This article is from the WeChat public account: Core Things (ID: aichip001) , author: ZeR0, title picture from: Visual China

Semiconductor companies have just gone through a difficult year.

The new crown pneumonia epidemic ebbs and flows, the Russia-Uzbekistan conflict and the Sino-US technology game have not come to an end, the market has suddenly turned from a shortage of chips to an avalanche of prices, the stock prices, market value, revenue, and net profit of chip manufacturers have all fallen, and the EU and the United States have successively issued historic chip laws , the global upsurge of chip factory construction and expansion, and huge semiconductor mergers and acquisitions are mixed… A series of complicated and major changes made the past December 2022 extraordinarily extraordinary.

In 2022, it has already left a strong and colorful stroke in the long scroll of world semiconductor history.

Farewell to this turbulent year full of turmoil and pressure. The global semiconductor industry is still moving forward under pressure. Although the future is still full of uncertainties, the successive severe tests have brought too much Only by clarifying the context of key changes in the market, strategy, policy, technology, mergers and acquisitions, can we go through the cycle more steadily and wait until the turning point of recovery arrives.

The market value plummeted: the stock price fell for a whole year, and the stock market was so cold

The haze hangs over the semiconductor capital market in 2022.

From the beginning of the year to the end of the year, the total market value of most mainstream US stock semiconductor giants is declining.

Market value changes of 20 US stock semiconductor giants in 2022

As of December 30, among the top ten semiconductor giants in terms of total market value, 6 have shrunk by more than 40% , namely TSMC, the world’s largest foundry company, Intel, the world’s largest IDM chip maker, and 3 chip design giants. Nvidia, Qualcomm, AMD, and semiconductor equipment giant Applied Materials. The companies highlighted with a green background have seen a drop in market value of close to or more than 50%.

Other semiconductor equipment giants are also in trouble in the stock market. The market value of ASML, the overlord of Dutch lithography machines, and Lam Group, an American equipment giant, have shrunk by 33.22% and 43.89% respectively. Relatively speaking, the overall market value fluctuations of major analog chip manufacturers such as Texas Instruments, ADI, and ON Semiconductor are relatively small.

Among the new IPO companies, Mobileye, an autonomous driving computing company owned by Intel, has received the most attention. It landed on Nasdaq in the United States on October 26. This is the largest chip IPO in the US stock market in 2022. After listing, the market value of Mobileye has been rising all the way. On the first day, the market value exceeded 22 billion U.S. dollars, and it rose to 28.282 billion U.S. dollars by the end of December.

Among the domestic A-share listed companies, Fudan Microelectronics, the domestic FPGA leader, can be called “a little red among the green clusters”. From January to October, the market value rose steadily, and reached the highest market value of about 79.5 billion yuan on October 27, and then began to decline. , but by the end of the year, the market value was still nearly 40% higher than that at the beginning of the year.

Market value changes of 15 A-share semiconductor giants in 2022

Weil (OmniVision) , the largest image sensor chip company in China, and Sanan Optoelectronics, the largest LED chip manufacturer in China, have seen the most serious market value shrinkage. However, both companies will make breakthroughs in 2022. For example, Weil’s market share in the automotive CIS market will further increase, and San’an Optoelectronics’ Mini LED chips will be certified by Apple in March 2022, successfully entering the “fruit chain” .

Although the overall stock market is not good, the enthusiasm for domestic semiconductor IPOs has not diminished.

In 2022, domestic chip companies will continue to enter the capital market in batches, and many companies in the manufacturing, equipment, materials, EDA, CPU, baseband chips and other tracks will go public.

This year, the Science and Technology Innovation Board has produced a number of “first stocks” of chips, including “the first stock of baseband chips” Aojie Technology, “the first stock of charging pile chips” Dongwei Semiconductor, and the first stock of “fast charging chips” Yingjixin, “the first stock of car-gauge chips” Naxinwei…

However, it is a little regrettable that BYD Semiconductor, which had received much attention before, failed to succeed in its IPO in 2022, and announced on December 30 that it would terminate the spin-off and listing.

