1. Company Profile

Huaneng Hydropower is the second largest river basin hydropower development company in China. The actual controller is China Huaneng Group. It is mainly engaged in the development, investment, construction, operation and management of hydropower projects.

The company has the right to develop hydropower resources in the main stream of the entire Lancang River Basin, and is fully responsible for the construction and operation of the Lancang River Basin. It is second only to Yangtze Power and is a veritable second brother of hydropower. According to data , the Lancang River is rich in hydropower resources, with a total developable installed capacity of about 32 million kilowatts. At present, the installed capacity of the company’s hydropower stations is 22.95 million kwh. In the 2021 annual report, the power generation was 94.396 billion kWh, the revenue was 20.202 billion, and the net profit was 5.838 billion.

Why analyze Huaneng Hydropower? First, the main business of Huaneng Hydropower is hydropower business, and there are very few wind-solar hybrid new energy businesses. Therefore, it has the advantages of a hydropower company: the business model and financial report are simple and easy to understand, with few variables; high cash flow and high dividend; high certainty. The second is that Huaneng Hydropower is not as popular as Yangtze Power, and at the same time has better growth, and there are some new energy themes (the odds will be higher than that of Yangtze Power). Third, the share capital of Huaneng Hydropower is 18 billion, but only about 10% of it is actually in circulation, and the rest are held by the top ten shareholders. After deducting some long-term holding interest funds, the annual circulation is relatively small, and the stock price volatility is high. If you buy when the low valuation is strong, you may get a certain excess return.

Let’s take a look at the operation of Huaneng Hydropower in the past five years.

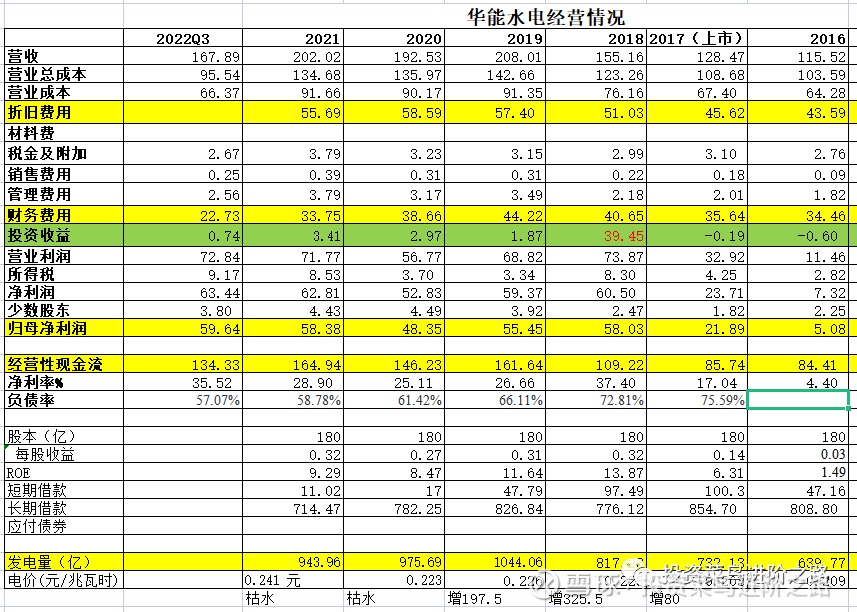

2. Business data analysis

It can be seen from the above table that depreciation and financial expenses account for about 65% of the cost, which is the core part of the cost of hydropower companies. The annual free cash flow is about 11 billion, and the operating cash flow is about 15 billion.

Because of the continuous reduction of depreciation expenses and financial expenses in recent years, the net interest rate is slowly increasing; at the same time, the debt ratio is also continuously decreasing, from 75.6% in 2017 to the current 57%. It is expected that the net interest rate will not change significantly in the next 2-3 years.

In 2018, the company sold 23% of the equity of its subsidiary Jinzhong Company, and obtained a transfer income of 3.676 billion yuan, which greatly increased its performance that year. After 2019, the company’s performance has tended to be stable, and the annual investment income has basically remained at around 200-300 million. Compared with the annual investment income of about 5 billion yuan of Yangtze Power, this is really insignificant.

2017-2019 is the peak period for the company’s hydropower stations to be put into operation, with newly added hydropower installed capacity of 800,000, 3.065 million and 1.975 million kilowatts respectively. At present, except for the Tuoba Hydropower Station (which is expected to be put into operation for power generation in 2024), the hydropower projects under construction have basically been put into operation, and the rest of the hydropower stations are still in the pre-construction or pre-planning stage.

