(1) The future downward loss is limited

Recently, the holding price of COSCO SHIPPING has indeed been falling. Many people think that in the future, COSCO SHIPPING will lose the excess profits it has earned so far. It is a company with a very high moat and in fact very low fixed costs.

Remark 1: We only discuss the international business of container shipping here, because COSCO SHIPPING Ports, which is responsible for port business, and Pan Asia, which is responsible for domestic trade, have been profitable for many consecutive years, and do not need blood transfusions from Haikong.

1. A low percentage of fixed expenses

In Haikong’s operating expenses, two parts are fixed expenses, and the other is depreciation and amortization. Here, it is also divided into two parts, and the other is the fixed depreciation of equipment. According to Haikong’s balance sheet estimates, it is about the depreciation and amortization of fixed assets. No more than 1.2 billion US dollars, and the amortization of right-of-use assets does not exceed 600 million US dollars; part of it is salary bonuses, which will not be issued for dozens of months according to the industry downward cycle, and the upper limit is 1.4 billion US dollars.

For these two parts, the cash expenditure shall not exceed 2 billion US dollars, and the calculated depreciation and amortization cost shall not exceed 3.2 billion US dollars.

Cash expenses only account for about 10% of operating costs in ordinary years, and costs after amortization of fixed assets only account for about 15% of total costs.

2. Variable costs are controllable

In the case of low fixed expenses, the main cost of shipping is closely related to the voyage of the shipping liner itself, that is, the cost of container handling and the cost of the voyage.

Analysis of container shipping is that this is a relatively rigid industry. In the past few decades, only the economic crisis in 2008 brought an 8-9% single-year freight drop, and other years remained stable or increased.

Under the condition that the demand will not plummet by tens of percent, the transportation price will not fall below the variable cost of the industry: the existence of the alliance is not to monopolize the route to increase the price, but to increase the price when the cargo volume cannot guarantee a high loading rate Under the common warehouse, the transportation cost is reduced.

When the freight rate falls due to insufficient volume, if the freight rate is lower than the variable cost, it will enter such a cycle:

Decrease in freight rates and variable costs -> liner companies reduce frequency and cost -> decrease in supply -> increase in freight rates to match demand

This will result in that the container shipping company can always take the initiative to adjust the supply to ensure the lower limit of the freight rate. Moreover, this will further enhance the competitive advantage of the alliance, which can reduce costs by co-storing while ensuring the route, while for the supply chain, when the freight rate of the main line is only 2-3% of the value of a single box of goods At the same time, ensuring the security of the supply chain is far better than tens of dollars cheaper (and the freight rate of 3% of the value of a single box of goods on the European and American lines also means that Haikong has an EBIT of more than 8 billion US dollars).

3. Industry losses are limited

In the history of the development of container shipping, it has always been a fiercely competitive industry, but we have also seen that industry leaders like Maersk and boutique transportation companies like OOCL are actually able to maintain profitability 95% of the time.

In the container shipping industry, the main reason for losses is large-scale investment. There are two ways to invest in shipbuilding losses. One is to buy second-hand ships on a large scale, and the other is to rent ships on a large scale.

The predecessor of Haikong, the main reason for the loss in the history of COSCO, is actually the same as the current ZIM, which originated from the large-scale and high-priced chartering of ships when the freight rate was rising. The impact of shipbuilding on EBIT is very limited, mainly due to the increase in interest costs; and high-priced chartering has a very serious impact on the company. Just like Yixing, the current book cash is 3.3 billion US dollars. However, with Star has an average of $4.3 billion in ship charter liabilities of $10/day/TEU, while the average cost of Haikong in the same period is only below $1.7/TEU/day. These leases are huge financial burdens once freight rates drop. The recent drop in freight rates and his high charter contracts have led to some operating losses on some routes, which explains why ZIM’s stock price has fallen rapidly.

MSC and CMA CGM purchased second-hand ships in large quantities. For example, Mediterranean Shipping purchased 4 Panamax container ships at 7 times the price . The second-hand ships were all fired to sky-high prices. These 4 ships have entered the end of their life cycles and are still sold. Arrived at twice the price of a new boat. This will lead to the calculation of the depreciation cost of ships in the future, the use cost of each ship will reach more than 5 times the depreciation of a single ship of Haikong.

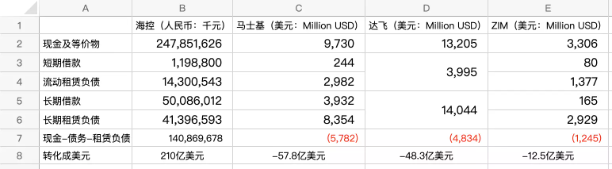

4. An extremely safe balance sheet

As mentioned in the previous chapter, the industry’s losses are all due to aggressive ship investment, which is reflected in the accounts as high right-of-use assets and lease liabilities. Compare the balance sheets of industry peers:

Perhaps because of aggressive chartering in the last decade, Haikong has neither purchased a high-priced second-hand ship nor renewed the lease of high-priced ships. The cash on the book can not only cover the liabilities, but also cover all the leases. Excluding leases, it still had $21 billion in cash after the half-year report.

And we have also seen that from Maersk, Dafei, to Yixing, these companies can’t even cover all ship charters to cash and equivalents, and these companies have all chartered ships in the past year and bought second-hand ships. , especially CMA CGM, which has increased its holdings of second-hand ships and chartered ships by more than US$9 billion in the past year and a half; at the same time, in the past year and a half, CMA CGM has increased its goodwill and port usage by US$5 billion through acquisitions in the past year and a half. Intangible assets such as rights assets.

To sum up, even if there is the most serious industry downturn, Haikong is still the best performer among all liner companies, and it is almost impossible to lose money.

In the next article, let’s discuss Haikong’s expected upper limit in the future.

There are 226 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/9070764642/231699022

This site is for inclusion only, and the copyright belongs to the original author.