Changes in the market value of 20 A-share semiconductor IPOs in 2022, incomplete statistics

At present, among the top ten market capitalization companies on the Science and Technology Innovation Board, the 6th to 9th are all semiconductor companies, namely Haiguang Information, the leader of domestic x86 CPU, SMIC, the leader of domestic wafer foundry, Montage Technology, the leader of domestic memory interface, and domestic power IDM. Leading China Resources Micro. Among them, Haiguang Information is a rare semiconductor IPO with a market value of 100 billion in 2022.

Some companies that are on the key domestic alternative track are still in the lineup for the Science and Technology Innovation Board, including wafer foundry companies such as Huahong Grace, SMIC, and Jinghe Integrated, and semiconductor material suppliers such as Zhongxin Wafer. Semiconductor equipment suppliers such as Tang shares, Zhongke Feice, Jingyi Equipment, etc.

Market reversal: the industry has entered a severe downturn, and the decline in revenue and profits is difficult to slow down

The chart compiled by Objective Analysis based on the data of the World Semiconductor Trade Statistics Organization (WSTS) shows that from 1976 to 1996, the average annual growth rate of the global semiconductor market was as high as 22%, but in the past 20 years, this figure has dropped to 3.9%.

The average annual growth rate of the global semiconductor market has dropped to about 4% in recent years (Source: Objective Analysis)

WSTS lowered its forecast for the growth of the global semiconductor market in 2022 and 2023 twice in September and November. It is estimated that global semiconductor revenue will reach US$580 billion in 2022, and may drop by 4.1% to US$557 billion by 2023.

Things change so fast. In the first half of 2022, chip customers who are deeply involved in the “chip shortage tide” are still worrying about tight production capacity. Trends such as chip hoarding and order rush buying have driven the number of orders and prices of core manufacturers in the upstream chip industry chain to skyrocket, and key components and raw materials are in short supply. It also brings out the order backlog and revenue deferred.

In the second half of the year, the topic of “chip shortage” came to an abrupt end, and the shortage of supply turned into excess inventory, and many consumer-grade chip quotations avalanche. The sudden drop in market demand and frequent supply chain interruptions caused by the new crown epidemic have not only disrupted the production rhythm of upstream suppliers, but also caused some speculators who stock up and speculate chips to suffer a lot.

As the largest sub-industry of semiconductors in the world, memory chips are especially “hardest hit.” As the consumer electronics market fell into a cold winter, the performance of memory chip giants declined sharply. According to TrendForce, a market research organization in Taiwan, China, the prices of DRAM and NAND Flash are expected to decline quarter by quarter throughout 2023. The double-digit decline may end in spring and reach the lowest level by the end of the year.

Due to a certain delay in the transmission of changes from the downstream market to the upstream, the third quarter of 2022 has become the “last glorious period” of many upstream chip suppliers. Pessimism has shrouded the financial report forecasts of various semiconductor manufacturers. The visibility of market demand is very low, and the imbalance between supply and demand will not recover until at least the second half of 2023.

Despite the sudden chill in the market in the second half of the year, benefiting from the benefits brought about by the shortage of chips in the first half of the year, my country’s chip design industry will still maintain a high-speed development trend in 2022.

According to the forecast of the IC Design Branch of the China Semiconductor Industry Association, the number of domestic chip design companies will be 3,243 in 2022, a year-on-year increase of 15.4%, and the growth rate will drop slightly; among them, 566 companies are expected to have sales of more than 100 million yuan. 37% increase.

Growth in the number of domestic chip design companies from 2010 to 2022 (Source: ICCAD)

Save money for the winter: The pressure to cut orders spreads to the upstream, and major manufacturers have cut expenditures one after another

After the sudden cooling of demand in the consumer electronics industry, the chip semiconductor industry quickly entered a period of severe recession. The major chip giants are very vigilant and have begun to prepare and implement measures such as layoffs and capital expenditure cuts to deal with this round of down cycle.