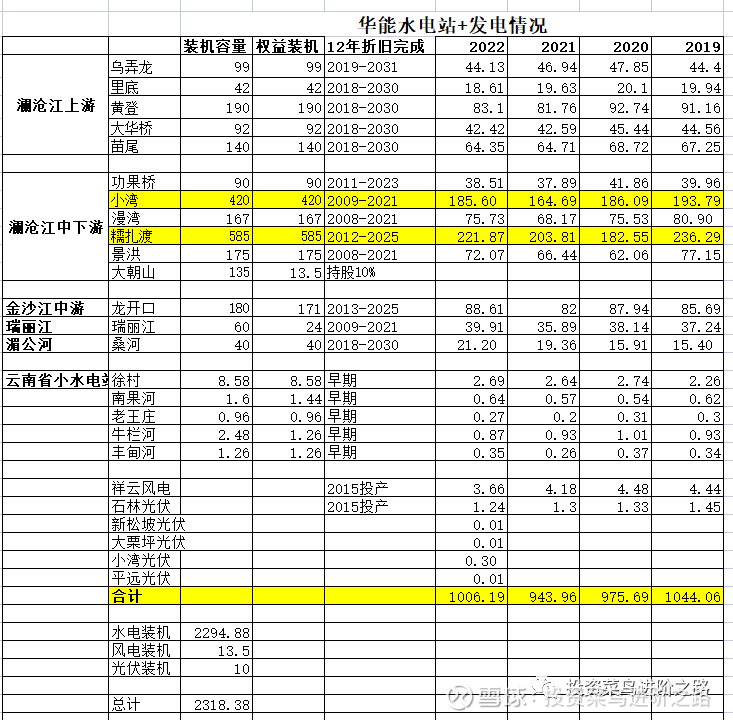

3. Hydropower station and power generation analysis

The performance of hydropower companies is mainly determined by the power generation, which in turn is determined by the installed capacity and the inflow of water in the year. Let’s take a look at Huaneng Hydropower’s installed capacity and power generation over the years.

At present, the installed capacity is 23.1838 million kwh, of which the hydropower installed capacity is about 22.95 million kwh. The Xiaowan and Nuozhadu hydropower stations have the largest scale, the highest water head, and the highest power generation efficiency. They can be said to be the basic assets of Huashui. Moreover, both power stations are multi-year regulating reservoirs, which have significant regulating functions and compensation benefits for downstream cascade power stations. Due to the dry season in 2020 and 2021, the power generation will be reduced. In other years, the power generation is basically stable at around 100 billion kWh. Two days ago, the company announced the power generation capacity of Huaneng Hydropower in 2022, with a total power generation of 100.619 billion kWh, a year-on-year increase of 6.59%, and on-grid electricity of 99.889 billion kWh, a year-on-year increase of 6.6%. It seems that the performance in 2022 will be stable.

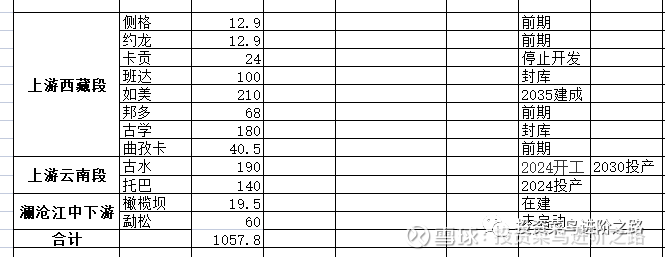

It can be seen from the above table that the installed capacity of the undeveloped hydropower stations of the company is about 10.58 million kwh. The closest to commissioning is the Tuoba hydropower station in the middle and lower reaches, with an installed capacity of 1.4 million kwh, and is expected to be commissioned in 2024.

Others are basically in the Tibet section of the upper reaches of the Lancang River, and are basically in the early stage of development. The key is that it is easy to build, the terrain is good, and the power generation conditions are basically completed. There are hard bones to gnaw at the back. The construction is difficult, the investment is large, and we can’t have too much expectation of the rate of return.

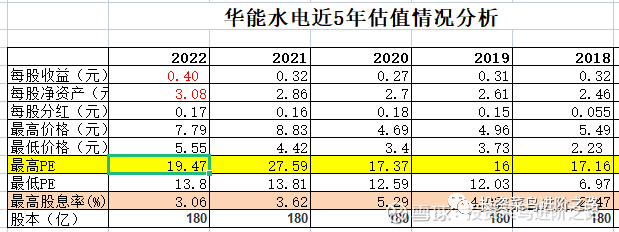

4. Valuation analysis

Let’s take a look at the valuation of Huaneng Hydropower in the past five years.

