BYD auto manufacturing plant under the Qinling Mountains in Xi’an

BYD auto manufacturing plant under the Qinling Mountains in Xi’anWelcome to the WeChat subscription number of “Sina Technology”: techsina

Text / Gu Yue

Source: Brocade (ID:jinduan006)

The “new four modernizations” that define the future development of the auto industry are: electrification, intelligence, networking, and sharing. So far, this logic line is still an industry consensus.

Globally, Tesla came out on top, taking the lead in the fields of electrification (three-electric system) and intelligence (FSD service).

As BYD, which can currently compete with Tesla in terms of sales, has also achieved general recognition in electrification, and the next overall advancement will inevitably require it to make breakthroughs in intelligence.

Extending from a micro perspective to a macro perspective, China’s new energy vehicle cluster has gradually won the first-mover advantage of the entire electric industry chain, but in the dimension of the intelligent value chain centered on autonomous driving, it is facing Tesla The depth pressure of the overseas legion headed.

This also means that in the upcoming 2023, intelligence will become the core focus of the new energy track, and an inevitable all-out war is about to begin.

01

noise

Figure: Autonomous driving accident, source: Internet

Figure: Autonomous driving accident, source: InternetRecently, there has been a lot of discussion around the “broken halberd” of autonomous driving companies, and the long-term suspension of intelligence has begun to confuse the market.

E.g:

-

At the end of October, Intel re-listed its asset MOBILEYE for $17 billion, while Intel privatized it for $15.3 billion in 2017, during which MOBILEYE’s valuation once ballooned to over $50 billion;

-

Due to Ford’s decision to stop investing in Argo AI, Argo AI, an L4 autonomous driving company with a valuation of at least US$7 billion and planning an IPO, recently announced that Ford will focus its resources on the development of L2+ intelligent driving in the future;

-

Waymo, an industry pioneer backed by Google, was once valued at as high as $175 billion, but has now fallen to $30 billion, and consumes at least $1 billion in operating expenses of Google’s parent company every year, and took the lead in acquiring Robotaxi in Phoenix and San Francisco in 2018. After the operation license, the speed of its commercialization has been questioned;

-

And Cruise, which relies on blood transfusions from GM and Honda, also recorded a loss of nearly $5 billion on the Robotaxi business (also starting in 2018), and its future commercialization profit and loss point is still unclear;

-

Domestic companies focusing on L4 autonomous driving, such as Baidu and Pony.ai, are also faced with continuous huge investment and commercialization problems, and autonomous driving has become a dream that is difficult to achieve;

-

The speed of autonomous driving around the world has even made the “father of autonomous driving” – Lewandowski sighed: “Forget about profits, all self-driving taxis, self-driving trucks or similar companies. What’s the total revenue? Millions? Maybe, but I think zero revenue is more likely.”

The intelligent road resistance represented by L4-level autonomous driving is long. The direct reason is of course the restrictions at the level of policies and regulations. Behind it are the moral problems implied by small-probability events, and of course, the accident responsibility that car companies need to bear. Wait, the fundamental reason is that there is no significant breakthrough in technology.

It seems that the general development dilemma of autonomous driving has made it a mirage. Although the vision to build is beautiful, it seems unreal to be implemented.

However, Tesla has shown full determination and confidence in autonomous driving. After announcing that it will abandon lidar and enter the pure visual perception solution, it has demonstrated a full-stack, self-developed and full-production full-link autopilot software and hardware architecture. And based on the current performance of L2 automatic assisted driving, it continuously trains and iterates its own pure visual system effect.

Although Tesla is still far from achieving the level of autonomous driving, there are corresponding improvements based on each beta iteration. In contrast, the gradual effect optimization has made the market begin to have a more open attitude towards pure vision solutions. , and also deepened the market’s awareness of Tesla’s “intelligent” label.

02

visual solution

From a general perspective, the realization path of autonomous driving can be divided into single-vehicle intelligence and vehicle-road coordination. The former can be divided into sensor perception solutions based on lidar and visual perception solutions based on cameras. In addition to Tesla, almost all OEMs and autonomous driving companies have chosen the single-vehicle lidar solution, and on the basis of the lidar solution in China, they are simultaneously promoting the infrastructure construction of vehicle-road coordination.

The reason why most manufacturers choose the lidar solution with a much higher cost is because the sensor naturally has the detection and perception capability of the vector space, and the lidar can meet the necessary requirements for restoring road condition information under high-speed real-time conditions, but the sensor It also faces multi-signal fusion problems and is susceptible to weather conditions.