In August 2022, according to CCTV Finance reports, the mobile phone chip giant Qualcomm is experiencing order cuts and has reduced orders for its flagship mobile chip Snapdragon 8 series by about 15%, and will reduce the price of two flagship mobile chips by about 40% by the end of the year; Samsung Efforts are also being made to clear inventories to reduce the impact of weakening demand for consumer electronics on memory chip shipments.

Capital expenditures of memory chip giants have become more conservative. SK Hynix warned that major adjustments to capital expenditures in the new fiscal year are “inevitable”; Samsung is still trying its best to keep capital expenditures stable. Capital expenditures for the fiscal year are expected to decrease by 30% year-on-year, and 10% of the workforce has been announced.

In terms of chip manufacturing, Intel was reported by foreign media in November to implement a temporary suspension strategy for its manufacturing business. Up to 2,000 employees in its Irish branch will receive three months of unpaid leave. In December, it was revealed that it planned to lay off hundreds of workers in California. Employees; GlobalFoundries, the largest foundry in the United States, announced that it will lay off nearly 800 people worldwide in December, accounting for about 5.7% of GlobalFoundries’ 14,000 employees worldwide; Quarterly reduction of 15%, capital expenditure has been tightened accordingly.

Despite the chill in the semiconductor industry, given the cyclical nature of the semiconductor industry, demand will eventually rebound and long-term growth prospects remain strong, so most chip giants are still ramping up research and development in advanced technologies despite their decision to tighten their purse strings investment.

“Supply cut-off” upgrade: The United States has increased its pressure on China, and the heart hurts a lot under the “decoupling”

2022 may be the most critical year of global semiconductor policy changes in history, especially for the United States.

The U.S. government regards China as a threat. For the sake of its so-called “national security” and “the largest possible lead”, the U.S. government continues to tighten policies, pursue technological hegemony, and impose layers upon layers of export control rules to prevent Chinese companies from producing advanced chips. And more Chinese companies were included in the entity list, causing many American suppliers to suspend sales and services to Chinese companies.

The “Technological Iron Curtain” imposed by the United States is triggering a chain shock effect. China is not only the world’s largest semiconductor importer, but also has accelerated its market share in new energy vehicles and other markets , and such markets have a very strong demand for semiconductor chips. If we forcibly follow the “decoupling” route, it will only hurt both sides.

The U.S. government is still coercing allies to “stand in line” and form a chip four-party alliance (Chip4) ; and is trying to lobby Japan, the Netherlands and other countries that occupy the core voice of global semiconductor materials and equipment to impose export restrictions on China.

As the “decoupling” of technology continues to escalate, the US’s review pressure on chip exports to China has also spread to Israel, the “Second Silicon Valley”. Some Israeli semiconductor companies face potentially large revenue losses and layoffs due to new U.S. export controls.

Although we hope that the US-China relationship can be further eased, thereby reducing the pressure on Chinese chip companies to a certain extent, we can no longer have illusions or flukes—the US government is not only very likely to continue to expand the scope of its “chip allies”, but also More drastic measures are highly likely in other tech areas.

Self-control is the only long-term way.

Policy incentives: Chip bills are being promoted in many places around the world, and the manufacturing industry is being restructured

In recent years, the U.S. government has continued to use “sabotage and delay” methods to deal with China’s rise in the semiconductor field. This has also caused a serious impact on the mutual trust of the global chip “circle of friends”, and countries have gradually become skeptical of cooperation and interdependence. .

High concerns about backward competitiveness, supply chain vulnerability and dependence have prompted decision makers in many core regions of the semiconductor industry around the world to issue the latest semiconductor regulations, including providing incentives such as huge subsidies and tax breaks, and actively attracting advanced manufacturers in the industry. Its local investment and construction of factories.

In February 2022, the European Commission officially announced the “European Chips Act”, planning to invest more than 43 billion euros to boost the European chip industry; then the “American Chips and Science Act” (CHIPS Act), which was revised for more than two years, was officially announced in August. Promulgated, it promised to directly subsidize US$52.7 billion for semiconductor manufacturing and research.

