding process, you should also be mentally prepared for growth style characteristics and high volatility. Du Meng takes a long-term perspective, has high volatility tolerance, and is aggressive. His long-term returns are good and record highs repeatedly, which shows that his stock selection is no problem, and he can still rise after falling. Therefore, when there is a sharp retracement, do not sell easily, but consider taking the opportunity to cover your positions.

Zero City Investment, focus on fund research, follow us for more relevant analysis articles.

Reminder: The fund has risks, and investment needs to be cautious! This article is only for personal research and analysis, not as an investment basis, and operate at your own risk. The individual stocks involved in this article are for example only and do not constitute investment advice.

@Today’s topic @snowball talent show @snowball fund

#雪ball star plan public offering talent# #Find you who loves funds # #Investment and finance#

$ Shanghai Investment Morgan Emerging Power Hybrid (F377240)$ $ Fuguo Tianhui LOF (SZ161005)$ $ Xingquan Herun LOF (SZ163406)$

There are 5 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/9290769077/223585048

This site is for inclusion only, and the copyright belongs to the original author.