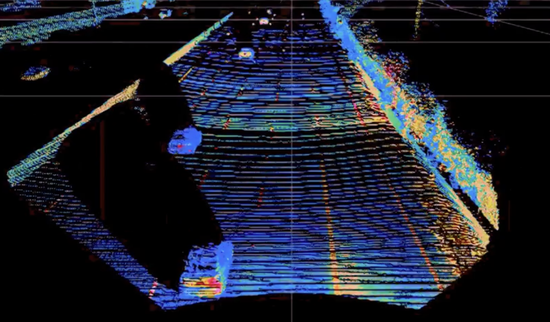

Figure: Demonstration of NIO ET7 lidar night imaging effect, source: Internet

Figure: Demonstration of NIO ET7 lidar night imaging effect, source: InternetHowever, the camera cannot directly restore the three-dimensional space information. It requires a large number of intelligent algorithms to be converted and interpreted after the learning process, and the visual solution has extremely high requirements on computing power and algorithm delay. The biggest difficulty of the visual solution lies in the anthropomorphic intelligence of the system, such as the predictive ability based on driving experience and the generalization ability based on one inference.

Vehicle-road coordination, although it can reduce the intelligence and computing power requirements of bicycles to a certain extent, on the other hand, it requires the promotion of large-scale new infrastructure (such as high-precision maps, 5G, cloud computing, big data, Internet of Things, etc.). Therefore, in the short term, the implementation of vehicle-road coordination will mainly depend on the effect of the trial operation area. At present, it is still far from determining the path and promoting it on a large scale.

At present, from the perspective of L2-level user experience, the experience of Tesla’s autonomous driving assistance system autopilot is excellent, probably not inferior to the performance of any production car’s intelligent assistance system. Tesla finally gained a first-mover advantage in scale with a low-cost solution.

With the significant increase in its delivery volume (about 4 million Tesla vehicles and about 10% of vehicles equipped with FSD), and a complete set of automatic driving systems that are constantly learning and optimized based on normal activation operation and “shadow mode” operation, its Both autopilot and FSD are doing optimization iterations hand in hand.

After getting the most traffic data in the world, Tesla needs to do three things:

One is to convert the 2D road width data into 3D to complete the formatting and standardization of data information. This process is a huge workload. In addition to the data labeling team consisting of thousands of people, Tesla has also developed automation for this. Data annotation tools;

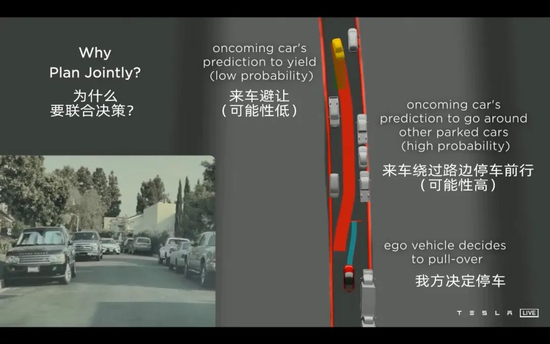

The second is to import the processed data to train the “intelligence” of the control decision-making system. To this end, Tesla has rewritten the FSD infrastructure in recent years, and has used a combination of Monte Carlo tree search and neural network to continuously read data, look at road conditions, pick out complex road conditions or accident problems, and simulate and compare decision-making results. , and then simulate and construct complex road conditions in the real world in the virtual environment, covering as much long-tail road condition information as possible, and further train the decision-making system to deal with low probability events calmly;

The third is the need for a powerful computing power module and system architecture. For this reason, Tesla developed a Dojo chip based on a distributed architecture, and optimized the communication bandwidth between chips (that is, shortening the delay). In theory, it can achieve unlimited computing. Power expansion, which will be expanded synchronously with the needs of data volume and computing power.

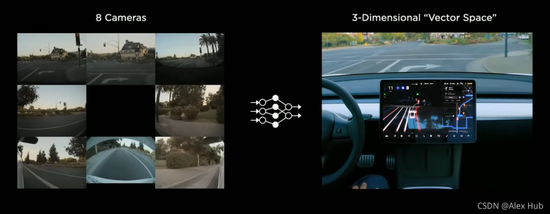

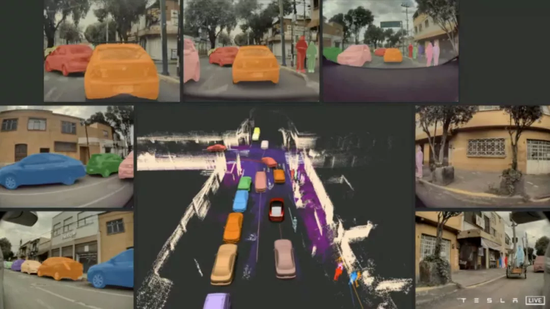

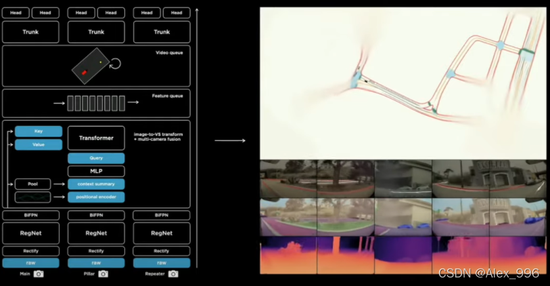

Figure: Tesla visual perception renderings, source: Internet

Figure: Tesla visual perception renderings, source: Internet  Figure: Tesla’s visual perception effect presentation, source: Internet