The Mexican federal government has also begun to draft a new incentive plan, hoping to use its geographical advantage close to the United States to strengthen its semiconductor supply chain and attract semiconductor investment, especially in assembly, testing and packaging. The Canadian government has also announced that it wants to provide incentives for new investment in chip design, manufacturing and key materials.

Japan’s incentive strategy is to invest in local companies while attracting overseas giants to build factories. Internally, Japan promoted eight Japanese companies including Toyota, Sony, and Kioxia to jointly establish Rapidus, a new wafer company, aiming to achieve mass production of 2nm and below chips around 2027; externally, Japan invited TSMC, Micron Technology, etc. to build Advanced logic chip factory, memory chip factory.

Taiwan, China has also just passed the revised draft to encourage innovation in the chip industry. It plans to invest in forward-looking innovative research and development and advanced process equipment, and each will give 25% and 5% investment tax credits. 50% of the tax paid.

The United States, Europe, etc. promote the “return” of the chip manufacturing industry. Although it is expected to enhance the resilience of the local supply chain, it may also push up the cost of chip production. Zhang Zhongmou, the founder of TSMC, once publicly stated that the cost of chip manufacturing in the United States is 50% higher than that in Taiwan, China.

Expansion of production capacity: Global large-scale construction of factories, duo competing for hegemony at 3nm

With the release of incentives in various places, the world is setting off a new wave of semiconductor factory construction and expansion.

Europe is actively attracting international advanced chip manufacturers such as Intel and TSMC to build factories. As early as March 2022, Intel announced that its initial investment in Europe would exceed 33 billion euros, covering Germany, France, Ireland, Italy, Poland and Spain, covering the entire semiconductor industry chain. TSMC has also been rumored to have visited Germany and plans to discuss the possibility of setting up a factory in Germany in early 2023.

In addition to Europe, TSMC will fully launch plant expansion plans in the United States, mainland China, Taiwan and Japan in 2022. The process covers 28nm-5nm, including the construction of two 4nm/3nm fabs in Arizona, the United States, and the expansion in Nanjing, China. 28nm process capacity, the construction of fabs from 28nm to 2nm in Taiwan, China, and the joint construction of 22/28nm fabs in Kumamoto, Japan and Sony.

On December 7, 2022, a historic scene occurred in Phoenix, Arizona, USA: Zhang Zhongmou, Huang Renxun, Su Zifeng, Liu Deyin, Wei Zhejia and other most influential Chinese in the global semiconductor industry, together with Apple CEO Cook, US President Biden, etc. On the same stage, celebrating TSMC’s first US factory on the machine.

SMIC, the leading domestic wafer foundry, is also continuing to expand its 12-inch and 8-inch production lines. In the next 5 to 7 years, there will be a total of about 340,000 new 12-inch production lines.

