(The picture comes from the subgraph network)

(The picture comes from the subgraph network)Welcome to the WeChat subscription number of “Sina Technology”: techsina

Original title: Jingdong Cloud is standing still

Text | Hernanderz

Source: Value Institute

On November 1, JD Cloud held the 2022 City Summit (Shanghai Station). At the meeting, Gao Liqiang, vice president of JD Group and president of JD Cloud Business Group, released a series of new strategies and the achievements of JD Cloud in the past period.

Gao Liqiang said that JD Cloud will continue to penetrate into ten major industrial scenarios, including transportation and logistics, digital smart sources, digital smart retail, auto services, central state-owned enterprises, digital smart finance, industrial interconnection, rural revitalization, zero-carbon parks and cities, to serve corporate customers. Create more efficient industrial clusters and digitally-intelligent supply chains.

Data shows that in the past year, JD Cloud has served more than 95% of large state-owned enterprises, nearly 100 cities, 2,048 large enterprises, 914 financial institutions and more than 2.07 million small, medium and micro enterprises. The strategy of focusing on industrial scenarios has brought great benefits to the group. Over 110% performance growth. Especially in industrial scenarios such as logistics and services, JD Cloud has a certain share advantage and is not afraid of competition with other competitors.

However, there are many challenges in front of JD Cloud.

Alibaba, Tencent, Huawei, Baidu and other giants have long regarded cloud computing as a key project, and have used years of investment in exchange for a solid “four clouds” status. Even the young ByteDance made a high-profile move to the cloud last year, and fully entered the IaaS market through products such as Volcano Engine. It’s not too early to start. JD Cloud, which has been showing Buddhism in the early years, may have missed the opportunity to enter the game.

It will not come to the cloud business until 2022. Can the Buddhist JD Cloud still get a piece of the pie from Ali?

The development process has twists and turns

JD Cloud will no longer lie flat

The current embarrassing situation of JD Cloud seems to have been foreshadowed from the very beginning.

Insufficient mobility and slow start are the first problems encountered by JD Cloud.

In 2011, the number of users of Dropbox, which was less than four years old, exceeded the 50 million mark, becoming the hottest emerging unicorn in Silicon Valley and making the front page of Forbes magazine that year. Liu Qiangdong, who is thousands of miles away, was inspired by this technological unicorn nicknamed “Treasure Box”, and first came up with the idea of making a cloud disk – which is also the predecessor of JD Cloud and JD Digits.

It is a pity that it has been five years since Liu Qiangdong’s cloud disk business went from budding to taking root, and then to the brewing of the new business of JD Cloud. In 2012, Jack Ma, who was inspired no earlier than Liu Qiangdong, established the Alibaba Cloud Independent Business Group.

At this time, the second problem comes: the positioning is not clear, and the early “green leaf” attribute is too obvious.

In 2016, JD Cloud was officially established and was positioned as the “fourth carriage” of JD after e-commerce, logistics and financial technology. But at this time, Jingdong Cloud has a clear “supporting role” attribute, and has been making wedding dresses for e-commerce, finance and other businesses. The two products of basic cloud and data cloud and the four solution services of e-commerce cloud, industrial cloud, intelligent cloud and logistics cloud, which were launched for the first time, are all tailor-made for JD.com’s original e-commerce and logistics business.

In recent years, it was the heyday of e-commerce promotion activities such as 618 and Double 11, and JD Cloud still had many opportunities to show its face. During 618 last year, 100% of JD.com’s orders were transferred to the cloud, the peak value of access per second increased by 223% year-on-year, and the access bandwidth increased by 140% year-on-year, but JD Cloud still withstood the pressure.

However, at this time, JD Cloud has missed the first wave of growth dividends in the domestic public cloud market, and the wishful thinking of using the opportunity of e-commerce promotion festival to increase its popularity and attract external customers has not started.

Finally, and the most important issue, is the word “change”: from management to business, JD Cloud seems to be changing all the time, but it has not found the right path and lacks long-term strategic planning.

In the first two years of its establishment, JD Cloud focused its efforts on building a technical team and cloud base. In just two years, the size of the team has tripled. As of 2018, the number of registered users of JD Cloud was only 330,000. In the V4.0 service launched that year, JD Cloud provided 108 products for 10 industries.

At that time, in addition to providing technical support for JD’s e-commerce, retail, and logistics businesses, JD Cloud successively established partnerships with SOHO China, Kingdee Software, and Huobi.com this year, taking a key step in external expansion. Shen Yuanqing, president of JD Cloud Business Unit, said confidently at the time that although JD Cloud entered the market late, the advantage is that the market has already received education, and JD Cloud has gone to a higher level as soon as it enters the market.

