Last Friday, ETFs got a big news:

ETFs are about to be included in the Internet Connectivity. Domestic investors can buy ETFs on Hong Kong stocks, and foreign investors can also buy ETFs on A-shares.

When I saw this news, the first thing that came to my mind was: I can finally buy ETF products in Hong Kong.

Although there are not many ETF products in the Hong Kong market (about 150, data source: Wind), there are some novel ETF products that can enrich the choices of mainland investors.

For example, some leveraged ETF products, or some products that track South Korea and Taiwan indices.

However, after I took a closer look at the access conditions, I found that things were not as good as I imagined.

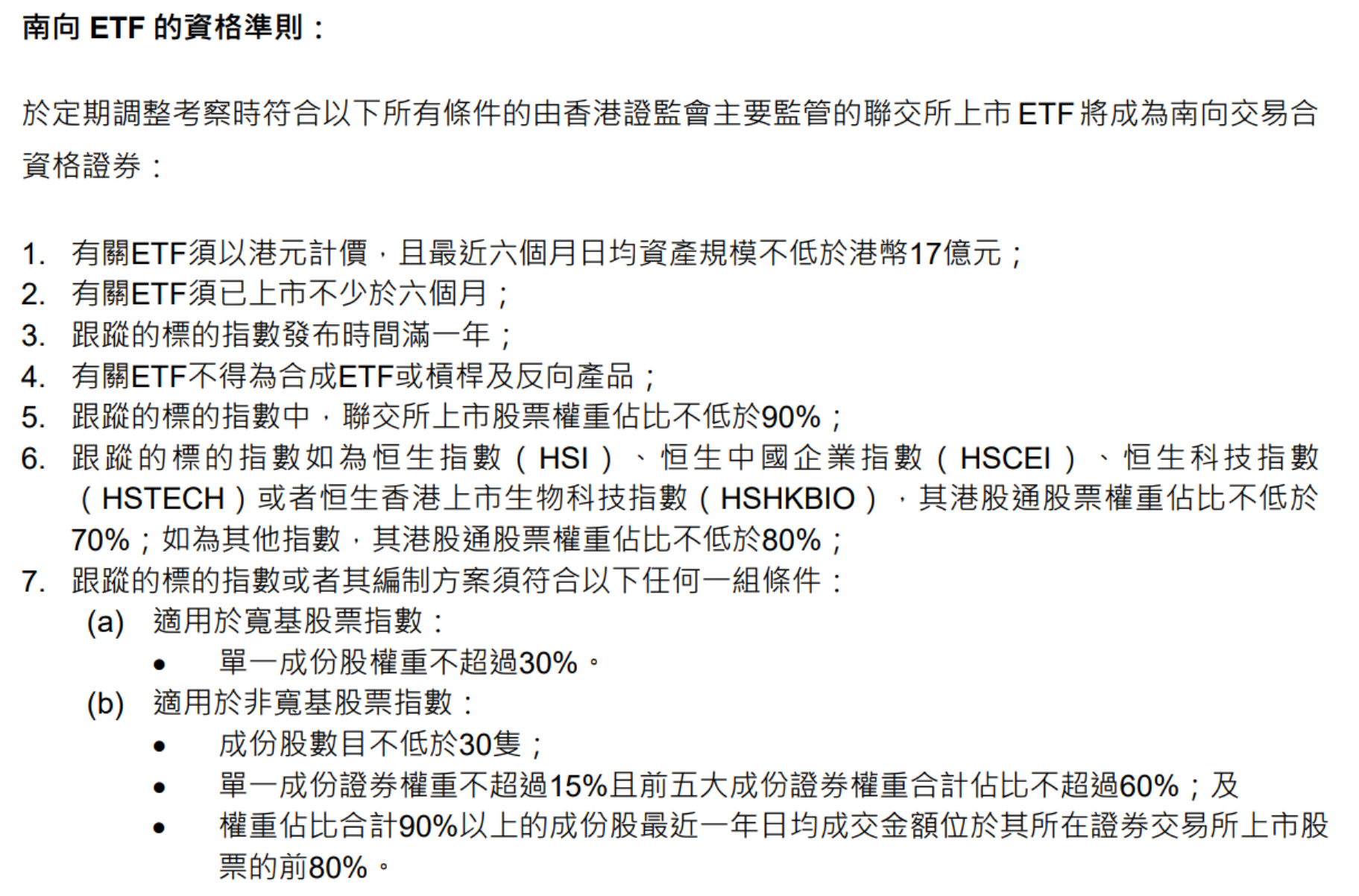

The first one has stuck most ETFs out the door.

At present, there are only 26 ETFs listed in Hong Kong with a fund size of more than 1.7 billion Hong Kong dollars. If you exclude the RMB share (-R) and the US dollar share (-U), there are only 14.

Looking further down, Article 5: Among the underlying indices being tracked, the stock exchange-listed stock revaluation ratio shall not be lower than 90%.

Most products can be excluded here: for example, A50 ETF products of managers such as Anshuo and Nanfang, which track the FTSE China A50 Index, Anshuo Asia Ex-Japan ETF that heavily holds TSMC, Samsung and other well-known Asian companies, and A-share new energy companies. The GX China Electric Vehicle ETF, the GX China Clean Energy ETF with heavy positions in the clean energy industry chain.

Coupled with some other restrictions, there are only a few Hong Kong stock ETFs that can be selected for interconnection:

The only bright spot may be the Transcript Fund (2800.HK).