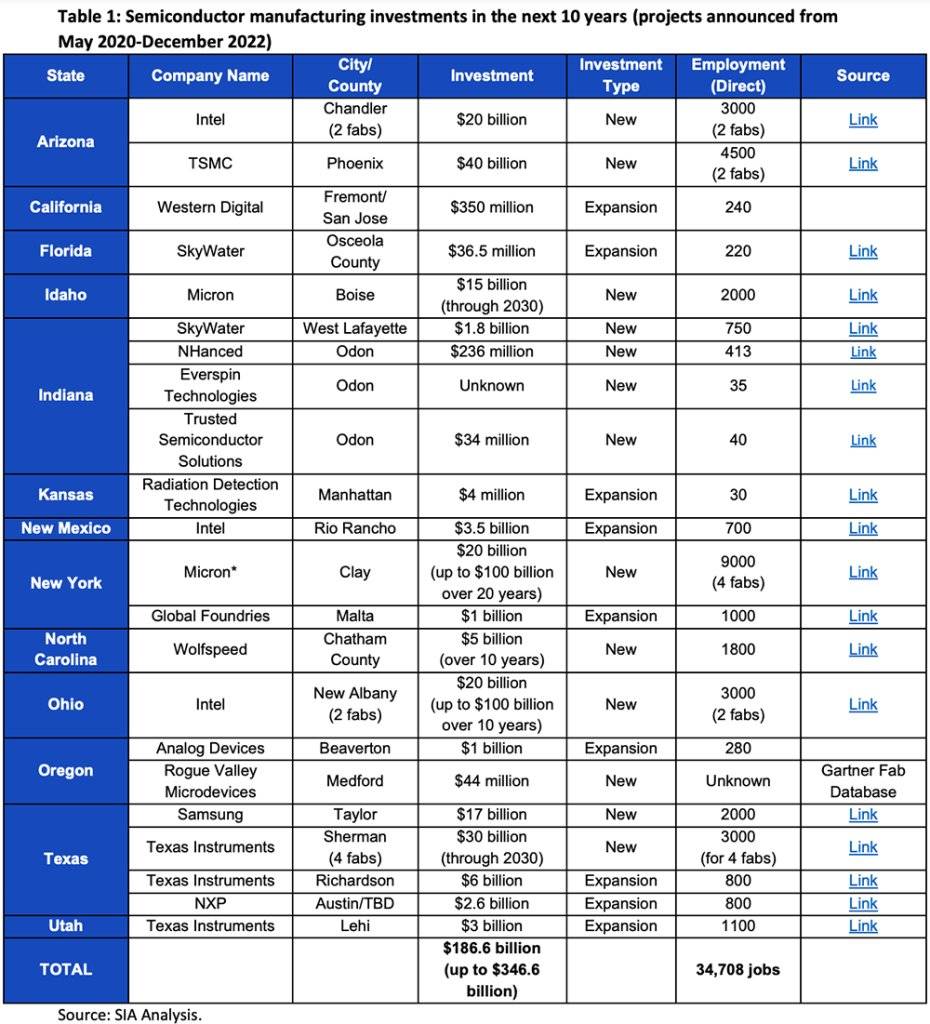

According to the disclosure of the US Semiconductor Industry Association (SIA) , driven by the chip bill, more than 40 new semiconductor ecosystem projects have been announced across the United States, including the construction of 23 new chip factories, the expansion of 9 fabs, and investment in the construction and supply of chip manufacturing. Facility of materials and equipment used. A total of 186.6 billion US dollars of private investment.

U.S. chip manufacturing investment over the next 10 years – projects announced from May 2020 to December 2022 (Source: SIA)

Semiconductor materials and equipment investment in the United States in the next 10 years-projects announced from May 2020 to December 2022 (Source: SIA)

In June and December 2022, Samsung Electronics and TSMC respectively announced the successful mass production of 3nm. According to foreign media reports, a Chinese mining machine chip company will be the first customer of Samsung 3nm, but so far no mass production of its 3nm customers has been seen. TSMC 3nm has received orders from customers such as Apple, Qualcomm, AMD, MediaTek, and Nvidia.

Huge mergers and acquisitions: Nvidia’s acquisition of Arm fell through, and cross-border transactions were frequently blocked

Mergers and acquisitions and investment have long been high-frequency hot words in the semiconductor industry.

In 2022, there will be many huge mergers and acquisitions that have attracted the attention of the global technology circle. Some transactions have been successfully completed, some are still in the progress stage, and some have finally failed after several twists and turns.

Nvidia’s proposed $66 billion acquisition of Arm, which was opposed by regulators in many countries and many industry insiders, was finally announced to be terminated on February 8, 2022, and the listing process of Arm was announced.

Nvidia and SoftBank Announce Termination of Acquisition Transaction

In the same month, Taiwan’s semiconductor silicon wafer giant Universal Wafer’s plan to acquire the German silicon wafer manufacturer Shichuang also fell through because it failed to obtain the approval of the German government before the deadline.