“For the business of cloud computing, JD.com must do it, and it has the ability to do it, with a high probability of success.”

Unexpectedly, just one year later, the founding team of JD Cloud has undergone major changes: He Gang and Shen Yuanqing left one after another, and there was even news that JD Cloud was going to merge with Kingsoft Cloud. Later, the merger rumors went unresolved. In March 2020, JD Cloud and JD AI Division were integrated. The three major businesses of JD Cloud, JD AI, and JD IoT were merged into JD Zhilian Cloud, and the management team also underwent major changes again.

Zhou Bowen, then president of JD Cloud and AI Division, said that JD Zhilian Cloud was established to improve the competitiveness of JD Group in the technical service sector. The positioning is the same as when JD Cloud was first established in 2016. In other words, after years of tossing in the middle, JD Cloud has been standing still, going around and back to the original point.

By March 2021, JD.com announced that JD Cloud and JD AI will be fully divested to JD Digital, with a total transfer value of 15.7 billion yuan. JD.com, a subsidiary company, also took advantage of the trend to manage the three businesses of cloud, AI and financial technology in a unified manner.

Judging from the development process since its establishment, the above three major problems have successively caused JD Cloud to miss the opportunity to enter the game, fail to seize market dividends, and cannot find its own positioning, which has caused it to fall behind in the cloud battle of Internet giants. Now that we are catching up, we can see that JD Cloud still has no impact on cloud computing business.

It’s just that the industrial scene is only now starting to work, will it be a little late?

Bet on Industry Cloud

Can JD.com shake the “four clouds” pattern?

According to media reports, Liu Qiangdong has repeatedly emphasized at internal SEC strategic executive committee meetings that what Amazon and Alibaba have, Jingdong also has.

Looking at JD.com’s current business map, e-commerce and retail include a series of sub-projects such as JD.com Main Station and Jingxi. The logistics and big health sectors have long been self-reliant. Only in the cloud computing business, JD.com and Amazon and Ali are two old enemies. There is still a big difference.

Whether for the purpose of catching up with AWS and Alibaba Cloud, or for being optimistic about the prospects of the cloud computing industry, JD.com needs to strengthen this shortcoming.

From the perspective of the timeline, from about the second half of last year, JD Cloud gradually determined the strategic positioning of “industrial cloud”, focused on industrial scenarios, and successively launched a series of products and services. Gao Liqiang also bluntly stated at last year’s summit that it will take three years for JD Cloud to “become the strongest industrial cloud, the lowest carbon cloud and the most open cloud”.

On July 13, 2021, JD Cloud released the industry’s first hybrid cloud operating system “Cloud Ship” and seven basic technology products, and also put forward the slogan of “Building Four Strongest Clouds in Three Years”. In April this year, JD Cloud released a bulk commodity digital warehouse solution and a bulk industry chain upgrade plan.

According to the official introduction, the data processing capabilities and underlying technologies of “Cloud Ship” have been polished for a long time. JD.com’s 32 “Asia No. 1”, 1,000+ warehouses, over 200 industrial belts, and online commodity transactions and over 100 billion financial services are normal. The operation is inseparable from the support of JD Cloud. The new products with “Cloud Ship” as the core will focus on government and enterprise services, supply chain services, retail services and logistics services to provide support for external customers.

It is worth noting that at the JD Cloud Summit in the past two years, openness was the key word. Obviously, JD Cloud does not want to be only a subsidiary of JD.com, but wants to become an autonomous hematopoietic like AWS and Alibaba Cloud, and strive to compete for third-party users. Over the past year, JD Cloud has also reached cooperation with BTG Group, Country Garden, Beijing Academy and other customers to provide tailor-made industrial cloud services for the latter. The progress is visible to the naked eye.

However, is this enough for JD Cloud to catch up with Alibaba and AWS?

The answer, of course, is no – although China’s cloud service market has a bright future, the front-row seats have long been carved up.

According to the “Cloud Computing White Paper (2022)” issued by the China Academy of Information and Communications Technology, the overall market size of my country’s cloud computing market in the past year was 32.2 billion yuan, a year-on-year increase of 54.4%. Among them, the public cloud still occupies the main position, up 70.8% year-on-year to 218.1 billion yuan, which is the growth engine of China’s cloud computing market at this stage; the private cloud market also increased by 28.7% year-on-year to 104.8 billion yuan, breaking the 100 billion mark for the first time .