This fund tracks the Hang Seng Index, and the fund rate is only 0.1%. In contrast, the largest ETF product tracking the Hang Seng Index in China is the China AMC Hang Seng ETF, with a comprehensive rate of 0.75%, which is still a lot worse.

For mainland investors, the benefits of Hong Kong ETFs being included in the Stock Connect are actually very limited:

1. Not enriching our portfolio.

2. Investing in ETFs related to Hong Kong stocks, A shares are more convenient than Hong Kong Stock Connect.

Therefore, even if the interconnection of ETFs is opened, it is difficult to increase the scale of funds going south.

However, for overseas funds, the inclusion of A-share ETF products in the interconnection is an absolute benefit.

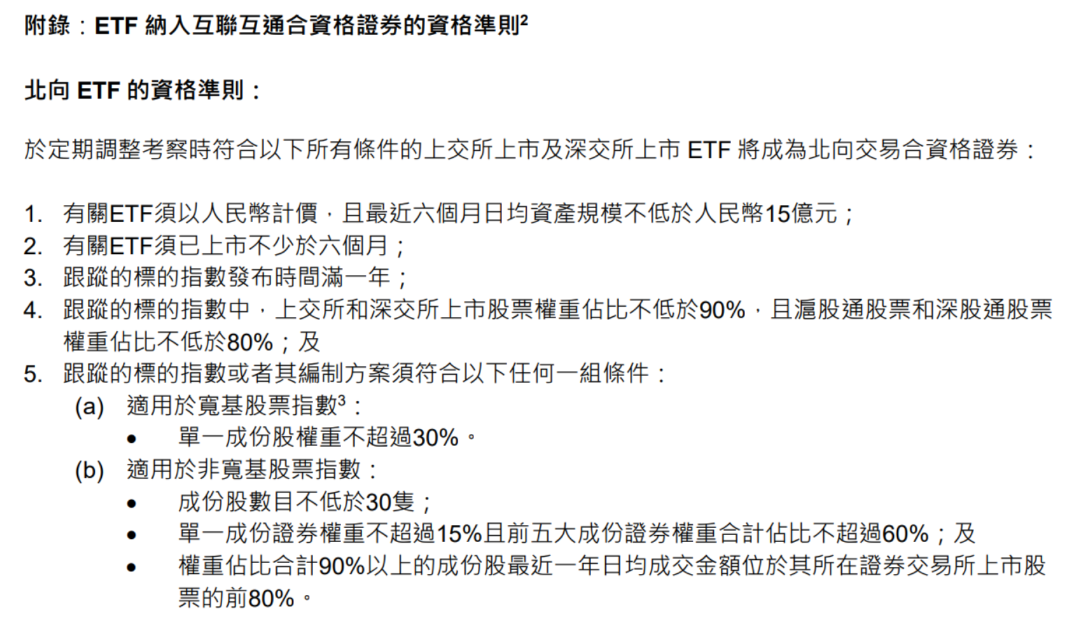

ETFs in the A-share market also have access conditions for interconnection. For example, the average daily asset size of ETFs is not less than 1.5 billion yuan. But this restriction is negligible for A shares.

As of the close of last Friday, there were more than 100 ETFs with a scale of more than 1.5 billion yuan in A-shares. Basically, the mainstream broad-based indexes and industry indexes of A-shares have related ETFs that can be included in the Hong Kong Stock Connect.

The most critical point is that although there are many products in A-share ETFs that track the Hong Kong market index, there are very few A-share ETFs in Hong Kong stocks, especially in some industries with A-share advantages.

It is very likely that after the liberalization of ETF interconnection, northbound funds will flood into those “core assets” in A-share ETFs.

For example, China’s high-end manufacturing of photovoltaics that go overseas is definitely an advantageous industry for A-shares compared to other markets.

However, there is only one ETF that tracks the domestic photovoltaic industry in the Hong Kong market, Southern China Securities Photovoltaic (3134.HK), with the latest scale of about 100 million yuan.

Although there are related products, the scale is too small and the liquidity is too poor, which is prone to tracking errors.

Another example is China’s long-term best-performing industry, the brewing industry. As of now, Hong Kong stocks have no related ETF products.

One more thing to say here, Penghua Wine, the most famous alcohol ETF in A shares, may not appear in the list of interconnection ETFs, because Penghua Wine’s holdings in Kweichow Moutai account for more than 15%, more than the single There is only a 15% access limit for individual stocks.

However, some consumer ETFs with heavy holdings of liquor can still be included in the Hong Kong Stock Connect, and they still belong to the core assets of A shares.

It seems that ETF interconnection is an “equal clause” between A shares and Hong Kong stocks, but in fact, the expected inflow of funds from the north will be far greater than the expected outflow of funds from the south. A-shares will also further “squeeze out” the liquidity of the Hong Kong market.

For domestic investors, although the interconnection of ETFs does not enrich the investment portfolio, the northbound funds attracted are still a positive.

It can not only improve the liquidity of the market, but also improve the valuation level of individual stocks.

In particular, some advantageous industries of A shares, including but not limited to photovoltaics, new energy, consumption and so on.

Original Misty Lee iETF Linghu Chong

@Today’s topic @snowball creator center @ golfer welfare

#InvestmentNew Trend! ETF interconnection is coming # #Emerging consumption recovers, what do you think of Hong Kong stock consumption#

This topic has 7 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/5223191485/221341676

This site is for inclusion only, and the copyright belongs to the original author.