Speaking of it, the German government’s review of cross-border semiconductor mergers and acquisitions seems to have become more stringent last year. In addition to Universal Wafer, the German government also blocked the acquisition of the FAB5 chip factory of Elmos in Dortmund, Germany by Silex, a wholly-owned subsidiary of China’s Sai Microelectronics Group, and another Chinese company’s investment in ERS electronic, a leader in semiconductor temperature management solutions. .

Wingtech’s wholly-owned subsidiary Nexperia Semiconductor’s proposed acquisition of NWF, the UK’s largest chip factory, also encountered obstacles. In November 2022, Wingtech Technology issued an announcement stating that the British Ministry of Business, Energy and Industrial Strategy required Nexperia to divest at least 86% of NWF’s equity.

In contrast, non-border mergers and acquisitions seem to be going more smoothly.

Still in February, AMD announced the completion of a $49.8 billion acquisition of Xilinx, the world’s largest FPGA company.

Intel plans to spend $5.4 billion to acquire Tower Semiconductor, Israel’s largest wafer foundry, and is expected to be completed in early 2023.

In addition to mergers and acquisitions of chip companies, some chip companies are also trying to expand their software capabilities through mergers and acquisitions. For example, in April 2022, AMD announced plans to acquire chip and software startup Pensando Systems for US$1.9 billion; in May, Broadcom announced that it plans to spend US$61 billion to acquire cloud computing company VMware.

Broadcom acquires VMware for about $61 billion in cash and stock

In China, M&A transactions in the EDA industry are relatively intensive. For example, Xinhuazhang announced in September the acquisition of Shunyao Electronics, a leading company in high-performance simulation software. .

There is also the much-watched Zhilu Jianguang consortium’s “acquisition” of the Tsinghua Unigroup transaction, which has finally come to an end-the 60 billion yuan fund for the overall restructuring of the Tsinghua Unigroup will be in place in March 2022, and the equity will be officially completed in July. Changes, the new Unisplendour is ready to go.

Trendy technology: China and the United States released the Chiplet standard, and chip “assembly” became a trend

In 2022, the two major chiplet technical standards of the United States and China will be officially released , which is of great significance for the system-level chip to break through the limitations of advanced manufacturing processes and continue to improve integration and computing power.

In March, Intel, AMD, Arm, ASE, Google Cloud, Microsoft, Meta, Qualcomm, Samsung, TSMC and other international chip and technology giants jointly released the universal chip interconnection standard UCIe 1.0; in December, China’s first native chiplet technology standard ” The group standard “Technical Requirements for Small Chip Interface Bus” was officially approved and released by the China Electronics Industry Standardization Technology Association of the Ministry of Industry and Information Technology. The standard was formulated jointly by Chinese integrated circuit related companies and experts.

Open Industry Interconnection Standard UCIe

Chiplets are usually translated as “chiplets” or “small chips”. Through the die-to-die internal interconnection technology, the bare chips that meet specific functions can realize chips with more functions or higher performance. Under the current technological progress, the chiplet solution can reduce the complexity of chip design and design cost, and will also greatly improve the yield rate of large chips, while reducing chip manufacturing costs.

Whether it is domestic or foreign-led Chiplet technical standards, the purpose is to promote the formation of a broad social division of labor for Chiplet architecture design chips, and to create a more comprehensive and open Chiplet ecosystem.

Such an “assembly” idea seems to be one of the hottest chip innovation methods in 2022.

In March alone, new flagship chip products from Apple and Nvidia have appeared one after another. Apple released the last core of its self-developed computer chip M1 series, the M1 Ultra, which “sticks” two M1 chips together based on a unified memory architecture, doubling each core hardware index.

Nvidia then brought the “strongest surface” data center GPU – H100 GPU series new products. In addition to releasing the H100, which is composed of two groups of symmetrical structures, Nvidia also released two Grace super chips, one of which is assembled by two CPUs, and the other is assembled by a CPU and a GPU.