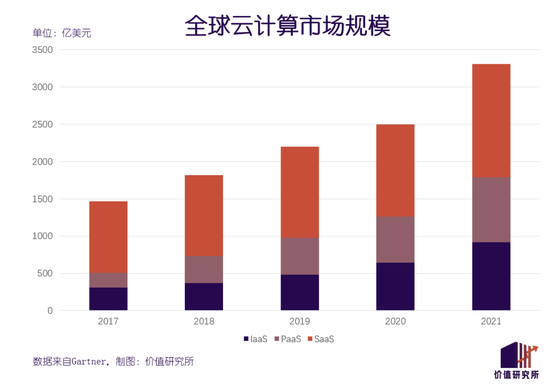

Looking at the global market, despite the uncertainty of the epidemic, the growth rate of the public cloud market bottomed out last year and even exceeded the level before the epidemic. According to data from Gartner, as of the end of last year, the global public cloud computing market size was US$330.7 billion, a year-on-year increase of 32.5%, and the growth rate reached a new high in the past five years.

From the perspective of market share, aside from Tianyi Cloud, which has a special background and is backed by China Telecom, Alibaba, which has a first-mover advantage, Tencent, which has been catching up after the major reform of its organizational structure in 2018, and has gradually matured in the past two years. Baidu and Huawei hold the majority of the market share.

Data shows that Alibaba Cloud occupies 34.3% of the public cloud IaaS market, while Tencent Cloud and Huawei Cloud account for 11.2% and 10% respectively. Baidu Smart Cloud also has obvious advantages in segments such as AI and edge computing, and its revenue growth rate of 55% is in a leading position among leading manufacturers.

In general, the “Four Clouds” have a solid status, and there is not much room for latecomers and marginal players. More importantly, none of these competitors have the advantage of JD Cloud; but there are too many alternatives in the market for the business JD Cloud is doing.

“Four Clouds” have their own advantages

What is the competitiveness of JD Cloud?

At first glance, the cloud businesses of Alibaba, Tencent, Huawei, and Baidu are similar, and the entire track has already become a red sea, and growth is becoming more and more difficult. However, a careful analysis of its development history, business development and customer composition can still reveal that Alibaba, Tencent, Huawei, and Baidu all have their own unique advantages.

Alibaba Cloud: Self-developed core technology is the biggest trump card

The success of Alibaba Cloud is largely attributable to the development strategy centered on technology: including the elimination of the IOE architecture, the self-built “Flying” distributed computing operating system, the proposal of the “big and middle Taiwan” strategy, and the establishment of the Damo Academy. A series of measures have provided support for technological innovation.

The IOE architecture is relatively closed, and the problems of high disaster recovery cost, high operation and maintenance cost, and difficulty in rapid capacity expansion were quite obvious in the early years. Alibaba Cloud’s de-IOE strategy and the research and development of the “Flying” system are almost simultaneously carried out. The fully self-developed new cloud computing system has laid a solid technical foundation for Alibaba Cloud.

Of course, in addition to “Feitian”, Dharma Academy has also contributed to Alibaba Cloud’s innovations in underlying technologies and discussions on cutting-edge technologies. The “Pingtou Ge” chip self-research program has successively released a series of products such as Xuantie and Hanguang, and many papers have been selected by ISCA, which is already at the leading level in the industry.

During the epidemic, the medical AI technology of DAMO Academy was launched, and the new AI model covered all aspects such as admission diagnosis, detection, comparison, observation, etc., which improved the efficiency of patient diagnosis and treatment and provided great help in the early battle of the epidemic. In addition, there are also representative works such as a shared intelligent platform tailored for Ant Group, database encryption technology, and the first self-developed cloud-native database in China.

All in all, technology is the most important trump card of Alibaba Cloud, and the Bodhidharma Academy and the “Flying Sky” system are behind the scenes to maintain Alibaba Cloud’s dominance.

Tencent Cloud: Comprehensive Internet Service Ecosystem and To B Business Layout

Compared with Alibaba Cloud, Tencent Cloud started later, and there is limited room for breakthroughs in the underlying technology of the cloud. Technology is not Tencent’s strength, but at least it will not be a hindrance. The advantage of Tencent Cloud lies in Tencent’s strong Internet service ecology and huge B-side business layout. All sectors work together to maximize the influence of Tencent Cloud.

After the “930 Reform” that caused a sensation in the Internet industry in 2018, Tencent’s B-end “circle of friends” has continued to expand. Its industrial Internet strategy and digital assistant positioning allow Tencent Cloud to have a strong presence in front of various customers. Tang Daosheng, senior vice president of Tencent and president of the cloud and smart industry business group, once said bluntly:

“Jointly building an ecosystem is the only option for industrial development. The success of Tencent’s industrial Internet business is inseparable from the support of upstream and downstream partners.”

In the first two years of the reform, Tencent Cloud has vigorously developed more than 300 industry solution businesses and established cooperative relationships with leading companies in more than 20 industries. Customers who use Tencent’s cloud services get not only cloud services – but also the support of almost all Internet ecological products behind Tencent.

