Original link: https://www.williamlong.info/archives/6827.html

![]()

On June 6, Apple held its Worldwide Developers Conference to launch Apple Pay Later for iPhone and Mac users in the United States. Customers can shop in four interest-free installments over six weeks through Apple Pay Later. This service will be based on Apple’s own Apple Pay payment. When paying with Apple Pay, in addition to the “pay in full” option, a “postpay” option has been added. Users can use Apple Pay Later at any store that supports Apple Pay. , the launch of this service also marks Apple’s official entry into the buy now pay later service market.

“Apple” is not fresh

Apple’s Buy Now Pay Later service is nothing new. On August 1, 2021, the US mobile payment giant Square announced that it would acquire Afterpay, an Australian buy-now-pay-later service provider, in a US$29 billion all-stock transaction. At the end of September 2021, Mastercard announced “Mastercard Installment” for the US, Australia and UK markets. In October 2021, Visa courted BNPL. According to research data, 18% of merchants currently offer buy-now-pay-later services.

SimilarWeb, a well-known digital analysis provider, released a survey result and found that the website conversion rates of merchants that provide BNPL and those that do not provide BNPL are 4.5% and 2.4% respectively, which is almost twice the difference. Under such a huge temptation, merchants will only take the initiative to cooperate with the BNPL platform to obtain greater benefits.

According to the survey results of CouponBirds, a coupon website, the three giant payment brands Klarna, Afterpay and Affirm have been warmly welcomed by cross-border merchants and consumers, showing explosive growth. At present, the three companies have a total of 729,000 cooperative merchants, an increase of about 235% compared with the data in 2019 before the epidemic; active users are 178.7 million, an increase of about 127% compared to 2019.

With this growth, some well-known international brands also quickly joined.

Gradually heating up “buy now, pay later”

The core of BNPL is installment payment, but the flexible way of charging interest is different from ordinary credit card installments. The accrued interest on credit cards makes it more expensive to buy an item. BNPL, on the other hand, allows users to make payments by dividing consumption into four instalments within six weeks without any additional interest or fees within the agreed-upon period. Compared with the cumbersome application and review process of the bank, BNPL is more convenient. Even people with financial problems can obtain the installment qualification through the quick registration method. Compared with the traditional payment model, the BNPL payment model brings more flexibility to consumers.

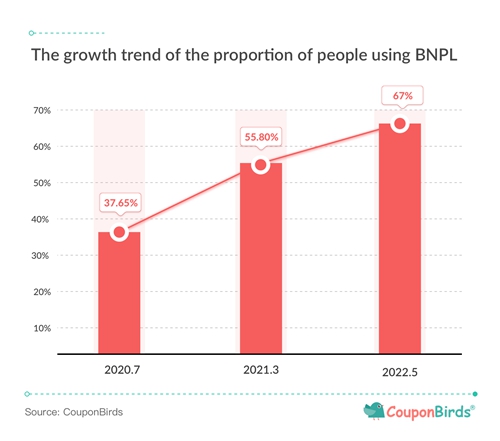

According to the survey data, the proportion of Americans using “buy now, pay later” services rose from 37.65% in July 2020 to 55.8% in March 2021. As of May this year, the proportion continued to rise to 67%. More than half of Americans have used the buy now, pay later service, a 50% increase in just eight months in the first phase. BNPL has not only ushered in a craze in business, but has also been popular with consumers.

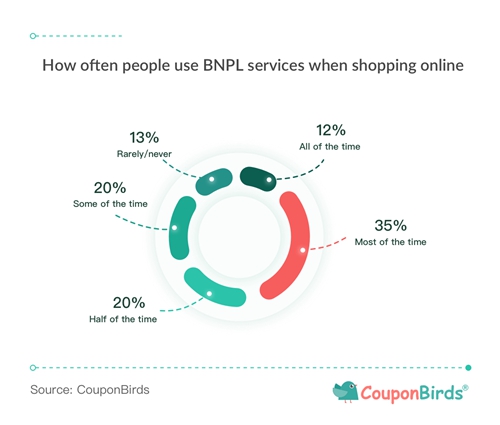

Of consumers using BNPL services, nearly 29% use it at least once a month, and 51% buy it now, paying every three to six months. More than two-thirds (67%) of consumers use BNPL at least half of the time when shopping online, with 12% using it all the time and 35% most of the time. And consumers who have never used BNPL services only account for only 13%, and more than half of such people say they will use BNPL in the next 12 months, so there is still room for rapid growth of BNPL services.

“Buy now, pay later”, enjoy 7 years in advance in China?

The buy-first-pay-later model has been popular in foreign countries in the past three or five years, but it has already become a part of people’s daily experience in China. Buy now, pay later. It is worth noting that the buy now pay later model is also developing rapidly in China. According to the latest survey released by research consultancy PayNXT360, China’s “buy now, pay later” industry is becoming the fastest growing market in the Asia-Pacific region, and is expected to grow by 51.3% year-on-year this year to reach US$82.78 billion. “The actual business scale of China’s buy now, pay later model may be far lower than the above estimate.” A domestic financial technology platform business director involved in buy now pay later service revealed to reporters.

In addition, compared with the European and American markets, the buy-before-pay service mainly solves the pain point of young people who are “unwilling to spend money” but want to obtain goods and services. China’s buy-before-pay service mainly solves the pain point of prepayment loss in certain industries. In the past, many Domestic users make large one-time prepayments in beauty, fitness, medical beauty and other institutions, but because these institutions “run away”, consumer rights and interests will suffer considerable losses. In this case, the buy-before-pay model can effectively help consumers avoid the risk of prepayment loss caused by the running away of institutions.

“Buy now, pay later”, as a new species of marketing increment, seems to be attractive to users at present, but whether the income of the product itself can maintain a healthy development, it will take time to observe.

“Buy now, pay later” is good, but it needs to be enjoyed with caution

With the launch of Apple Pay Later and the continued impact of COVID-19 on the global economy, more users will choose this payment method. The entry of any new product or new technology into the market requires a running-in stage, from savage growth to orderly prosperity. This is a necessary process. Although it is convenient to buy first and pay later, it is still similar to a credit card in essence, and the risks it faces cannot be avoided. ignore. This model is essentially a kind of excessive consumption, which will expand residents’ debt and prevent excessive surge in personal debt. There are still many things to avoid.

At the same time, the BNPL market also needs more reasonable planning and strict supervision. While the growth potential of the BNPL industry is undeniable, its potential impact on society as a whole is still worthy of market consideration. Some opponents worry that BNPL’s rapid growth will inspire unhealthy consumerism, while proponents argue that BNPL is a more sophisticated form of credit that can be used as an effective tool to help consumers manage cash flow. With “buy now, pay later” expected to become the most common payment method in addition to digital wallets, credit cards, debit cards and bank transfers by 2024, the market for an emerging payment method such as BNPL should not be underestimated.

Source: Reader Contribution

This article is reprinted from: https://www.williamlong.info/archives/6827.html

This site is for inclusion only, and the copyright belongs to the original author.