As can be seen from the above table, the valuation of Huaneng Hydropower is generally between 13-18 times PE . In 2018, it sold 23% of the equity of its subsidiary Jinzhong Company, and obtained a transfer income of 3.676 billion yuan, which led to a substantial increase in performance. At the same time, there was a trade war, which together led to a 7 times PE. Another analogy to Yangtze Power, therefore, we can be sure that 13 times PE is the bottom of Yangtze Power. As for the highest valuation, it is necessary to combine the market sentiment at that time. At the same time, because the market expects that Huaneng Hydropower will have better growth and has the blessing of new energy themes, the valuation should not be lower than that of Yangtze Power.

5. Anticipation and countermeasures

For Huaneng Hydropower, although there is an expectation of a substantial increase in the installed capacity of wind-solar hybrid new energy, we cannot have too much hope. For the time being, let’s value it according to the hydropower company.

The company proposed in the 2021 working conference: to fully realize the “4131” goal during the 14th Five-Year Period (2025). 4, means that the total installed capacity of the company will reach 40 million kilowatts in 2025; 1, means that the “14th Five-Year Plan” will increase the production of new energy exceeding 10 million kilowatts; 3, means that the revenue in 2025 will reach 30 billion; The latter 1 means that the operating profit in 2025 will reach 10 billion.

Let us analyze in detail whether the above objectives can be achieved. First of all, with an installed capacity of 40 million kilowatts, the current total installed capacity is 23.18 million, and the hydropower part is 1.4 million toba that will be put into operation in 2024, which is only 25 million. If 10 million of new energy is added, it will not be enough. There are only two possibilities, either Huaneng Group will inject its other hydropower stations into listed companies (similar to Yangtze Power’s acquisition of Wubai Power Station), or new energy will develop 15 million kilowatts of installed capacity. Let’s watch as we go.

At present, under normal water supply conditions, the company’s annual power generation capacity is 100-105 billion kWh. If the Tuoba Hydropower Station, which will be put into operation in 2024, is added, the annual power generation capacity will be about 110 billion kWh. In 2015 and 2016, due to the disorderly competition in the power market in Yunnan Province, the electricity price was too low, only 0.21 yuan/kWh, and it has been rising slowly in recent years, and it will be 0.241 yuan/kWh in 2021. In contrast, the electricity price of Yangtze Power is 0.2656 yuan, and there is still a big gap. The 2021 annual report shows that the company closely followed up the national and inter-provincial negotiations, and facilitated the signing of the “14th Five-Year Plan” cloud power transmission to Guangdong and Guizhou framework agreements, keeping the power transmission scale stable, and the price mechanism basically clear. Therefore, we can expect that electricity prices will improve to a certain extent. Of course, the expectations should not be too high. Let’s beat our heads and slowly increase by 1% every year. The revenue is about 1100*0.241*1.01*1.01*1.01=27.3 billion, plus 10 million kilowatts of new energy revenue of 2 billion to 3 billion yuan (235,000 kilowatts of wind and solar installed capacity in 2021, achieved 280 million revenue), achieved The probability of 30 billion revenue is very high.

The last is the operating profit of 10 billion, how much net profit will be generated. As can be seen from the above operating data table, the operating profit minus the income tax, and then deducting the profit of minority shareholders, is the profit attributable to the parent. Our gross estimated income tax is 1 billion, and after deducting the income of 500 million minority shareholders, the net profit in 2025 will be about 8.5 billion, supplemented by 15-18 times PE, and the market value will be about 110.5-153 billion. If the market gives 20 times PE, with a market value of 170 billion.

Let’s talk about the performance in 2022. The net profit from the first to third quarters was 5.964 billion, a year-on-year increase of 22.68%. The online electricity consumption in the fourth quarter of 2021 is 19.063 billion kWh, and the online electricity consumption in the fourth quarter of 2022 is 21.165 billion kWh, a year-on-year increase of 2.1 billion kWh. The annual net profit in 2022 is about 7 billion yuan, earnings per share is 0.4 yuan, and the probability of dividends is 0.2 yuan.

It is estimated that the earnings per share in 2023-2025 will be about 0.43 yuan, 0.45 yuan, and 0.48 yuan; the 3-year dividend will be about 0.6 yuan, and the stock price in 2025 will be about 7.2-9.6 yuan (corresponding to 15-20 times PE). If you buy it below 6 yuan, the three-year compound return will be 11.6%-20%.

The above is Xiaobai’s first analysis of Huaneng Hydropower. If it is inappropriate, please give advice from the bosses and friends of the official account.

$Huaneng Hydropower(SH600025)$ $Yangtze River Power(SH600900)$

There are 18 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/9185887755/239524288

This site is only for collection, and the copyright belongs to the original author.