Figure: Tesla’s visual perception effect presentation, source: Internet  Figure: Tesla Visual Perception Architecture, Source: Network

Figure: Tesla Visual Perception Architecture, Source: Network  Figure: Tesla’s narrow lane meeting scene, source: Internet

Figure: Tesla’s narrow lane meeting scene, source: InternetIn order to greatly improve these three things, Tesla’s core focus is on the field of AI, so the purpose of this year’s AI day is to recruit a wide range of talents.

Objectively, Tesla has a systematic methodology for autonomous driving. Since the camera has a standard data format and common data interface, Tesla only needs to complete a breakthrough on the software side; however, multi-sensor fusion faces difficulties in generalization and standardization. , Among them, lidar is still in the debate on the route of mechanical, semi-solid, and solid-state. In addition, there is a strong coupling relationship between car companies and hardware suppliers, which will face the systematic problem of synchronization and coordination.

So, to a certain extent, the path problem can also be reduced to another problem, is one person running faster or a group of people running faster?

03

China needs to call

Many car companies claim that their “intelligence” is not inferior to Tesla, or claim to have L4-level hardware foundation and capabilities, and will update the system to adapt to it through OTA in the future.

However, compared to Tesla’s “full-link autonomous controllability”, the intelligence of most car companies requires suppliers to take the lead. If the underlying foundation is unstable, it is difficult for car companies to make major breakthroughs. .

At this stage, the intelligent context of domestic manufacturers is basically the product of a template, such as supporting OTA, chip computing power, voice interaction, camera resolution, lidar, driver assistance capabilities, and potential autonomous driving capabilities. In fact, brushing data from the dimension still focuses on the expression of “push configuration”, which is basically different from Tesla’s understanding and expression of “intelligence”.

Of course, within the window of constraints of laws and regulations, it is difficult for the market to really see which is better and which is worse.

However, if the intelligence represented by autonomous driving will eventually come to fruition, and it will take the lead in breaking through in the way of Tesla, it will drag down the process of the “new four modernizations” of my country’s overall automobile.

Figure: Visual Perception Display Figure, Source: Network

Figure: Visual Perception Display Figure, Source: NetworkThe penetration of electrification mainly relies on the objective law of manufacturing capacity expansion, and the cycle is long. We can still rely on the large market and industrial system to effectively catch up or even gain a first-mover advantage. However, intelligence will be different from the process cycle of automation. Once intelligence starts to be implemented, especially the pure visual solution that is more cost-effective for bicycles, it will siphon all dividends in the short term, and it will also firmly grasp the future to promote networking and sharing. initiative.

This means that whether it is for brand car companies, suppliers, or national competition based on the automotive industry, winning automation is only a battle to upgrade, and intelligence is the high ground that covers the entire new energy vehicle war. Battles are of strategic importance.

For this reason, we should not be satisfied with the first expression of automation on a global scale, while intelligence is bound to the industrial system. We should follow the example of Tesla, or at least bet on pure vision solutions, so that automatic driving can fully Possibly “decoupling” the constraints of the hardware dimension.

In the next window period, only BYD, which has the largest production capacity and sales volume, can leverage the maximum utility lever of the “intelligent” label in the short term.

04

realistic choice

One is that BYD is the only profitable new energy vehicle company in China; the other is that years of electrification have made it the electric vehicle company with the most profound industrial chain in the world; the third is that its scale is not limited to the domestic market. , has become the representative of the most competitive new energy vehicle companies in my country – and the most critical element of the road to self-driving breakthrough is data, and more data.

But as we all know, BYD’s intelligent performance lags behind the new domestic forces. To make up for this disadvantage, BYD has reached out to many rounds of suppliers in recent years.

The DiPilot assisted driving system will be launched in 2020. Bosch is the supplier of this L2 system, but there has been no update and iteration;

In 2021, BYD will launch its self-developed operating system, BYD OS, and begin to integrate its own supply solutions for autonomous driving assistance systems;

In the same year, BYD began to invest in chip supplier Horizon, lidar supplier Tengjuchuang, and autonomous driving solution provider Momenta;

In 2022, BYD will cooperate with Baidu to provide ANP (Urban Intelligent Assisted Driving Products) and Baidu Maps, and announced that it will cooperate with NVIDIA, a supplier of autonomous driving chips, and will use NVIDIA’s autonomous driving platform in the future. After that, BYD also cooperated with Huawei. Huawei’s MDC computing platform and autonomous driving solutions will also be introduced.