For example, the handheld flagship store jointly developed with Uniqlo has Tencent Cloud to provide cloud computing services, and at the same time directly connect to the WeChat applet. In addition, Tencent Cloud will also provide a series of additional products/services such as Tencent Classroom and Tencent Conference when developing customers in the education industry.

Tencent Cloud alone may not be that attractive. However, if you package WeChat, QQ, Tencent conference, Tencent documents and other “gift packages” at one time, I believe that not many companies can resist this temptation.

HUAWEI CLOUD: A powerful government-enterprise network

The success of HUAWEI CLOUD is largely based on Huawei’s strong customer connections – especially government and enterprise customers.

Official website data shows that HUAWEI CLOUD currently has more than 300 corporate customers around the world, including Shaanxi Coal Group, China Merchants Bank, China Life Insurance, FAW Group, Guangdong Rural Credit Bank and other large central and state-owned enterprises.

HUAWEI CLOUD is also well aware of its advantages. It has always been very knowledgeable about making use of its strengths and circumventing weaknesses, and has developed more customized services for core users in the finance, insurance, education and other industries. As early as May 2020, HUAWEI CLOUD released the “Government and Enterprise Strategy”, deploying projects such as local data centers for government and enterprise customers, HUAWEI CLOUD Optimus architecture, and HUAWEI CLOUD Stack, and launched a hybrid cloud zone.

Through the HUAWEI CLOUD Stack, government and enterprise customers can conduct full-cycle digital asset management, allowing historical data to be fully integrated into the cloud. For government and enterprise customers with a late start of digital transformation, a large amount of data processing, and a lot of confidential information, HUAWEI CLOUD’s exclusive customized services are very considerate.

Baidu Cloud: Specializing in AI technology to provide differentiated advantages

As for the relatively young Baidu Cloud – strictly speaking, it should be called Baidu Smart Cloud. From the name, you can see its differentiated route focusing on AI technology.

As early as 2020, Baidu CTO Wang Haifeng said that Baidu Smart Cloud will adhere to the integration route of intelligence and cloud, and promote the common progress of cloud technology and AI technology. There is even a saying in the industry that although other clouds also have AI technology capabilities, only Baidu Smart Cloud has the “AI gene”.

In terms of underlying technology, Baidu can’t compete with Ali, but compared with AI technology, Baidu also has nearly 10 years of in-depth accumulation: deep learning platform Fei Pao, Baidu Kunlun chip, as well as products and technologies such as voice, vision, knowledge map, and natural language processing. , all laid the foundation for the development of Baidu Intelligent Cloud.

Among them, Baidu Brain’s basic base flying paddle deep learning platform is my country’s first self-developed, fully functional industrial-level deep learning open source open platform, and has a complete developer ecosystem. The AI-Native cloud computing architecture first proposed by Baidu has already been applied in video cloud, blockchain and other fields.

At present, Baidu is still resolutely implementing the collaborative plan of AI and cloud computing, and has successively developed new projects such as virtual portraits. When Alibaba Cloud and Tencent Cloud are both taking the “big and comprehensive” route, Baidu Smart Cloud, which focuses on the AI industry, has undoubtedly found a way of differentiation.

Unfortunately, none of the above advantages JD Cloud seems to have. This is not only the punishment for Jingdong Cloud for missing the six-year golden development period, but also the resistance to its subsequent development.

write at the end

In early May of this year, it was reported that JD.com’s Hong Kong stock IPO plan may be shelved, because the regulators still have reservations about technology companies with strong financial attributes. You know, before that, Jingdong Technology had voluntarily withdrawn its application for listing on the Science and Technology Innovation Board. If the IPO plan to go to Hong Kong also fails, it will be a big blow to Liu Qiangdong, who is bent on harvesting the fourth IPO of JD.com.

Since the integration of JD Digits and JD Zhilian Cloud into JD Technology in January last year, JD has been striving to erase the financial color of this subsidiary, and put on a technology coat for itself by developing cloud services. However, from the perspective of the twists and turns of the IPO journey, or from the perspective of market share, the cloud business of JD.com is still far from Alibaba, Tencent and other big companies.

Focusing on specific industrial scenarios may not necessarily lead to a steady win, but it is definitely a reasonable choice for JD Cloud at this stage. Missing the opportunity to start, and the early development strategy has been changed many times, JD Cloud has a lot of homework to make up.

However, cloud computing has long been a battleground for major Internet companies. Knowing that there are tigers in the mountains, JD Cloud can only favor tigers.

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: https://finance.sina.com.cn/tech/csj/2022-11-02/doc-imqmmthc3032159.shtml

This site is for inclusion only, and the copyright belongs to the original author.