The larger the chip size, the lower the manufacturing yield, and Chiplet and multi-chip packaging design can cleverly bypass such difficulties.

With the help of advanced packaging technology like “chip glue” and faster chip interconnection technology, these innovative methods can break through transmission bandwidth and delay bottlenecks, and further improve chip performance and energy efficiency.

Fighting against the car cloud: Giants bet on the car/cloud/metaverse, the three emerging battlefields are hot

Smart cars, cloud computing, metaverse and other fields are generating more vigorous demand for chips. Previously, many chip giants focusing on different tracks have gathered in these emerging markets with strong future certainty.

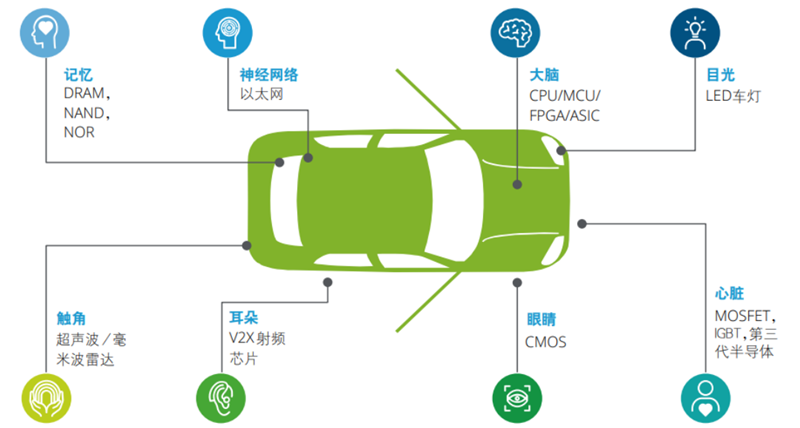

Electrification and intelligence are driving the rapid expansion of the automotive semiconductor market, and in-vehicle chips have become a battleground.

Distribution of automotive chips (Source: Caitong Securities)

In addition to STMicroelectronics, NXP, Microchip Technology, Renesas Electronics, Infineon and other automotive chip manufacturers, mobile chip giant Qualcomm, CPU giant Intel, and GPU giant Nvidia are also eyeing this promising market.

At the International Consumer Electronics Show (CES 2023) , the global consumer electronics vane that just ended, Qualcomm and Mobileye, a listed self-driving chip company under Intel, respectively set “small goals for 2030”: Qualcomm expects the total value of its automotive business orders to reach 300 Mobileye expects its advanced assisted driving ADAS business revenue to exceed $17 billion.

Nvidia, which contracted the mainstream autonomous driving computing market, announced another heavyweight product in September 2022-the new smart car chip Thor with a single computing power of up to 2000 TFLOPS, saying that it can simultaneously provide automatic parking, intelligent driving, Computing power is provided by multiple systems such as car machine, instrument panel, and driver monitoring.

In addition to cars, the cloud is also a high ground for chip giants.

In 2022, investing in cloud computing-based digital transformation strategies has become a key trend. It is not only a highly deterministic “second growth curve” for Internet giants, but also becoming a new growth pillar for computing chip giants such as Intel, Nvidia, and AMD. .

In recent years, Nvidia, Intel, and AMD have all taken the route of “heterogeneous computing” for cloud computing data centers.

Intel will launch the data center GPU Flex series in 2022, filling another piece of the puzzle of its XPU strategy; Nvidia will strengthen the “GPU+DPU+CPU” three-core strategy, and firmly sit on the dominant position in the AI training acceleration market; AMD will complete it in 2022 The acquisition of Xilinx, the world’s largest FPGA company, has CPU, GPU, APU, and FPGA product lines.