Figure: Display of BYD’s cooperative suppliers in the early days, source: Internet

Figure: Display of BYD’s cooperative suppliers in the early days, source: Internet  Figure: Early media evaluation of BYD Han, source: Internet

Figure: Early media evaluation of BYD Han, source: Internet  Figure: BYD models are in automatic parking, source: Internet

Figure: BYD models are in automatic parking, source: InternetObviously, the strategic purpose of casting a wide net is to make future products competitive in the intelligent dimension. It seems that multiple bets are foolproof, but in the long run, such an operation is too passive, and it may be difficult to establish intelligent competition barriers in the future. . From electrification to intelligence, the value chain will inevitably shift to the latter. And once Tesla takes the lead in opening up the second line of autonomous driving, the sales advantage that BYD has just established may not be guaranteed.

Therefore, on the basis of maintaining its own sales advantage, covering Tesla’s intelligent development path is a reasonable option for BYD to compete in the next stage of industry competition.

Then the first step, what BYD has to do is to reserve and test full-stack autonomous driving solutions (including software algorithms, hardware configuration, data processing and other dimensions). The biggest question involved is how long is the intelligent window period for the automotive industry.

If there is no time limit, I believe that BYD will be able to achieve full-stack self-development through recruitment and R&D investment in the future, and assemble it on mass-produced vehicles, and then continuously improve its own assisted driving system performance and future autonomous driving through large-scale data “feeding” However, if Tesla single-handedly accelerates the time for the industry to enter the intelligent stage, then Tesla will once again be far behind BYD and achieve a larger-scale market harvest on a global scale. It is very likely to weaken my country’s discourse influence in the process of “new four modernizations” of automobiles.

In fact, this should not be a multiple-choice question. “High-end manufacturing” is an important positioning and identity label for China in the world economic system in the future. The automobile industry is undoubtedly the foundation for demonstrating this strategic positioning. Car companies must climb and stand on the heights of intelligent automobiles.

At this stage, companies participating in “intelligence” can be roughly divided into three categories. One is the relationship between Great Wall Motors and Momo Zhixing, which is an intelligent driving company independently incubated by large car companies, mainly providing intelligent driving services for the parent company’s models; The other is to enter the field of intelligent suppliers as a technology company, such as Baidu, Huawei, Pony.ai, etc., mainly to provide overall solutions to car companies; another is the electric pioneer car company “Weixiaoli”. “This kind of self-developed company.

From the perspective of company background, positioning, and operation, Xiaopeng Motors’ intelligent concept is a company relatively close to Tesla. However, this year, the market sales performance of its products has experienced a certain decline, causing it to start to fall behind significantly. Whether in the situation of the industry, market, capital, or public opinion, Xiaopeng is becoming more and more difficult.

In China, the intelligent tags on Xiaopeng Motors are highly accepted by the market, but unfortunately it is due to its brand price positioning and SaaS-like business model. But for BYD, which has rich experience in manufacturing and electrification, it is very suitable for the needs of future intelligence.

Although Xiaopeng Motors does not follow the route of pure vision, its full-stack self-developed self-driving system is very similar to Tesla’s. In the high-speed NGP scene, Xiaopeng adopts the strategy of high-precision map, but when entering the urban NGP stage, it will adopt a visual perception-based solution, and now Xiaopeng is also committed to opening up the three “high-speed, city, and parking”. This kind of driving system usage scenario, and truly achieve “end-to-end” one-piece system integration, which may require work similar to Tesla’s 2020 FSD code rewrite.

If BYD can form an in-depth cooperation with Xiaopeng, it will help BYD’s intelligent process to cope with the wave of intelligent automatic driving that Tesla may be the first to set off. But the premise is whether Xiaopeng can accept the situation of “making wedding clothes for others”.

Of course, another important option for BYD also includes Baidu. Baidu, which has been immersed in the field of autonomous driving for nearly 10 years, is considered to be the Chinese company that understands autonomous driving best. In particular, Baidu has more options for solutions, which itself is walking on two legs with vehicle-road coordination and vision.

The process of the “new four modernizations” of automobiles will inevitably bring about the reconstruction of the market structure, but it is also a process of sweeping the sand. And car companies are not always just a single competitive relationship. In the face of larger missions and responsibilities, forward-looking car companies need to reach a tacit understanding of competition and cooperation.

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: https://finance.sina.com.cn/tech/csj/2022-11-09/doc-imqqsmrp5452932.shtml

This site is for inclusion only, and the copyright belongs to the original author.