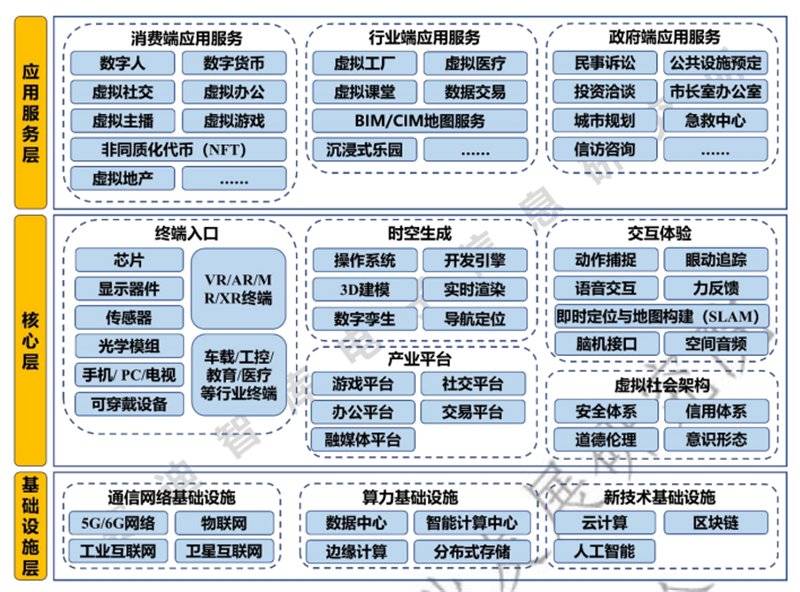

These chip giants have already extended their hardware and software layout to the fledgling Metaverse field.

A panorama of the Metaverse industrial chain (Source: China Electronics and Information Industry Development Research Institute)

Nvidia holds the “ace” software of the Omniverse real-time collaboration and simulation platform, lowering the threshold for building 3D virtual world content; Intel focuses on providing computing hardware such as CPU, GPU, IPU and software solutions such as oneAPI for Metaverse; Qualcomm focuses on the XR chip market , Cooperate with Microsoft, ByteDance, etc.; MediaTek has a layout in multiple fields such as multimedia, network connection, and mobile processors.

The value of the automotive and data center markets has been gradually reflected in the quarterly financial reports of these chip giants. Judging from the latest actions, their steps towards these emerging markets will only become more firm.

Epilogue: Rebuilding order from chaos in 2023

The global chip semiconductor industry is undergoing major changes. From the alleviation of the shortage of chips to the weak demand in the downstream market, the chip industry has entered a downward cycle. Various semiconductor companies have taken various measures to prepare for the ensuing challenges.

Entering 2023, the recovery of the chip market, the progress of local supply chain support in various countries, and the trend of the semiconductor technology game between China and the United States are expected to remain the focus of long-term attention of the global semiconductor industry.

The U.S. government’s “bullying behavior” to suppress China’s high-tech and chip industries may further intensify the impact of Sino-U.S. tensions on global chip companies and undermine the stability of the global semiconductor supply chain. From another point of view, this also pushes the “localization opportunity” to China’s local chip companies.

Breaking technological monopoly, strengthening technological innovation, and realizing self-control are commonplace paths that must be adhered to for a long time.

The road of localization replacement is bound to be bumpy and long, but some people insist on gnawing at the hard bone of deep replacement, starting from scratch, and then from having to excellent, passing the test of the market, can dilute the risk of being controlled by others for the future of China’s information technology industry .

Although the road is far away, the journey is approaching.

This article comes from the WeChat public account: Core Things (ID: aichip001) , author: ZeR0

media reports

Tiger Sniff Sohu Technology Sohu Sohu Technology

related events

- Chip change 2022 2023-01-11

- It is revealed that the A17 chip of the Apple iPhone 15/Pro series will pay more attention to battery life2022-12-30

- It is reported that Apple has slowed down the improvement of iPhone chips and is fully committed to Mac chips2022-07-04

- Apple and Intel will be the first to adopt TSMC’s 3nm technology

2021-07-02 - TSMC predicts that the global chip shortage may continue until next year2021-04-15

This article is transferred from: https://readhub.cn/topic/8mu8W1zOXMs

This site is only for collection, and the copyright belongs to the original author.